Best Silver Stocks 2025: Deficit Market Creates Gains

Silver faces 5th year of supply deficit as industrial demand hits record 700M oz. Best silver stocks: Americas Gold & Silver, Vizsla, First Majestic offer leverage to $40+ prices.

- The global silver market is experiencing its fifth consecutive year of structural supply deficits, with demand consistently outstripping supply by significant margins, creating a fundamental imbalance rather than a temporary cyclical issue.

- Global silver mines are projected to yield 835 million ounces in 2025, representing a 7.23% decrease compared to 2016 levels, while global demand is expected to remain stable at 1.20 billion ounces, highlighting persistent challenges within the mining sector.

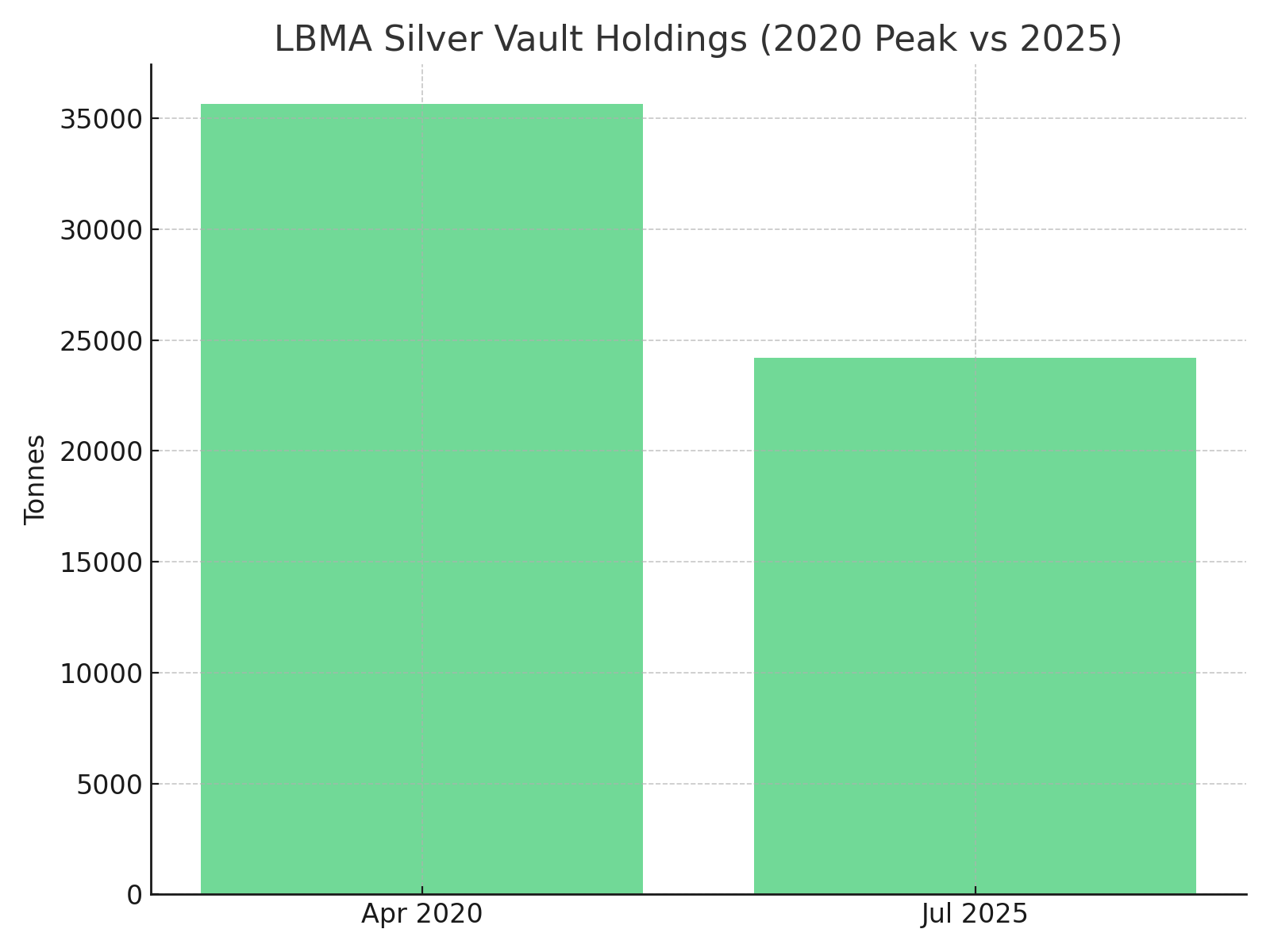

- LBMA vault data shows London silver inventories have declined dramatically to 24,199 tonnes in July 2025, down nearly 50% from the COVID-era peak of 35,667 tonnes in April 2020, indicating real physical scarcity in global markets.

- Silver industrial fabrication is forecast to grow by 3% in 2025, driven primarily by renewable energy applications like solar panels and automotive electrification, with volumes expected to surpass 700 million ounces for the first time.

- The combination of supply-demand imbalances, transparent market reporting, and silver's dual role as both an industrial metal and monetary asset creates compelling investment opportunities across the silver value chain, from physical silver to mining stocks.

Global silver demand is expected to remain broadly stable in 2025 at 1.20 billion ounces, as gains in industrial applications and retail investment will be mitigated by weaker jewelry and silverware demand. However, the supply side tells a different story. Global silver mines are projected to yield 835 Moz in 2025, signifying a 7.23% decrease compared to 2016 levels, highlighting persistent challenges within the mining sector.

This supply-demand imbalance, coupled with transparent reporting from institutions like the London Bullion Market Association (LBMA), creates a compelling investment thesis for silver-focused companies. The combination of macro transparency and micro execution positions select producers to capitalize on what may be silver's most significant bull market in decades.

LBMA Vault Data: The Physical Foundation Under Pressure

