Copper's Trade War Opportunity: Best Plays for 2025

Copper faces trade disruption and supply chain shifts while exploration successes and strong capital markets create diverse investment opportunities across development stages.

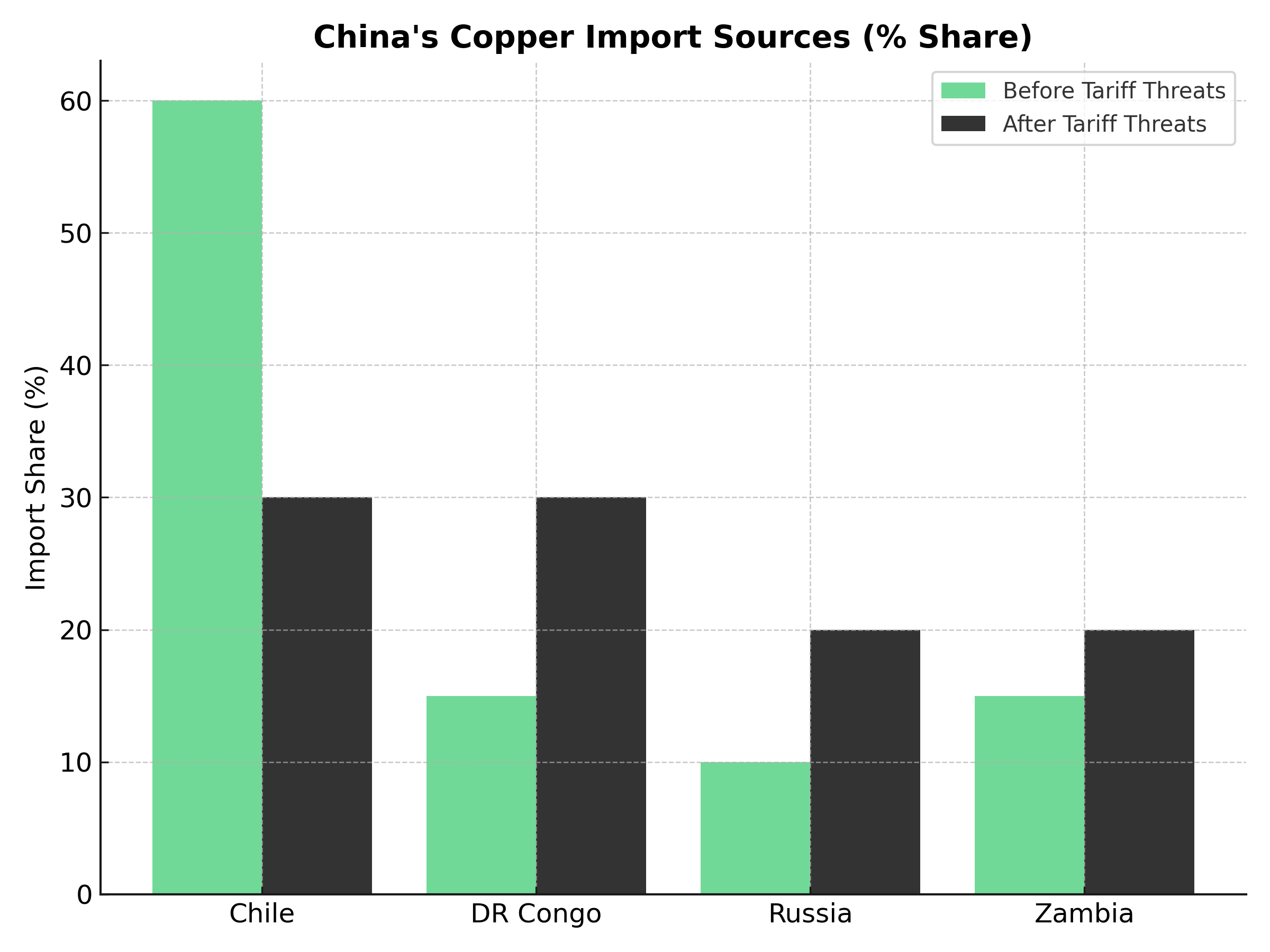

- U.S. copper tariff threats are forcing global trade flow restructuring, with China pivoting from traditional suppliers like Chile to alternative sources including DR Congo, Russia, and Zambia, creating both supply disruption risks and new market opportunities.

