China's Temporary Easing of Graphite Export Controls & the Shifting Global Supply Outlook for Battery Materials

China suspends graphite export controls to US until Nov 2026, easing trade tensions temporarily but reinforcing long-term supply chain risks for batteries.

- China's suspension of enhanced graphite export controls to the United States until 27 November 2026 temporarily eases a key geopolitical bottleneck at the centre of the battery supply chain.

- The policy shift smooths licensing processes and lowers trade frictions, but reinforces long-term uncertainty once the suspension expires in late 2026.

- Near-term trade fluidity supports graphite pricing stability, but structural supply risks remain due to China's dominant role in spherical graphite and battery anodes.

- Non-Chinese developers, such as Sovereign Metals with its Kasiya project in Malawi, offer strategic diversification as Western markets seek alternatives to Chinese supply chains.

- Investors should evaluate graphite exposure through the lens of regulatory volatility, cost competitiveness, and the emergence of low-cost, politically neutral jurisdictions.

A Policy Pause with Global Battery-Supply Implications

Geopolitical tensions between the United States and China have increasingly focused on battery-critical minerals, with graphite emerging as a strategic vulnerability. Unlike lithium or nickel, where supply is globally distributed, China controls approximately 75 percent of natural graphite production and dominates the downstream processing of spherical graphite used in battery anodes. This concentration makes any policy adjustment by Beijing highly consequential for United States and allied battery supply chains.

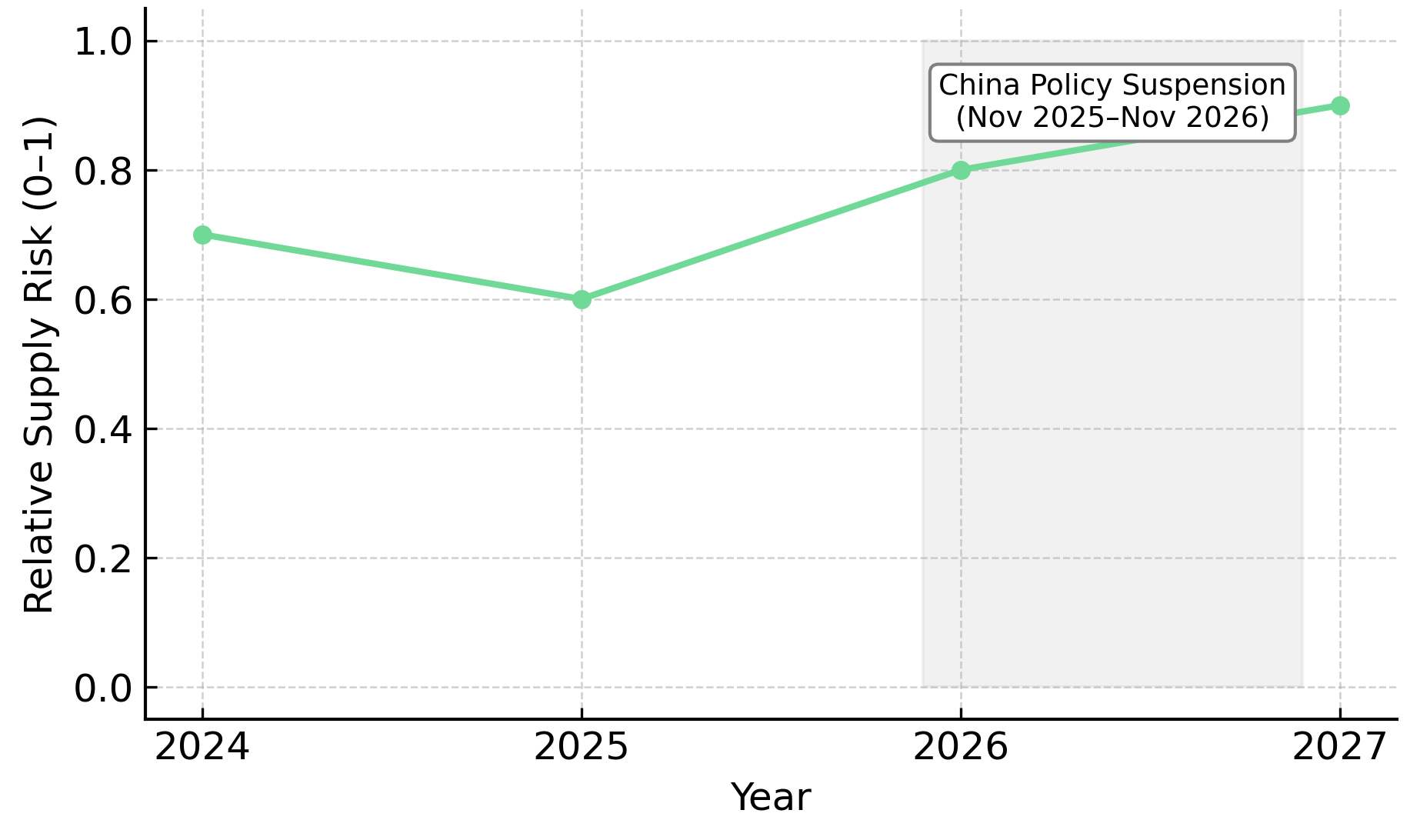

On 9 November 2025, China's Ministry of Commerce issued Announcement No. 72, suspending stricter end-user verification measures introduced in 2024 and temporarily easing export licensing requirements for graphite shipments to the United States. The suspension, valid through 27 November 2026, reduces immediate trade friction but leaves structural supply risks unresolved beyond the expiration date.

This article evaluates how China's regulatory pause affects graphite markets, upstream developers, downstream battery supply chains, and the investment case for non-Chinese graphite assets. The temporary nature of the policy underscores the strategic importance of supply chain diversification and reinforces the premium for low-cost, geopolitically neutral production capacity.

Understanding China's Regulatory Adjustment: Scope, Intent & Expiration Risk

China's November 2025 policy adjustment represents a calculated recalibration of export controls rather than a structural deregulation of graphite trade. Understanding the scope, duration, and strategic intent of Announcement No. 72 is essential for assessing near-term trade flows and long-term supply chain risks.

What Exactly Has Changed in China's Export Regime?

Announcement No. 72 suspends Paragraph 2 of the 2024 export policy, which had imposed enhanced end-user verification requirements on graphite shipments classified as dual-use materials. The suspension simplifies licensing procedures, reduces inspection frequency, and improves predictability for Chinese exporters. Dual-use classification applies to graphite products used in semiconductor manufacturing, aerospace composites, and energy-storage applications, reflecting the material's strategic importance across defense and civilian sectors.

The policy adjustment does not eliminate export controls entirely but rather streamlines compliance processes for shipments to the United States. Chinese exporters still require licenses, but the administrative burden has been reduced, allowing faster processing and lower transaction costs for compliant shipments.

The Temporary Nature of the Policy Window

The suspension is explicitly valid only until 27 November 2026, creating a defined policy window rather than a permanent regulatory shift. This structure preserves China's strategic leverage while reducing bilateral trade friction in the near term. The temporary nature of the policy introduces planning uncertainty for downstream consumers, particularly battery manufacturers operating on multi-year procurement cycles.

Historical precedents exist for temporary relaxations in export controls. China has previously adjusted export restrictions on rare earth elements, gallium, and germanium in response to trade negotiations, only to reinstate controls when geopolitical conditions shifted. The graphite suspension follows this pattern, suggesting that the November 2026 expiration date should be treated as a material risk factor rather than a formality.

Alignment with Broader Trade Diplomacy

The timing of Announcement No. 72 aligns with bilateral consultations between China and the United States held in Kuala Lumpur in recent months. The policy adjustment appears designed to reduce trade tensions while maintaining China's structural control over critical mineral supply chains. By offering temporary relief, Beijing signals willingness to negotiate while preserving the option to reinstate controls if diplomatic conditions deteriorate.

This approach reflects China's broader strategy of using export controls as a geopolitical tool. For investors, this dynamic reinforces the importance of supply chain diversification and the strategic premium associated with non-Chinese graphite sources.

Implications for Graphite Supply Chains & Near-Term Trade Flows

China's export control suspension directly affects global graphite supply chains, particularly the processing pathway from natural flake graphite to spherical graphite to battery-grade anode material. This value chain is almost entirely controlled by Chinese producers, giving Beijing outsized influence over battery manufacturing costs and supply reliability.

Eased export controls lower compliance friction, increase shipment velocity, stabilize near-term supply for United States consumers, and potentially reduce spot-market volatility. These effects are most pronounced in the battery sector, where procurement cycles depend on consistent access to high-purity, low-sulphur spherical graphite feedstock.

Short-Term Relief vs. Long-Term Structural Dependence

The policy easing provides immediate operational benefits for battery original equipment manufacturers and their tier-one suppliers, but it does not reduce structural dependence on Chinese supply chains. China produces approximately 1.2 million tonnes per annum of natural graphite at a weighted average cash cost of 257 United States dollars per tonne, according to Benchmark Mineral Intelligence. This cost advantage, combined with China's dominance in spherical graphite processing, ensures that alternative supply chains must compete on both cost and technical specifications.

Battery OEMs have responded to supply chain risks by diversifying spherical graphite suppliers and increasing demand for low-sulphur, high-purity feedstock. However, the limited availability of non-Chinese natural flake graphite constrains the effectiveness of these diversification strategies. The temporary nature of China's policy suspension reinforces the urgency of developing alternative sources, particularly for large-flake and jumbo-flake graphite used in premium battery applications.

Market Reactions & Pricing Dynamics

The suspension is expected to stabilize pricing bands in the near term by reducing supply uncertainty, but pricing volatility is likely to return as the November 2026 expiration date approaches. Market participants are closely monitoring the premium for large-flake graphite relative to smaller size fractions. Deposits capable of producing high proportions of large and jumbo flakes command pricing advantages due to their suitability for expandable graphite, lithium-ion battery anodes, and other high-value applications.

Strategic Sectors Most Affected: Battery Manufacturing

The battery sector faces the greatest exposure to China's graphite export policies due to the concentration of spherical graphite production and battery anode manufacturing in China. Lithium-ion batteries for electric vehicles and energy storage systems require spherical graphite with high carbon purity, low sulphur content, and consistent particle size distribution.

United States Inflation Reduction Act restrictions increase the urgency of developing non-Chinese graphite sources. IRA tax credits for domestically produced batteries require that critical minerals meet foreign entities of concern rules, effectively limiting Chinese content in qualifying battery supply chains. This regulatory framework creates structural demand for non-Chinese graphite regardless of near-term export control adjustments.

Battery manufacturers are particularly focused on low-sulphur feedstock, typically specified at less than 0.05 percent sulphur content. Sulphur impurities degrade battery performance and require additional processing steps that increase production costs. Natural flake graphite deposits with inherently low sulphur content offer processing advantages and lower downstream capital requirements.

Non-Chinese Graphite Developers Gain Strategic Optionality

China's temporary export control suspension paradoxically strengthens the long-term investment case for non-Chinese graphite developers. While near-term trade friction decreases, the policy reinforces the structural risks associated with concentrated supply chains and highlights the strategic premium for diversified sources.

Sovereign Metals' Kasiya project in Malawi represents a case study in supply chain diversification. The project offers attributes directly aligned with Western battery supply chain requirements: large resource scale, favorable flake size distribution, high-purity concentrate, low sulphur content, and a cost structure competitive with Chinese production.

Sovereign Metals' Kasiya Project as a Case Study in De-Risked Supply

The Kasiya project hosts the second-largest known natural flake graphite resource globally based on publicly disclosed resources. The deposit's flake size distribution includes 57 percent large and jumbo flakes, the size categories commanding the highest market premiums due to their suitability for expandable graphite, battery anodes, and other high-value applications.

Metallurgical characteristics differentiate Kasiya from hard-rock graphite deposits. The graphite occurs in weathered saprolite, a softer host rock requiring lower energy input for liberation compared to fresh crystalline rock. Test work demonstrates that Kasiya graphite can be upgraded to 96 to 98 percent carbon purity using conventional flotation, with sulphur content consistently below 0.02 percent.

The project's economics are further enhanced by its dual-product strategy. Kasiya is structured as a primary rutile operation, with graphite produced as a by-product. Rutile, a titanium feedstock used in pigment manufacturing, generates the majority of project revenue. Based on the Optimised Pre-Feasibility Study published in January 2025, graphite is produced at an incremental cost of only 241 United States dollars per tonne FOB, positioning Kasiya at the bottom of the global graphite cost curve.

Ben Stoikovich, Chairman of Sovereign Metals, emphasized the project's unique positioning:

"The way we think about Kasiya is that it is a primary rutile deposit and the graphite will be produced as a byproduct, in fact it's the only known deposit where graphite is a byproduct."

This by-product structure creates substantial cost advantages. Stoikovich noted:

"Where other projects can't make money in the current market, we'd be selling graphite at a 50% operating margin even if we only sold into the lower value battery graphite market."

Cost Competitiveness in a Market Dominated by China's Low-Cost Base

Kasiya's incremental cost of 241 United States dollars per tonne compares favorably to China's weighted average cash cost of 257 United States dollars per tonne. This cost advantage reflects the by-product structure, favorable metallurgy, and large-flake distribution that commands premium pricing. Cost curve positioning becomes increasingly important as battery manufacturers seek supply chain diversification. Projects capable of competing on cost while offering geopolitical diversification benefits will command strategic premiums in offtake negotiations.

Financial & Development Metrics Investors Should Monitor

Institutional investors evaluating graphite developers in response to China's regulatory shifts should focus on financial metrics that indicate cost competitiveness, capital efficiency, and execution risk.

Core Financial Indicators

Sovereign Metals' Optimised Pre-Feasibility Study for Kasiya provides a representative framework for evaluating graphite project economics. The OPFS estimates pre-tax net present value at 8 percent discount rate of 2.32 billion United States dollars, internal rate of return of 27 percent, and annual earnings before interest, taxes, depreciation, and amortization of 409 million United States dollars. EBITDA margin of 64 percent reflects the low-cost structure enabled by the by-product model. Initial capital expenditure to first production is estimated at 665 million United States dollars.

Development Milestones & Timing Windows

Sovereign Metals is targeting completion of the Kasiya Definitive Feasibility Study in the fourth quarter of 2025. Completion of the DFS will provide updated capital cost estimates, production schedules, and market assumptions, positioning the project for financing discussions and potential construction decisions subject to permitting approvals and financing arrangements.

The project has completed a pilot mining and processing phase, extracting and processing 170,000 cubic metres of material to validate resource assumptions and metallurgical flowsheets. This work reduces execution risk by confirming grade, flake size distribution, and concentrate quality at commercial scale.

Capital Structure & Strategic Shareholders

Rio Tinto holds a 19.9 percent equity stake in Sovereign Metals, established through a 60 million Australian dollar strategic investment in 2023. The investment provides both financial credibility and technical validation. Rio Tinto is involved in technical collaboration through the Sovereign-Rio Tinto Technical Committee, with subject matter experts closely involved in project development.

For institutional investors, Rio Tinto's involvement reduces perceived execution risk and signals confidence in the project's technical and commercial viability. Strategic shareholders of this caliber also facilitate project financing by providing comfort to lenders and joint venture partners.

Geopolitical Considerations, Policy Risk & Supply Chain Security

Graphite supply chains are increasingly shaped by geopolitical tensions, trade policy, and national security considerations. China's temporary export control suspension highlights these dynamics but does not resolve the underlying strategic vulnerabilities driving Western governments to prioritize supply chain diversification.

The November 2026 Deadline as a Structural Risk

The expiration of China's export control suspension creates a defined time horizon for supply chain planning. Battery manufacturers, spherical graphite processors, and anode producers must evaluate whether to treat the suspension as a temporary reprieve or a signal of sustained trade normalization. Historical precedent suggests that China is unlikely to permanently relinquish export control authority over strategically important materials. For investors, this pattern reinforces the structural premium for non-Chinese graphite sources that offer long-term supply security independent of bilateral trade dynamics.

United States Strategy for Graphite Security

The United States Inflation Reduction Act establishes explicit restrictions on Chinese content in battery supply chains eligible for domestic manufacturing tax credits. The foreign entity of concern provisions effectively prohibit Chinese-sourced critical minerals in IRA-qualifying batteries after specified phase-in periods. This regulatory framework creates guaranteed demand for non-Chinese graphite regardless of Chinese export policy adjustments.

Jurisdictional Risk & Corporate Strategy

Environmental, social, and governance considerations increasingly influence battery supply chain decisions. Projects demonstrating strong ESG performance and operating in jurisdictions with transparent regulatory frameworks command commercial premiums in offtake negotiations. Malawi has maintained a stable regulatory framework and established mining code, with Sovereign Metals emphasizing community engagement and land rehabilitation as core elements of the Kasiya development strategy.

The Investment Thesis for Graphite

The graphite sector offers exposure to battery demand growth, supply chain diversification trends, and strategic positioning opportunities arising from China's dominant market position.

- Policy volatility creates long-term structural upside despite near-term easing, as China's temporary suspension reduces immediate trade friction but reinforces the strategic importance of non-Chinese supply chains, particularly as the November 2026 expiration date approaches and Western battery manufacturers seek guaranteed long-term supply security.

- Non-Chinese supply remains scarce relative to battery demand growth trajectories, with Kasiya's combination of resource scale, low production cost, high-purity concentrate, and favorable flake size distribution creating scarcity value in a market dominated by Chinese producers operating at higher cost points.

- Battery demand growth trajectories remain robust across multiple scenarios, driven by electric vehicle penetration, grid-scale energy storage deployment, and IRA compliance requirements for battery-grade graphite independent of near-term economic cycles.

- Global cost curves favor large, low-sulphur deposits with favorable metallurgy, as saprolite-hosted graphite deposits with inherent low-sulphur characteristics and simple processing requirements offer capital efficiency advantages over hard-rock deposits requiring complex purification.

- Strategic partners provide execution de-risking and financing credibility, with Rio Tinto's equity position in Sovereign Metals validating the technical and commercial merit of the Kasiya project while improving access to development capital and technical expertise.

A Temporary Policy Pause Reinforces Long-Term Supply Chain Realignment

China's suspension of enhanced graphite export controls to the United States through November 2026 represents a tactical adjustment rather than a strategic shift in Beijing's approach to critical mineral trade. The policy provides near-term operational relief for battery manufacturers and reduces immediate supply chain friction, but the temporary nature of the suspension ensures that long-term structural risks remain intact.

Investors should view the export control suspension as a pressure valve that temporarily reduces bilateral trade tensions while preserving China's strategic leverage over global graphite supply chains. The November 2026 expiration date creates a defined planning horizon during which Western battery manufacturers, spherical graphite processors, and anode producers must secure alternative supply sources or accept continued dependence on Chinese exports subject to future policy adjustments.

The investment case for large-scale, low-cost, geopolitically neutral graphite projects strengthens in this environment. Projects like Kasiya offer exposure to battery demand growth while providing strategic diversification from Chinese supply chains. The combination of bottom-quartile cost positioning, battery-grade product specifications, and alignment with Western supply chain security priorities creates a differentiated value proposition for investors seeking exposure to the energy transition without accepting concentrated geopolitical risk.

TL;DR

China has temporarily suspended enhanced graphite export controls to the United States until November 27, 2026, reducing immediate trade friction in the battery supply chain. While this eases short-term licensing burdens, it doesn't resolve underlying structural risks, as China controls 75% of natural graphite production and dominates spherical graphite processing for battery anodes. The temporary nature of this policy reinforces the strategic importance of supply chain diversification. Non-Chinese developers like Sovereign Metals' Kasiya project in Malawi offer crucial alternatives, combining low production costs, high-purity concentrate, and geopolitical neutrality. As the 2026 expiration approaches, Western battery manufacturers must secure alternative sources or remain dependent on Chinese supply chains subject to future policy changes.

FAQs (AI-generated)

China issued the suspension to reduce bilateral trade tensions while maintaining strategic leverage, aligning with broader trade diplomacy efforts during recent consultations between the two nations.

The suspension is valid until November 27, 2026. It's explicitly temporary, not a permanent policy shift, creating planning uncertainty for battery manufacturers operating on multi-year procurement cycles.

Graphite, specifically spherical graphite, is essential for lithium-ion battery anodes used in electric vehicles and energy storage. China dominates approximately 75% of natural graphite production and nearly all spherical graphite processing.

Non-Chinese developers like Sovereign Metals' Kasiya project in Malawi offer strategic diversification with competitive costs, high-purity concentrate, low sulfur content, and favorable flake size distribution suitable for battery applications.

The IRA restricts Chinese content in battery supply chains eligible for tax credits through "foreign entity of concern" provisions, creating structural demand for non-Chinese graphite sources regardless of China's export policy adjustments.

Analyst's Notes

Subscribe to Our Channel

Stay Informed