Chile Copper Project Targets Low-Cost Supply Response

Marimaca's US$587M Chilean copper project delivers 39% IRR, US$2.09/lb costs, and district-scale growth potential amid global supply constraints and major producer cutbacks.

- Marimaca Copper's MOD project delivers a post-tax NPV of US$1.1 billion with 39% IRR and just 2.2-year payback, positioning it among the lowest capital-intensity copper developments globally at US$11,700 per tonne capacity.

- The project features exceptionally low all-in sustaining costs of US$2.09/lb against production of 50,000 tonnes per annum cathode copper, securing second-quartile cost positioning with 58% EBITDA margins.

- Initial capex of US$587 million leverages existing infrastructure near Antofagasta, with 100% renewable power, recycled seawater, and 38% lower carbon emissions than traditional flotation processing.

- Proven and probable reserves stand at 179 million tonnes grading 0.42% copper, with 88% conversion from measured and indicated resources and discovery costs below US$0.02 per pound.

- District-scale exploration across Sierra de Medina offers significant expansion potential through satellite deposits and sulphide systems, supporting a hub-and-spoke growth model beyond the initial 13-year mine life.

Introduction: Supply Constraints Create Development Premium

When Antofagasta plc, one of Chile's best-managed copper producers, revised its 2025 production guidance to the lower end of 660,000-700,000 tonnes in October 2025, global copper markets took notice. The company's flat 2026 outlook of 650,000-700,000 tonnes confirmed what Citi analysts had warned: even well-capitalized producers face structural growth headwinds. With copper prices hovering near US$11,000 per tonne and major miners cutting capex (Antofagasta reduced 2025 spending to US$3.6 billion from US$3.9 billion), the premium for low-cost, shovel-ready copper projects has never been clearer.

Against this backdrop, Marimaca Copper Corp.'s Marimaca Oxide Deposit project emerges as a rare near-term supply response. Located in Chile's proven Coastal Copper Belt near Antofagasta, the heap-leach development combines exceptionally low capital intensity with top-quartile margins. The October 2025 Definitive Feasibility Study positions MOD among fewer than a dozen global copper projects with initial capex below US$1 billion and profitability indices exceeding 1.5 times, according to Wood Mackenzie Q1 2025 benchmarking data.

The investment case rests on three pillars: competitive economics that withstand price volatility, execution advantages from Tier-1 infrastructure and jurisdiction, and district-scale optionality through satellite resource consolidation. For investors seeking leveraged exposure to supply-side tightness without billion-dollar construction risk, Marimaca represents a differentiated entry point in the copper development landscape.

Company Overview: Purpose-Built for Margin Optimization

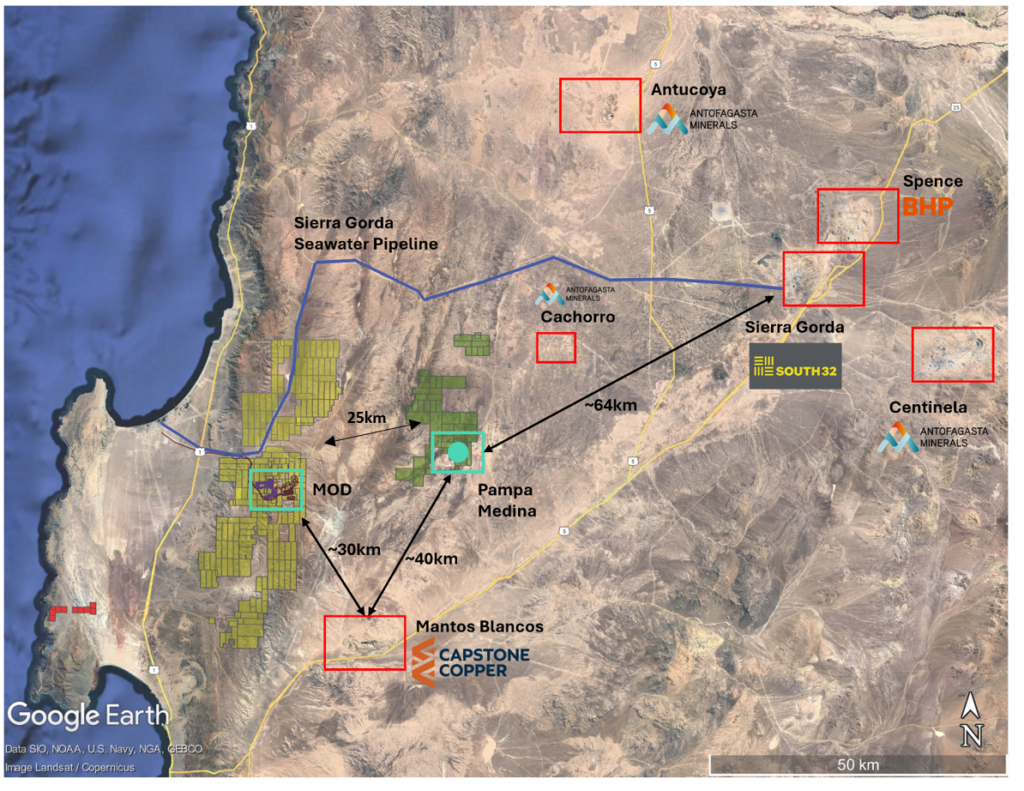

Marimaca Copper Corp. operates as a single-asset development company focused on the Marimaca Oxide Deposit in Chile's Antofagasta Region. The company controls approximately 14,000 hectares in the coastal copper belt, positioned between established operations including Mantos Blancos, Spence, and Chuquicamata. This geographic concentration provides immediate access to port facilities, grid power, and skilled labor pools (infrastructure advantages that materially reduce both construction and operating risks compared with greenfield locations).

Corporate leadership brings operational pedigree from mid-tier producers and successful development exits. CEO Hayden Locke previously led Papillon Resources through to acquisition and served as CEO of Emmerson Plc, while the board includes veterans from First Quantum Minerals, Capstone Copper, and Assore Holdings. The strategic investor base reflects institutional confidence: Greenstone Resources holds 22%, Assore 16%, Ithaki Capital 14%, and Mitsubishi Corporation 4% of the approximately 115 million shares outstanding.

The company's capital structure as of June 2025 showed US$24.3 million cash following an A$80 million raise, with zero debt. At a market capitalization of C$1.33 billion (at C$11.56 per share), Marimaca trades at roughly 1.2 times the DFS post-tax NPV, a discount to peers at similar development stages. Analyst coverage from BMO Capital Markets, RBC, Canaccord Genuity, Tamesis Partners, and Raymond James provides institutional research support ahead of construction financing.

Key Development: DFS Confirms Top-Tier Economics

The October 2025 Definitive Feasibility Study establishes MOD as one of the most capital-efficient copper developments in the current pipeline. At US$587 million initial capex, the project delivers US$11,700 per tonne of annual production capacity (substantially below the industry average of US$18,000-25,000 for comparable heap-leach operations). This efficiency stems from simple processing (three-stage crushing to P80 12.5mm, acid curing, conventional SX-EW), low strip ratio of 0.8:1, and leveraging existing regional infrastructure rather than building from zero.

The financial returns prove robust across price scenarios. At the base case of US$5.05 per pound copper, post-tax NPV reaches US$1.1 billion with 39% IRR and 2.2-year payback period. Sensitivity analysis shows the project maintains positive economics even at US$4.30 per pound, generating US$709 million NPV and 31% IRR. All-in sustaining costs of US$2.09 per pound (C1 cash costs of US$1.69 per pound) position MOD in the second quartile of the global cost curve, providing significant margin buffer should copper prices moderate from current levels.

Production targets 50,000 tonnes per annum copper cathode during steady state over a 13-year initial mine life, averaging 48,000 tonnes annually across the first decade. The processing flowsheet features 12 heap leach cells with expansion infrastructure pre-sized for Phase 2, which adds 670 tonnes per hour tertiary crushing capacity and two additional leach cells for US$77 million sustaining capex. Seven phases of metallurgical testing support 72% copper recovery assumptions and demonstrate lower-than-expected acid consumption rates, de-risking operating cost projections.

Strategic Significance: Infrastructure & ESG Differentiation

Marimaca's location advantage extends beyond proximity to existing mines. The project benefits from a 32-kilometer pipeline delivering recycled seawater from Mejillones at 208 liters per second capacity, eliminating dependence on scarce freshwater resources that increasingly constrain Chilean copper operations. Access to 100% renewable electricity from the Norte Grande grid addresses both cost stability and environmental considerations, while the coastal Atacama Desert setting presents minimal ecological disturbance compared with highland or forested locations.

The heap-leach processing route carries inherent sustainability benefits. Compared with traditional flotation mills, the SX-EW flowsheet generates approximately 38% lower carbon emissions per pound of copper produced (a critical differentiator as copper buyers and financiers implement scope-3 emissions requirements). No land-use conflicts exist with local communities, and the project employs a regional workforce with established mining skills, reducing both social risk and the need for costly fly-in-fly-out operations that burden remote developments.

Capital cost benchmarking underscores the competitive positioning. Among projects with initial capex below US$1 billion, MOD ranks in the top tier for profitability index (NPV divided by capex) at 1.9 times. The DFS includes 10% contingency on direct and indirect costs, with detailed execution planning by tier-one engineering firms. Conventional truck-and-shovel mining using 220-tonne haul trucks and 29-cubic-meter shovels requires no novel technology adoption, further constraining execution risk relative to projects dependent on unproven processing methods or automation.

Resource Base: High-Confidence Conversion Metrics

The 2025 mineral resource estimate totals 213 million tonnes measured and indicated grading 0.40% copper, containing 854,000 tonnes copper metal, plus 21 million tonnes inferred at 0.29% copper for an additional 62,000 tonnes contained metal. Critically, 93% of total resource tonnes now sit in measured and indicated categories, reflecting extensive drilling that provides unusual confidence for a development-stage asset. This compares favorably with peers where inferred resources often comprise 30-50% of the total, introducing material uncertainty into reserve conversion assumptions.

Proven and probable reserves stand at 179 million tonnes grading 0.42% copper, yielding 748,000 tonnes contained copper metal. The 88% conversion rate from measured and indicated resources to reserves substantially exceeds industry norms of 60-70%, demonstrating both deposit quality and conservative mine planning. At less than US$0.02 per pound discovery cost, Marimaca ranks among the lowest-cost resource additions globally (a function of targeted exploration in a well-understood geological setting rather than broad regional prospecting).

Mine planning divides the deposit into eight pit phases across a 13-year schedule, with conventional 12-meter bench heights and standard geotechnical parameters. The extremely low 0.8:1 strip ratio minimizes waste movement and associated costs, while the simple oxide mineralization requires no complex metallurgical treatment. Resource expansion potential exists both through additional drilling within the existing pit shell and through incorporation of satellite deposits currently in various stages of evaluation across the broader property package.

District-Scale Exploration: Optionality Beyond Base Case

Marimaca's acquisition strategy in the Sierra de Medina region, approximately 25 kilometers from MOD, creates significant upside optionality beyond the DFS mine plan. The Pampa Medina and Madrugador properties host high-grade oxide copper mineralization at surface with compelling sulphide systems at depth, identified through an ongoing 10,000-meter drill program. Early results suggest potential for satellite deposits in the 20-40 million tonne range grading 0.3-0.4% copper (sufficient to meaningfully extend mine life or increase annual production rates).

Multiple additional exploration targets exist across the property portfolio, including Cindy, Mercedes, Tarso, Sierra, and Roble prospects. The company envisions a hub-and-spoke operating model where the central MOD processing facilities treat ore from satellite pits via short-haul trucking, leveraging infrastructure investment across a broader resource base. This approach has proven highly successful in Chilean copper districts, where operators like Mantos Copper have extended operations decades beyond initial mine plans through systematic near-mine exploration.

The sulphide potential beneath oxide zones represents a longer-term value driver. While the current DFS focuses exclusively on heap-leachable oxide material, drill intercepts confirm sulphide mineralization at depth typical of Chilean porphyry systems. Should copper prices sustain elevated levels and flotation technology costs decline, these sulphide resources could support a Phase 3 expansion incorporating conventional milling (a pathway that would transform Marimaca from a 50,000-tonne-per-annum oxide producer into a potentially 100,000-tonne-per-annum integrated operation).

Financial Performance: Cash Generation & Expansion Funding

The DFS projects average annual EBITDA of US$330 million during steady-state production, translating to margins exceeding 60% in the first five years of operation. Free cash flow generation tops US$200 million annually through the initial decade, providing ample internal funding for the US$529 million sustaining capex program and potential self-financing of Phase 2 expansion. This cash generation profile positions Marimaca to operate without significant additional equity dilution post-construction, preserving value for current shareholders.

Construction funding requirements total US$587 million plus working capital and cost escalation contingencies, likely implying a US$650-700 million financing package. The company's debt-free balance sheet and strategic investor base provide multiple pathways: project finance debt (typical 60-70% of capex for permitted copper projects), strategic partnership or streaming arrangements, or equipment financing for mobile fleet. The 2.2-year payback period enhances debt capacity, as lenders can model full capital return within standard loan tenures.

Commodity price sensitivity demonstrates downside protection. At US$4.00 per pound copper (roughly 20% below October 2025 spot prices), the project generates 25% IRR and US$580 million post-tax NPV. Even at US$3.50 per pound, returns remain positive though uncompelling, establishing a floor well below consensus long-term price forecasts of US$4.25-4.75 per pound. Operating cost sensitivity shows similar resilience, with the project maintaining attractive economics even if all-in sustaining costs increase 15% from base-case assumptions.

Current Market Context: Supply Response Urgency

Antofagasta's October 2025 guidance revision crystallizes the supply-side thesis supporting development-stage copper investments. When a tier-one producer with established operations, strong balance sheet, and operational excellence reduces production expectations and defers capex, it signals systemic constraints beyond individual asset challenges. Water availability, power costs, permitting delays, and labor availability affect Chilean operations broadly (issues that advantage greenfield projects like Marimaca that have secured water, power, and permits ahead of construction).

The flat global production outlook for 2026 from major producers occurs against demand forecasts pointing to 3-4% annual consumption growth driven by electrification, renewable energy infrastructure, and electric vehicle adoption. This supply-demand imbalance historically leads to sustained elevated pricing and valuation premiums for companies delivering incremental production. Copper inventories on major exchanges remain at multi-year lows, providing limited buffer against supply disruptions or demand surges.

For development-stage companies, this environment creates acquisition interest from major miners seeking to replenish project pipelines. Mid-tier producers including Lundin Mining, Hudbay Minerals, Capstone Copper, and Sandfire Resources have articulated growth strategies emphasizing brownfield expansion and selective development-stage acquisitions. Marimaca's combination of development readiness, manageable capex requirement, and district-scale growth potential positions it squarely within this acquisition target profile (a dynamic that establishes valuation floors independent of commodity price movements).

The Investment Thesis for Marimaca Copper Corp.

- Allocate 3-5% of copper equity exposure to development-stage producers with sub-US$600 million capex and sub-three-year payback periods to capture supply-response premiums.

- Overweight Chilean coastal copper projects that have secured water permits and renewable power access given increasing constraints on highland operations.

- Prioritize copper developers trading below 1.5× post-tax NPV with proven management teams and institutional investor bases to minimize financing risk.

- Diversify into oxide heap-leach projects that offer 60%+ EBITDA margins as hedges against flotation cost inflation and concentrate treatment charge volatility.

- Target companies with district-scale exploration optionality beyond base-case mine plans to capture potential re-rating as satellite resources convert to reserves.

- Establish positions ahead of construction financing announcements, which historically trigger 15-30% valuation re-ratings for development-stage miners.

Marimaca Copper presents a distinctive value proposition within the copper development landscape: exceptional economics delivered through infrastructure leverage rather than geological exceptionalism. The US$1.1 billion post-tax NPV, 39% IRR, and second-quartile cost positioning establish financial credibility, while the 88% resource-to-reserve conversion rate and detailed DFS engineering reduce execution uncertainty. For investors seeking copper exposure without the operational risks of producing miners or the binary exploration risks of early-stage developers, the company occupies a specific niche.

The investment timing aligns with multiple catalysts. Construction financing arrangements expected in coming quarters will validate project economics through third-party due diligence and establish a clear path to production. Ongoing exploration at Sierra de Medina satellite deposits offers potential resource expansion announcements that could materially extend mine life or production rates. The broader copper market supply tightness, evidenced by major producer guidance revisions, creates favorable conditions for development-stage acquisitions and strategic partnerships.

Risk considerations center on execution rather than economics. Construction inflation, permitting delays, or metallurgical underperformance could compress returns, though the DFS includes standard contingencies for these factors. Copper price volatility presents two-sided risk: sustained prices below US$4.00 per pound would impair returns, while prices sustainably above US$5.50 per pound might attract competing projects that pressure long-term pricing. Geographic concentration in a single Chilean asset creates jurisdiction risk, though this is partially offset by the country's century-long copper mining history and established legal frameworks.

The ultimate bull case extends beyond the initial 13-year mine plan. If Marimaca successfully integrates satellite deposits and converts sulphide resources, the MOD hub could evolve into a multi-decade, 100,000-tonne-per-annum operation (transforming the company from a mid-tier producer into an acquisition target for majors seeking to replace depleting reserves). At current valuations near post-tax NPV, investors effectively receive this optionality without premium pricing, establishing an asymmetric risk-reward profile appropriate for 3-5% positions within diversified resource portfolios.

TL;DR

Marimaca Copper's Marimaca Oxide Deposit project in Chile offers investors exposure to copper supply tightness through a low-capex, high-margin development positioned in proven infrastructure. The October 2025 DFS confirms US$1.1 billion post-tax NPV, 39% IRR, and 2.2-year payback on US$587 million initial capex (among the lowest capital intensity metrics globally). With all-in sustaining costs of US$2.09 per pound placing it in the second quartile of the cost curve, the project generates 58% EBITDA margins and over US$200 million annual free cash flow during steady-state operations producing 50,000 tonnes per annum copper cathode.

Strategic advantages include 100% renewable power, recycled seawater supply, and location in Chile's established Coastal Copper Belt near Antofagasta with immediate port and skilled labor access. The resource base shows exceptional conversion confidence, with 88% of measured and indicated resources translating to proven and probable reserves totaling 179 million tonnes at 0.42% copper grade. District-scale exploration across Sierra de Medina satellite deposits offers significant expansion optionality beyond the base 13-year mine life, supporting potential hub-and-spoke operating model.

The investment case strengthens against October 2025 market context, where Antofagasta and other major Chilean producers revised 2026 guidance to flat or declining production despite copper prices near US$11,000 per tonne. This supply constraint environment favors shovel-ready projects like Marimaca that secured permits and infrastructure access ahead of tightening regulations. Trading at roughly 1.2× post-tax NPV with strategic investors holding 56% of shares and zero debt, the company presents development-stage exposure without the execution risks typical of larger, more complex projects.

FAQs (AI-Generated)

At US$11,700 per tonne annual capacity and 2.2-year payback, MOD ranks among the lowest capital-intensity projects globally while maintaining second-quartile all-in sustaining costs of US$2.09 per pound.

The project utilizes a 32-kilometer pipeline delivering recycled seawater from Mejillones at 208 liters per second, eliminating dependence on scarce freshwater resources that constrain competing operations.

With DFS complete and environmental permits secured, construction financing expected in 2026 would enable approximately 24-month construction, targeting first production in 2028-2029.

The 88% conversion from measured and indicated resources to proven and probable reserves substantially exceeds typical industry rates of 60-70%, reflecting high-confidence geology and conservative mine planning.

Ongoing exploration at Sierra de Medina satellite deposits 25 kilometers from MOD targets 20-40 million tonnes additional oxide resources, with deeper sulphide systems offering potential Phase 3 flotation expansion.

Analyst's Notes

Subscribe to Our Channel

Stay Informed