Neometals (ASX: NMT) - Seals 50/50 Battery Recycling JV with Multinational

Interview with Chris Reed, Managing Director & CEO of Neometals Ltd. (ASX: NMT)

Neometals Limited is a mineral and advanced material company involved in the recycling, and production of high-grade lithium and vanadium. The company was founded in 2001 and is headquartered in Australia. Alphamet Management Pty. Ltd, Mount Finnerty Pty. Ltd., Reed Advanced Material Pty. Ltd., Mt. Edwards Lithium Pty. Ltd., Barrambie Gas Pty Ltd., and Inneovation Pty. Ltd (formerly Australian Vanadium Exploration Pty. Ltd.), are the companies' subsidiaries.

Matt Gordon caught up with Christopher Reed, Founder, CEO, and Managing Director, Neometals. Mr. Reed started his career in the mining industry in 1990 and co-founded Reed Resources in 2001. He is a member of the AusIMM (Australasian Institute of Mining and Metallurgy) and former Vice President of the Association of Mining & Exploration Companies. His educational background includes a Bachelor of Commerce degree from the University of Notre Dame and a graduate certificate in Mineral Economics from the WA School of Mines.

Company Overview

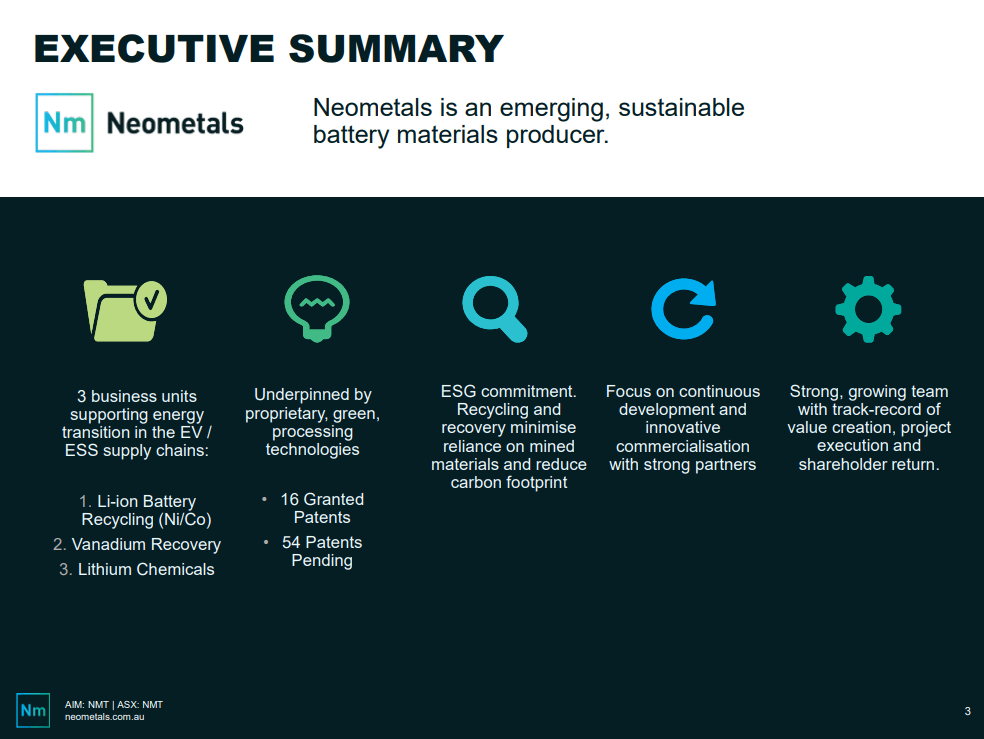

Neometals is an innovative mineral and advanced materials company focused on a sustainable future. The company seeks to de-risk and develop long-life projects with strong integrated partnerships throughout the value chain. The company was founded in 2001 and is headquartered in Australia. It is listed on the Australian Stock Exchange (ASX: NMT) and the London Stock Exchange’s Alternative Investment Market (AIM: NMT).

Neometals is a sustainable battery materials producer. According to the company, the current macro levels in the market are less than ideal. Recently, the company’s representatives were in London to conduct business and board meetings for Primobius GmbH. The company will also provide the latest updates to the shareholders at the AGM (Annual General Meeting). At Primobius, the company has started hiring additional staff. The head of recycling and head process engineers have relocated to Germany. Primobius is being built as a separate operating company, by putting all the necessary systems in place.