The LBMA's monthly vault data provides rare transparency into global silver liquidity, serving as a barometer for physical market conditions. Latest data shows 24,199 tonnes of silver in July 2025, valued at USD 28.2 billion, equivalent to approximately 806,631 standard silver bars.

This figure represents a dramatic decline from historical peaks. During the COVID-era market volatility of April 2020, London vaults held a record 35,667 tonnes of silver, nearly 50% more than current levels. This drawdown isn't merely statistical noise; it reflects real physical tightness in global silver markets.

Physical Scarcity Indicators

Dana Samuelson, president of American Gold Exchange, explained that silver is particularly vulnerable to a supply shock as London Bullion Market Association's physical silver supplies have decreased by 30 to 40 percent, while gold has only lost 3 to 4 percent.

This divergence between gold and silver inventory levels underscores silver's unique position. While gold primarily serves as a store of value, silver's dual role as both monetary asset and industrial input creates competing demand streams that are depleting available stocks.

The transparency provided by LBMA vault data builds investor confidence while simultaneously highlighting the physical constraints facing the market. For investors, this creates a measurable baseline against which to evaluate supply scarcity, a luxury rarely available in commodity markets.

Americas Gold & Silver: North American Excellence in Focus

Americas Gold & Silver represents one of the purest plays on North American silver production, with the company deriving 80% of its revenue from silver, providing direct leverage to price appreciation. The company's recent operational achievements demonstrate how established producers are capitalizing on current market conditions.

Paul Andre Huet, Chairman and CEO, recently highlighted the company's exploration breakthrough:

"The identification of this high-grade copper-silver-antimony extension to the 149 Vein is an exciting development that builds on our ongoing success in unlocking additional value at the Galena Complex. With some extraordinary intercepts, including 24,913 grams per ton silver over 0.21 metres, and nearly 120 meters of vertical continuity demonstrated above the current mining level and exceptional grades in the intercepts, this extension positions us to potentially expand production from an already high-performing vein."

The company's portfolio spans Idaho's Silver Valley (Galena Complex) and Mexico's Cosalá Operations. Recent exploration drilling has yielded exceptional results, with DDH 43-317 returning 24,913 g/t Ag and 16.9% Cu over 0.21 meters, and DDH 43-304 intersecting 2,816 g/t Ag, 2.0% Cu and 1.05% Sb over 1.05 meters. These results demonstrate the high-grade nature of the 149 Vein extension at Galena.

Americas Gold and Silver has successfully closed a US$100 million senior secured debt facility with SAF Group, primarily aimed at funding growth and development capital spending at the Galena Complex. Regarding strategic positioning, Huet noted:

"We are also pleased with the completion of the share consolidation, which represents a strategic move to strengthen our capital structure. By reducing the number of outstanding shares, the consolidation maintains shareholder value and opens the doors to institutional investors with minimum price thresholds."

The company trades at 0.77x NAV versus a peer average of 1.08x, suggesting potential re-rating as silver fundamentals improve.

Industrial Demand: The Green Economy's Silver Appetite

Silver's industrial applications drive its fundamental demand story. Silver industrial fabrication is forecast to grow by 3 percent this year, with volumes on track to surpass 700 million ounces (Moz) for the first time. This milestone represents a structural shift in silver consumption patterns.

Photovoltaics Leading the Charge

The solar industry alone exemplifies silver's critical role in the global energy transition. Despite looming pressure on US renewable energy projects under President Trump's second term, global photovoltaics installations are expected to achieve another all-time high in 2025, benefiting silver demand. The Silver Institute projects solar demand at 232 million ounces for 2024, up from just 59.6 million ounces in 2015.

Automotive Electrification Accelerates

In the automotive industry, even assuming slower growth in battery electrical vehicle production, greater vehicle sophistication, electrification of powertrains (albeit at a reduced pace), and ongoing investment in expanding related infrastructure will boost silver demand.

This demand growth occurs regardless of political winds or regulatory changes. The technological requirements of electric vehicles, advanced driver assistance systems, and charging infrastructure create inelastic demand for silver's unique conductive properties.

Critical Applications Beyond Green Tech

Silver's industrial utility extends far beyond renewable energy. Demand for silver in the "other" industrial category should edge higher due mainly to some upside in the ethylene oxide (EO) sector. At the same time, modest gains are also projected for brazing alloys. These applications, while less glamorous than solar panels, provide steady demand growth that underpins silver's industrial profile.

Supply Challenges: Mining Sector Under Pressure

While demand surges, silver supply faces significant headwinds. Around 80% of silver supply comes from lead, zinc, copper, and gold projects, where silver is a by-product. This dependency on other metals' economics creates supply inflexibility that exacerbates shortages when primary demand increases.

.png)

Production Decline Trends

In 2024, global silver mine production rose by 0.9 percent to 819.7 Moz, underpinned by increased output from lead/zinc mines in Australia and the recovery of supply from Mexico. However, this modest growth pales compared to demand increases, contributing to persistent deficits.

The challenge extends beyond production levels to resource quality. Mine grades have declined over recent decades, requiring more extensive processing for equivalent output. New project development timelines have also lengthened, limiting supply responsiveness to price signals.

Recycling Cannot Bridge the Gap

Projections from the World Silver Survey 2025 data show an anticipated 195 Moz from secondary sources in 2025, a notable increase of 24.06%. While recycling growth is encouraging, despite the commendable growth in recycling, the increase from these secondary sources is not projected to fully offset the decrease in mine production and meet total global demand.

Vizsla Silver: District-Scale Development Strategy

Vizsla Silver represents a different investment profile, a late-stage developer targeting massive-scale production. The company's strategic approach demonstrates how development-stage companies are positioning for silver's structural bull market.

Michael Konnert, CEO, emphasized the company's comprehensive exploration strategy:

"As our development team continues to de-risk and advance Project #1 in the west, our exploration team led by Dr. Jesus Velador, has been busy compiling and analysing new data to locate additional mineralized centers across not only the original contiguous Panuco District but within Vizsla Silver's newly acquired properties situated along the emerging Western Mexico Silver Belt."

With an estimated in-situ combined measured and indicated mineral resource of 222.4 million ounces silver equivalent and an in-situ inferred resource of 138.7 million ounces silver equivalent, Vizsla's Panuco project in Mexico has the potential to join the ranks of billion-ounce silver districts. The company aims to become the world's largest single-asset primary silver producer by 2027.

Konnert outlined the company's extensive development work:

"Since our initial discovery at Napoleon we have completed over 390,000 metres of diamond drilling, made several new discoveries and outlined a robust, high-grade resource base which serves as the foundation for Panuco Project 1, located in the southwest corner of the district. We are now determined to identify the next epicenter of high-grade mineralization with the potential to host similar resources to that outlined in Project 1."

Preliminary economic assessments show attractive metrics: 15.2 million ounces silver equivalent average annual production, $9.40/oz all-in sustaining costs, 86% internal rate of return, and payback under one year.

Mexico hosts eight of fourteen known billion-ounce silver districts globally. Vizsla's Panuco district could become the ninth, positioning the company to capture district-scale economics.

Investment Implications: Macro Trends Meet Company Fundamentals

The convergence of supply deficits, industrial demand growth, and transparent physical market reporting creates multiple investment opportunities across the silver value chain.

Physical Silver Investment

Silver physical investment is also forecast to rise by 3 percent, thanks to improving demand in Europe and North America. As Western investors adjust to new price levels, fresh investment is expected to improve, and profit-taking will also ease.

Price Outlook and Expert Predictions

First Majestic Silver CEO Keith Neumeyer's silver price prediction sees it reaching $100 per ounce. While such projections may seem aggressive, they reflect genuine supply-side constraints. Neumeyer reiterated his belief that the silver market is in an extreme supply deficit and that eventually silver prices will have to rise in order to incentivize silver miners to dig up more of the metal.

Current market conditions support bullish sentiment. Silver rose to 39.09 USD/t.oz on August 28, 2025, up 1.28% from the previous day and is up 33.06% compared to the same time last year.

Cerro de Pasco Resources: Strategic Transformation in Peru

Cerro de Pasco Resources represents a unique approach to silver investment through environmental remediation and resource recovery. The company's transformation demonstrates how innovative business models can create value in the silver sector.

Chief Executive Officer Guy Goulet, outlined the company's strategic pivot:

"The past year marks a turning point for Cerro de Pasco Resources. With the sale of the Santander mine, we have removed significant liabilities from our balance sheet and sharpened our strategic focus on advancing our world-class Quiulacocha Tailings Project. The Company is now well-capitalized and strongly positioned to execute on the next phase of development."

The Quiulacocha Tailings Project represents a novel approach to silver production through the processing of historical mining waste. This environmental remediation model allows the company to extract valuable metals while addressing legacy pollution issues, creating both financial returns and positive environmental impact.

This business model positions Cerro de Pasco Resources uniquely in the silver space, offering investors exposure to both metal production and environmental, social, and governance (ESG) benefits through remediation activities.

Diversified Silver Investment Strategies: Established Producers

First Majestic is one of the purest plays on silver in the mining sector. The company gets an industry-leading 57% of its revenue from silver. Pan American Silver bills itself as the world's premier silver mining company. It has grown into one of the largest silver-focused companies by market cap through a series of acquisitions.

Streaming Companies

Wheaton Precious Metals is a streaming company for precious metals. Instead of operating physical mines, Wheaton provides mining companies with cash to cover portions of their mine development costs. In exchange, the company receives the right to buy some of the metal produced by the mines at fixed prices.

This model provides silver exposure with reduced operational risk, making it attractive for conservative investors seeking precious metals diversification.

Market Dynamics & Investment Strategy

The resulting 182 million ounce deficit might not seem like a lot, but it marks the fourth consecutive year of considerable shortages. This alarming trend indicates a structural imbalance that could have consequences for the silver market for years to come.

The persistence of these deficits, despite higher prices that should theoretically incentivize additional supply, demonstrates the structural nature of current imbalances.

Geopolitical Considerations

Concerns about President Donald Trump's anticipated tariff policies have fueled short covering and deliveries of silver (and other precious metals) into CME warehouses since late 2024. This, coupled with rising economic and geopolitical uncertainties, has underpinned a healthy recovery in silver prices since the start of 2025.

Trade policy uncertainty supports precious metals demand as portfolio diversification tools, benefiting silver alongside gold.

Risk Considerations & Market Outlook

Silver's industrial applications create different volatility patterns than gold. However, potential tariff hikes under Trump's administration and their impact on global economic growth, particularly in China, will likely restrain investor enthusiasm across the broader industrial metals complex.

Supply Response Timing

While higher prices should eventually incentivize new supply, development lead times for mining projects mean supply responses lag price signals by years, potentially extending current deficit periods.

Substitution Risks

Studies are ongoing for alternative technologies using cheaper metals but their viability remains uncertain. Despite current price fluctuations, experts anticipate that substitution will become more appealing as silver prices rise, ultimately leading to a market equilibrium at higher price levels.

However, silver's unique properties make substitution challenging in many critical applications.

Silver's Strategic Investment Case

The convergence of structural supply deficits, accelerating industrial demand, and transparent market reporting creates compelling investment opportunities in silver. LBMA vault data provides measurable evidence of physical market tightness, while companies like Americas Gold & Silver, Vizsla Silver, and Cerro de Pasco Resources offer different approaches to capturing silver's potential upside.

Key Investment Takeaways

The silver market's fifth consecutive year of deficits, combined with record industrial demand and declining inventories, suggests prices may need to move significantly higher to restore balance. For investors, this creates opportunities across the silver value chain, from physical silver and ETFs for conservative exposure to mining stocks for maximum leverage.

Strategic Positioning

Looking ahead, uncertainty over US trade and foreign policy, record-high US equities, and worries about US public debt levels should all reinforce interest in portfolio diversification, which in turn will benefit silver and gold investment.

Silver's dual role as an industrial metal and monetary asset positions it uniquely for a macroeconomic environment characterized by inflation concerns, currency debasement, and technological transformation. The question for investors isn't whether silver prices will rise, but which companies and investment vehicles will best capture this structural opportunity.

For institutional investors and individuals alike, silver represents more than a commodity play, it's exposure to the intersection of technological advancement, monetary uncertainty, and resource scarcity. The companies positioned to benefit from these trends offer compelling risk-adjusted returns in an increasingly uncertain global economy.

The Investment Thesis for Silver

- Allocate 60% to established producers (First Majestic, Pan American Silver), 25% to development-stage companies (Vizsla Silver), and 15% to streaming companies (Wheaton Precious Metals) to capture different risk-return profiles while maintaining sector exposure.

- Focus on companies deriving 70%+ revenue from silver like Americas Gold & Silver (80% silver revenue) rather than diversified miners, as these stocks typically provide 2-3x leverage to silver price movements during bull markets.

- Increase silver equity allocations by 25-50% if LBMA vault inventories decline below 20,000 tonnes or industrial demand exceeds 750 million ounces annually, as these metrics historically precede significant price breakouts.

- Weight portfolio toward Mexican operations (60%) given the country's position as the world's largest silver producer, while maintaining meaningful exposure to US operations (40%) for political stability and currency considerations.

- Deploy dollar-cost averaging strategies during 15%+ price corrections in silver stocks, as historical analysis shows these drawdowns typically reverse within 6-9 months during structural bull markets driven by supply deficits.

- Increase portfolio weights by 20% when solar industry silver consumption exceeds 300 million ounces annually or EV silver demand surpasses 100 million ounces, as these thresholds indicate irreversible industrial adoption curves that support sustained higher prices.

Analyst's Notes

Subscribe to Our Channel

Stay Informed