Analyst's Notes: What Feasibility Studies Should Tell You

Get industry analysts take on the latest mining company press releases, and its effect on you - the investor.

We are committed to helping investors come to grips with the resources sector and learn how to interpret news releases made by companies. In these Analyst’s Notes we illustrate how news from companies affects the investment case for the stock, and how it can your investment decisions. The topics are selected based on what we think is both relevant and informative to you, the investor.

This week, we have selected four companies that demonstrate different scenarios that could prove to be future Red Flags or Green Lights.

Victoria Gold

A key example of:

- How new mines are often over-optimistic

- How heap leach operations struggle in cold weather

- How company share prices can suffer when sweet hope meets harsh reality

What the Company reports

On 6 January 2020 Victoria Gold Corporation ("Victoria") (OTC:VITFF) (TSX:VGCX) announced its Q4 results for its Eagle mine, proudly revealing it had produced 77,748 oz during H1 2020 compared to guidance of 72,000-77,000 oz.

Table 1 shows the results extracted from the press release.

What the Analysts see

The headline news that Victoria came in at the top end of guidance was positive. So far, so good.

However, we did a little digging and made a few observations:

- Commercial production was declared only on 1 July 2020, therefore the company deemed that the first two quarters were not “commercial” or steady state.

- Table 1 illustrates that total mine production actually dropped between Q3 and Q4, which can probably be attributed to weather conditions in the northern Yukon getting worse towards the end of the year.

Interestingly, the forecasts made in a Technical Report dated 6 December 2019 were for production at a commercial level all through 2020, in terms of throughput, grade and metallurgical recovery.

And as noted above, commercial production was only achieved by 1 July. This illustrates that when a Technical Report is commissioned by an Issuer (in this case Victoria Gold Corp) and written by a third party (in this case JDS Energy and Mining Inc), it is very easy to be over-optimistic. And when one is over-optimistic, the realities of life are bound to lead to disappointment.

In this case the planned and publicly forecast production for the year was from 140,000 oz to 154,000 oz, but the reality was only 116,644 oz.

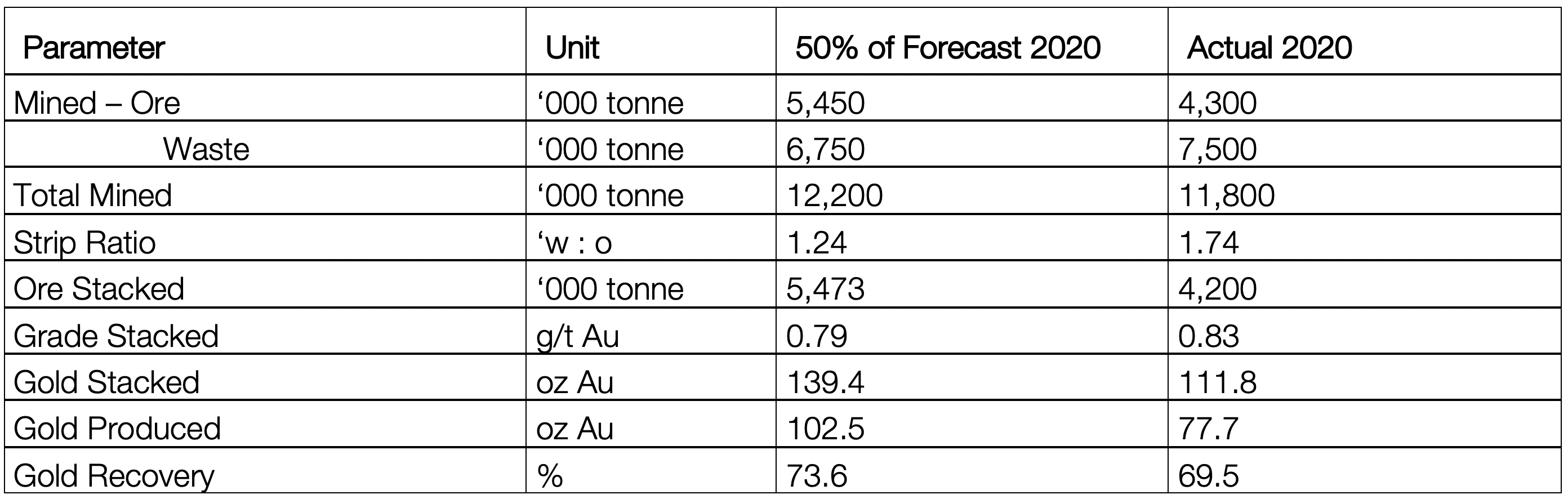

Looking at the numbers in a bit more detail, we have split the ‘full year’ forecast in two, generating Table 2 above, and compared it to the actual numbers for all of 2020.

Whereas total mine production is close to forecast, ore mined is lower by 21%, and stacked ore is lower by 23%. These lower mining and stacking rates are somewhat compensated by a higher than planned grade, but recovery is 69.5% compared to planned recovery of 73.6%. (Remember that recoveries for heap leach operations often take a year or two to settle down to predicted rates.) Regardless, the net result is a H2 gold production of 77.7 koz which lags ½ forecast of 102.5 koz by more than 24%.

Should you really want to get into the detail, note that these stacking rate numbers are slightly behind the mining rate, which we hope is a temporary feature.

Remember that in heap leach operations, some of the most important factors are leach dynamics and flow through the stacked heap. Given that the Eagle Mine is in the Yukon and the pad is likely to freeze in Q1 of any given year, the production plan provides for cessation of stacking in the coldest months, but with mining continuing.

During Q1 the ore mined is stockpiled and then drawn during the rest of the year. This means that during Q1, gold production is only from material stacked previously. It also means that the operation needs to be able to stack 12 months of ore in 9 months.

What it means for Investors

What may concern investors in Victoria Gold is the fact that stacking rates for Q4/20 were lower than planned, which can only lead to lower-than planned Q1/21 production. The shortfall in stacking in Q4/20 will become evident when the company releases its results, typically between one and two weeks after quarter end and full financials (approximately 6 weeks later).

Could it be that expectations of lower production rates from Victoria (announced in April 2021) will weigh on the share price? Or will production be a surprise disappointment when it comes?

Still, with the spring will come the thaw. We expect that 2021 will see the Eagle Mine find its way.

TMAC Resources

A key example of:

- The importance of feasibility studies in avoiding expensive mistakes

- How other companies can benefit from another’s mistakes

What the Company reports

As a general rule, it is worth completing a feasibility study on a new deposit so that engineering parameters such as metallurgical performance can be properly evaluated before investing large sums of capital. TMAC Resources Incorporated (“TMAC”) (TSX:TMR) ignored these fundamentals and the shareholders of the company have paid the penalty.

The Hope Bay gold project in Nunavut, Canada, was given the go-ahead in mid-2015 on the back of a pre-feasibility study (“PFS”). Moving ahead on a PFS is always a risky proposition although some companies can get away with it if:

- The work has been particularly thorough,

- The CapEx is particularly low (Capital Expenditure)

- The deposits in the area are particularly well-known

What the Analysts see

None of these factors applied at Hope Bay, and the description of metallurgical test work in the PFS report was particularly skimpy. The PFS only discussed test work on two samples from one particular deposit (i.e. Doris) and two from another (“Naartok”) and all were treated using the same process route. The report also refers to previous metallurgical test work by Newmont, dated 2012, but without reviewing this work.

It did not take long for the cracks in the plan to appear.

In January 2016 a fresh “Tactical Plan” indicated trouble, as it included changes to “provide the mill with significant high-grade feed at start up, and a smooth production ramp up to 1,000 tonnes per day in 2017 and to 2,000 tonnes per day in 2018”.

Further problems became evident when plant commissioning did not start at the end of 2016 as promised. Then followed announcements highlighting that commissioning problems were experienced. The processing cost started to bleed the company to death and it got very close to insolvency.

Figure 2 shows the share price of TMAC over the last 5 years, which makes for dreadful viewing.

The company commissioned a new pre-feasibility study, but with heavy emphasis on resolving the metallurgical issues. The latest study was published on 30 March 2020, recommending construction of a new processing plant. Ouch.

The problem was that by now finding entities willing to fund the company was not straightforward. A knight in shining armour arrived in the guise of Shandong Gold Mining Co. Ltd (“SD Gold”) which agreed to purchase all of the outstanding shares of TMAC at a price of C$1.75 per share in cash, an offer that was unsurprisingly and overwhelmingly supported by TMAC shareholders.

On 21 December 2020 the company announced that the Canadian government had disallowed the plan of arrangement with SD Gold.

However, the breathing space provided by SD Gold and the high prevailing gold price had turned the mine cash positive according to the same press release. The decision of Canadian authorities must not have come as a surprise with another suitor standing in the wings in the form of Agnico Eagle. It is highly unlikely it would have been able to bid on 5 January 2021 had it not already carried out substantial due diligence.

What it means for Investors

Agnico Eagle improved on the offer of SD Gold by raising the bid to C$2.20, equating to an equity value of C$287M. In addition Agnico Eagle agreed to retire TMAC’s outstanding debt and deferred interest and fees to Sprott Lenders, originally secured in July 2015.

At 30 September 2020 the financial statements showed the balance of this debt to be C$170M. Agnico Eagle, a classy operator, has bought the project for C$450M, knowing that it will need a new processing plant.

To put the bid into perspective we compared the value placed by Agnico Eagle with the value the market places on Sabina Gold and Silver ("Sabina") (TSX:SBB) (OTC:SGSVF), which develops its Back River gold project also located in Nunavut, Canada with similar climatic and logistical conditions as Hope Bay. The Back River project is fully permitted and in pre-construction status with construction planned in 2021 after winter.

Sabina Gold and Silver

A key example of:

- The importance of feasibility studies

What the Company reports

The go-ahead decision for Sabina’s Back River project is based on a feasibility study dated 2015, which envisaged production of 0.2 million ounces per annum (“Mozpa”) over almost 12 years from a series of three open pits and one underground at the Goose site. Since 2015, material discoveries and significant resource extensions have been made at the Back River, including the delineation of two separate high-grade underground zones at a deposit called Umwelt.

According to management, internal studies were undertaken to determine what potential improvement these areas might have to meaningfully increase the production profile and/or mine life, with a similar or marginally increased throughput, through a combination of open pit and underground mines at the Goose site. The Company is well advanced on the underground feasibility study, (“UFS”) which is expected in early Q1, 2021. The goal for the UFS is to increase gold production on an annual and total life of mine basis, which is expected to improve the overall financial metrics of the project.

Probably having been warned by TMAC’s experiences Sabina has undertaken additional metallurgical test work programs which have provided better certainty to the process plant design. According to management this will allow the company to obtain a fixed price proposal for plant construction, a major de-risking issue.

It should be noted that Sabina, in addition to Back River, also owns a significant silver royalty on Glencore’s Hackett River Project. The silver royalty on Hackett River’s silver production is comprised of 22.5% of the first 190 million ounces produced and 12.5% of all silver produced thereafter. Hackett River has 200 million ounces in mineral resources at an average grade of 144 g/t and 4.65% Zn.

At this point, it is worth looking at the comparison between TMAC and Sabina Gold and Silver, to illustrate the value proposition that inspired Agnico Eagle to make the bid, and to review the value proposition for Sabina Gold and Silver shareholders.

The table above indicates that Agnico Eagle’s bid makes a lot of sense should the gold price remain at its current levels.

One way of looking at how to buy full production at the mine is to consider the purchase cost of the company (the EV of C$296 million) and then the CapEx required to reach full production (Investment to Full Production of C$683 million), which is a total of C$980 million.

The NPV8 figures is C$1420 million. Then, calculating the ratio is easy, which is 1420 / 980 = 1.45. This ratio of NPV8/Investment of 1.45 gives a lot of slack to cover potential negative surprises and teething problems.

Looking at Sabina, the numbers are a bit harsher, with NPV8 (C$1050 million) / (EV of C$1072 million + Investment required of C$415 million) = 1050 / (1072 +415) = 0.71. In other words, there is a lot of value in the Sabina equity which is not yet showing in the NPV based on old technical reports. We await the publication of the UFS with interest.

What it means for Investors

The C$1.1 billion of Sabina compares generously with the EV at the same number, which means that a pre-development asset is trading without a discount to its NPV, which would normally be considered a very full valuation. But this does not account for a number of favourable aspects that are not included in a straight NPV comparison.

In addition to the Hackett River royalty, Sabina has very robust economic performance in the early years with high grade production by means of open pit mining. Furthermore, substantial additional high grade underground production will become evident from the UFS and then there is the blue-sky potential of the other deposits along the belt as is evident from the very large difference between resources and reserves in Table 3.

The moral of this tale is similar to the tale of the three little pigs, in which it pays to study the risks first and build your house properly. TMAC built its mine on the equivalent of straw or twigs, and eventually fell to the wolf. Sabina is the wise little piggie who is building its house out of bricks, and we expect it to have a long and prosperous life.

Discovery Metals

A key example of:

- The challenges associated with transforming the economics of a large low-grade deposit by drilling high grade structures

Back in September 2020 Crux Investor released a detailed company analysis of Discovery Metals Corporation (“Discovery Metals”) (OTCQX:DSVMF) (TSX:DSV).

What the Company reports

The main conclusion was that Discovery Metals would struggle to transform the economics of Cordero by drilling out high grade structures. Cordero is the Spanish word for lamb, and in September made an occasional lamb pun, based on concerns that the project would not make it as an economic proposition. Since September the Company has published a number of exploration updates, and we take this opportunity to revisit our earlier work and check to see if our view has changed.

As a reminder, the company is exploring the very large, but low-grade Cordero polymetallic deposit in Mexico, with silver the dominant economic metal. It was acquired in August 2019 from Levon Resources Limited (“Levon”) and since taking control Discovery Metals has embarked on a drilling programme targeting high grade veins to establish their “sweetening” impact on the overall resources.

What the Analysts see

We question the validity of this strategy because:

- The aggregate volume of veins which have a width of at most 2 metres will be extremely limited. At the most optimistic aggregate strike length of 4 km, and a depth extent of 300 m with an average width of (at best) 1.5 m, the potential tonnage contribution is less than 5 Mt, or 0.8% of the tonnage of 615 Mt within the outline of the resource estimation pit.

- Bulk mining narrow, high-grade structures, which are often in contact with waste, will result in high dilution of the vein grade, greatly diminishing their impact.

Announcing high grade intercepts makes for good headlines, but these will contribute little in terms of improving the economics of the Cordero project. This is particularly the case when drilling is not random with holes collared not in a regular grid, but targeting favourable structures, whereas the envisaged mining operation is of a bulk open pit that is unselective by nature.

Review and analysis of the drill results reported by Discovery Metals showed that only 16.6% of the hole length had grades deemed of interest. Moreover, it still needs to be proven that the intersections delineated well-defined deposits and are not for isolated blocks that can only be mined accepting substantial dilution of adjacent ground, or by including internal waste, further reducing the average grade. A review of cross sections provided by Discovery Metals showed the mineralisation to be spotty and often at considerable depth below surface.

Since the release of the Crux Investor report the company has released 4 sets of results in announcements in September, October and November 2020 and on 6 January 2021. This meant that another review was due to establish whether there have been developments to change its view on the project and the company.

Table 4 shows the released drill results.

Whereas previous results included a number of dud holes in terms of mineralisation, this set of results seems to be devoid of such holes, which suggests a more managed selection of collar locations. In aggregate the results are very close to the pre-September 2020 results with 21.2% of the hole length intersecting mineralisation reported upon (16.6% previously) at a grade of 64 g/t Ag Eq (previously 82 g/t Ag Eq.).

The silver grade equivalent calculated by us differs substantially to numbers quoted by Discovery Metals for three reasons:

- We accounted for metallurgical losses, which will be particularly high for Gold (60%), and high for Lead (16%) and Zinc (28%).

- We accounted for treatment charges incurred for treating Lead and Zinc concentrate in which the Silver and Gold occur.

- We used spot metal prices as per 7 January 2021 with a much higher silver price of US$27.1/oz compared to US$16.5/oz used by Discovery Metals. Using a relatively low silver price increases the relative importance of the by-products expressed in silver equivalent with the reader then bound to apply the spot silver price to the total quoted, thereby overestimating the attractiveness of the reported numbers.

What it means for Investors

For anyone wanting to pore over cross-sections, we have reviewed the data, the maps, the new positions of new drill holes, the extensions of the ore-body, and reviewed whether recent results indicate better consistency of individual deposits.

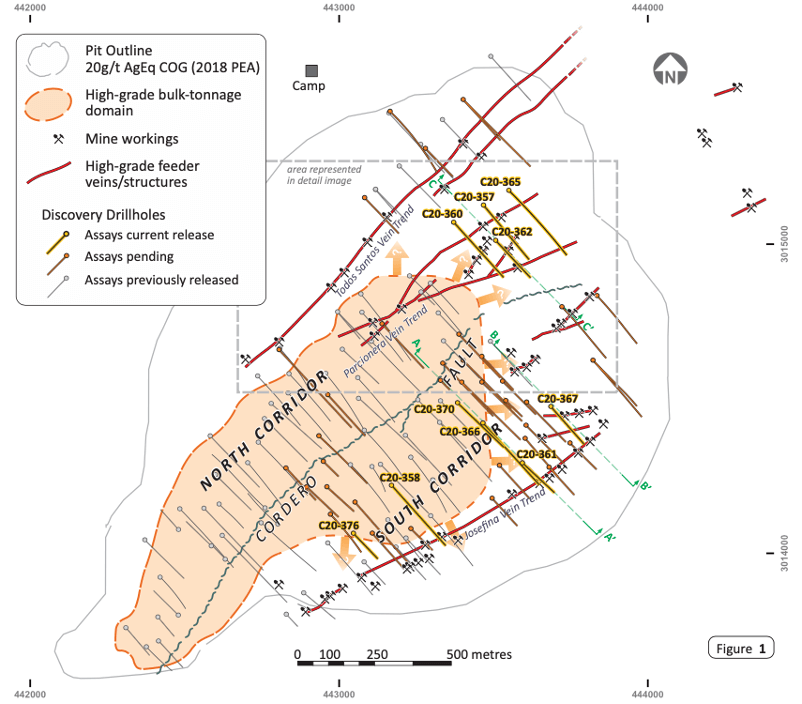

Figure 3 shows the drill hole collar positions and drill-hole traces of holes reported upon until 6 January 2021.

Compared to the same map included in the September report drilling since that date has been extended to the north-east and tested the South Corridor in more detail, especially towards the east.

This note will present two parallel cross section in the Norther Corridor and two in the Southern Corridor.

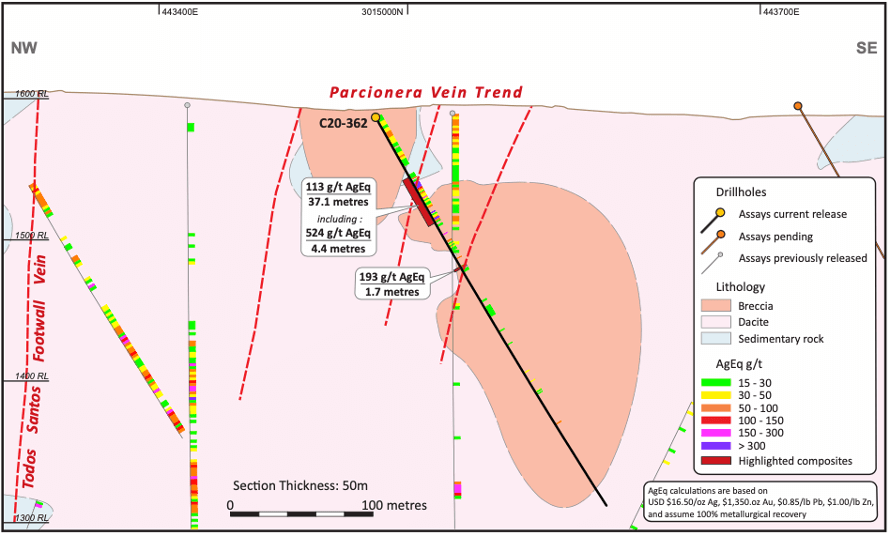

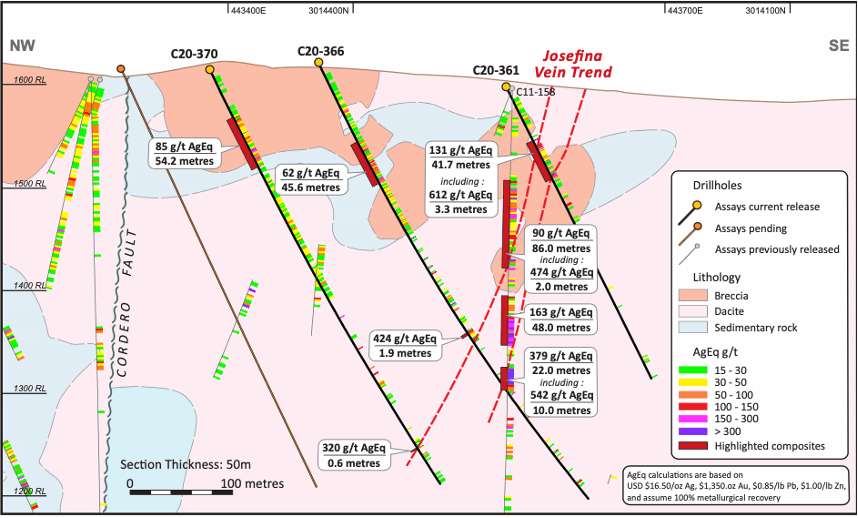

Figure 4 has two cross sections in the Northern Corridor area. The location of C20-362 is highlighted on the map in Figure 3. Hole C20-349 and C20-354 were collared some 300 m and 500 m to the north of C20-362.

Very noticeable from these cross sections is the very localised nature of the mineralisation, confined to fault structures. These deposits will only be mineable by open pit mining to shallow depth after which the stripping ratio becomes excessive. The “pit outline” in Figure 3 must be seen in this light.

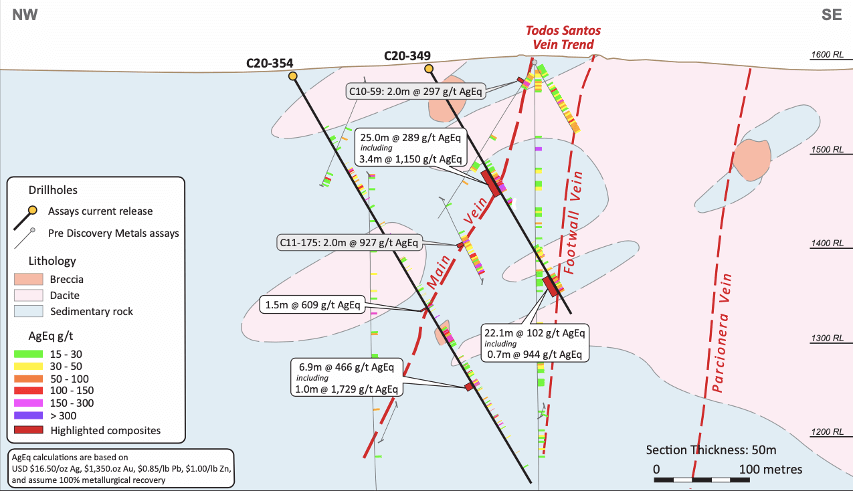

Figure 5 has two cross sections in the Southern Corridor area. All holes are specifically identified in Figure 3 with the two cross sections approx. 200 apart.

The top section is within the light-brown “high-grade bulk tonnage domain” shown in Figure 3. We leave it to the reader to agree or disagree with this classification, but points to the limited extent of the identified intersections, which are a mixture of breccia mineralisation and vein mineralisation. The bottom section shows isolated deposits at considerable depth below surface.

Based on the above we sees no reason to change its conclusion in the September report that the drill results by Discovery Metals only add to the pessimism about whether the mineral resource grade of Levon can be sweetened. On the contrary, it is hard to understand how a mineral resource could have been defined in the first place with a prospective waste strip ratio below 1.0 and the suggested average grades. Holes in close proximity to each other have often distinctly different grades and large sections of internal waste.

Key Takeaways

Company Red Flags

- New mining companies being overly-optimistic in projected production

- Companies failing to achieve their projected production rates

- Companies deciding not to complete the full feasibility study

- Companies trying to manipulate drill results by targeting favourable structures

Company Green Lights

- Companies thoroughly completing feasibility studies

- Openly keeping investors informed along the exploration process

If you are a Family Office investor, or an Institutional investor, and you would like the full report behind this article, please contact matthew@cruxinvestor.com

Analyst's Notes

Subscribe to Our Channel

Stay Informed