ATEX Resources Inc.

NYSE: CLOSED

TSE: CLOSED

LSE: CLOSED

HKE: CLOSED

NSE: CLOSED

BM&F: CLOSED

ASX: CLOSED

FWB: CLOSED

MOEX: CLOSED

JSE: CLOSED

DIFX: CLOSED

SSE: CLOSED

NZSX: CLOSED

TSX: CLOSED

SGX: CLOSED

NYSE: CLOSED

TSE: CLOSED

LSE: CLOSED

HKE: CLOSED

NSE: CLOSED

BM&F: CLOSED

ASX: CLOSED

FWB: CLOSED

MOEX: CLOSED

JSE: CLOSED

DIFX: CLOSED

SSE: CLOSED

NZSX: CLOSED

TSX: CLOSED

SGX: CLOSED

Commodities

Development Stages

Exchanges

Project Locations

Themes

Marimaca Copper

Crux Investor Index

9

–

Market Cap (USD)

984861947

Symbol

TSX:MARI

Stage of development

Development

Primary COMMODITY

Copper

Additional commodities

No items found.

Company Overview

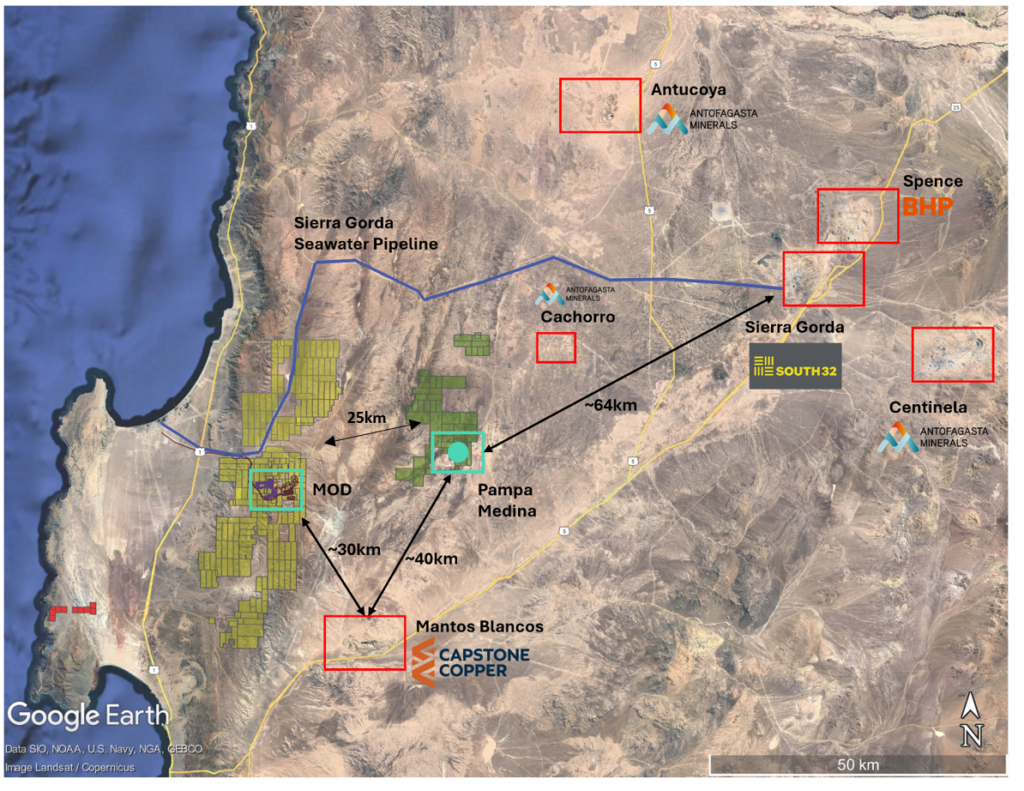

Marimaca Copper Corp operates as a development-stage copper company advancing projects in Chile's Antofagasta region. The company controls approximately 14,000 hectares in the Coastal Copper Belt, located 25 kilometers from the Port of Mejillones and 40 kilometers from Antofagasta. Trading on the Toronto Stock Exchange (MARI), Australian Securities Exchange (MC2), and OTCQX (MARIF), the company maintains a market capitalization of approximately C$1.4 billion as of November 2025 with 118.5 million shares outstanding. The shareholder base includes strategic investors Greenstone Resources (21.6%), Assore (18.9%), Ithaki Limited (13.6%), and Mitsubishi Corporation (3.9%).

The flagship Marimaca Oxide Deposit (or “MOD”) contains Proven and Probable reserves of 178.6 million tonnes grading 0.42% total copper for 748,000 tonnes of contained copper. Total Measured and Indicated resources stand at 213.5 million tonnes at 0.40% copper containing 854,000 tonnes of metal, with additional Inferred resources of 21.2 million tonnes at 0.29% copper. The 88% conversion rate from Measured and Indicated resources to reserves demonstrates confidence in the geological model and mine plan. The operational plan centers on conventional open-pit mining feeding a heap leach and solvent extraction-electrowinning processing facility producing copper cathodes.

The company completed a Definitive Feasibility Study in August 2025 and received its Resolución de Calificación Ambiental (environmental approval) in November 2025, removing a key permitting hurdle. The project has secured critical infrastructure requirements including recycled seawater supply from Mejillones Bay through a signed water option agreement and access to renewable electricity.

The company controls additional exploration properties at Pampa Medina and Madrugador within the Sierra de Medina region, located 25 kilometers from the MOD, where recent drilling has identified both oxide extensions and high-grade sulphide mineralization at depth. The company is completing a standalone PEA on the historical oxide resource at Pampa Medina and has recently commenced a 30,000m follow-up Phase II drill program. The company reported US$78.7 million in cash as of September 30, 2025, with zero debt.

Opportunity

The Marimaca Oxide Deposit presents a low capital intensity copper development with robust economics across various copper price scenarios. The August 2025 Definitive Feasibility Study outlined a post-tax net present value of US$709 million at 8% discount rate assuming US$4.30 per pound copper, generating a 31% internal rate of return with a 2.5-year payback. At US$5.05 per pound copper, the post-tax NPV increases to US$1.1 billion with 39% IRR and 2.2-year payback. The project requires US$587 million in initial pre-production capital, translating to capital intensity of US$11,700 per tonne of annual copper production capacity, positioning the development among the lowest capital intensity copper projects globally. The mine plan targets steady-state production of 50,000 tonnes per annum of copper cathode over a 13-year mine life, with cash operating costs of US$1.69 per pound (C1 basis) and all-in sustaining costs of US$2.09 per pound during steady-state operation, placing the operation in the second quartile of the global cost curve.

The strategic location in Chile's Antofagasta region provides direct highway access along Route 1, proximity to port facilities, and access to skilled labor from nearby Antofagasta and Mejillones, eliminating remote camp requirements. The secured recycled seawater supply avoids freshwater resource competition, while renewable energy access supports carbon intensity targets estimated at 38% lower than traditional concentrator-based processing. The low life-of-mine strip ratio of 0.8:1 including pre-stripped material reflects favorable deposit geometry and shallow mineralization. Project economics demonstrate resilience with average annual EBITDA of US$241 million over mine life representing a 58% margin, while the project maintains positive economics with 20% IRR at copper prices above US$3.50 per pound.

Beyond the oxide development at the MOD, Pampa Medina represents significant expansion potential outside of the known near-surface oxide deposits. Recent drilling has intersected sulphide mineralization including 198 meters grading 0.7% copper from 460 meters depth, with individual high-grade intervals of 26 meters at 4.1% copper from 580 meters. These high-grade sulphide intercepts have identified a favourable mineralized stratigraphic sequence over a 1.6km by 1.4km area and 600 meters vertically, remaining open for expansion. The sediment-hosted copper mineralization style at this scale may be unique to Chile, with implications for district-scale resource potential. Multiple near-mine exploration targets including Cindy, Mercedes, Tarso, Sierra, and Roble represent potential satellite deposits that could complement the Madrugador deposit to feed the central copper oxide processing facility under a hub-and-spoke development model.

Management

The executive leadership combines copper industry experience with Chilean operational expertise. CEO, President and Director Hayden Locke brings nearly 20 years of experience in mining and finance, previously serving as Head of Corporate Development at Papillon Resources and CEO of Emmerson Plc. Managing Director Chile and CFO Jose Antonio Merino contributes 15 years of international natural resources finance and M&A experience, including previous roles as General Manager of Business Development and M&A at SQM, providing specific Chilean market knowledge. Vice President of Exploration Sergio Rivera has over 30 years of exploration geology experience and is credited with the original Marimaca Deposit discovery. Vice President of Project Execution Alexis Munoz brings nearly 30 years managing construction of large-scale projects, most recently managing construction for Capstone Copper's Mantoverde project in the same Chilean region.

Non-executive Chairman Michael Haworth co-founded Greenstone Resources and brings nearly 30 years of resources investment experience. The board includes Clive Newall, co-founder of First Quantum Minerals, providing extensive copper production experience spanning exploration, construction, and operations globally. Giancarlo Bruno, former CEO of Mantos Copper and Vice President Chile for Capstone Copper, contributes significant Chilean copper operating experience. Alan Stephens, who co-founded the company in 2005, previously served as Vice President of Exploration for First Quantum. Tim Petterson brings mining industry experience spanning research, finance, and corporate development as founder and Executive Chairman of Minera Cobre.

The concentration of Chilean-specific copper experience, particularly recent project development and operations, differentiates this team from many junior developers. The direct experience with Capstone Copper's Mantoverde construction in the same region through Alexis Munoz reduces development risk significantly. The involvement of major shareholders Greenstone Resources, Assore, and Mitsubishi Corporation provides additional development support and credibility for project financing.

Growth Strategy

The immediate strategic priority centers on advancing toward a construction decision at the MOD targeted for second half 2026. With environmental approval (RCA) secured in November 2025, the company is progressing sectorial permits required for construction and operational phases. Detailed engineering work continues to refine capital and operating estimates and support long-lead equipment procurement, with budget quotes obtained for 80% of mechanical equipment. The financing process represents the critical path to development, with the US$587 million initial capital requirement positioning the project within range accessible through combinations of project finance debt, strategic partnerships, and equity capital.

The company continues to define credible district growth potential to increase copper production beyond the 50,000 tonnes per annum of copper cathode contemplated in the MOD DFS. The hub and spoke district model envisions the Marimaca processing facility receiving a copper-rich leach solution from the Sierra de Medina land package, leveraging permitted infrastructure to optimize capital efficiency.

Parallel exploration activities target extending mine life and increasing production scale. The Company recently completed its 10,000 meter Phase I extensional and discovery drilling program at Pampa Medina, which successfully defined a laterally continuous sediment-hosted copper horizon with both oxide and sulphide mineralization over a footprint of approximately 1.6 km by 1.4 km. The 10,000m Phase I drilling program confirmed extensions of the sulphide horizon to the north, west, and at depth, validating the geological model and demonstrating that mineralization remains open along strike and down-dip. Highlight results included hole SMRD-16, which intersected 70 meters at 1.03% copper from 434 meters, including 10 meters at 4.2% copper, as well as deeper intervals of 116 meters at 0.61% copper from 516 meters, indicating potential for substantial sulphide resource growth.

Building on the strong results and geological validation achieved in the Phase I program, Marimaca has now commenced a fully funded 30,000-meter Phase II drilling campaign at Pampa Medina, with five rigs currently active on site. Phase II is designed to significantly advance the understanding of the broader Sierra de Medina district and unlock the next stage of resource growth. The program will focus on:

- Large-scale extensional drilling focused to the north and west of the current Pampa Medina footprint, targeting strike and lateral continuity of both oxide and sulphide horizons;

- Further definition and expansion of the Pampa Medina Norte discovery, where earlier drilling confirmed substantial northern extensions to the system; and

- Systematic testing of deeper sulphide mantos within the productive sedimentary sequence to support future resource estimation, evaluate the scale of the sulphide system, and assess potential integration synergies with the MOD development plan.

Phase II represents the first district-wide program designed to map the full extent of this tier-one opportunity, defining a single, continuous sediment-hosted copper system across Sierra de Medina region.

Financial Overview

The Definitive Feasibility Study provides comprehensive financial metrics at multiple copper price assumptions. At US$4.30 per pound copper with US$0.10 per pound cathode premium, the project delivers post-tax NPV of US$709 million and 31% IRR. Base case at US$5.05 per pound copper increases post-tax NPV to US$1.1 billion with 39% IRR. The project generates average annual post-tax free cash flow of US$160 million during years 1-10 of operation. Sensitivity analysis shows the project delivers 34% IRR with 10% cost overruns at base case copper prices, demonstrating economic robustness. The project maintains positive economics with 20% IRR at copper prices above US$3.50 per pound.

Initial capital expenditure of US$587 million comprises US$437 million direct costs (74%), US$80 million indirect costs (14%), US$17 million owner's costs (3%), and US$53 million contingency (10%). The capital estimate achieves AACE Class 3 guidelines with expected accuracy of -20% to +25%. Operating costs average US$11.90 per tonne processed over mine life, with C1 costs declining to US$1.45 per pound and AISC to US$1.97 per pound during first five years of steady state. The project delivers 550,000 tonnes of copper production over 13 years, with peak annual production of 50,000 tonnes for five consecutive years. Expansion capital of US$77 million in year six increases tertiary crushing and leaching capacity from 12 million tonnes to 16 million tonnes per annum, while sustaining capital totals US$529 million over mine life.

The capital structure includes zero debt with US$78.7 million cash as of September 30, 2025. The diversified shareholder base across institutional and strategic investors supports market liquidity. Analyst coverage from eight firms including BMO Capital Markets, RBC Capital Markets, Canaccord, and Raymond James provides market visibility. The development timeline targeting FID in H2 2026 positions the company to arrange project financing and begin construction within 12-18 months. The oversized initial processing infrastructure enables cost-effective future expansion in Phase 2 and further integration with regional oxide copper deposits.

Risk Factors and Mitigation

- Commodity Price Volatility: Project economics demonstrate sensitivity to copper prices with post-tax IRR declining from 39% at US$5.05/lb to 31% at US$4.30/lb, requiring sustained prices above US$3.50/lb to maintain 20% returns. Second-quartile C1 costs of US$1.84/lb, 58% EBITDA margins, 2.5-year payback period, and capital intensity of US$11,700/tpa ranking among lowest globally provide downside protection.

- Regulatory and Permitting Risks: While RCA environmental approval was received, sectorial permits remain required before construction with potential for regulatory changes or community engagement challenges creating delays. The on-schedule receipt of the RCA approval in Q4 and strong relationship with local and national regulators demonstrates the Company’s ability to meet key permitting milestones, reducing execution risk for remaining approvals. Early regulator engagement, experienced local management, recycled seawater use, renewable energy access, and absence of community land overlaps mitigate permitting risks.

- Technical and Operational Risks: Project assumes specific metallurgical recoveries averaging 72%, equipment availability from equipment suppliers, and mining rates reflecting industry standards, with actual results potentially differing from feasibility assumptions. Seven phases of geometallurgical testing, engagement of engineering groups Ausenco and NCL with significant Chilean experience, 88% resource-to-reserve conversion, and budget quotes for 80% of equipment reduce technical uncertainty.

- Environmental and Social Risks: Project faces ongoing environmental management and community relations requirements with potential for opposition or incidents resulting in regulatory action or production disruptions. Coastal Atacama Desert setting with limited ecological impact, recycled seawater and renewable energy use, ongoing stakeholder engagement, and no community land overlaps support social license maintenance.

- Financing Risk: Project requires US$587 million initial capital with potential for delays or unfavorable financing terms impacting development timeline. Strong economics with 31% IRR, strategic shareholders including Greenstone (21.6%), Assore (18.9%), and Mitsubishi (3.9%), current cash of US$78.7 million, and potential for streaming or offtake agreements mitigate financing challenges. The Company has a strong track record of accessing equity markets to support development activities, providing an additional mitigant to financing risk.

- Execution Risk: Converting feasibility study into operating mine requires successful procurement, construction management, and commissioning with potential for cost overruns or schedule delays. Alexis Munoz's recent Mantoverde construction experience, proximity to Antofagasta's skilled labor pool, conventional project scope, and 10% capital contingency reduce execution challenges.

Conclusion

Marimaca Copper Corp presents a copper development opportunity characterized by low capital intensity, robust project economics, and meaningful exploration upside in an established mining jurisdiction. The Definitive Feasibility Study demonstrates project viability with 31% IRR at US$4.30 per pound copper, industry-leading capital intensity of US$11,700 per tonne annual production capacity, and 2.5-year payback. The November 2025 environmental approval removes a key permitting hurdle, positioning the company toward a construction decision in second half 2026. The project benefits from strategic location near world-class infrastructure, low technical risk through conventional mining and processing, second-quartile operating costs, and access to recycled water and renewable energy.

Beyond the oxide development, exploration potential across Pampa Medina's sulphide mineralization offers meaningful upside optionality. Recent drilling validating sediment-hosted copper at depth suggests potential for materially extending mine life and production scale. Intercepts such as 198 meters at 0.7% copper and 26 meters at 4.1% copper highlight the strength and continuity of the mineralized horizon amenable to conventional mining practices. The hub-and-spoke district development strategy provides a near-term pathway to leverage initial infrastructure to expand production beyond the 50,000 tonnes of copper oxide per annum contemplated in the MOD DFS. The management team combines relevant copper operations experience, Chilean mining expertise, and project development track records, with a strategic shareholder base providing development support.

Key catalysts through 2026 include completion of sectorial permitting, detailed engineering finalization, project financing execution, and continued Pampa Medina drilling with potential resource definition. The combination of near-term production visibility from 748,000-tonne oxide reserve, longer-term expansion potential from sulphide and satellite deposits, and advancement toward construction decision creates a balanced risk-return profile for investors seeking copper development exposure in a Tier-1 jurisdiction with established resources and district-scale exploration potential.

Article

Marimaca Copper Analyst Notes

No analyst notes

Company Resources

Submitted by

Marimaca Copper

Charts

Similar Companies

Stay Informed

Sign up for our FREE Monthly Newsletter, used by +45,000 investors

By clicking send you'll receive occasional emails from Crux Investor. You always have the choice to unsubscribe within every email you receive.