Cobalt Blue (COB) - Cobalt Sector Heating Up & Cash Costs Coming Down

Cobalt Blue Holdings Limited is a cobalt exploration and development company. The Company is focused on developing the Broken Hill Cobalt Project in New South Wales.

Cobalt Blue Holdings is a cobalt exploration and development company. The Company is focused on developing the Broken Hill Cobalt Project in New South Wales, Australia.

We caught up with Joe Kaderavek, CEO of Cobalt Blue Holdings to talk about the progress during 2020 and his forecast for the company and the cobalt sector for 2021.

Company Overview

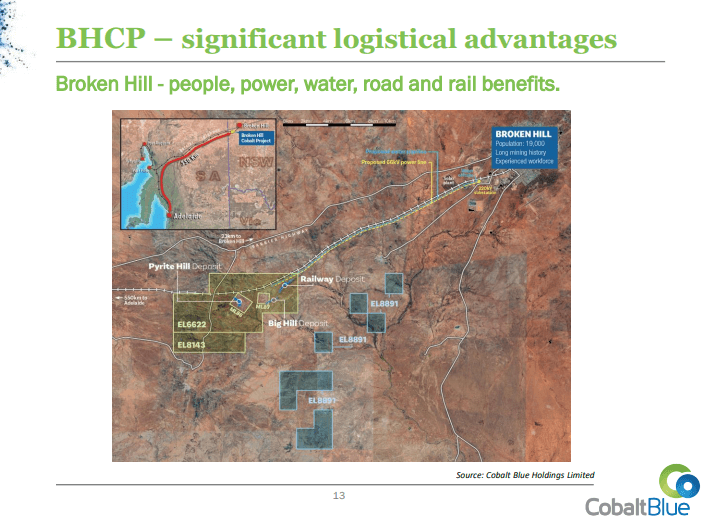

Cobalt Blue is a 100% owner of the Broken Hill Cobalt project located in the safe and stable jurisdiction of New South Wales, Australia. Broken Hill is a very large integrated mine concept, looking to make 3,000t Cobalt metal, which is just under 18,000t Cobalt Sulphate, during a 20-year mine life. The Cobalt Sulphate will be used to make a high purity battery and Cobalt Blue will be finalising the Feasibility Study in the next 2 years which demonstrates the metallurgical process. In parallel with that the company is running a number of commercial partner pilot programmes to determine and provide a commercial supply relationship.

Kadervek is meticulous character. And one that instills confidence when grilled about that state of the market and how Cobalt Blue intends to navigate it. He is an ex banker and analyst with a technical background, so it interesting to note that he has spent time to clean up the corporate structure of the company and has taken advantage of some of the govt grants available to minimise shareholder dilution that this stage of development.

The Future for the Cobalt Market

There are different use cases for batteries, and therefore there will be different designs and different constructs to suit those use cases. There is a narrative that cobalt is being phased out of batteries because it is expensive, and also, a thought that cobalt is not actually required for the electro-motive properties of the battery. The reality is that there is only so much you can remove from a battery as it keeps it stable. In some batteries, for example in the more commoditized EV's such as hybrids, where battery weights and scale don't really matter, you can get away with non-cobalt batteries and their inherent lower-energy densities. However, in the mass market, particularly in cold climates (non-cobalt batteries don’t work as well in cold temperatures), a cobalt cathode is needed for the mid to upper-range vehicles,

Because cobalt has different uses and different automotive manufacturers use different types of battery designs, just under 60% of cobalt demand goes into batteries, which is chemical cobalt, the remaining 40% is used in super-alloys, which are effectively cobalt as an additive to Steels, Aluminium aircraft-grade frames, gas turbines, etc.

Looking forward, the cobalt required for some of those industries may reduce but the cobalt-battery industry is rapidly expanding. EVs will have a much broader range of products and a much higher quality of product led by infrastructure rollouts, and more recently, EV subsidies. The big 40-50Kwh batteries are going to require a lot of cobalt.

The other part of the battery industry is consumer goods such as phones and laptops etc which follows GDP growth rates. The small but rapidly growing part of the battery industry is energy storage systems in utility, but also household-scale storage, particularly for photo-voltaic or wind turbines.

Post Covid, the EV manufacturers are now starting to forecast elevated sales, particularly from 2022-23 onwards due to the subsidies available. These predictions transfer demand to the battery manufacturers and upstream to the precursor cathode manufacturers which leads to demand for cobalt from the producers. Cobalt Blue is now starting to receive requests for additional supply based on 2022-23 predictions for EVs.

2020 Review: Progress Made, Problems Solved

In 2020, Cobalt Blue completed the purchase of the Broken Hill Cobalt project and now have 100% ownership. 2020 was a difficult year for cobalt as the market demand for cobalt collapsed in Q2/20 in response to Covid and the fears by industry participants over its future.

On the funding side, the company has secured over AUD$2M in grants through the CRC project from the Australian government which thinks there is potential to extract Cobalt from other pyrite deposits or tailings in South Australia and Queensland.

Cobalt Blue is now a member of the Future Battery Industry CRC, which is a collaborative group of some big participants in the battery industry. Their contribution to the FBI CRC is with Cobalt in the NCM precursor trial facility as they're looking to make a precursor in Australia.

Following a scoping report the company has been granted the ability to start the state-significant development approval process in New South Wales which is a fast-track process to get into development. They have delivered technical benchmarks for two new products. The first is an intermediate product, an MHP, a mixed Hydroxide, which enables them to make a Cobalt-rich MHP. Most MHPs are Nickel rich, and typically, a 22-25:3 ratio of Nickel to Cobalt. This new ratio is 37% Cobalt and 7% Nickel, so is cobalt rich and valuable in its ability to blend in the cathode. They also produced a benchmark Cobalt Sulphate product which is the precursor-ready high spec product at a 20.8% Cobalt purity.

During mid-2020, Cobalt Blue delivered a project update, which enhanced and cost-optimized the PFS. The capex was dramatically reduced and opex significantly improved for the C1 cost for Cobalt Sulphate at AUD$9.00, and the All-in Sustaining Cost for the Cobalt Sulphate at AUD$12. This makes them very competitive.

The pilot plant at Broken Hill has recently received new items of equipment including reactors, tanks, filters, pumps and spirals. The pilot plant will inform the Broken Hill Feasibility Study as well as supply cobalt product samples to the global sample partner program. The plant is nearing completion and will be commissioning within the next 3-4 weeks.

The ESG component of mining especially EV commodities is critical as funds and OEMs start to demand track & trace into the supply chain management and accountability. Non DRC Cobalt will be no less scrutinised. Cobalt Blue had a community day at Broken Hill in mid-December and invited 50 of the local community, project supporters, council members, business members and other interested citizens. The project is well received locally and the company is well placed for future interaction with the community and local businesses there.

Contracts with Potential Partners & Improving Economics

A strategic partner is important to Cobalt Blue specifically for further cost optimisation and their ability to prove on scale improved recoveries from this point forward. They have assumed an 85% recovery from inground to payable but realise that number on the lab bench can go as high as 90% and are hopeful that they can increase 1-3% more from their current position. There are a number of options on energy optimization such as potentially sourcing gas, which is a big infrastructure issue at Broken Hill. If gas is sourced from the movement to the Adelaide pipe, about 250km away, the energy costs will reduce significantly and energy is a big factor at about 23% of the cash cost. The right partner will enable the scale and rigour of test work that the additional capital and focus will provide.

Cobalt Blue also needs to focus on producing the right product as different battery manufacturers require different purity specs so they need to produce the relevant spec whilst optimizing the cost inputs. With the right partner they can look at capital additions such as the gas pipeline to produce a lower-cost product and a better quality of product which is aligned with market requirements for the next 5-10 years.

Finding the 'right' partner for the business is a really important decision for Cobalt Blue. The ideal partner would be interested in sharing project equity and ownership, with which there will be a commensurate offtake. With equity, the onus will be on the partner to create a balance sheet to help Cobalt Blue guarantee their own portion of equity going forward. They are currently working to understand the next steps and to construct a commercially attractive package for a partner. Cobalt has a small market with few potential partners and the ethical and green component is important to consider too as it is a big part of the Cobalt Blue proposition.

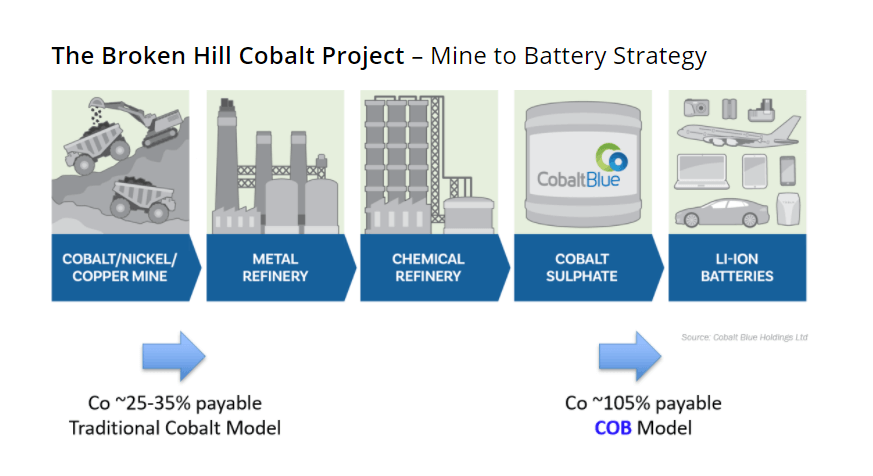

The Cobalt Blue strategy plans to integrate the mine refinery and make a sulphate, to avoid the middleman refining complex that exists predominantly in China. 80% of intermediate Cobalt is refined in China. Cobalt Blue aims to keep the margin and instead of selling a 20% Cobalt payable product want to sell an 80%-90% product. That commercially allows the company to deal directly with battery manufacturers in Europe, Korea and Japan. The commercial strategy to bypass the Chinese refining industry has been a good decision considering what is happening at the moment with Australian and Chinese relations.

Timeline & Timing: Will They Hit the Cycle Right?

Technically, the timeline between a potential customer receiving a sample and making a long term purchasing decision is 12-18 months to qualify as a supplier for a major precursor and cathode company. As a cobalt producer, the product needs to be repeatable at scale and precise quality. The impurities, crystallography, the Sulphate margin, the consistency are all vital for consistency. Cobalt Blue will start putting the product to the market on the pilot scale and later next year will have a much larger demonstration plant, which will allow battery companies to make physical test batteries from that product which is the final technical hurdle to get into that pre-qualification.

Looking at the market balance, there is some current stock to get through so prices are unlikely to increase much this year. Cobalt demand is likely to have much more impact on supply and price from 2023 onwards when the scarcity factor comes in. Cobalt Blue are expecting to be in production commercially within 12 months so are aiming to hit the market at the right time.

Ethical Investing VS Minimizing the Supply-Demand Gap

At the point when supply cannot meet demand, there is an acceleration of thrifting, for example, certainly on the non-battery side, the lower economic value side, the hard facing tools, the magnetic tools, the dyes, etc will start to go elsewhere. 40% of today's market has some substitutability. In terms of substitution within the batteries themselves, on the energy storage side you can go to an LFP formulation, or a flow battery. In consumer electronics given the AUD$0.10-0.15c worth of Cobalt contained in an iPhone, it’s unlikely to be substituted. With the EV market, substitution is difficult as consumers may not be happy to take risk on a lower-quality LFP battery to try and save AUD$500 - $1,000 off the purchase price.

In terms of industry participants and market dynamics, customers have for a number of years signalled their ability to pay a premium for ethical sourcing and low carbon footprint. These target products have now become more mainstream as consumers continue to demand a lower carbon footprint, the industry’s demands are now there. Cobalt benefits from the decarbonization angle and Cobalt Blue also from the ethical sourcing side. They can prove source and providence so will ultimately get a premium for their product that the battery manufacturer can prove an ethical source of Cobalt to a consumer electronics business or an EV business.

Money Matters: Cash Position, Burn Rate, & Raises

Cobalt Blue identified long lead-time items for the pilot project which was effectively their leaching autoclave circuit. It was designed in mid-2019 and ordered in Q4/19 and they're on track for commissioning in late February.

The capital raise in Q3/20 was entirely to complete the pilot plant. They then want to expand to a larger demonstration scale costing around AUD$10M, of which AUD$2.5M has already been spent locally. Another AUD$7.5M will get to a 2t-3t proof in terms of production of the intermediate Sulphates. That amount of money will get them through 2021 and tick all the boxes including a Feasibility Study and also go towards their commercial de-risking. Cobalt Blue will be looking for a partner to help with the funding and to get all the way through the Feasibility Study towards production.

We look forward to hearing more about the Cobalt Blue story in the near future as we are spending a lot of time in the Cobalt space at the moment. It's getting exciting and 2021 looks to be an interesting year for Cobalt.

To find out more, got to Cobalt Blue Holdings' Website.

Analyst's Notes

Subscribe to Our Channel

Stay Informed