Regulatory and Cost Pressures Accelerate Shift to Synthetic Rutile & Strategic Repricing of Natural Rutile Assets

ESG rules & higher rates drive shift to synthetic rutile, repricing natural assets. Sovereign's Kasiya offers Tier-1 scale amid supply chain disruption.

- Stricter global environmental and labor regulations are accelerating the adoption of synthetic rutile, compressing traditional pricing spreads between natural rutile and ilmenite feedstocks.

- Deglobalisation trends and tariffs on Chinese and South African imports are reshaping supply chains, increasing premiums for secure and traceable sources of rutile and synthetic feedstocks.

- Sovereign Metals' Kasiya project in Malawi, backed by Rio Tinto, represents a jurisdictionally stable Tier-1 asset with dual exposure to rutile and graphite, offering resilience in a high-cost financing environment.

- Natural rutile scarcity continues to underpin premium pricing, but substitution pressures from synthetic rutile and upgraded ilmenite are changing long-term demand patterns.

- Investors must evaluate exposure across natural and synthetic rutile projects, balancing geopolitical risk, ESG alignment, and capital efficiency to capture upside in a structurally constrained titanium feedstock market.

ESG Compliance & Trade Tensions Transform Titanium Supply Dynamics

The global titanium feedstock market is experiencing a fundamental restructuring as regulatory pressures, monetary tightening, and supply chain disruptions converge to reshape demand patterns between natural and synthetic rutile. This transformation is creating both challenges and opportunities for investors evaluating exposure to critical mineral projects across diverse jurisdictions.

Stricter global environmental and labor regulations are accelerating the adoption of synthetic rutile, compressing traditional pricing spreads between natural rutile and ilmenite feedstocks. The regulatory environment now favors producers capable of demonstrating enhanced environmental, social, and governance compliance, particularly in markets where traceability and carbon footprint transparency command premium pricing.

Deglobalisation trends and tariffs on Chinese and South African imports are reshaping supply chains, increasing premiums for secure and traceable sources of rutile and synthetic feedstocks. These geopolitical shifts are forcing pigment producers to reconsider their sourcing strategies, prioritizing jurisdictional stability and supply security over pure cost optimization.

Structural Shifts in Titanium Feedstocks & Global Markets

The global titanium feedstock industry is undergoing significant structural transformation as declining natural rutile production intersects with technological and regulatory tailwinds favoring synthetic alternatives. This shift represents more than cyclical market dynamics, reflecting fundamental changes in how pigment producers evaluate supply security, cost stability, and regulatory compliance.