LICULAR GmbH is Mercedez-Benz AG’s recycling unit. It serves as a special-purpose recycling vehicle for the automaker. The Primobius JV (Joint Venture) is owned 50:50 by Neometals and SMS group GmbH, while LICULAR was founded for the specific purpose of running a consortia-based research program with Mercedes-Benz to develop a holistic and sustainable recycling approach for lithium-ion batteries.

Ongoing Operations

Neometals does not have an official listing on the German stock exchange. However, the company’s second largest group of shareholders is German. The Deutsche Börse has its own share register called Clearstream which Neometals uses to track the investments. According to the company, every announcement based around Primobius or Germany leads to a positive response from German investors. In fact, the investors turn over more stock than London.

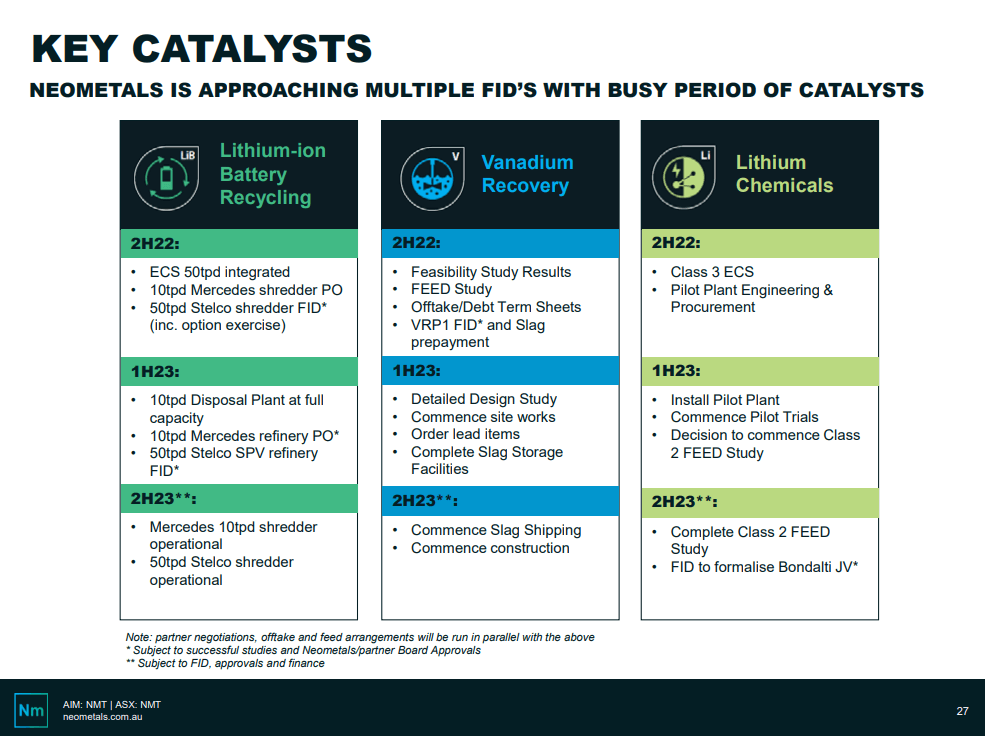

The company is scaling up operations at Hilchenbach. It is putting in a third shift. Dedicated trials are being run for Mercedes this week and the next. In the March quarter, the company will be offering Mercedes the spoke plant agreement, while the hub plant agreement will be offered in the June quarter. The company will commence construction on the hub plant in the second half of 2023. This would be a 10t spoke up to a 10t integrated plant. Following this, Neometals will start the R&D (Research and Development) collaboration with Mercedes Benz.

The company is currently working on the engineering for the 50t spoke plant, which is the next step in the process. At the same time, Stelco is running all of Mercedes’ commercial approvals. Neometals will offer Mercedes the plant supply agreement in the June quarter. This would trigger the 30-day window where the former will need to buy into the joint venture.

Financial Considerations

Currently, Primobius is generating small cash flows out of Hilchenbach. A 50% equity in the Stelco recycling joint venture, would lead to $50M, out of which $25M will be invested in the project over a 12-month construction period. Neometals has a strong cash balance in its current standing. The company is looking to maintain a strong balance sheet so that it can enter additional joint ventures over time.

