Central Asia Metals PLC

NYSE: CLOSED

TSE: CLOSED

LSE: CLOSED

HKE: CLOSED

NSE: CLOSED

BM&F: CLOSED

ASX: CLOSED

FWB: CLOSED

MOEX: CLOSED

JSE: CLOSED

DIFX: CLOSED

SSE: CLOSED

NZSX: CLOSED

TSX: CLOSED

SGX: CLOSED

NYSE: CLOSED

TSE: CLOSED

LSE: CLOSED

HKE: CLOSED

NSE: CLOSED

BM&F: CLOSED

ASX: CLOSED

FWB: CLOSED

MOEX: CLOSED

JSE: CLOSED

DIFX: CLOSED

SSE: CLOSED

NZSX: CLOSED

TSX: CLOSED

SGX: CLOSED

Commodities

Development Stages

Exchanges

Project Locations

Themes

East Star Resources PLC

Crux Investor Index

5

–

Market Cap (USD)

19605827

Symbol

LSE:EST

Stage of development

Exploration

Primary COMMODITY

Copper

Additional commodities

Gold

REE

Company Overview

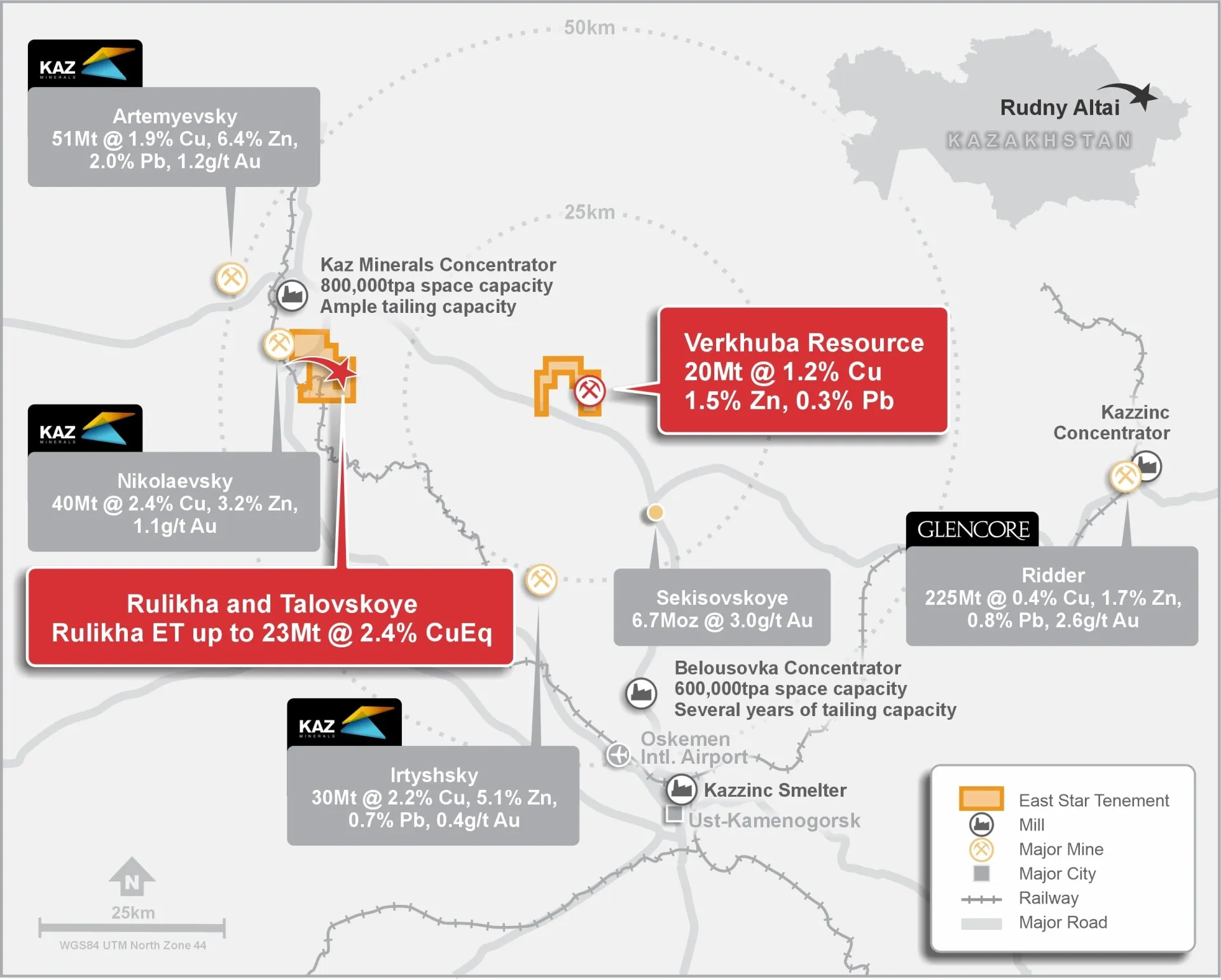

East Star owns 100% of a historical, high grade copper deposit in an established copper producing region with excess processing capacity. Confirmatory drilling is underway and intends to set East Star on a pathway to being a low CAPEX and OPEX copper producer with significant exploration upside.

From more than 42,000m of historical drill data, East Star has derived a JORC exploration target of up to 23Mt at 1.9% copper equivalent, setting the company up for a potential 13x share price re-rate on a peer comparison basis on conversion of the target to a JORC resource. The historical Verkhuba deposit has further upside potential from the addition of gold and silver, not previously assayed for but known to be in the deposit due to metallurgical test work. Previous test work also indicated a copper recovery from floatation of 96%.

Better core recovery and brownfields exploration provide even further potential upside in this high impact deposit, located in a region with roads, power, water and accommodation already at the site and two processing plants and a smelter within trucking distance for a potential low-cost open pit production scenario.

The greater licence area contains another historical deposit, four historical very high-grade copper mines, and numerous geophysical targets with known mineralisation derived from processing of East Star’s 2022 heli-borne EM survey, a detailed geological review of historical data and confirmatory site visits.

Opportunity

East Star has been operating in Kazakhstan since 2019 with management based permanently on the ground. The Company has been collecting and digitising data on the copper rich VMS licences for over two years resulting in a database which would cost more than $20m and several years to replicate, and a drill-ready deposit in Verkhuba.

Kazakhstan is a fantastic operating jurisdiction with some of the lowest mining costs globally thanks to low-cost energy and labour. The mineral law - based on Western Australia’s - was changed in 2018 and is now starting to result in more global majors including Fortescue, Barrick and First Quantum, setting up exploration operations. The EU and UK recently signed MoUs with Kazakhstan for critical mineral supply validating the country as having both the mineral endowment and the political will to take advantage of this significant and imminent demand cycle. East Star is the only UK listed company through which to access the Kazakhstan exploration opportunity.

Copper is the principal commodity poised to take advantage of this cycle, driven by the green energy transition. Falling global grades and a lack of exploration are the main drivers behind a structural deficit from 2024 that will last at least a decade.

Risk Factors and Mitigation

Despite the large amount of historical data, the potential to convert it to JORC and progress to production still carries technical risks including drill results, metallurgy, mine plans and other aspects of the project feasibility study. The low CAPEX development option is dependent on signing a commercial agreement with one of the two mills in the region which currently have capacity. As an explorer, access to funding remains a key element in project advancement.

Conclusion

East Star has a supportive shareholder base including an Australian Family office and directors, with the last money raised at 5p, being a 2.8x premium to the current share price.

The Verkhuba exploration target currently being drilled is valued at $11.5/t Cu against a peer average of $147.5/t Cu providing significant return potential in the very short term.

Buying shares in East Star provides highly leveraged exposure to both near term exploration results as well as longer term exploration/development success and exposure to a significant and prolonged copper bull market.

Article

East Star Resources PLC Analyst Notes

No analyst notes

Company Resources

Submitted by

East Star Resources PLC

Charts

Similar Companies

Stay Informed

Sign up for our FREE Monthly Newsletter, used by +45,000 investors

By clicking send you'll receive occasional emails from Crux Investor. You always have the choice to unsubscribe within every email you receive.