Copper: Investing Gains Through Supply Shocks

Copper’s deep-mine risks, tight inventories and 2030 demand growth create volatility—and opportunity—for investors amid shifting geopolitics and policy.

- Deep-mine seismic risk is rising as operations move deeper and production rates increase - recent disruptions at El Teniente (Chile) and Kamoa-Kakula (DRC) show how quickly supply can be knocked offline.

- Inventories at major exchanges tightened and reshuffled through mid-2025; LME copper stocks fell ~65% YTD by late June, amplifying price sensitivity to outages.

- The structural demand story - power-grid build-out, EVs and (increasingly) data centers - keeps strengthening into 2030, with some forecasters now calling a ~1.8 Mt deficit by 2030 if mine growth lags.

- Policy and geopolitics are now central to copper: Chilean regulators are scrutinizing Codelco’s restart; the US, India and Argentina are maneuvering to secure supply chains and infrastructure.

- Near-term balances can flip month-to-month (e.g., April 2025 deficit) even if YTD shows a small surplus - underscoring how unplanned outages swing the market.

Copper’s Supply-Shock Problem: The Macro Bull Case

Copper is the wiring of electrification: from grid transformers and renewables to EVs and - more recently - AI-hungry data centers. That secular demand story collides with a more fragile supply reality as the world’s highest-quality deposits age, grades fall, and mines push deeper underground. In 2025, two events crystallized this tension.

First, Chile’s state miner Codelco suffered a fatal tunnel collapse at El Teniente—the world’s largest underground copper operation - suspending underground output while authorities launched investigations and Codelco reshuffled leadership and pursued a phased restart. Second, the Kamoa-Kakula complex in the Democratic Republic of Congo (DRC) suspended portions of mining following seismic activity and flooding before partially resuming operations and cutting 2025 guidance. Both incidents reinforced how sensitive copper supply has become to geotechnical and seismic factors.

At the same time, exchange inventories tightened and shifted geographically as tariff noise and arbitrage flows distorted traditional trade routes. The result: a market more prone to price spikes when any major mine hiccups.

This article lays out the investable logic: the micro (operational and safety risks), the meso (country and policy risk) and the macro (electrification demand and strategic re-shoring). We ground the analysis in the current news flow, independent datasets, and industry-standard sources - including the International Copper Study Group (ICSG), Reuters and the IEA -plus your supplied transcript.

Market Overview: Balances Look “Small", but Shocks are Getting “Big”

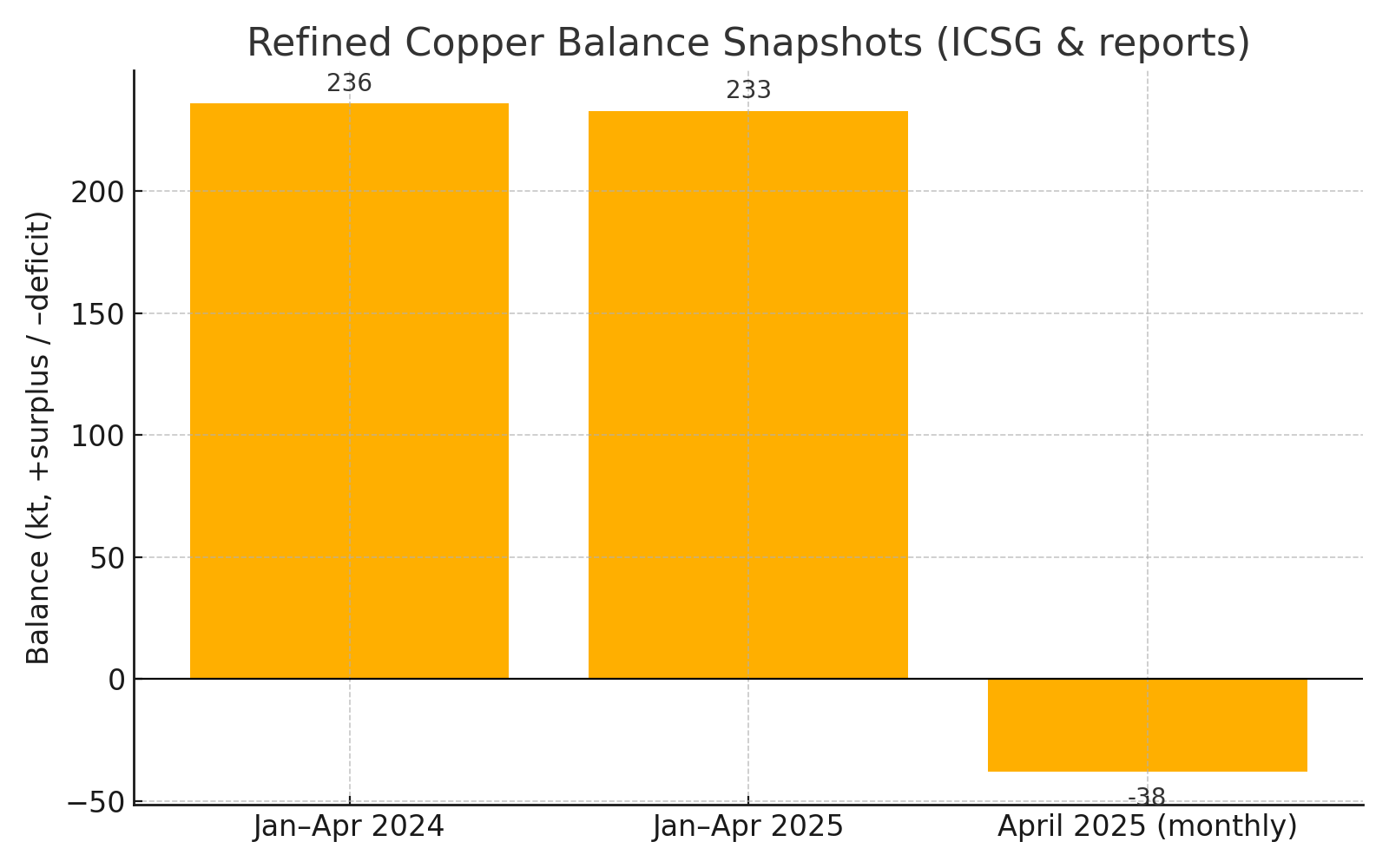

The copper market can swing from surplus to deficit on surprisingly short timelines. ICSG-based reporting shows that, through the first four months of 2025, the refined copper market posted a cumulative surplus of ~233 kt - similar to the same period of 2024. Yet April alone flipped to a deficit (~38 kt), highlighting how a single month can move the needle. Our second chart (below) illustrates this “calm surface, choppy current” reality.

Meanwhile, the plumbing of the physical market tightened and morphed. LME copper stocks fell ~65% YTD by late June, with available tonnage down to two-year lows - an illustration of how metal moved out of traditional hubs as tariff-driven arbitrage rerouted flows. That redistribution increased the market’s sensitivity to any new outage at scale.

What this means for investors: headline balances can appear benign, but they mask a system primed for volatility. When inventories are thin and unevenly distributed, operational shocks transmit into prices faster.

Deep-Mine Seismic Risk: When Geology Meets Throughput

Two recent disruptions bookend the risk set:

- El Teniente (Chile). After a fatal collapse killed six workers, Chilean authorities forced underground operations to halt pending investigations. Prosecutors later said 3,700 m of tunnels were damaged - far above initial estimates. Codelco began partial restarts but also replaced the mine’s general manager under mutual agreement. The company’s smelter was awaiting concentrate to resume operations, a reminder of how mine-level disruptions ripple into downstream assets.

- Kamoa-Kakula (DRC). Following tremors and flooding in May, Ivanhoe Mines partially restarted mining in June but cut 2025 output guidance to 370–420 kt, down from a prior 520–580 kt range. The company also withdrew a 2026 target, signaling longer-tailed effects.

From a technical perspective, seismicity and rock-burst risks typically climb as mines go deeper and as high-tonnage, high-stress stopes are cycled faster to meet demand. That risk is compounded in geologically complex, fault-prone orebodies. As one London brokerage framed it: “expect more earthquakes at copper mines around the world as faster mining rates release geotechnical tension… Kamoa and now El Teniente - who’s next?” The list of deep, high-altitude, technically challenging giants - Chuquicamata, Escondida, Grasberg - underscores what’s at stake if another Tier-1 asset stumbles.

Your transcript adds critical context: analysts estimated El Teniente alone could lose ~27 kt per month during a shutdown; ANZ noted unplanned global outages rising from just under 5% of world copper production in 2014 to ~5.7% last year, with >6% forecast this year - consistent with a world of deeper mines and falling head grades.

Investor angle: when single-asset disruptions can measure in tens to hundreds of kilotonnes, portfolios should price tail risk explicitly - via jurisdictional diversification and balance-sheet resilience (see “Investment Thesis” below).

“Expect more earthquakes at copper mines around the world as faster mining rates release geotechnical tensions… Kamoa and now El Teniente - who’s next?” The firm’s long track record covering mining equities gives this warning weight across both majors and juniors. - SP Angel, London Broker

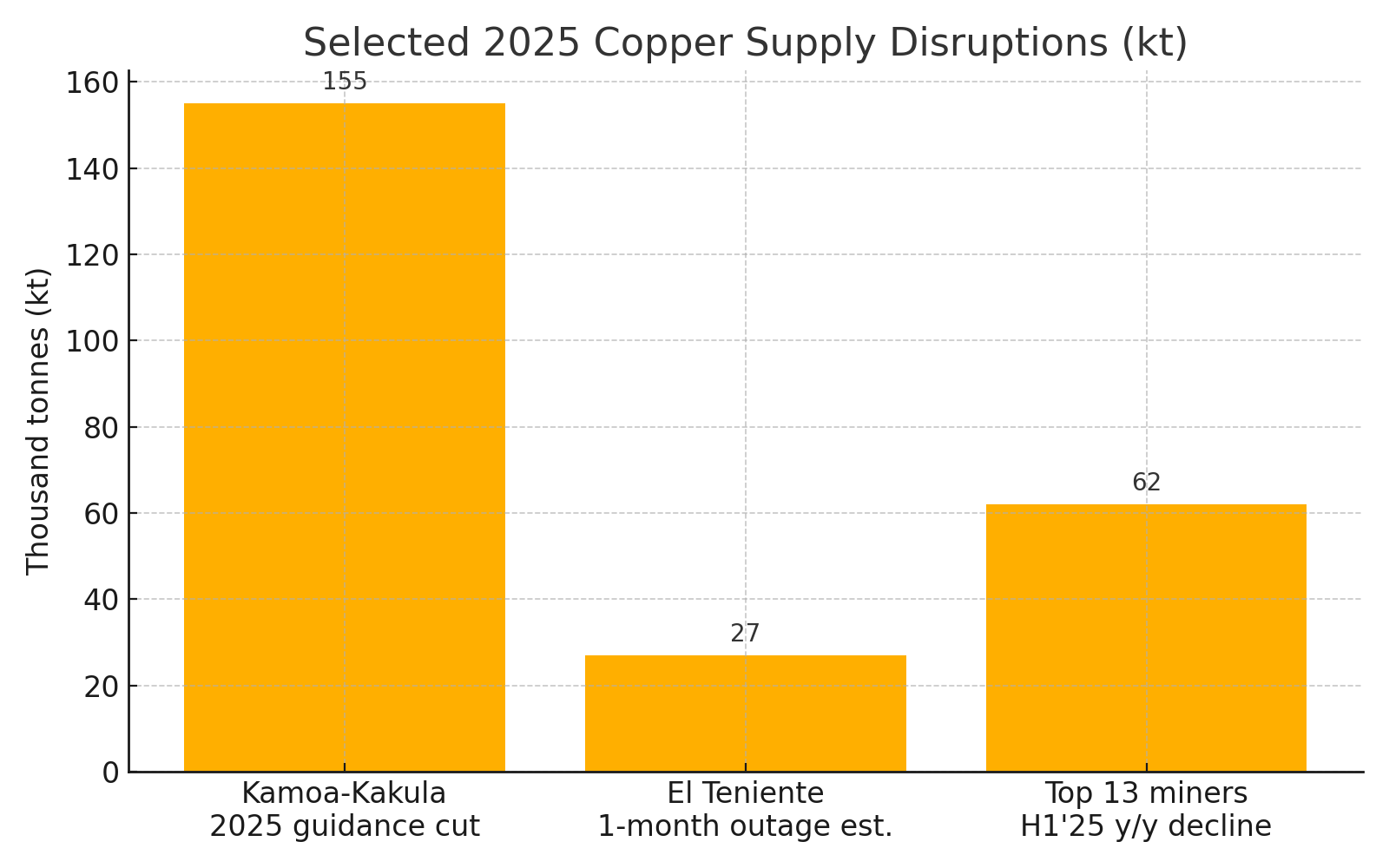

Charting the Supply Shocks: Selected 2025 Losses

To make the risk more tangible, our first chart compares three data points that investors can track in real time:

- Kamoa-Kakula 2025 guidance cut (midpoint reduction ≈155 kt vs. prior range).

- El Teniente estimated one-month loss at ~27 kt (from transcript/ANZ).

- Top-13 miners H1’25 combined output -62 kt YoY (ANZ, per transcript).

Takeaway: any single event can move the refined balance materially— - even in a year that prints a modest YTD surplus.

Prices, Spreads & Inventories: What the Tape is Telling Us

Copper rallied into mid-year and was set to close H1 with ~12% gains on the LME, a move accentuated by tariff-induced dislocations that briefly created feast-or-famine pockets across regions. Shanghai Futures Exchange stocks also fell to their lowest since December as exports surged, while U.S. and LME prices converged again after Washington narrowed its copper tariff plan to semis (wires, pipes) rather than refined or ore. These policy zig-zags help explain why inventories drained from some hubs even as global supply wasn’t collapsing.

For positioning: watch inventories by region, not just the global total. Local scarcity often leads the next leg in spreads and premia.

Demand Pillars to 2030: Power Grids, EVs, and Data Centers

On the demand side, three pillars matter:

- Power grids. The IEA estimates grid investment to exceed $400 bn in 2025 (from a record $390 bn in 2024). BMI projects copper demand for grid infrastructure to rise from 12.5 Mt in 2025 to ~14.9 Mt by 2030.

- Electric vehicles. Multiple analyses continue to see EV copper intensity supporting sustained growth through 2030; the IEA’s critical minerals work situates copper as core to clean-energy value chains.

- AI/data centers. As hyperscale campuses proliferate, copper is taking share from short-run optical links due to cost and power efficiency; JPMorgan analysis cited by industry press suggests ~2.6 Mt of incremental copper demand by 2030 from data centers—about 2% of global demand that year.

Add them up and forecasters such as Bank of America see total copper demand ~30.3 Mt by 2030, with a 1.84 Mt market deficit unless supply accelerates.

Investor implication: these are multi-cycle drivers. Even when cyclical sectors (construction, appliances) wobble, secular loads from grids/EVs/data centers can keep the floor under demand.

Policy & Geopolitics: Where Copper Meets Statecraft

Copper is now squarely in the “strategic materials” bucket:

- Chile. After El Teniente’s accident, prosecutors disclosed damage to 3.7 km of tunnels; regulators demanded detailed reports before approving a restart - delays that affect not only mine output but smelter runs. Leadership changes at the mine highlight heightened accountability and safety focus.

- United States. Tariff signaling initially distorted the global flow of refined metal toward U.S. shores; subsequent narrowing of tariff scope (to semis) helped bring U.S. prices back toward parity with LME. Policy still matters: permitting cadence and mid-stream investments (e.g., smelting) could alter North American supply resilience over the decade.

- India. New policy aims to attract foreign copper miners and expand domestic smelting/overseas tie-ups, a hedge against heavy import reliance as demand rises.

- Argentina. Ambitions to scale copper hinge on who funds and builds enabling infrastructure - roads, power and ports - and under what terms, a reminder that capex bottlenecks can be geopolitical as much as geological.

- Global concentration. The IEA warns that mining and (especially) refining are concentrated in a handful of countries - China, above all - raising exposure to trade or policy shocks across critical minerals, copper included.

Why this matters: policy “surprises” can whipsaw premia, flows and capex incentives. Investors should track regulatory calendars in producer countries and trade-policy signals in consuming blocs.

ESG, Safety & Social License: Costs & Consequences

Even apart from seismicity, ESG risks - tailings management, water, power sources - and community relations can halt projects. Chile’s regulatory posture post-accident demonstrates how safety can trump short-term output targets. The reputational and financial costs are severe if companies cut corners; conversely, best-in-class operators secure smoother restarts and financing.

Practical screen: demand evidence of independent geotechnical audits, water/tailings disclosures, and contingency plans for power and logistics. Diversify away from single-asset, single-jurisdiction exposure when possible.

What the Numbers Say

Refined market snapshots: YTD surpluses can coexist with monthly deficits - and that’s without assuming another “Tier-1” outage.

Selected disruption scale: 2025 guidance cuts at Kamoa-Kakula (~155 kt midpoint) dwarf a one-month shutdown at a large underground mine like El Teniente (~27 kt), and even exceed the combined YoY H1 decline of the top-13 producers (~62 kt) cited by bank analysts.

"Executive-level messaging across IEA publications stresses that supply concentration and under-investment in critical minerals could jeopardize the energy transition - copper chief among them. Investors should read these as policy direction signals as much as market forecasts." IEA

Putting it Together: Portfolio Strategy

- Blend duration: anchor with low-cost, multi-asset producers for resilience; pair with selective development names where permitting, power and water are de-risked.

- Diversify jurisdictions: consider exposure beyond the Andes/DRC axis into North America and parts of Asia with stable regulatory regimes.

- Track safety/ESG: insist on transparent geotechnical and tailings reporting; incidents are both moral tragedies and significant value-at-risk.

- Use volatility: inventory squeezes + outages = entries for patient capital; consider layering in on operational headline dips when balance sheets and geology remain intact.

- Watch policy calendars: tariffs, smelter incentives, and permitting reforms can re-price regional premia quickly (and sometimes reverse just as fast).

The Investment Thesis for Copper Exposure

- Secular demand uptrend from grids, EVs, and data centers underwrites medium-term growth toward ~30 Mt demand by 2030.

- Tighter and uneven inventories magnify price response to disruptions - shortages can emerge locally before the global data shows it.

- Operational fragility at deep, high-throughput underground mines raises the probability of non-linear supply shocks (El Teniente; Kamoa-Kakula), making new development capacity increasingly valuable.

- Near-term development optionality:

- Marimaca Copper offers a low-capex, near-surface oxide project in Chile that could deliver faster-to-market supply.

- Fitzroy Minerals targets small but ultra-high-grade deposits with potential for rapid development and strong margins in a high-price environment.

- Long-life, district-scale growth:

- NGEX Minerals (Los Helados, Lunahuasi) and Atex Resources (Valeriano) control large porphyry systems in the Andes with multi-decade production potential, though requiring significant capex and altitude management.

- Exploration and jurisdictional diversification:

- Firefly Resources adds Australian copper exploration exposure in under-developed districts.

- Hawk Resources advances copper-gold projects in Utah, USA, blending brownfield potential with stable jurisdictional risk.

- Policy-driven volatility (tariff scopes, safety reviews, restart approvals) can create trading opportunities but also long-tail risk.

- Actionable steps: monitor restart milestones at El Teniente; track Ivanhoe’s dewatering and stope sequencing; follow permitting and financing developments for Marimaca, NGEX, Atex, Firefly, Hawk, and Fitzroy.

- Risk controls: diversify across jurisdictions and lift exposure to integrated operators with flexible smelting/marketing alongside selected developers.

- Catalysts: large project financings, permitting breakthroughs, or another Tier-1 disruption.

Copper sits at the junction of unavoidable demand growth and increasingly tricky supply. In 2025, operational incidents at El Teniente and Kamoa-Kakula demonstrated how even world-class assets are vulnerable to seismic and geotechnical stresses. Exchange inventories tightened and shuffled, turning local scarcities into global price volatility, while policy shifts - from safety mandates to tariff tweaks - re-routed trade flows.

Against this backdrop, the project pipeline is critical. Marimaca Copper (Chile) offers near-surface oxide resources with a relatively low capital intensity, potentially positioning it as a near-term supplier into a high-price environment. NGEX Minerals (Argentina/Chile) continues to advance its Los Helados and Lunahuasi discoveries - high-altitude, large-scale resources that could define the next generation of Andean copper. Atex Resources is progressing the Valeriano project in Chile, a large-tonnage porphyry system with gold credits, while Firefly Resources (Australia) is exploring for copper in under-developed jurisdictions, giving investors leverage to exploration upside. Hawk Resources brings North American exposure with Utah copper-gold projects in historic districts, and Fitzroy Minerals targets small but ultra-high-grade deposits that can move rapidly to production, offering asymmetric returns in the right price environment and the potential to fund the exploration of its larger deeper copper sulphides.

For investors, blending these development stories with established producers offers both optionality and resilience. With careful project and jurisdictional selection, copper remains one of the most compelling cyclical-meets-secular themes in global commodities.

Why Invest in Copper

The global energy system is undergoing a once-in-a-century rebuild. Copper is the capillary network that makes it possible. The IEA’s critical-minerals work repeatedly flags two truths: (1) copper demand from clean-energy technologies is set to climb across all scenarios; and (2) mining and refining are highly concentrated, particularly in China, magnifying the risk of policy or logistics shocks. In 2025, power-grid investment is likely to top $400 bn; copper demand tied to grid infrastructure alone could climb from ~12.5 Mt in 2025 to ~14.9 Mt by 2030. Add EVs and data centers (with some estimates pegging 2.6 Mt of incremental copper by 2030), and the decade’s macro picture remains demand-positive even if broader manufacturing cycles wobble.

Set against this is the supply reality. The best deposits are older and deeper; grades are sliding, capital costs are higher, and social-license scrutiny is tighter. The El Teniente and Kamoa-Kakula episodes show the industry’s low tolerance for missteps when inventories are thin and financial markets are skittish.

Geopolitically, states are moving: the U.S. tinkers with tariffs and permitting; India courts foreign miners and smelters; Argentina seeks infrastructure partners. Meanwhile, Chile’s post-accident oversight signals tighter safety-first regimes. Each policy move nudges flows, premia and capex - making copper as much a macro-policy asset as a metal. For investors, the thematic is durable: scarce, strategic, and central to electrification - with volatility you can plan around.

Notes on the visuals

Figure 1 – Selected 2025 Copper Supply Disruptions (kt): compares Kamoa-Kakula’s midpoint guidance reduction (~155 kt), El Teniente’s one-month outage estimate (~27 kt), and the H1’25 YoY decline for top-13 miners (~62 kt). Sources: Reuters for Kamoa-Kakula guidance cut; ANZ/transcript for El Teniente monthly loss and H1 aggregate.

Figure 2 – Refined Copper Balance Snapshots: shows Jan–Apr 2024 surplus (~236 kt), Jan–Apr 2025 surplus (~233 kt), and April 2025 monthly deficit (~38 kt). Sources: ICSG-based reporting.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed