Battery Metals Investment Analysis: The Critical Materials Powering the Energy Transition

Battery metals surge on EV demand & supply constraints. Indonesia's nickel restrictions, lithium shortages by 2025, copper deficit create compelling investment case.

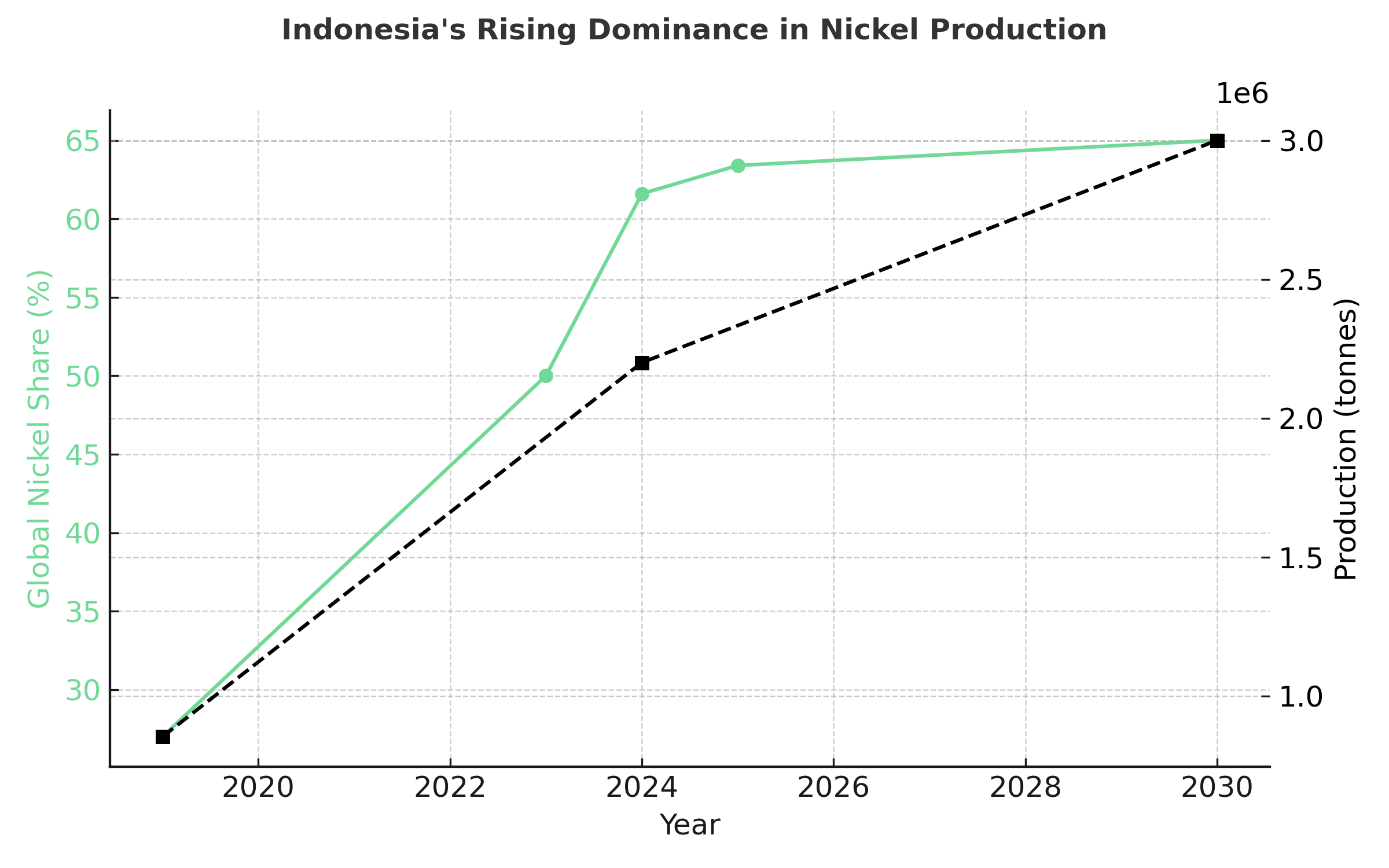

- Indonesia dominates nickel production with 50-61.6% of global output as of 2024, while China controls processing for most battery metals, creating geopolitical vulnerabilities. Indonesia's export restrictions and new regulations effective January 2025 further intensify supply chain concentration.

- Battery metals demand increased strongly in 2024, with lithium rising 30% year-over-year and nickel, cobalt, graphite growing 6-8%, driven by electric vehicles, battery storage, and renewable infrastructure. The energy sector accounts for 85% of battery metals demand growth.

- Following 2021-22 price surges, battery metals declined significantly - lithium falling over 80% since 2023, while graphite, cobalt and nickel dropped 10-20% in 2024 as supply expansions outpaced demand growth.

- Indonesia's nickel export ban since 2020 and mandatory domestic processing requirements are reshaping global supply chains, while the geographic concentration of refining increased from 82% to 86% among top three nations between 2020-2024.

- Critical mineral investment growth slowed to 5% in 2024 from 14% in 2023, with exploration activity plateauing. Current project pipelines show potential supply gaps - copper meeting only 70% and lithium 50% of requirements by 2035.

The Strategic Imperative: Why Battery Metals Define the Energy Transition

The global economy stands at an inflection point. The shift to clean energy technologies requires massive increases in mineral requirements, with the energy sector emerging as a major force in mineral markets for the first time. Unlike previous commodity supercycles driven by industrial expansion, today's demand surge is policy-mandated, government-subsidized, and existentially necessary for climate goals.

Electric vehicles and battery storage alone will grow demand for critical minerals by 10-30 times through 2040, with EVs displacing consumer electronics as the largest lithium consumer and positioned to overtake stainless steel as nickel's primary end-use. This isn't a typical demand cycle, it's a structural transformation of the global materials economy.

Global Market Dynamics: Supply Concentration Meets Exponential Demand

The battery metals landscape reveals stark geographical concentration that creates both opportunity and risk. Indonesia produces 48% of global nickel, China controls 75% of battery metal refining capacity, and the top three producers of key energy minerals increased their combined market share from 73% in 2020 to 77% in 2024.

This concentration isn't accidental. Indonesia's strategic nickel export ban, implemented in phases since 2014 and tightened through 2025, exemplifies resource nationalism designed to capture more value-added processing domestically. The policy has successfully attracted $4.5 billion in foreign investment including partnerships with Ford, Tesla's suppliers, and Chinese battery manufacturers.