Neometals is looking to fund the first spoke for the battery recycling plant through equity. It will generate sales out of the black mass, and the revenue will be invested in building the hub. Additional plants could be funded using debt. This financing strategy enables the company to minimize the technology risk.

Until the larger plants are up and running, the banks aren’t likely to take risks on a new technology for the first plant, at least until it operates at a steady state and starts generating a cash flow. From a theoretical perspective, the company is taking a 10t cash-generating business and making it into a 50t plant. Following this, the company intends on installing the integrated refinery to get the next step up and earning. This process would be replicated as required. The company anticipates that it would require funding around mid-2023.

Neometals’ investment strategy is based on the mine ranking and the return on invested capital. Within the portfolio, battery recycling offers the highest return on invested capital, followed by the vanadium recovery project as it is at a similar developmental stage. The company’s patented ELi lithium extraction process is expected to have a 2025-2026 FID (Final Investment Decision), which is a couple of years behind.

Based on the developmental strategy, the Barrambie project could enter production in 1-2 years. The project is in a similar stage as Widgie Nickel, where the company spinned-off its nickel assets into a separate entity. The Widgie Nickel asset has a fantastic base with mining leases in place. Notably, it required 2 years and about $20M to make it production ready. The asset had an entitlement issue, and the company decided to de-merge it, giving it a new life.

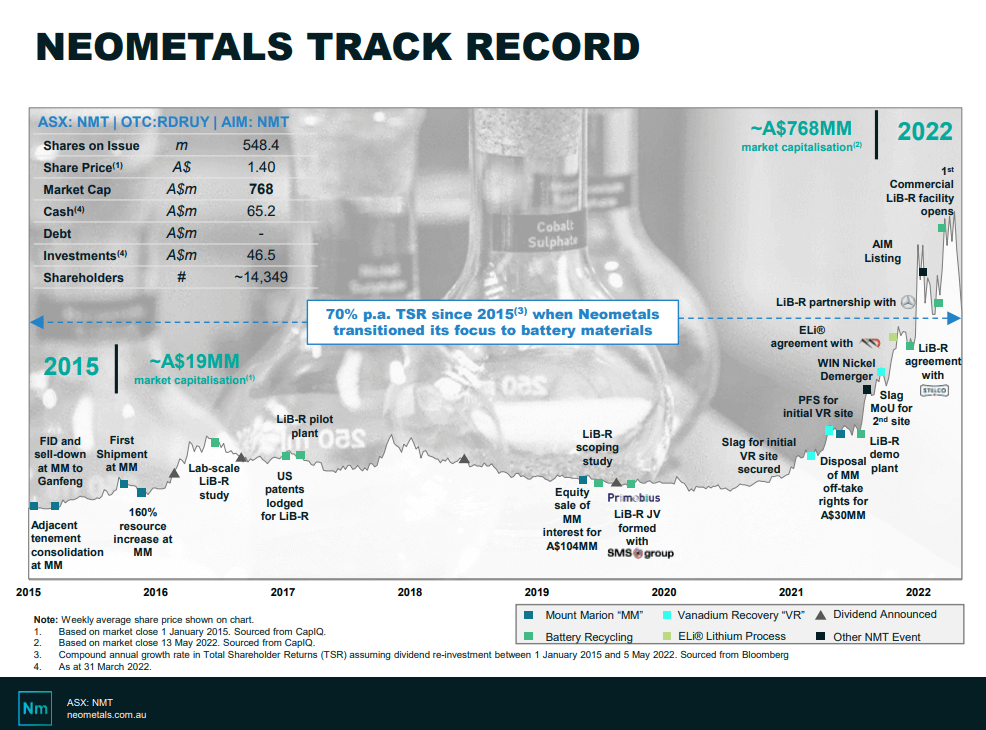

Neometals’ shareholders have been in a really strong position. The $0.20 investment hit $0.60 in 2022 and yesterday, it was trading at around $0.36-$0.37. According to the company, the Barrambie titanium and vanadium project is a fantastic asset. Euroz Hartleys published a strong research note estimating Barrambie’s value. The company anticipates that Barrambie could potentially be turned into Widgie mark 2.