- Recent drilling results from companies like Fitzroy Minerals demonstrate significant copper discoveries with near-surface oxide mineralization extending over 985 meters of strike length, indicating robust exploration success rates that could support future supply growth.

- Major copper developers like Marimaca successfully raised A$80 million at premium valuations, while explorers like Gladiator Metals completed upsized $22.5 million financings, signaling strong institutional appetite for copper exposure ahead of expected supply deficits.

- Canadian flow-through financing structures and government support for critical mineral exploration are providing tax-advantaged funding mechanisms for copper projects, particularly in politically stable jurisdictions like Canada's Yukon Territory.

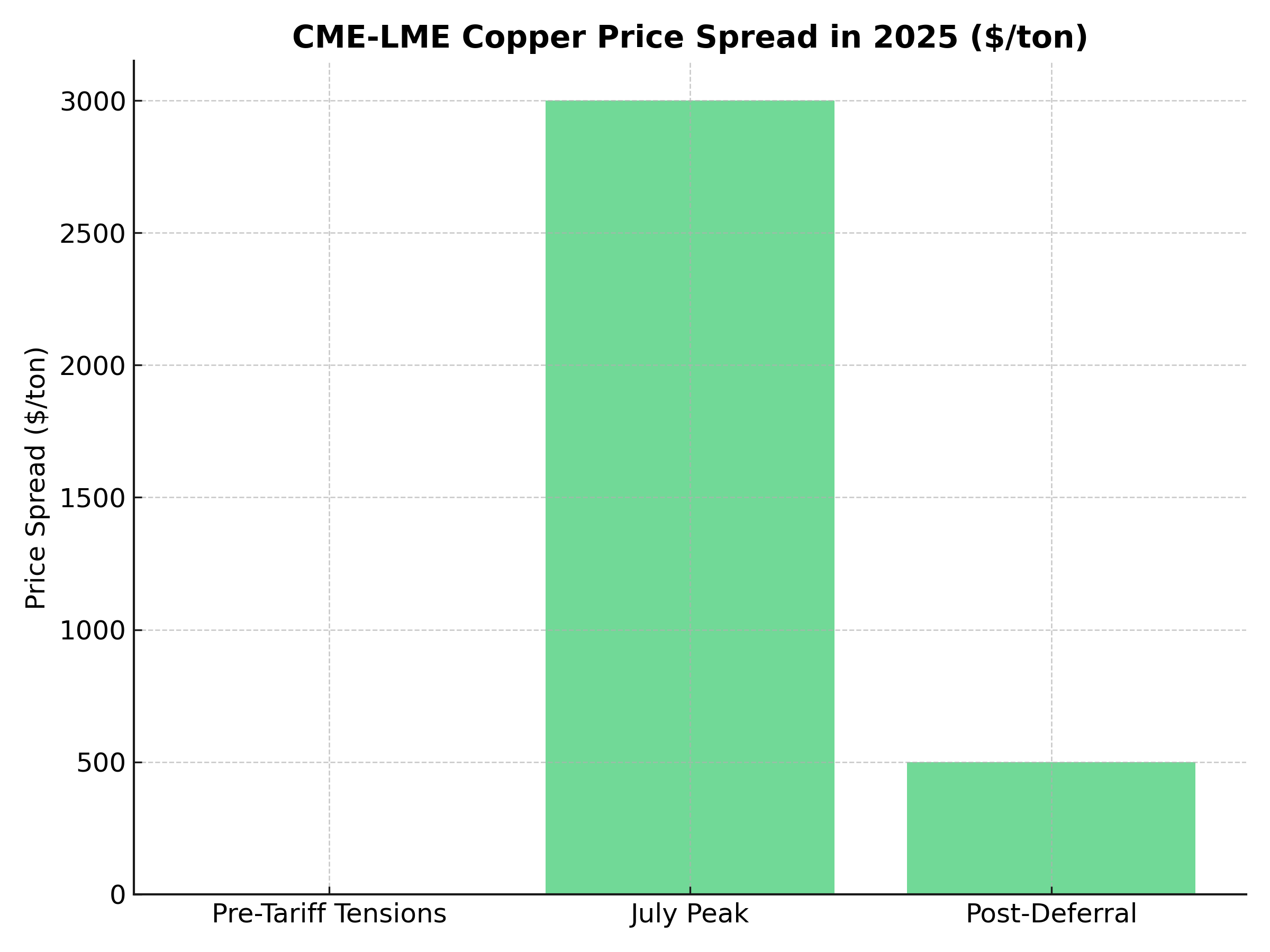

- CME-LME copper price spreads reached nearly $3,000/ton before collapsing when U.S. refined copper tariffs were deferred, highlighting significant trading opportunities and the market's sensitivity to policy developments.

The Copper Investment Case: Navigating Geopolitical Shifts & Resource Expansion Opportunities

The global copper market stands at a critical inflection point as geopolitical tensions reshape traditional supply chains while exploration companies deliver promising discoveries that could define the next generation of copper production. Recent developments spanning from U.S.-China trade dynamics to breakthrough drilling results in Chile paint a complex but ultimately bullish picture for copper investments in 2025 and beyond.

Global Trade Dynamics Creating New Investment Paradigms

The copper market's fundamental structure is undergoing dramatic transformation as trade policies force a reconfiguration of global supply relationships. China's net imports of refined copper dropped to a one-year low in July, directly linked to U.S. tariff investigations that began with a national security review in February 2025. This policy-driven disruption has created both challenges and opportunities across the copper value chain.

The immediate market response has been striking. Premiums between U.S. price (CME) and London (LME) widened dramatically (almost $3,000/ton in July) before collapsing when U.S. deferred refined copper tariffs. Such extreme price dislocations highlight the market's sensitivity to policy developments and create substantial arbitrage opportunities for sophisticated investors.

China's adaptive response demonstrates the market's resilience and flexibility. Rather than accepting reduced copper access, Chinese buyers have diversified their supplier base, with China increased imports from other countries: DR Congo (leading), Russia, Zambia. This shift toward African and alternative suppliers represents a fundamental realignment that could benefit mining companies operating in these emerging copper provinces.

The implications extend beyond immediate trade flows. Chinese smelters have strategically repositioned inventory, with LME‐registered Chinese copper stocks rose (e.g. from 25,000 tons → 98,000 tons in July), indicating sophisticated supply chain management that could influence global copper availability and pricing dynamics for months to come.

Exploration Breakthroughs Signaling Resource Expansion

While trade tensions dominate headlines, the exploration sector is delivering results that could reshape medium-term supply dynamics. Fitzroy Minerals' recent drilling program at the Buen Retiro Copper Project in Chile exemplifies the type of discovery that attracts institutional capital and validates regional exploration strategies.

The technical results are compelling from both geological and economic perspectives. Copper mineralization was intersected in all of the reported dozen+ holes (holes 21, 23–27), with The strike length in the Southwest Area has been extended to about 985 metres. This consistency across drilling targets suggests a robust mineralized system that could support significant resource expansion.

CEO Merlin Marr-Johnson of Fitzroy Minerals emphasized the strategic importance of these results:

"Drilling at Buen Retiro continues to demonstrate good copper grades and thicknesses below the gravels in the Southwest Area… our drilling takes the proven strike length of the system to almost 1 km, and the wide and shallow mineralization we are finding will increase the dimensions of any potential future pit."

Marr-Johnson, who has over 20 years of experience in mineral exploration and project development across South America, brings deep regional expertise to Fitzroy's Chilean operations.

Perhaps more importantly for near-term development economics, the project features substantial shallow mineralization. Key intersections include 32 m @ 0.90% Cu from 2 m depth, including 11 m @ 2.28% Cu from 11 m in hole BRT-DDH-25, indicating oxide material suitable for lower-cost heap leach processing. The combination of near-surface access and strong grades creates an attractive development profile that could generate positive cash flows relatively quickly.

The geological continuity observed across the drilling program suggests scale potential that goes beyond typical early-stage discoveries. With There is good shallow (oxide / mixed / secondary sulphide) mineralization generally from near surface (or shallow bedrock) down to ~150 m vertical depth in portions of the Southwest Area, plus deeper sulphide targets, the project appears to offer both near-term development upside and longer-term expansion potential.

Capital Market Dynamics Supporting Sector Growth

The copper sector's access to capital remains robust despite broader market volatility, as evidenced by recent successful financings across different company stages and jurisdictions. Marimaca Copper's substantial Australian placement demonstrates institutional appetite for advanced copper development projects, while smaller explorers continue attracting growth capital through innovative financing structures.

Marimaca's recent success is particularly noteworthy given current market conditions. The company successfully raised A$80 million through a brokered placement at A$9.70 per CDI, with proceeds earmarked for exploration at Pampa Medina Project and detailed engineering work at the Marimaca Oxide Deposit. The participation of established institutional investors and the premium pricing achieved suggest confidence in both the specific project fundamentals and broader copper market outlook.

President and CEO Hayden Locke highlighted the strategic positioning this funding provides:

"There are very few actionable copper projects in the near term that can become a reasonably significant producer. At 50,000 tonnes with a growth pipeline to 70,000, we expect strong interest given recent transactions like MAC's acquisition and Mitsubishi's move into Copper World. These deals suggest buyers are either underwriting nearly $5 copper or paying significant NAV multiples, which is instructive for the sector."

Locke, who previously served as Managing Director of Hot Chili Limited and has extensive experience in Chilean copper development, brings valuable M&A and strategic perspective to Marimaca's growth trajectory.

The Canadian market offers additional capital formation advantages through specialized structures like flow-through financing. Gladiator Metals' recent $22.5 million raise illustrates these benefits, with $15 million raised through flow-through shares at $1.42 per share for eligible Canadian exploration expenses. This structure provides Canadian investors with immediate tax deductions while funding high-risk exploration activities, creating a win-win dynamic that supports junior exploration companies.

CEO Jason Bontempo of Gladiator Metals emphasized the strategic value of the successful financing:

"The successful closing of our upsized $22.5 million financing provides the capital to accelerate exploration in the Yukon and advance our projects with a stronger balance sheet. With both flow-through and hard dollar support, we are positioned to create value while maintaining flexibility for corporate initiatives."

Bontempo, who has over 15 years of experience in mineral exploration and corporate development, has successfully led multiple exploration programs across Canada's premier mining districts.

The upsizing of Gladiator's original financing target signals strong investor demand and underwriter confidence. The involvement of established dealers including Cormark Securities, Beacon Securities, and Canaccord Genuity provides credibility and distribution capability that should support ongoing corporate development activities.

Mogotes Metals: Strategic Positioning in World-Class Discovery District

Mogotes Metals represents a compelling exploration story positioned adjacent to some of the world's largest copper discoveries. CEO Allen Sabet has assembled a strategic land package in Argentina's Vicuña district, where neighboring deposits including Filo del Sol are valued at $4.5 billion. The company's systematic approach over three years demonstrates methodical value creation rather than speculative positioning.

With a market capitalization of $107 million and treasury of $26 million, Mogotes offers significant leverage to discovery success. The company has invested $20 million in comprehensive exploration work, including 60 kilometers of new access tracks, extensive soil and rock chip sampling programs, and cutting-edge 3D geophysical surveys modeling electrical properties and resistivity.

"We've done extensive sampling program... five six months of work for teams of guys with 4x4 vehicles walking across mountains to do that first pass soil sampling grid rock chip sampling," explains Sabet. The company's technical advantage comes from leveraging discoveries at neighboring properties, compressing typical 20-year exploration timelines through systematic application of proven geological models.

The upcoming drilling program, scheduled for October, will test multiple high-priority targets for the first time. Mogotes benefits from elevation advantages, allowing access to targets at shallower depths than neighboring deposits while avoiding difficult drilling conditions like silica caps that constrained development at Filo del Sol. With depths ranging from 300-600 meters to target zones, the company can achieve faster drilling speeds and lower costs than regional peers.

Magna Mining: High-Grade Polymetallic Discovery and Infrastructure Advantage

Magna Mining exemplifies how operational expertise and existing infrastructure can accelerate development timelines and reduce capital requirements. CEO Jason Jessup, who previously managed operations at the Levack mine during its original development with FNX Mining, brings intimate knowledge of these Sudbury assets and their exceptional grade potential.

The company recently completed a $45 million financing with strong institutional participation, including 22 institutions and international generalist funds seeking copper and gold exposure. This funding supports aggressive drilling programs targeting replication of the Morrison deposit, which historically produced over 2 million tons at 10% copper and 10 grams precious metals with $1,200 NSR rock values.

Recent drilling results demonstrate the discovery potential, with intersections including 1 meter at 29% copper and 53 grams platinum-palladium-gold, plus 29 grams gold alone. Over 2.6 meters, the intersection averaged 14% copper and 29 grams combined precious metals. These results suggest proximity to a larger system, similar to the Morrison deposit's trunk veins that reached 6-7 meters width at depth.

The infrastructure advantage cannot be overstated. Existing ramps, ventilation, loading pockets, and shaft access dramatically reduce development timelines. Where the original Morrison deposit required 24 months to reach commercial production, Magna can potentially start deeper in the system where grades are highest, using existing infrastructure to access multiple mining levels simultaneously.

Firefly Metals: Rescue Story with Scale Potential

Firefly Metals demonstrates how experienced teams can unlock value from distressed assets through systematic approach and adequate capitalization. CEO Darren Cooke, with Northern Star background and business development experience, acquired the Green Bay copper-gold project from administration in August 2023, eliminating debt burdens and unfavorable contracts that constrained previous operators.

The project features substantial scale, with resources expanded from 40 million tons at acquisition to 60 million tons through 90,000 meters of drilling. Recent results include 25 meters at 5% copper equivalent, with downhole geophysics indicating conductors extending 700 meters beyond current drilling. The VMS system demonstrates over 3 kilometers strike length, comparable to world-class deposits like Kidd Creek.

Cook's team recently secured A$77-80 million funding, primarily from Canadian and international institutions including BlackRock as largest shareholder. This funding supports accelerated surface exploration, underground development expansion, and early works for production restart. The dual listing strategy on Toronto and Australian exchanges provides broader capital access.

"The great thing about Newfoundland is it's so far east, people forget. I fly from St. John's to London quicker than I can fly from Perth to Sydney," explains Cook, highlighting logistical advantages for European concentrate markets. The project benefits from skilled local labor, with experienced Newfoundland miners readily available for recruitment.

Technical advantages include 96% metallurgical recovery rates producing 27-29% copper concentrate with 8-12 grams gold content and no deleterious elements. This high-quality concentrate attracts multiple offtake partners and European credit agencies offering favorable debt financing. The planned 1.8 million ton processing plant will be constructed on-site, eliminating previous transport costs to mills 40 kilometers away.

Best Copper Companies for 2025 Investment Opportunities

The current market environment favors a diversified approach to copper exposure, spanning different stages of development and geographic exposure. Advanced development projects like Marimaca Copper offer near-term production upside with defined resources and feasibility-stage engineering, while exploration companies like Fitzroy provide leverage to discovery success and resource expansion.

Canadian explorers benefit from supportive government policies and flow-through tax advantages that effectively subsidize exploration risk. Gladiator Metals' Yukon properties operate within a mining-friendly jurisdiction with established infrastructure and regulatory certainty, factors that become increasingly important as permitting and community relations challenges intensify in other regions.

Chilean copper projects offer exposure to one of the world's premier copper provinces with established mining infrastructure and technical expertise. Fitzroy Minerals' Buen Retiro project benefits from proximity to Copiapó and existing power infrastructure, reducing development risk and capital requirements compared to greenfield locations.

The key for investors is matching investment timeframe with company development stage. Near-term copper price exposure is best captured through advanced developers with defined resources and feasibility studies, while longer-term supply growth opportunities require exposure to successful exploration programs that could define the next generation of copper mines.

Supply Chain Disruption Creating Investment Alpha

The ongoing reorganization of global copper trade flows creates both risks and opportunities that sophisticated investors can exploit. The shift away from traditional China-Chile trade relationships toward African and Russian suppliers introduces new variables into global supply chain planning and creates potential bottlenecks that could support higher copper prices.

Scrap copper supply disruption represents a particularly under-appreciated factor in current market dynamics. The collapse in U.S. scrap exports to China following reciprocal tariffs eliminates a significant secondary supply source, effectively tightening global refined copper availability. This dynamic should benefit primary copper producers while creating supply security concerns for major consuming regions.

The European Union's consideration of export restrictions on recyclable metals could further constrain secondary copper supply, amplifying the importance of primary mine production. Mining companies with established operations or advanced projects positioned to fill these supply gaps should benefit from sustained high prices and premium market positioning.

Infrastructure companies serving emerging copper provinces could also benefit from trade flow reorganization. As Chinese buyers develop new supplier relationships in Africa and other regions, investment in port facilities, transportation networks, and smelting capacity becomes increasingly valuable.

Regional Focus: Top Copper Mining Stocks by Geography

The combination of flow-through tax advantages, stable regulatory environment, and prospective geology makes Canadian copper explorers attractive for risk-tolerant investors. Gladiator Metals exemplifies this opportunity with its Yukon portfolio and recent successful financing at premium valuations.

Chile's established mining infrastructure and technical expertise provide natural advantages for copper project development. Fitzroy Minerals' Buen Retiro results demonstrate the continued mineralisation in the prolific Chilean copper districts and the potential for new discoveries within established mining regions.

Companies like Marimaca Copper, with both Canadian and Australian listings and international project portfolios, offer exposure to global copper opportunities with access to sophisticated capital markets and institutional investor bases.

The geographic diversification of copper opportunities reflects both geological reality and political risk management. Investors seeking copper exposure should consider portfolio construction that spans multiple jurisdictions while weighting investments toward regions with favorable mining policies and established infrastructure.

The Investment Thesis for Copper

- Allocate 40% to advanced developers like Marimaca with near-term production timelines, 35% to mid-stage explorers with defined resources, and 25% to early-stage discovery plays like Fitzroy for maximum upside leverage.

- Target companies serving emerging copper corridors (Africa-China, alternative supply routes) as traditional Chile-China relationships weaken, creating new premium markets for non-traditional suppliers.

- Maximize flow-through share allocations in Canadian copper explorers before year-end to capture immediate tax deductions while gaining exposure to government-subsidized exploration in mining-friendly jurisdictions.

- Prioritize investments in near-surface oxide copper discoveries that offer lower-cost heap leach processing and faster cash flow generation compared to complex sulphide projects requiring expensive concentrator facilities.

- Position for sustained higher prices as U.S.-China trade tensions eliminate significant secondary copper supply, creating structural tightness that benefits primary producers with established operations.

- Maintain exposure across stable mining jurisdictions (Canada, Australia, Chile) while avoiding single-country concentration that could be vulnerable to policy changes or resource nationalism trends.

Investment Outlook: Navigating Copper's Transformation

The copper investment landscape in 2025 presents a unique combination of geopolitical disruption, exploration success, and supportive capital markets that creates multiple pathways to investment returns. Trade war dynamics are reshaping global supply chains while exploration breakthroughs demonstrate continued resource expansion potential. Capital markets remain supportive of copper investment across development stages, with innovative financing structures providing additional advantages for Canadian-focused strategies.

Key investor implications center on portfolio diversification across development stages and geographic regions, with particular attention to companies that benefit from trade flow disruption or possess high-quality oxide copper resources suitable for low-cost development. The combination of supply chain reorganization, secondary supply disruption, and continued exploration success creates a favorable environment for copper investments that span near-term price exposure and longer-term supply growth opportunities.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed