.webp)

.webp)

New Gold Inc.

NYSE: CLOSED

TSE: CLOSED

LSE: CLOSED

HKE: CLOSED

NSE: CLOSED

BM&F: CLOSED

ASX: CLOSED

FWB: CLOSED

MOEX: CLOSED

JSE: CLOSED

DIFX: CLOSED

SSE: CLOSED

NZSX: CLOSED

TSX: CLOSED

SGX: CLOSED

NYSE: CLOSED

TSE: CLOSED

LSE: CLOSED

HKE: CLOSED

NSE: CLOSED

BM&F: CLOSED

ASX: CLOSED

FWB: CLOSED

MOEX: CLOSED

JSE: CLOSED

DIFX: CLOSED

SSE: CLOSED

NZSX: CLOSED

TSX: CLOSED

SGX: CLOSED

Commodities

Development Stages

Exchanges

Project Locations

Themes

Cartier Resources Inc.

Crux Investor Index

6

–

Market Cap (USD)

80683758

Symbol

TSXV:ECR

Stage of development

Exploration

Primary COMMODITY

Gold

Additional commodities

No items found.

Company Overview

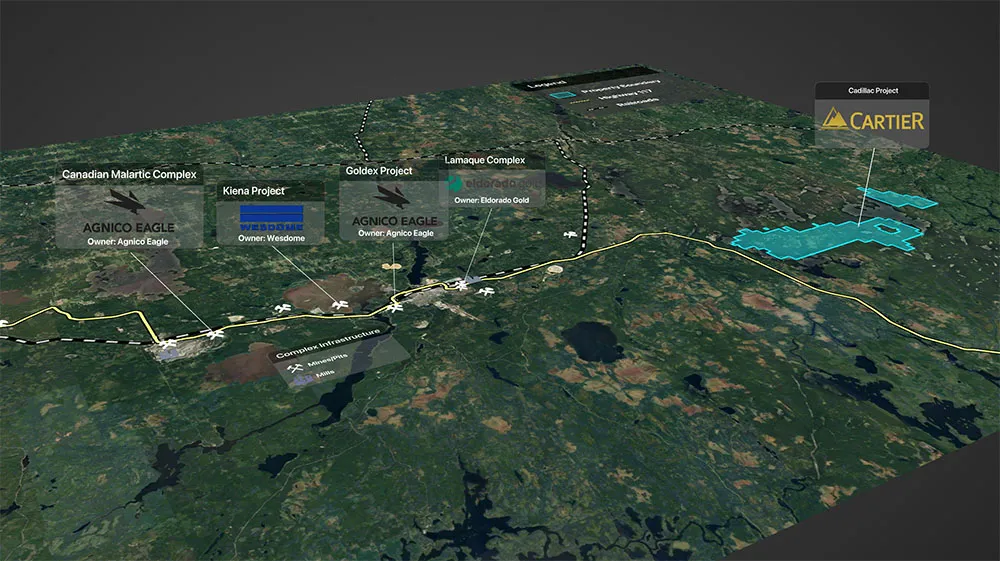

Cartier Resources (TSXV:ECR)is a junior gold exploration company focused on advancing its flagship Chimo Mine Project in Quebec's Val-d'Or mining district, one of the world's top three gold jurisdictions within the Abitibi Greenstone Belt. The company's primary asset combines the historical Chimo Mine, which previously produced approximately 379,000 ounces of gold across three operating periods between 1964 and 1997, with the recently acquired East Cadillac property. This strategic consolidation has created a significant land package with 15 kilometers of favorable gold strike in a proven mining jurisdiction.

The company trades on the TSX Venture Exchange under the symbol ECR and on the Frankfurt Stock Exchange under 6CA. With strong institutional backing, including Agnico Eagle (27%) as a major shareholder, Cartier Resources has positioned itself as an emerging player in Quebec's gold sector.

Opportunity

Cartier Resources presents a compelling investment opportunity, primarily driven by the significant disparity between its current market valuation and the demonstrated potential of its assets. The company's flagship Cadillac Project, supported by both a recent Mineral Resource Estimate (MRE) appears substantially undervalued at current market prices.

The recent2025 MRE outlines a significant Gold Resource Growth at Cadillac with 767,800 Ounces Measured and Indicated, a 7% Increase and 2,416,900 Ounces Inferred, a 48% Increase. Additionally, a significant Exploration Target was identified during the preparation of the MRE. This conceptual Exploration Target is integrated into the model used for the MRE, with the aim of facilitating future targeting and drill hole planning. Highlights of the Exploration Target: Estimated total of 8 to 12 million tonnes of mineralization grading between 2.2 to 2.8 g/t Au, representing 600,000 to 1,100,000 million ounces of gold.

A key competitive advantage lies in the project's location and existing infrastructure. The Cadillac Project benefits from existing power lines, a shaft, and tailings management facilities. This infrastructure significantly reduces capital requirements and accelerates the potential pathway to production. Furthermore, the project's location in the Val-d'Or mining district provides access to a skilled labor pool and established mining suppliers, reducing operational risks and costs.

Management

The company's leadership combines deep technical expertise with significant regional experience. President and CEO Philippe Cloutier, P.Geo., brings over 40years of mining exploration and development experience, including successful roles with major companies such as Noranda Inc. and Aur Resources Inc. His track record includes the discovery and delineation of the Bell-Allard South Cu-Zn Mine in Matagami, Quebec, demonstrating his ability to advance projects from exploration to development.

Vice President Ronan Deroff, P.Geo., who brings 20 years of experience in geochemistry, geology, and metallogeny. The financial oversight is handled by Nancy Lacoursière, who contributes 24 years of accounting experience, including 15 years specifically in the mining industry. And finally, Manon Waltz is a new member on the Cartier Resources team as Corporate Development Coordinator. With over 17 years of experience in management, she will bring valuable assets in advancing Cartier’s corporate development objectives.

Growth Strategy

Cartier Resources has outlined a clear growth strategy focused on systematic resource expansion and project de-risking. Additionally, the company is now flirting comfortably with the 100 million Canadian Dollar Market Cap levels. This should introduce us to a whole new audience of portfolio managers and sophisticated and HNW investors. Cartier remains focussed on gold and building shareholder value through discovery and development in one of Canada’s most prolific mining districts. The Company combines strong technical expertise and a track record of successful exploration programs to advance its flagship Cadillac Project.

Highlights of Accomplishments from 2025

- Initiated the restructuring of our management team, positioning Cartier for the next phase of growth.

- Secured significant funding, giving us the financial strength to execute plans.

- Optioned to Exploits Discovery Corp. (CSE: NFLD) (″Exploits″) the rights to earn 100% interests in three properties; the Wilson, Fenton and Benoist. The four-year option period grants Exploits the right to earn a 100% interest by paying Cartier an amount aggregating $1,750,000 in cash, issuing Cartier an aggregate of 9,250,000 common shares of Exploits and incurring not less than $12,250,000 in expenditures on the properties.

- Launched a major 100,000-metre diamond drill program, the most ambitious campaign yet, aimed at demonstrating the Cadillac Project has the potential to host an emerging mining camp. The drilling is on schedule and on budget and high-grade results have been reported steadily expanding known zones and increasing confidence in the resource.

- Awarded two major technical pillars to high-level independent engineering firms. Both mandates will support the entire project moving forward: Metallurgy studies, and Environmental baseline studies

- Increased marketing and rebranding as well as a new website

- Delivery of a Significant Gold Resource Growth at Cadillac with 767,800 Ounces Measured and Indicated, a 7% Increase and 2,416,900 Ounces Inferred, a 48% Increase. Additionally, a significant Exploration Target was identified during the preparation of the MRE. This conceptual Exploration Target is integrated into the model used for the MRE, with the aim of facilitating future targeting and drill hole planning. Highlights of the Exploration Target: Estimated total of 8 to 12 million tonnes of mineralization grading between 2.2 to 2.8 g/t Au, representing 600,000 to 1,100,000 million ounces of gold.

Looking Ahead to 2026

- 2026 is shaping up to be another exciting year for Cartier to re-rate Cartier valuation.

- Continue to release strong, frequent drill results from testing of historical gold showings, expanding known zones, and growing the resource base.

- Begin testing suite of highly prospective artificial intelligence targets, adding a new level of precision and technological advancement to the exploration strategy.

- Delivery of metallurgy and environmental baseline studies in Q2 and Q3 of 2026, providing essential data for upcoming engineering decisions.

- Run new iterations and model simulations on updated resource with strengthened gold price into the next scoping study for the entire project.

The company's strategy also includes investigating the potential for toll milling arrangements, which could significantly reduce initial capital requirements and accelerate the path to production. This approach, combined with the project's existing infrastructure and proximity to established mining operations, provides multiple pathways to value creation.

Financial Overview

Cartier Resources maintains a relatively strong financial position with approximately CAD 10 million in cash and a market capitalization of CAD 115 million. The company's share structure reflects strong institutional support, with Agnico Eagle holding a significant position, while maintaining sufficient retail investor participation (66.9%) for market liquidity.

The current valuation metrics suggest significant potential upside. The company trades at an enterprise value per ounce of gold of approximately $10, compared to recent M&A transactions in the sector averaging $98 per ounce.

Risk Factors and Mitigation

Resource risk represents a primary consideration for Cartier Resources. While the current resource estimate demonstrates robust potential, the expansion of resources remains crucial for optimizing project economics. The company addresses this risk through its ongoing systematic exploration program, which benefits from a strong technical team with a proven discovery track record. Importantly, the recent resource estimate, now shows resources along the entire favorable strike length and points to substantial opportunity for resource expansion through systematic exploration in 2026.

Commodity price risk poses another significant consideration, as project economics are inherently sensitive to gold price fluctuations. However, the company takes a conservative approach by using moderate gold price assumptions in its MRE. The high-grade nature of the deposit provides some natural protection against price volatility, and the potential implementation of ore sorting technology could further improve grades and project economics, helping to buffer against price fluctuations. New iterations and model simulations on updated resource with strengthened gold price into the next scoping study for the entire project

Financing risk remains a consideration as additional capital will be required for project development. The company has positioned itself well to address this challenge through strong institutional shareholders who could provide funding support. The existing infrastructure significantly reduces capital requirements compared to greenfield projects, and the company has maintained flexibility in its development path, including the potential for toll milling arrangements, which could substantially reduce initial capital needs.

Permitting and environmental risks are inherent in mining project development, as projects face increasing regulatory scrutiny. Cartier Resources benefits from operating in the mining-friendly jurisdiction of Quebec, and the project's history as a previous mining operation reduces permitting complexity. Additionally, the company incorporates carbon-friendly design elements into its project planning, aligning with modern environmental expectations and potentially streamlining the permitting process.

Conclusion

Cartier Resources represents an attractive investment opportunity in the junior gold mining sector. The combination of a substantial resource base, strong project economics, excellent infrastructure, and significant exploration upside creates multiple pathways to value creation. The company's current valuation appears to significantly discount these attributes, providing investors with a favorable risk-reward proposition.

The presence of a major mining company as a shareholder validates the project's potential and provides potential strategic options. The experienced management team, clear growth strategy, and strong financial position further support the investment thesis. While risks exist, as with any mining investment, the company has demonstrated thoughtful approaches to managing and mitigating these challenges.

The significant gap between the company's current market value and the project's demonstrated fundamental value suggests strong potential upside for investors willing to take a longer-term view. As Cartier Resources executes its growth strategy and continues to de-risk the project, multiple catalysts exist for value realization, making it an attractive opportunity for investors seeking exposure to the gold sector.

Article

Cartier Resources Inc. Analyst Notes

No analyst notes

Charts

Similar Companies

Stay Informed

Sign up for our FREE Monthly Newsletter, used by +45,000 investors

By clicking send you'll receive occasional emails from Crux Investor. You always have the choice to unsubscribe within every email you receive.