The ELi lithium extraction is 2 years away from any big investment. The company is earning 50% on the vanadium recovery project. This is expected to crystallize soon. The investment decision is due on June 30th, 2023. The company has appointed debt advisors and an investment bank in Scandinavia. Both parties are working with the EIB (European Investment Bank) and NIB (Nordic Investment Bank) for the project funding process. This process will help determine the amount of equity that needs to be raised for the asset. This is a Scandinavian special-purpose vehicle for projects where battery material is produced from waste while carbon is captured and sequestered in the tailings. Europe and London offer a lot of green funds, debt, and equity.

From a technological perspective, Neometals is an early mover in the space. The company is working with different technologies which are going through the national phase of patents. It is in a very good position from an IP (Intellectual Property) standpoint.

The Competition

Neometals is seeking overlapping competition in the sector. According to the company, competition is needed to service the market. It is looking to ensure that people are always looking at lithium batteries as there are solutions available to recycle them and close the loop.

The current installed capacity for recycling through pyromet and hydromet in Europe is between 100,000t-110,000t, out of which 3,000t is hydrometallurgy. The company estimates that by 2026, the total addressable market would be around 350,000t. Unicore is looking to build a 150,000t capacity plant by 2026, while the Hydrovolt JV between Northvolt and Norsk Hydro is expected to have a 125,,000t capacity by 2030. Neometals considers these companies as genuine competitors. The major difference is that the companies are going into recycling as the end products can be used for their downstream business.

Umicore is the world’s best and biggest cathode producer outside of China. The company decided to enter the recycling business because, for each ton that isn’t gathered from recycling, the company needs to get to the market and fight for it.

Northvolt is a cell maker. To meet its ambitions, the company needs to enter the recycling business.

One of the unique selling propositions for Neometals is that the company has a plant builder as a partner that is looking to build bigger plants. The company will generate revenue at Hilchenbach, a project that is fully booked for 2023, corner-stoned by a German carmaker that’s not Mercedes. While the company will continue to process batteries from Mercedes, it also has batteries from all German carmakers at Hilchenbach.

The company is looking to provide a disposal service for smaller volumes. A cell maker can build a 50t per day plant in a joint venture. For plants that are significantly larger, the company has the option to choose the plant supply and licensing route. Neometals has designed the business in a way that it generates less money per unit of throughput, leading to an increase in volume that offers a strong return on invested capital. Every plant being built is principal, where Neometals will pay 100% of the CapEx (Capital Expenditure). For every joint venture, the company will need to put in half as much.

For the plant supply and licensing business, a 500t plant could require around $1Bn in CapEx, which would be too much off the company’s balance sheet. Instead, the company has decided to not put in any CapEx and generate revenue through royalties. The company has a number of royalties. A 10% GSR (Gross Sales Royalty) will be highly attractive for the company.

Currently, Neometals has 8 income streams. The top 5 in the basket of goods are nickel, lithium, cobalt, copper, and aluminum. These commodities can be hedged on the LME. A 500t plant for a carmaker will generate substantial royalties. The company has been successful in exploiting its exclusive access to the plants.

While the majority of the lithium producers are using pyromet for extraction, Neometals is utilizing hydromet. This gives the company a competitive advantage as hydromet offers better prospective recoveries and a lower carbon footprint. These aspects make for a stronger project from an ESG (Environmental, Social, and Governance) perspective.

The company acquired a green accreditation last month. The accreditation enables the company to gain better access to green funds as it now has a third-party endorsement for the business model. The company’s maiden MSCI ESG rating was based on the 2021 sustainability report. It received a maiden BBB rating. Based on the 2022 sustainability report, the company is looking for ways to get the rating upgraded.

Targets 2022 and Beyond

Neometals is currently focused on targeting customers. Car makers are likely to be 500t a day plant customers, while cell makers are likely 50t a day. Meanwhile, the waste aggregators offer a smaller daily volume. Over the next 5-7 years, the company intends to scale up operations from 10t to 50t and eventually 500t a day capacity. In order to achieve this, the company would need a hub. Every carmaker that takes a 50t spoke and a 50t hub would require a 500t plant in time for the end of life. This aspect is a major driver for prioritizing the order book.

In order to cover the US and European markets, the company chose the JV route. Stelco SPV is responsible for their sites and procuring the feed. Neometals formed a JV with Stelco to commercialize the operations in the United States. Neometals does not have a similar deal in Europe. Instead, the company has its own 10t plant and is looking at a 50t plant. The plant will only be built when a partner or a lucrative long-term contract is available for underpinning. It has received a lot of interest from cell makers, carmakers, and waste aggregators. The company has also been approached by battery material suppliers in Europe who are now looking to have a minimum recycled content in the batteries along with a lower carbon footprint in order to meet the customer demands. Mining companies are looking to become recyclers by selling recycled material to battery makers or through the supply chain. This makes the industry highly dynamic in nature.

Due to the battery regulations, every customer is looking for battery materials with carbon footprint information. This is because the battery makers and car makers are now required to put carbon footprint stickers on cells and cars. In Europe, cars and batteries need to have 10% recycled content by 2030. In order to achieve this target, every battery in Europe would need to be recycled. Furthermore, the recycled content requirements for batteries will double in 2035. This presents an unparalleled opportunity for market penetration. In Europe, by the end of 2030, there will be €600Bn worth of recoverable material in cells. This is equivalent to more than 300Moz of gold and each ton of these batteries is equivalent to 4oz/t to 5oz/t grades.

Since the material has already been extracted from the ground, the company simply needs to build plants to process them. The value of material sitting in the batteries is expected to grow to €100Bn per annum by 2030. The IRA in the US is offering grants and tax incentives for battery recycling.

Since the plants require a significant capital investment, Neometals decided to partner with SMS. Taking into consideration the number of electric vehicles that need batteries, between 10%-20% is scrap, serving as early fade for the 50t plants. The end-of-life batteries would work on a lag basis. While there are better mines in production, advancing to the next tier of operation, there’s very little involvement on the recycling end of the equation. As a result, the company decided to focus on recycling, recovering exotic materials from batteries, and processing them for reuse.

Recycling gives battery-purity grade products a second life, which results in an even lower carbon footprint and the lowest point in the cost positions. The scale of operations is a key factor here. The company is taking a cookie-cutter approach when it comes to building processing plants. SMS can build about five 10t plants in a year, or three 50t plants. A 500t plant requires a big CapEx spend, and SMS could potentially build one per year. Neometals has a fantastic partner that has 14,500 employees and production facilities across Germany, the US, India, and China.

If the company has 2 volume car makers, 1 volume cell maker, and some waste aggregators, it would need to build hubs and spokes followed by bigger hubs and spokes. Following this, the company would need to determine the build capacity. Even if the company achieves massive success, the penetration rate would be limited due to the massive size of the market.

Neometals is looking to commission a 50t plant in the June quarter. For each deal or a series of plants announced, there’s a value add-on for the company. The penetration rate for technologies can be typically defined by the total addressable market. The DCF NPV based on the announced plants is based on peer metrics.

The company is being covered by several analysts including Tyler at RBC, Trent at Euroz, and John-Marc at Cenkos. Looking at the 50t spoke, 50t hub, 500t spoke and 500t hub, it is evident that the 10t plants aren’t moving the needle in a significant way.

The plants can be valued on a 100% equity basis, and a few assumptions can help determine the value of the joint venture and Neometals’ equity. On the plant supply and licensing side, valuations can be made based on the 10% GSR. Big Mining companies trade on a P/E (Price/ Earnings) ratio. If the company is integrated and is producing battery chemicals, its growth is well into the double digits, about 10 or 20 times. Meanwhile, good royalty companies are 40 to 50 times or even up to 100 in a booming market.

Neometals is focused on getting a P/E by putting the earnings on the balance sheet and maintaining transparency. While Primobius is not consolidated, the performance and statement of performance or the P&L (Profit and Loss) and the balance sheet will appear on Neometals’ accounts as notes, similar to Mount Marion.

Future Outlook

Even if the world stops producing cells today, yesterday’s production will continue to go into cars and will come back in 10 years. This gives plenty of runaway for the company to continue the recycling business for decades to come.

The Gigafactories are lithium-ion based. The market is struggling to determine where the raw material for all the batteries will come from in the future. This is because the discoveries are getting harder each year.

The EU (European Union) battery regulations are focusing on mandatory recycling, and the US is expected to adopt a similar strategy in the near future. At Primobius, the company is looking at an endless loop where the recycled batteries will need to be recycled once again at the end of life. Lab testing for recycling recycled batteries is currently being carried out by the company and its partners. Each time a battery is recycled, it results in a lower carbon footprint, which leads to a much more sustainable end product.

To find out more, go to the Neometals website

Analyst's Notes

Subscribe to Our Channel

Stay Informed