Demand Projections: The Numbers Behind the Transition

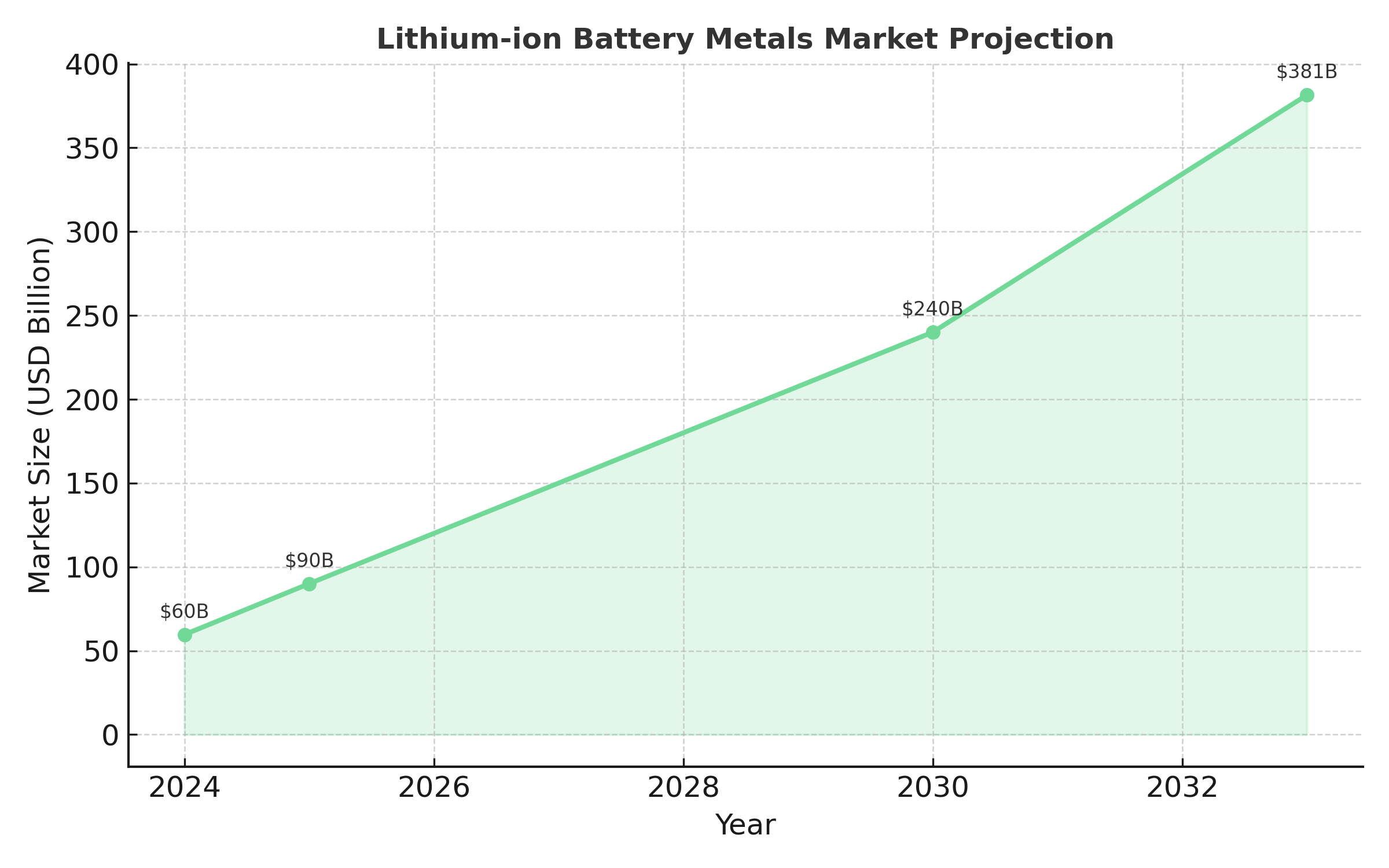

The lithium-ion battery metals market, valued at $59.63 billion in 2024, is projected to reach $381.46 billion by 2033, representing a 22.9% compound annual growth rate. This growth is underpinned by multiple converging trends:

Global EV sales reached over 17 million units in 2024, marking a 25% increase from the previous year. China led with 11 million units (40% growth), while EV battery demand is projected to grow 4.5 times by 2030 and seven times by 2035 in climate scenarios.

Grid Infrastructure: Electricity networks account for significant mineral demand from energy technologies, with copper requirements expected to more than double through 2040 for grid expansion.

Energy Storage: Battery storage capacity additions reached a record 40 GW in 2023 alone, doubling from 2022, requiring substantial quantities of lithium, nickel, and graphite.

Metal-by-Metal Investment Case

Indonesia's dominance creates the most compelling supply-side investment story in battery metals. The country accounts for 61.6% of global nickel production in 2024, expected to rise to 63.4% in 2025. New regulations effective January 2025 extend export bans to nickel ore concentrates while requiring foreign companies to maintain maximum 49% ownership in mining operations. The US-Indonesia trade framework announced in July 2025 aims to address these restrictions, but implementation remains uncertain.

Indonesia's nickel output increased dramatically from 853,000 tonnes in 2019 to 2.2 million tonnes in 2024 - a 158% increase over five years. Some estimates suggest production could reach over 3 million tonnes by 2030, representing 65% of global supply.

Investment Implications: Canada Nickel's Crawford project, targeting a 2025 construction decision with the world's second-largest nickel reserve, represents a premier non-Indonesian supply source positioned to benefit from Western supply chain diversification efforts.

Copper: The Structural Supply Gap

Copper presents the most concerning supply-demand outlook, with anticipated mine supply from announced projects meeting only 70% of copper requirements by 2035. The combined market value of key energy transition minerals - copper, lithium, nickel, cobalt, graphite and rare earth elements - is projected to more than double to reach $770 billion by 2040 in Net Zero scenarios, with copper seeing the largest absolute increase due to electrification demands.

Exploration companies like Gladiator Metals in Yukon's Whitehorse Belt offer discovery upside in the 35 km Whitehorse Copper Belt with multiple past-producing mines and strong infrastructure advantages.

Graphite: China Dependency Drives Diversification

China accounts for 95% of manganese sulfate production and nearly all graphite used in anode materials, creating the most concentrated supply chain in battery metals. Western alternatives include Sovereign Metals' Kasiya project in Malawi holds both the world's largest rutile resource and second-largest flake graphite resource, with graphite as a by-product of rutile mining reducing production costs to $241/t FOB versus China's $257/t average.

Rutile: Specialized Supply Constraints

Sovereign Metals' position as the only known deposit where graphite is a by-product of rutile mining, combined with Rio Tinto's 19.9% strategic stake, creates a unique investment proposition in this specialized titanium feedstock market.

Company Case Studies: Canada Nickel: North American Battery Supply Leadership

Canada Nickel represents the strategic shift toward Western hemisphere battery supply chains with its flagship Crawford Nickel Sulphide Project in Ontario's Timmins Nickel District. The company is advancing the world's second-largest nickel reserve toward a 2025 construction decision, with the project showing exceptional scale and economics. The Crawford project's feasibility study demonstrates robust fundamentals: US$2.5 billion NPV8%, 17% IRR, positioning it as a long-life, low-cost, large-scale nickel producer. Further optimization through Front-End Engineering Design (FEED) work has enhanced the project economics to US$2.8 billion NPV8% with 17.6% IRR, while the Environmental Impact Statement has been filed with permits expected in Fall 2025.

Beyond Crawford, Canada Nickel has consolidated a district-scale opportunity spanning 20+ ultramafic targets across an area 25 times Crawford's footprint. The company has published six resources by mid-2025 with three more expected, including the "Three Giants" (Reid, Mann, Midlothian) showing higher grades and large footprints. Recent drilling at Reid confirmed continuity of higher-grade nickel zones, while Mann West and Midlothian consistently deliver higher grades across broad intercepts.

"Reid continues to deliver, with today's results confirming its substantial potential size and scale and the potential for multiple projects in the Timmins Nickel District. These results also validate the considerable potential identified when the initial resource was published at the end of last year, supported by a 3.9-square-kilometre geophysical target that is more than twice the size of Crawford. We look forward to further demonstrating Reid's scale with an updated resource by year-end." — Mark Selby, Chief Executive Officer, Canada Nickel

Strategic differentiation comes through the NetZero Metals initiative, planning North America's largest nickel processing and stainless-steel facility in Timmins with carbon capture integration via IPT Carbonation to deliver zero-carbon nickel products - a crucial ESG advantage in today's market. This vertical integration strategy positions Canada Nickel to capture value across the entire nickel supply chain while meeting growing demand for sustainably-produced battery materials from Western automakers and battery manufacturers seeking to diversify away from Indonesian and Chinese supply sources.

Sovereign Metals: Dual-Commodity Innovation

Sovereign Metals' Kasiya project in Malawi transforms traditional mining economics through the world's only known deposit where graphite is produced as a by-product of rutile mining. This unique positioning creates compelling investment fundamentals with the world's largest rutile resource (17.9 Mt contained) and second-largest flake graphite resource (24.4 Mt contained). The optimized pre-feasibility study shows exceptional economics: pre-tax NPV8% of US$2.3 billion, 27% IRR, and 64% EBITDA margin with steady-state production of 246,000 tons rutile and 265,000 tons graphite annually. Rio Tinto's 19.9% strategic stake validates both the technical feasibility and strategic value of the dual-commodity approach.

Sovereign's competitive advantage extends to processing economics, with less intensive processing preserving flake size to yield 96-98% carbon concentrate suitable for 94% of natural graphite end-uses. The incremental graphite production cost of US$241/t FOB competes directly with China's average C1 cost of US$257/t, while electrochemical testwork shows Kasiya's coated spherical purified graphite matches or exceeds China's BTR, the leading global battery anode supplier. Environmental credentials provide additional strategic value, with independent life cycle analysis estimating Sovereign's graphite produces just 0.2 tonnes CO2 per tonne versus 1.2 for Chinese natural graphite and 15-25 for synthetic graphite, positioning the company to support EV battery supply chain decarbonization.

Infrastructure development receives strong government backing, creating powerful strategic positioning for project development.

"Japan's commitment to the Nacala Corridor infrastructure validates our strategic positioning and creates powerful opportunities for Kasiya's development. The initiative demonstrates the highest level of government backing for the corridor that underpins our project economics, while Japan's focus on securing critical mineral supply chains aligns perfectly with Kasiya's world-class rutile and graphite resources." — Frank Eagar, Chief Executive Officer, Sovereign Metals.

With the Definitive Feasibility Study targeted for Q4 2025, Kasiya represents a world-class dual-commodity project positioned to supply both titanium feedstock and battery anode materials to global markets.

Gladiator Metals: Whitehorse Belt Copper Discovery

Gladiator Metals has identified significant new copper-gold discovery potential across the historic 35 km Whitehorse Copper Belt in Yukon, a Tier-1 jurisdiction with exceptional infrastructure advantages including road access, grid hydro power, and proximity to skilled workforce in Whitehorse. Recent developments highlight the expanding scope of mineralization, with newly identified skarn and intrusive-related copper-gold zones at both the Valerie trend and Little Chief expansion. The 2.5 km long Valerie trend, highlighted by gravimetric and aero-magnetic geophysics, represents first drilling of a large system previously untested, while Little Chief, historically the belt's largest producer with 8.54 Mt at >1.5% Cu and ~0.75 g/t Au, shows new mineralization south and up-dip of previously mined zones.

The broader Whitehorse project includes multiple advanced prospects demonstrating the belt's substantial potential. Cowley Park features 300+ holes drilled showing shallow Cu-Mo systems with multiple 50-100 meter intercepts grading 1-2% Cu, while the Chiefs Trend shows 2024-25 drilling confirming >500 meter strike with copper-gold grades including 22 meters @ 1.41% Cu, 0.28 g/t Au. Emerging targets Arctic Chief and Best Chance show near-surface high-grade copper intercepts with footprint potential comparable to Cowley Park, reinforcing the belt's capacity for multiple discovery areas across diverse mineralization styles including skarn, intrusive-related, and exoskarn systems.

Strategic positioning benefits from the company's Capacity Funding Agreement with Kwanlin Dün First Nation (October 2024), demonstrating commitment to Indigenous partnership and social license, while current drilling programs total 27,000 meters across multiple targets with plans to advance Cowley Park toward inferred resource by H1 2026.

"With the recent closing of a $22.5M financing plus existing treasury of $8M, Gladiator is fully funded for significant exploration until the end of 2026." — Jason Bontempo, Chief Executive Officer & Director, Gladiator Metals.

This financial runway provides stability to execute systematic exploration across the belt while copper supply fundamentals remain constructive for new discoveries in established mining jurisdictions.

Investment Thesis Framework: Positioning for the Battery Revolution

Theme 1: Supply Chain Security Western governments prioritize domestic processing capacity to reduce dependence on Chinese refining. The average market share of top three mining countries could decline to 2020 levels by 2035, but refining operations will remain highly concentrated in China.

Theme 2: Policy-Driven Demand Unlike commodity cycles driven by economic growth, battery metal demand is mandated by climate policies, EV adoption targets, and renewable energy deployment goals. This creates more predictable, less cyclical demand patterns.

Theme 3: Technology Evolution Battery chemistry evolution affects individual metals differently, with manganese and nickel seeing faster growth while cobalt usage declines in favor of lithium iron phosphate alternatives. Silicon-doped graphite already comprises 30% of anodes, with further innovation reducing traditional graphite intensity.

Theme 4: Early-Stage Supply Response Extended price weakness has forced production cuts, project delays, and workforce reductions across the sector, setting up potential supply shortages as demand accelerates. Benchmark Mineral Intelligence forecasts lithium supply shortages beginning in 2025.

Risk Assessment & Mitigation

Geopolitical Concentration: Supply disruptions could cause fivefold price increases, raising battery costs by 20%, or tenfold increases raising costs by 40-50%. Mitigation strategies include geographic diversification and strategic stockpiling.

Technology Displacement: Innovations like sodium-ion or nickel-metal hydride batteries could reduce demand for specific materials, particularly lithium and cobalt. However, transition timelines suggest decades of continued lithium-ion dominance.

Environmental and Social Governance: Indonesian nickel mining has caused significant environmental degradation, with 76,301 hectares of tropical forest cleared since 2019. Sustainable extraction becomes increasingly important for institutional investment.

The Investment Thesis for Battery Metals

- Prioritize companies with unique competitive advantages - Canada Nickel's district-scale consolidation and zero-carbon processing, Sovereign Metals' dual-commodity by-product strategy, and Gladiator Metals' infrastructure-advantaged copper exploration in a tier-1 jurisdiction.

- Combine exposure to development-stage companies (Canada Nickel, Sovereign Metals), exploration plays (Gladiator Metals), and established diversified miners (BHP, Freeport-McMoRan) to balance risk and return potential across extraction, refining, and manufacturing.

- Focus on companies developing non-Indonesian, non-Chinese supply sources in stable jurisdictions like Canada, Australia, and established mining regions, as geopolitical premiums will likely persist throughout the energy transition.

- Current price weakness following 2021-22 peaks creates attractive entry points for long-term positions, particularly as supply cuts and project delays set up potential 2025-2027 shortages across multiple battery metals.

- Weight portfolios toward companies with environmental advantages (Sovereign's low-carbon graphite, Canada Nickel's NetZero strategy) and universal electrification exposure (copper projects) while maintaining awareness of battery chemistry shifts.

- Major miners offer defensive exposure with dividend yields, advanced developers like Canada Nickel and Sovereign provide leveraged upside to specific large-scale projects, while exploration plays like Gladiator offer highest-risk/highest-reward exposure to new discoveries in established belts.

Key Takeaways & Investor Implications

The battery metals sector represents one of the most compelling secular investment themes of the next decade. Demand growth of 20-40x for key materials, combined with supply chain concentration in politically sensitive regions, creates both substantial opportunity and meaningful risk.

Successful investing in this space requires understanding that this is not a traditional commodity cycle but a structural transformation of the global economy. Policy mandates, not economic cycles, drive demand, while supply responses are constrained by permitting timelines, environmental regulations, and geopolitical considerations.

The current environment offers attractive entry points following significant price corrections, but selectivity matters more than broad exposure. Companies with secure supply sources, established customer relationships, and strong environmental credentials will command premium valuations as the energy transition accelerates.

Most importantly, investors must recognize that battery metals are not merely a play on electric vehicles but on the fundamental rewiring of global energy infrastructure. Grid expansion, renewable integration, and industrial electrification will drive demand even if EV adoption disappoints. This diversified demand base provides more stability than traditional commodity investments while maintaining substantial upside from policy-driven growth.

TL;DR

Battery metals face unprecedented demand growth as electric vehicles and renewable energy reshape global materials consumption. Key metals, nickel, copper, graphite, and rutile, show significant demand growth potential driven by policy mandates, while supply chains remain concentrated in China and Indonesia. Recent price corrections following 2021-22 peaks create attractive entry points despite supply shortages forecast for 2025. Investment opportunities span from major miners (BHP, Freeport-McMoRan) offering diversified exposure to focused developers like Canada Nickel (world's second-largest nickel reserve), Sovereign Metals (unique rutile-graphite dual production), and Gladiator Metals (Whitehorse Belt copper discovery). Policy-driven demand provides more stability than traditional commodity cycles, but geopolitical supply risks require geographic diversification. The energy transition creates a structural, decades-long investment theme.

Frequently Asked Questions (AI-Generated)

Benchmark Mineral Intelligence forecasts lithium supply shortages starting as early as 2025, while copper faces a potential 30% supply shortfall by 2035. However, supply responses to price signals could accelerate if investment momentum returns to 2023 levels.

Indonesia's export restrictions, extended through January 2025, require foreign companies to process ore domestically and limit foreign ownership to 49%. This forces companies to either invest in Indonesian facilities or develop alternative supply sources in countries like Canada and Australia.

Lithium shows the fastest growth trajectory at 40x by 2040, followed by graphite at 25x and nickel at 20x. However, copper provides the most universal exposure to electrification across EVs, grids, and renewable energy infrastructure.

Sodium-ion batteries and solid-state designs could reduce lithium intensity, while silicon-enhanced anodes are already reducing graphite demand by 6%. However, transition timelines suggest decades of continued lithium-ion dominance for most applications.

Focus on companies developing mines in stable jurisdictions (Canada, Australia, US), diversified major miners with global operations, and Western processing facilities. ETFs like the Amplify Lithium & Battery Technology ETF (BATT) or iShares MSCI Global Metals & Mining Producers ETF (PICK) provide broad exposure.

Note: These FAQs are AI-generated based on the analysis above and current market research. Always consult with financial advisors and conduct your own due diligence before making investment decisions.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed