Santacruz Silver Delivers Strong Q1 2025 Results Amid Operational Transformation

Santacruz Silver Q1 2025: Multi-metal producer reports $70M+ revenue, $27M EBITDA. Strong treasury position, debt reduction on track, operational excellence focus drives margin expansion.

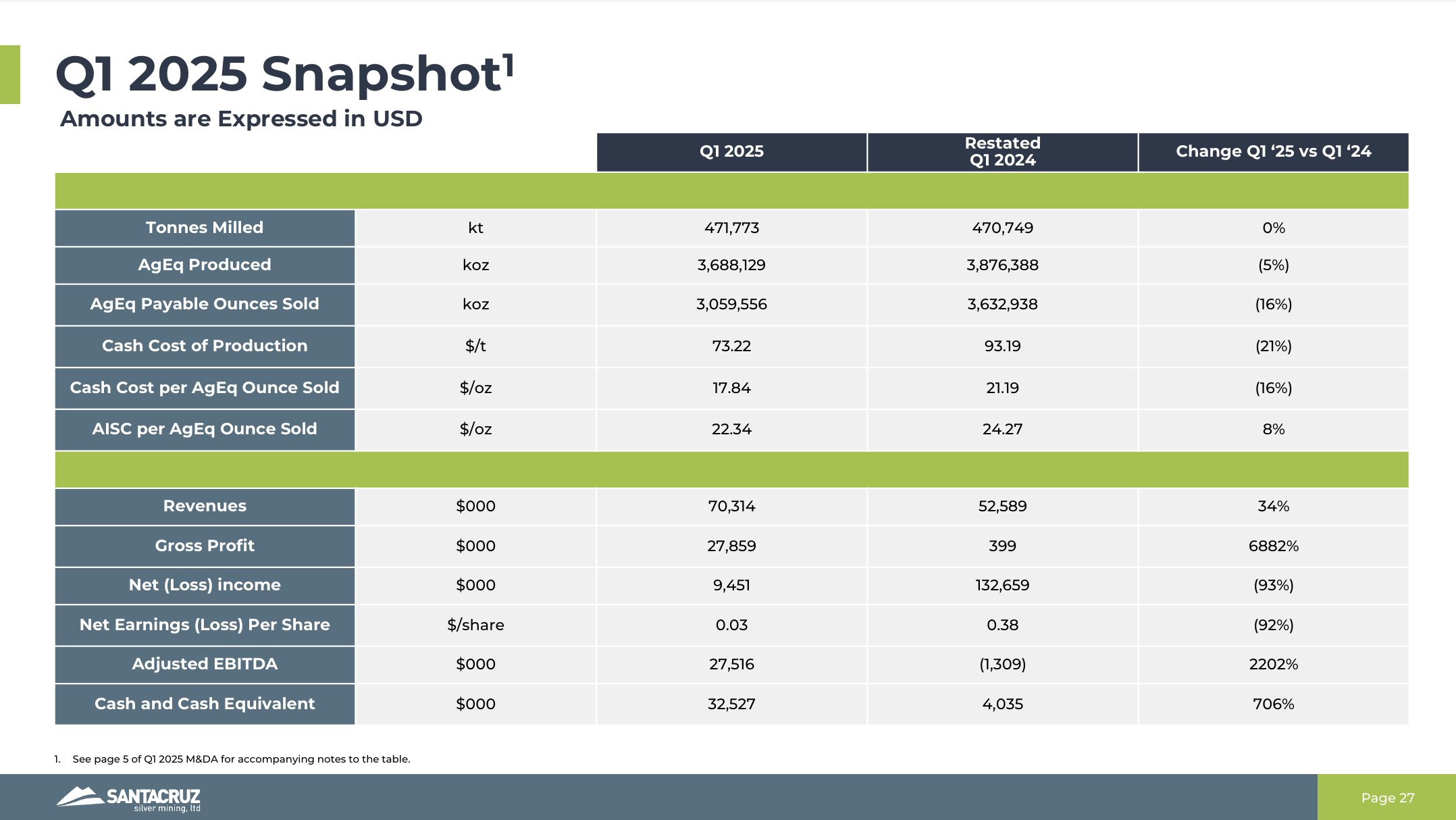

- Santacruz Silver reported revenues north of $70 million with EBITDA of $27 million, demonstrating significant operational improvement with gross profit up nearly 7,000% year-over-year.

- The company has paid down $17.5 million of its Glencore consideration, with $22.5 million remaining to be paid in three installments of $7.5 million each, completing by late October 2025.

- Significant capex deployment in Mexican operations, particularly at Level 960 of the Zimapán mine, with acquisition of 15+ pieces of underground equipment to enhance future production efficiency.

- Management expects all-in sustained cash costs to normalize to $22-23 per silver equivalent ounce across assets by Q4 2025, down from elevated Q1 levels due to equipment investments.

- Company maintains over $60 million in treasury with no immediate M&A plans, focusing on operational efficiency and building cash reserves while maintaining a $4 million annual community investment commitment.

Santacruz Silver Mining (TSXV:SCZ) has demonstrated remarkable operational transformation, with Executive Chairman and CEO Arturo Préstamo Elizondo highlighting the company's continued evolution from a struggling operation to a profitable multi-metal producer. The company's Q1 2025 results showcase the benefits of strategic investments made over the past 18 months, positioning the organization for sustained profitability as metal prices remain favourable and operational efficiencies materialize.

Financial Performance and Operational Metrics

The company's Q1 2025 financial performance represents a significant milestone in its operational turnaround. Santacruz Silver reported revenues "north of $70 million" for the quarter with EBITDA of $27.5 million, reflecting the company's successful transition to consistent profitability. The gross profit increase of nearly 7,000% year-over-year demonstrates the dramatic improvement in operational efficiency and the positive impact of favourable market conditions.

Préstamo attributed the strong performance to multiple factors:

"Metal prices is helping us indeed, and also we have a few things that contribute to our gross margins. One has been the result of previous year's investments into our mines which have improved our margins, definitely the metal prices today and also the exchange rate in Bolivia where the exchange rate has suffered a devaluation."

The Bolivian peso devaluation provides a structural cost advantage for the company's operations in that jurisdiction, with Préstamo noting this is "a chronical thing happening in Bolivia" that should remain beneficial "for many years to come."

Debt Management and Treasury Strength

Santacruz Silver has made substantial progress in reducing its debt obligations, particularly the Glencore consideration that has been a focus for investors. The company has paid down $17.5 million of the obligation, leaving $22.5 million remaining. Management has structured the remaining payments at $7.5 million bi-monthly installments, with the final payment scheduled for the last week of October 2025.

The company's treasury position provides confidence in its ability to meet these obligations while maintaining operational flexibility.

"Today our treasury is strong, we have north of US$60 million in our treasury, so we have no concerns about meeting our objectives of getting these payments done on time."

This strong cash position, combined with the structured debt reduction plan, positions the company to operate without financial constraints while building reserves for future growth opportunities.

Strategic Capital Investment Program

The company's capital allocation strategy focuses on maximizing the potential of existing assets rather than pursuing acquisitions. The most significant investment has been in the Mexican Zimapán mine, particularly the development of Level 960, which represents what management believes is "the future of this mine."

The scale of investment has been substantial, with the acquisition of over 15 pieces of underground equipment over the past year and a half.

"This quarter we have been investing a significant amount of capex in our Mexican mine especially through the acquisition of different underground equipment."

Level 960 currently contributes approximately 40,000 tons monthly out of the mine's total 75,000 tons per month throughput.

While this investment temporarily elevated all-in sustained cash costs (AISC) to $34.32 per silver equivalent ounce in Q1, management expects these costs to normalize as the equipment becomes fully operational and production transitions from development ore to stope ore.

Interview with Executive Chairman Arturo Préstamo Elizondo

Production Optimization and Cost Reduction

The company's production strategy is evolving from development-focused extraction to more efficient stope mining, which should significantly improve margins. Currently, most ore from Level 960 comes from development activities, which inherently have higher dilution rates and suboptimal recovery characteristics.

"Our objective is to have ore from stopes, fresh stopes that we are preparing as we speak by the end of this year, so at that moment you will realise a better all-in sustained cash cost.”

The target AISC for the Zimapán mine is $22-23 per silver equivalent ounce, expected to be achieved by Q3-Q4 2025.

The seasonal nature of production, particularly in Bolivia, affected Q1 results, with carnival celebrations and other cultural events impacting production rates. However, management expects production to normalize throughout the year, with Q4 traditionally being the strongest quarter.

Asset Portfolio Optimization

Santacruz Silver has implemented strategic operational changes to optimize its asset portfolio performance. The company reorganised its Caballo Blanco and San Lucas operations by moving the Reserva mine from Caballo Blanco to San Lucas processing facilities. This change addresses metallurgical challenges where "when you put Reserva mine into that ore, you depress the silver coming to the lead concentrate."

The reorganization has yielded immediate benefits, with Caballo Blanco maintaining the same production levels with only two mines that it previously achieved with three mines.

"This is a significant improvement and more silver reporting now to the lead concentrate which helps us significantly in terms of the economics."

The San Lucas operation serves as a strategic buffer, processing ore from small miners and providing flexibility when other operations face temporary challenges. This operation is expected to contribute approximately 1.2 million ounces of silver equivalent quarterly.

Resource Development and Exploration

The company maintains a disciplined approach to resource development, following a principle where the geology department should always maintain ore reserves at least 1.5 times the rate of mine depletion. This conservative approach ensures operational continuity while managing capital efficiently.

The Soracaya exploration asset represents a significant future opportunity, with a preliminary assessment indicating potential production of 4 million ounces of pure silver annually at full capacity of 800 tons per day. However, management is taking a measured approach:

"This year we're going to keep doing more exploration, more methodological work and we'll be very disciplined with the management of our treasury."

Community Investment and Social License

Recognizing the importance of community relations in mining operations, Santacruz Silver maintains a consistent commitment to social investment. The company allocates approximately $4 million annually to community development programs, focusing on education, infrastructure, and quality of life improvements.

"We definitely believe that we should contribute to those communities where we have operations going and it's important to make a significant contribution to the families and to the communities to improve their wealth and their life."

These investments include school improvements, teacher training, and infrastructure projects such as clean water systems.

The Investment Thesis for Santacruz Silver

- Operational Turnaround Complete: The company has successfully transitioned from struggling operations to consistent profitability, with Q1 2025 demonstrating sustainable cash generation capabilities and dramatic margin improvement.

- Strong Financial Position: With over $60 million in treasury and a clear debt reduction plan, the company operates without financial constraints while building reserves for future opportunities.

- Strategic Asset Base: Operations in Bolivia and Mexico provide geographic diversification, with the Bolivian peso devaluation creating a structural cost advantage for a significant portion of operations.

- Capital Efficiency Focus: Management's disciplined approach to capital allocation, focusing on optimising existing assets rather than pursuing acquisitions, should maximize returns on invested capital.

- Production Growth Potential: The Level 960 development at Zimapán mine and operational optimisations across the portfolio position the company for increased production efficiency and lower costs.

- Commodity Price Leverage: As a silver-focused producer (approximately 50% of revenues), the company benefits from silver price appreciation while maintaining diversification through zinc and copper production.

- Exploration Upside: The Soracaya project represents significant future production potential with 4 million ounces of annual silver production capacity, providing long-term growth optionality.

Macro Thematic Analysis

The silver mining sector is experiencing renewed investor interest as industrial demand for silver continues to grow, driven by renewable energy applications, electronics manufacturing, and emerging technologies. Santacruz Silver's operational turnaround coincides with this favorable macro environment, positioning the company to benefit from both improved operational performance and supportive commodity prices.

The company's geographic positioning in Latin America provides exposure to regions with established mining infrastructure while benefiting from currency devaluations that reduce operational costs. Bolivia's chronic currency weakness, as noted by management, creates a sustainable cost advantage for operations in that jurisdiction. Mexico's stable regulatory environment and supportive local communities provide additional operational security.

The focus on operational excellence rather than growth through acquisition reflects a mature management approach that prioritizes cash generation and balance sheet strength. This strategy should appeal to investors seeking exposure to silver production without the execution risks associated with development projects or complex M&A transactions.

It reflects a disciplined approach to value creation that prioritizes operational excellence and financial strength over rapid expansion.

Analyst's Notes

Subscribe to Our Channel

Stay Informed