East Star Leverages Tier-One Partners to Fund Exploration and Fast-Track Development

East Star secures Endeavour Mining & Shanghai partnerships for Kazakhstan copper-gold projects, targeting cash neutrality 2026 & production 2027-28 while retaining tier-one upside

- East Star Resources is a Kazakhstan-focused copper and gold explorer that has secured strategic partnerships with Endeavour Mining and Hong Kong Shanghai Mining Services to derisk development

- The company leveraged Kazakhstan's reformed mining code and Soviet-era data to build an extensive project database, attracting major partners including BHP Explore program participation

- Endeavour Mining invested $5 million over two years with potential $20 million additional funding, plus taking a £1.8 million equity stake to become the largest shareholder in the joint venture for gold exploration

- Hong Kong Xinhai Mining Services will fund and develop the Verkhuba copper deposit (20Mt @ 1.2% Cu) to production, with East Star retaining 30% ownership without additional capital expenditure

- The company expects cash flow neutrality in 2026 through management fees while maintaining 100% ownership of three porphyry projects

East Star Resources is pioneering an alternative approach to junior resource development, leveraging strategic partnerships to advance multiple copper and gold projects in Kazakhstan without the traditional capital constraints that often stifle small exploration companies. CEO Alex Walker's recent discussion outlined how the company has transformed from early-stage explorer to a near-term producer through calculated joint ventures with major mining companies and contractors, while maintaining meaningful equity positions across a diversified portfolio.

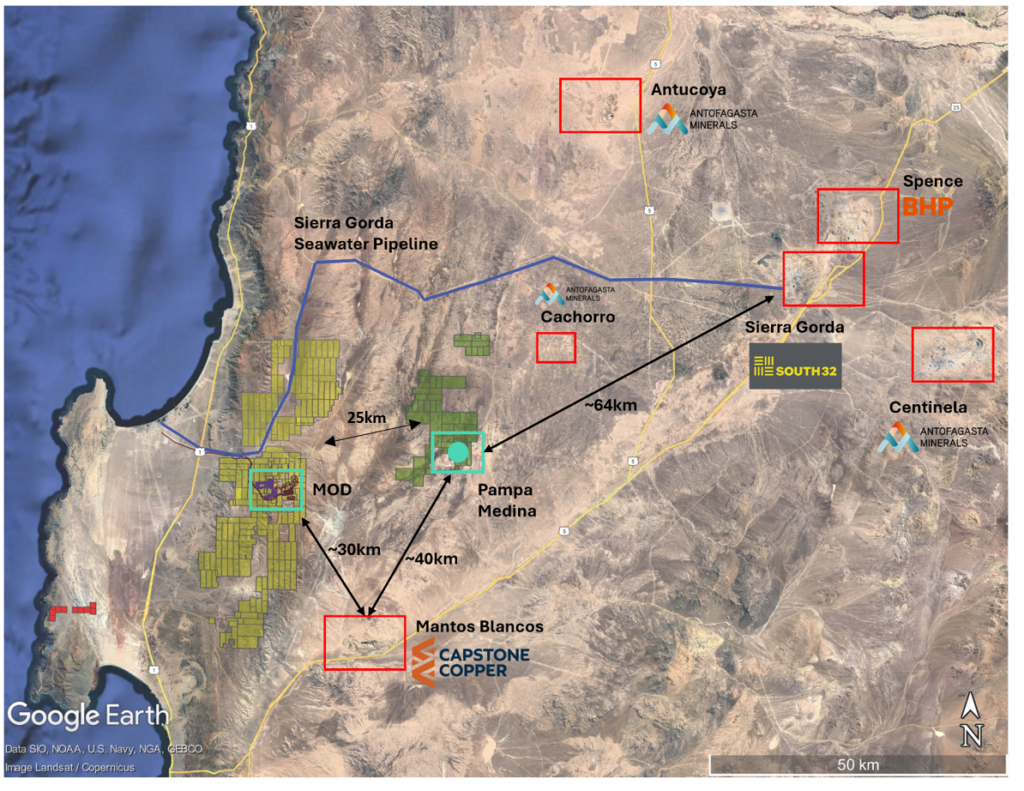

The company's strategy centers on Kazakhstan, a jurisdiction Walker describes as offering "tier one copper porphyry deposits like Aktogay with 10-12 plus million tons of contained copper" and "Vasilkovskoe with over 15 million ounces" of orogenic gold. This geological prospectivity, combined with reformed mining laws and extensive Soviet-era exploration data, created what Walker characterizes as an opportunity comparable to "being in Western Australia and having just about anywhere to peg in the 1970s."

The Kazakhstan Advantage: Jurisdiction and Infrastructure

East Star's foundational thesis rests on Kazakhstan's 2018 mining code reform, which Walker notes "modelled their new code on Western Australia's, which essentially made it a first come first serve system." This regulatory shift opened previously inaccessible geological terrain to junior explorers, while the availability of digitized Soviet exploration data significantly reduced early-stage exploration costs and risks.

The jurisdiction offers practical advantages beyond geology. Walker emphasized the infrastructure already in place:

"The mine nearest us ..was discovered in 1749. So it's been producing for hundreds of years and has railways and international airports, assay labs, smelters 70 kilometers away and underfed concentrators."

This existing infrastructure dramatically reduces capital intensity for new projects, particularly in the VMS (volcanogenic massive sulfide) belt where East Star is focused.

The company's early positioning is now being validated by major industry players. Walker noted:

"We've seen Endeavour Mining come in through us most recently. Ivanhoe have come in recently. We were part of the BHP Explore program in 2024. Rio Tinto were there. First Quantum have come in since we started."

This influx of major miners confirms the jurisdiction's emerging status as a tier-one exploration destination.

The Endeavour Mining Partnership: Gold Exploration at Scale

The most significant recent development is Endeavour Mining's multi-faceted investment in East Star. The partnership comprises two components: a joint venture agreement and a direct equity investment that made Endeavour the company's largest shareholder. Walker explained the joint venture structure:

"The first deal was $5 million over two years and then $20 million to do the maiden JORC resource and then they'll carry us through to PFS on however many projects we manage to find that reach that hurdle."

For East Star, the partnership provides access to Endeavour's balance sheet and technical expertise while the company contributes in-country operating experience and its extensive project database.

The target profile for the joint venture is ambitious. Walker stated:

"When I say tier one, it's minimum of sort of 3 million ounces plus which is certainly Endeavour's target and therefore is our target for orogenic or intrusive related gold systems or epithermal gold systems."

Endeavour's decision to take a £1.8 million equity stake alongside the joint venture represents significant validation. Walker noted:

"For them to come in at the equity level validates us as a company and all of our other strategies. They're comfortable supporting our work even though that's not their main goal."

The Xinhai Mining Services Agreement: Path to Production

While the Endeavour partnership targets high-risk, high-reward gold exploration, East Star's agreement with Hong Kong Xinhai Mining Services provides a clear path to near-term copper production. The deal covers the Verkhuba copper deposit, which hosts a JORC resource of "20 million tons at about 1.2% copper" in the VMS belt of eastern Kazakhstan.

Xinhai Mining Services, described by Walker as "a huge Chinese EPCM contractor" that has "built over 500 processing plants globally," will fully fund development through to production. The structure allows East Star to retain 30% ownership while contributing minimal capital. Walker explained:

"They will complete the resource drill out by putting an initial A$1.5M in and then they'll do all of the feasibility work."

East Star's role focuses on regulatory approvals and stakeholder management, leveraging existing relationships. The development timeline is aggressive, with Walker suggesting production could commence "by the end of 2027 but I would say 2028 would be" more realistic. The partnership's appeal to Xinhai Mining Services extends beyond Verkhuba. Walker suggested:

"Not unlike Endeavour, they see East Star with our database, with our operating track record as a fantastic way to get that initial exposure. Verkhuba could be the first of more opportunities with them."

Interview with Alex Walker, CEO, East Star Resources

Risk Diversification Strategy: VMS vs. Porphyry Assets

East Star's portfolio deliberately balances different risk-reward profiles. The company initially focused on VMS deposits specifically because they offered lower capital intensity. Walker explained:

"My focus initially was how do we get projects into production? They need to have comparatively low capital requirements. What's the capital intensity per ton of copper, but also what is the overall capex?"

VMS deposits in Kazakhstan's established mining belt offer infrastructure advantages that reduce development costs.

"I believe Kazakhstan is the cheapest place in the world to dig a hole. You can put projects into operation faster and cheaper than just about anywhere else in the world."

This cost structure potentially enables shorter payback periods and lower feasibility thresholds. For higher-risk porphyry and epithermal gold targets, East Star pursued the partnership model rather than self-funding exploration. The BHP Explore program provided initial funding for systematic target generation, which Walker described as involving "huge belt reconstruction, digitizing 1:200,000 scale maps" and ranking "more than 200 lithocaps."

Retained Assets for Future Optionality

Despite partnering on flagship projects, East Star maintains 100% ownership of significant assets that provide strategic optionality. The company controls three porphyry and epithermal projects independently, though Walker indicated openness to partnerships:

"These are big assets, potentially billion dollar developments and the discovery of a porphyry. So why not partner on those early and have someone do that higher risk exploration and we end up with a minority on that."

The Rulikha project represents another substantial wholly-owned asset. Walker announced: "Recently we announced the exploration target. It's nearly 500,000 tons of contained copper equivalent on the deposit." Like Verkhuba, this target is based on digitized Soviet drilling data rather than speculative extrapolation. Walker emphasized: "It's not taking a rock chip sample and extrapolating out along a trend by 10 kilometers. This is historic drilling that's been digitized."

Drilling at Rulikha North and Talovskoye targets has yielded encouraging results awaiting public disclosure. Walker noted:

"There's no specific discovery publicly announced today and so we need to continue to do work on that, but we're incredibly encouraged by what we've seen."

Financial Runway and Cash Flow Trajectory

The partnership structure fundamentally alters East Star's capital requirements and dilution profile. Walker outlined the 2026 outlook:

"It's arguable that in 2026 we will be cash flow neutral from an entire company perspective, a cash flow neutral exploration company with somewhere between $3 to $6 million being spent on exploration completely undiluted to East Star shareholders at the corporate level."

Management fees from Endeavour will cover in-country operating costs, while Xinhai's funding of Verkhuba drilling addresses another significant cost center. This structure allows the company to maintain exploration momentum without equity raises. Walker explained:

"The Endeavour fees will cover our in-country Kazakhstan costs. With Xinhai putting in the money for the drilling at Verkhuba, that covers a significant portion of the other costs."

Looking beyond 2026, potential production from Verkhuba could generate meaningful cash flow. The production revenue would provide internal funding capacity to maintain equity in future developments without external capital.

TL;DR: Executive Summary

East Star Resources has secured partnerships with Endeavour Mining ($5-25M committed) and Hong Kong Xinhai Mining Services (full Verkhuba funding) that provide cash flow neutrality through 2026 while advancing copper production (2027-28 target) and tier-one gold exploration without shareholder dilution. The company retains 30% of Verkhuba, 20% of Endeavour discoveries, and 100% of three porphyry projects plus the Rulikha VMS deposit (500,000+ ton Cu equivalent), positioning for production revenue to fund future development equity while major partners deploy exploration capital in an underexplored, infrastructure-rich jurisdiction validated by recent major miner entry.

FAQs (AI Generated)

Walker explained the risk-reward calculation: "You can spend a few million dollars per target and not have enough to show for it." Partnerships allow tier-one scale exploration while preserving capital and ownership stakes in multiple assets.

The combination of reformed mining laws, extensive Soviet drilling data, existing infrastructure (smelters, railways, concentrators), and tier-one proven deposits creates unique advantages. Walker notes: "Truly amazing belts and completely underexplored belts that have tier one copper porphyry deposits."

Walker explained: "For them to come in at the equity level validates us as a company and all of our other strategies. They're comfortable supporting our work even though that's not their main goal" of gold exploration.

Management fees from Endeavour cover in-country costs, while Xinhai funds Verkhuba drilling. Combined: "$3 to $6 million being spent on exploration completely undiluted to East Star shareholders at the corporate level" without equity raises.

Rulikha provides 100% owned development optionality independent of partnerships. Walker: "That's a deposit that's sitting on a license, 100% owned by East Star" with Soviet drilling defining a 500,000+ ton copper equivalent exploration target.

Analyst's Notes

Subscribe to Our Channel

Stay Informed