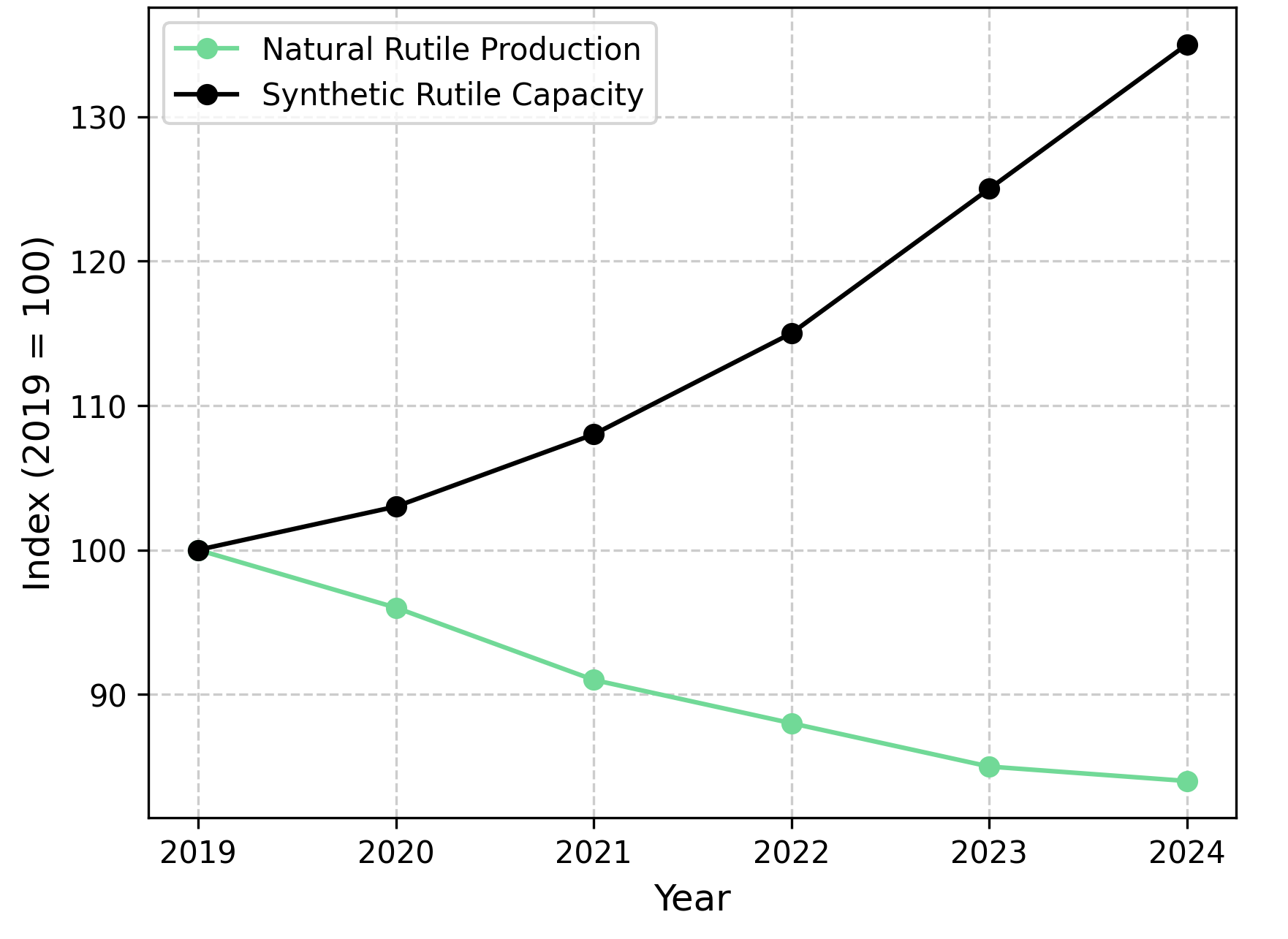

Global natural rutile production has declined approximately 15% over the past five years, primarily due to mine depletion in Australia and operational challenges in African deposits. Simultaneously, synthetic rutile capacity has expanded rapidly, particularly in China, where environmental regulations paradoxically favor synthetic production over traditional mining operations in certain provinces.

The divergence between sulfate and chloride TiO₂ pricing has created new dynamics in feedstock selection, with rutile premiums compressing from historical levels of 30-40% to current ranges of 15-20%. This compression reflects both increased synthetic rutile availability and technological improvements in beneficiation processes that enhance the quality of lower-grade feedstocks.

Demand Growth Drivers

Structural demand growth from aerospace, defense, and renewable energy sectors continues to sustain long-term titanium feedstock demand despite short-term substitution trends. These end-use markets typically require higher-purity feedstocks, supporting premium pricing for both high-grade natural rutile and advanced synthetic alternatives.

The aerospace sector's recovery post-pandemic has been particularly significant, with Boeing and Airbus ramping production schedules requiring consistent, high-quality titanium supplies. Defense applications, driven by increased global military spending, represent another growth vector for premium titanium feedstocks.

Natural rutile projects with exceptional economics and strategic backing are emerging as preferred investment vehicles in this constrained environment. Sovereign Metals' Kasiya project in Malawi exemplifies this trend, offering Tier-1 scale as the largest rutile resource globally while maintaining a unique co-product model where graphite emerges as a byproduct rather than competing revenue stream.

Monetary Tightening & Cost of Capital in Critical Mineral Projects

The Federal Reserve's sustained higher interest rate environment has fundamentally altered the financing landscape for capital-intensive rutile projects, particularly those located in emerging markets. This monetary policy stance creates a challenging backdrop for project development, forcing companies to demonstrate exceptional economics and risk mitigation strategies to attract investment capital.

African rutile projects face disproportionate impacts from higher discount rates, foreign exchange volatility, and rising debt servicing costs. Traditional project financing structures are under pressure as commercial lenders demand higher risk premiums for emerging market exposures, particularly in the mining sector where commodity price volatility adds additional uncertainty.

Projects with robust economics, Tier-1 scale, and strong backing increasingly stand out in this constrained funding environment. Strategic partnerships with established mining companies provide critical validation and access to capital, as demonstrated by Rio Tinto's 19.9% equity stake in Sovereign Metals and technical committee oversight of the Kasiya project, which validates project quality while reducing financing and development risks.

Currency & Consolidation Pressures

Currency hedging costs have increased substantially, adding operational complexity for projects with multi-currency revenue and cost structures. African projects generating US dollar revenues while incurring local currency costs face particular challenges in managing foreign exchange exposure, requiring sophisticated financial instruments that add to overall project costs.

The elevated cost of capital environment has also accelerated consolidation trends, as smaller developers struggle to advance projects independently. Strategic partnerships with established mining companies or offtake agreements with end-users have become increasingly valuable for accessing both capital and technical expertise.

Regulation, ESG, & Traceability as Price Drivers

Environmental, social, and governance regulations are creating new sources of value differentiation in titanium feedstock markets, with compliance capabilities increasingly determining market access and pricing power. These regulatory frameworks extend beyond traditional environmental protection to encompass labor standards, community engagement, and supply chain transparency.

China's 14th Five-Year Plan has intensified environmental enforcement, leading to production cuts at facilities unable to meet stricter emission standards. This regulatory tightening has reduced Chinese titanium feedstock exports while simultaneously increasing demand for compliant international sources, creating pricing opportunities for ESG-aligned producers.

United States Environmental Protection Agency and Securities and Exchange Commission disclosure requirements are adding compliance premiums to supply contracts, as downstream users seek to minimize regulatory exposure through supplier qualification programs. These requirements favor producers with established environmental management systems and transparent reporting capabilities.

European Standards & Premium Pricing

European Union REACH regulation continues driving demand for higher-purity feedstocks, as stricter chemical safety standards eliminate certain processing routes and require enhanced raw material specifications. Projects with naturally advantageous ore characteristics gain significant competitive positioning, as demonstrated by Sovereign Metals' Kasiya deposit with its low-sulfur, free-dig mineralization.

Buyers demonstrate willingness to pay 10-15% premiums for traceable, low-carbon feedstocks, particularly in European and North American markets where corporate sustainability commitments drive procurement decisions. This premium pricing reflects both regulatory compliance value and brand protection considerations for downstream users.

Chairman Ben Stoikovich of Sovereign Metals emphasizes the environmental advantages of their Kasiya project:

"The ore body is contained in totally weathered material and in terms of graphite this leads to significant advantages the ore is free dig and has very low levels of sulfur"

Supply Chain Realignment & Strategic Alliances

Deglobalisation trends and escalating trade tensions are forcing comprehensive reevaluation of titanium feedstock supply chains, with buyers prioritizing security and diversification over pure cost optimization. This strategic shift creates opportunities for suppliers in stable jurisdictions while challenging traditional trade relationships.

Proposed tariffs of 60% on Chinese goods and 30% on South African imports would significantly alter competitive dynamics in North American titanium markets. These trade barriers favor domestic production and allied suppliers, potentially creating substantial pricing advantages for compliant producers in friendly jurisdictions.

Shipping disruptions through the Red Sea and Panama Canal have highlighted supply chain vulnerabilities, adding urgency to supplier diversification initiatives. These logistical challenges demonstrate the value of multiple supply sources and robust transportation infrastructure, factors that favor established mining regions with developed export capabilities.

Strategic Sourcing & Long-term Contracts

Strategic sourcing approaches now emphasize "China+1" strategies, nearshoring to Mexico, Vietnam, and India, and increased emphasis on supply chain resilience over cost minimization. Jurisdictional stability becomes paramount, with projects in mining-friendly jurisdictions like Malawi offering regulatory predictability and established export infrastructure through rail-linked transportation networks.

The growing prevalence of long-term offtake agreements with aerospace and pigment producers reflects buyers' willingness to sacrifice some pricing flexibility for supply security. These contracts often include ESG compliance requirements and quality guarantees, favoring established producers with proven operational capabilities.

Technology & Production Trends in Synthetic Rutile

Technological advancement in beneficiation and synthetic processing continues improving titanium concentration and product consistency, enhancing the competitive position of synthetic rutile relative to natural alternatives. These improvements are reducing the quality premium traditionally associated with natural rutile while increasing synthetic production flexibility.

Energy-efficient kiln technologies and artificial intelligence-based process optimization are reducing production costs while improving product quality consistency. These technological developments enable synthetic producers to compete more effectively with natural rutile in applications previously reserved for higher-grade natural feedstocks.

Expansion of synthetic rutile capacity in China, Italy, and Rio Tinto's modernization projects in Quebec represents significant supply additions that could pressure natural rutile pricing in certain market segments. However, these capacity additions also reflect growing demand for titanium feedstocks across multiple end-use applications.

Production Flexibility & Economic Advantages

Comparative economics between synthetic rutile and upgraded ilmenite continue evolving as processing technologies improve and environmental regulations favor certain production methods. Natural rutile projects with exceptional cost positioning demonstrate resilience against synthetic competition, with bottom-quartile cost structures providing sustainable competitive advantages.

Processing flexibility represents a key advantage for synthetic producers, allowing product customization for specific end-use applications and rapid response to changing market requirements. However, natural rutile projects with unique co-product models can achieve comparable economic flexibility, as demonstrated by projects generating graphite byproducts at incremental costs as low as $241 per ton. Chairman Ben Stoikovich highlights this economic positioning:

"Our incremental cost to produce a ton of graphite as a byproduct from the Kasiya project will only be $241 US per ton"

Market Volatility, Currency Effects, & Investment Risks

African foreign exchange volatility creates additional complexity for rutile projects, particularly those with mixed currency revenue and cost structures. These currency fluctuations can significantly impact project returns and complicate investment analysis, requiring sophisticated hedging strategies and financial risk management.

Oversupply risk from expanding Chinese synthetic rutile capacity represents a persistent threat to natural rutile pricing, particularly in lower-grade market segments where synthetic alternatives compete effectively. This competitive pressure requires natural rutile producers to demonstrate clear value propositions beyond pure cost considerations.

Substitution risk from TiO₂ slag and recycled titanium scrap continues evolving as recycling technologies improve and circular economy initiatives gain momentum. These alternative sources could pressure titanium feedstock demand over longer time horizons, though current recycling capacity remains limited relative to primary demand.

Development & Political Risk Factors

Project development timelines face increasing constraints from permitting delays in ESG-sensitive jurisdictions, as regulatory approval processes become more comprehensive and community engagement requirements expand. However, well-advanced projects with upcoming definitive feasibility studies, such as those scheduled for Q4 2025 completion, offer near-term re-rating catalysts that can enhance project valuations despite broader market challenges.

Political risk in African mining jurisdictions remains elevated, with potential for resource nationalism, changing fiscal terms, and operational disruptions. These risks require careful evaluation and mitigation strategies, including political risk insurance and stakeholder engagement programs.

The Investment Thesis for Rutile

The investment case for rutile exposure encompasses multiple converging trends that support strategic positioning in well-selected assets across the natural and synthetic rutile value chain.

- Supply deficit persistence maintains natural rutile's premium pricing despite synthetic substitution trends, as declining production from established mines creates structural supply constraints that synthetic alternatives cannot fully address in all market segments.

- ESG premiums continue rising as regulatory requirements and corporate sustainability commitments drive demand for traceable, low-carbon feedstocks, creating sustainable competitive advantages for compliant producers with established environmental management systems.

- Cost curve positioning favors projects with bottom-quartile production costs for both rutile and graphite, providing resilience against commodity price volatility and competitive pressure from synthetic alternatives while enabling co-product revenue diversification.

- Strategic partnerships de-risk project development as demonstrated by major mining companies taking equity stakes and providing technical oversight, validating project quality while providing access to expertise and potential development capital that reduces financing risk.

- Synthetic rutile capacity expansion reshapes supply dynamics by providing producers with beneficiation capabilities enhanced resilience against supply shocks and market disruptions, though requiring different investment approaches than traditional mining projects.

- Geopolitical diversification becomes essential as deglobalisation trends and trade tensions create premiums for stable-jurisdiction projects that offer supply security and regulatory compliance, favoring established mining regions with developed infrastructure.

Structural Repricing in Titanium Feedstocks

The convergence of higher interest rates, stringent ESG regulations, supply chain realignment, and substitution trends is fundamentally reshaping titanium feedstock markets, creating both challenges and opportunities for investors with appropriate strategic positioning.

Natural rutile retains inherent scarcity value supported by declining global production and unique quality characteristics, though increased price volatility reflects competitive pressure from synthetic alternatives and changing buyer preferences prioritizing supply security over cost optimization.

The evolving market structure favors diversified, stable-jurisdiction projects that combine Tier-1 resource scale, demonstrated ESG compliance, and strategic backing from established industry participants. Projects meeting these criteria, particularly those with unique co-product models and free-dig mineralization advantages, offer exposure to structural market trends while providing downside protection through superior economics and operational advantages.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed