$5,000 per ounce possible as Gold passes $3,600: Best Mining Stocks for 2025 Bull Run

Gold reaches historic $3,600/oz driven by Fed rate cuts, central bank buying, dollar weakness. Top miners like Barrick, Newmont post record profits. Strong 2025 outlook.

- Gold has reached unprecedented heights of $3,600+ per troy ounce, driven by weak U.S. labor market data raising hopes for Federal Reserve rate cuts, with gold entering the second half of 2025 up 26% shaped by a weaker US dollar, persistent geopolitical risk, robust investor demand and continued central bank purchases.

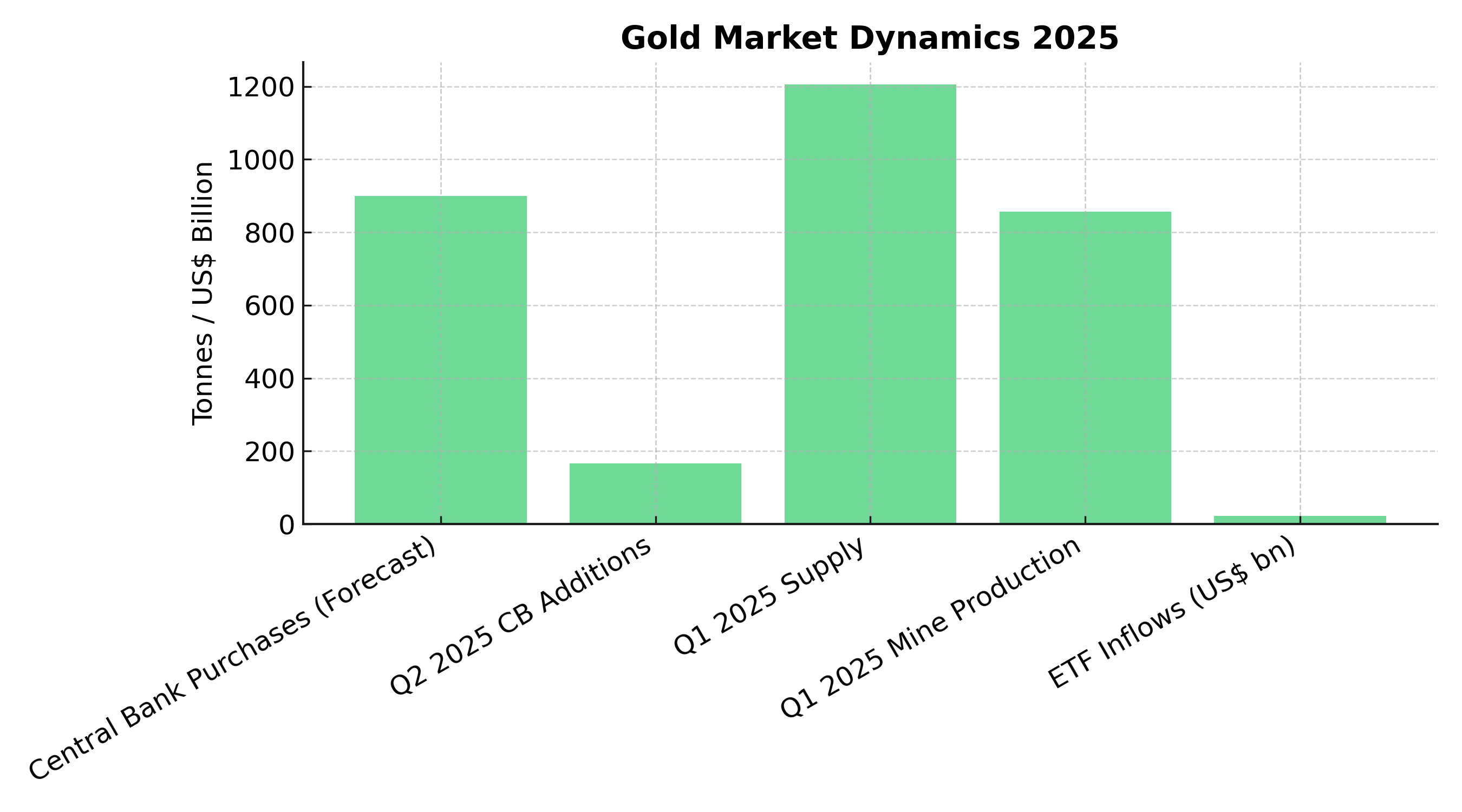

- Consistently high levels of purchases by CBs (900 tonnes forecasted in 2025) are expected, given the current macro environment, with Central banks remained a key pillar of global demand, adding 166t to global official gold reserves in Q2 alone.

- Total Q1 gold supply grew 1% y/y to 1,206t. Mine production inched up to a Q1 record of 856t, while demand continues surging with Bar and coin investors also joined the fray, attracted by the rising price and gold's safe-haven attributes.

- Cumulative net flows for North American gold-backed ETFs have reached US$22bn in inflows through July – 99% of which came from US based funds– and are on pace for their second-strongest annual performance on record.

- Research predicts gold will rise to $3,700 a troy ounce by the end of 2025, with Prices are expected to average $3,675/oz by the fourth quarter of 2025 and climb toward $4,000 by mid-2026.

Why Gold Investment Dominates 2025: The Ultimate Safe Haven Strategy

Gold has entered a historic bull market phase, with gold entering the second half of 2025 coming off an exceptionally strong start to the year – up 26%. The precious metal's surge reflects a confluence of macroeconomic pressures that position it as the premier hedge against uncertainty. From Federal Reserve policy shifts to geopolitical tensions and dollar weakness, gold has reclaimed its role as the ultimate store of value in an increasingly volatile financial landscape.

The current environment presents compelling reasons for investors to consider gold exposure. In 2024, gold prices soared to record highs. In 2025, gold has continued its strong performance and moved above $3,000. It has been the best-performing major asset over the past year. This performance isn't merely speculative – it's driven by fundamental shifts in global monetary policy, central bank behavior, and investor sentiment that suggest sustained strength ahead.

Global Monetary Policy Driving Demand

The most significant catalyst for gold's rally has been the shifting U.S. monetary policy landscape. Gold hits $3,600 as US rate cut expectations rise, reflecting how financial markets are positioning for a more accommodative Federal Reserve stance. As we look into 2025, market consensus suggests that the Fed will deliver 100 bps in cuts by year end, with inflation softening but still above target.

This monetary easing cycle creates multiple tailwinds for gold. Lower interest rates reduce the opportunity cost of holding non-yielding assets like gold, while concerns about currency debasement drive investors toward hard assets. A steep 10% drop in the dollar's value during 2025 underpins gold's gains, demonstrating how dollar weakness translates directly into gold strength.

The political dimension adds another layer of complexity. Trump's attempt to dismiss Fed governor Lisa Cook deepens fears of a compromised central bank, increasing gold's attractiveness as an inflation hedge. Such political interference concerns reinforce gold's appeal as a monetary asset independent of government control.

Central Bank Accumulation Strategy

Perhaps the most structurally significant driver of gold demand comes from central banks worldwide. Consistently high levels of purchases by CBs (900 tonnes forecasted in 2025) are expected, given the current macro environment. This isn't a temporary phenomenon but part of a strategic shift in global reserve management.

Diversification away from U.S. dollar (USD) reserve holdings, while still moderate, has been accelerating in recent years, according to the latest Currency Composition of Official Foreign Exchange Reserves (COFER) data from the International Monetary Foundation (IMF). Central banks are increasingly viewing gold as essential for monetary sovereignty and protection against sanctions risks.

The scale of this demand is remarkable. Central banks remained a key pillar of global demand, adding 166t to global official gold reserves in Q2 2025 alone. This surge has been driven, in part, by robust central bank demand—including from emerging markets such as China, India, and Turkey. Such consistent, price-insensitive buying provides a strong floor for gold prices.

Supply-Side Constraints & Market Dynamics

While demand surges, supply growth remains constrained. Total Q1 gold supply grew 1% y/y to 1,206t. Mine production inched up to a Q1 record of 856t. This modest supply increase pales compared to demand growth, creating structural imbalances that support higher prices.

Mining companies face significant challenges in expanding production. The documents reveal that even established producers are managing complex operational dynamics. For instance, Serabi Gold demonstrated how challenging it is to scale production, with EBITDA: US$12.4M; Post-tax profit: US$8.8M AISC per oz: US$1,636 (vs. US$1,700 in 2024) in Q1 2025, showing the thin margins that characterize the industry.

The supply-demand imbalance becomes more pronounced when considering recycling trends. In contrast, recycling declined 1% y/y as consumers held onto their gold hoping for higher prices. This hoarding behavior further tightens available supply.

Investment Flows & Market Participation

The investment landscape for gold has transformed dramatically in 2025. Cumulative net flows for North American gold-backed ETFs have reached US$22bn in inflows through July – 99% of which came from US based funds– and are on pace for their second-strongest annual performance on record. This institutional adoption represents a significant shift in gold's investor base.

Bar and coin investors also joined the fray, attracted by the rising price and gold's safe-haven attributes. Two consecutive quarters generated the strongest first half for bar and coin investment since 2013. This broad-based participation from both institutional and retail investors creates multiple layers of demand support.

The ETF flows are particularly significant because they represent long-term strategic allocations rather than speculative trading. Strong demand from conviction buyers—not just retail—supports sustained momentum. Portfolio managers are increasingly viewing gold as essential portfolio insurance rather than a speculative play.

Company Case Studies: Mining Sector Performance

The gold mining sector has experienced a remarkable transformation, with several companies demonstrating how to capitalize on the current environment. Let's examine three compelling case studies from the provided documents:

Perseus Mining: Established Mid-Tier Excellence

Perseus Mining Limited exemplifies operational consistency and financial discipline in the current gold environment. The company delivered Gold Produced: 496,551 oz (within guidance) for FY2025, while maintaining AISC: US$1,235/oz (below guidance range) and generating exceptional Notional Cashflow: US$650M (up US$160M YoY).

"Our revenue was… about 1.25 billion US dollars, that was up 22%. The profit after tax was 421.7 million US dollars, up 16%. Operating cash flow 536.7 million dollars, up 25%."

What sets Perseus apart is its geographic diversification and cash generation ability. With operations across Yaouré (Côte d'Ivoire), Edikan (Ghana), and Sissingué (Côte d'Ivoire), the company has built resilience against single-country risks. The company's Net Cash & Bullion: US$827M, zero debt position provides exceptional financial flexibility, while their track record of Last 4 years: Averaged 509,000 oz/year at AISC US$1,048/oz demonstrates consistent execution across commodity cycles.

Integra Resources: Strategic Growth in the Great Basin

Integra Resources represents a compelling growth story in Nevada's prolific mining region. The company achieved record revenue: $61.1 million; net earnings: $10.6 million (or $0.06/share) in Q2 2025, with strong Operating margin: 41%; mine-site AISC: $2,641/ounce at their Florida Canyon operation.

CEO George Salamis has positioned Integra as a "Growing Precious Metals Producer in the Great Basin" with a three-pillar strategy spanning Florida Canyon, DeLamar, and Nevada North projects. The company's Mine Plan of Operations (MPO) received a determination of completeness from the U.S. BLM for the DeLamar Project, advancing it toward environmental review. With Cash & cash equivalents: $63 million as of June 30, 2025, Integra has the balance sheet strength to execute its expansion plans in a rising gold price environment.

"If there's one thing I can say about where the company is now, it's that I've never been more proud of the team I work with. We truly have passionate, bright, and hardworking people all pulling in one direction, and it's an exciting time to be here."

Serabi Gold: Sustainable Growth Model

Serabi Gold exemplifies how focused execution can drive shareholder returns. The company achieved Record quarterly gold production: 10,532 oz, a 17% increase YoY in Q2 2025. CEO Mike Hodgson, with over two decades of experience in Brazilian mining operations, has positioned the company for Phased Growth Strategy Toward 100koz+ Output through systematic operational improvements.

"We've been down and through the ringer a little bit at Coringa with permitting… We will take that experience and we back ourselves to… put this operation… into operation."

The company's financial metrics demonstrate operational excellence: First Half 2025 (H1): Gold production: 20,545 oz (14% YoY increase); EBITDA: US$26.3M (vs. US$13.0M in H1 2024); post-tax profit: US$18.9M; EPS: US$0.2499 – more than doubling from prior year. This performance showcases how well-managed miners can generate substantial returns during gold bull markets.

West Red Lake Gold: Development Success Story

West Red Lake Gold Mines presents a compelling restart story, having Purchased Madsen in 2023, a distressed asset, for a restart ahead of rising gold prices. The company's execution has been exemplary, achieving 9,550 oz produced (Jan–July 2025), average 650 tpd throughput, 95% recovery.

"When a gold bull market happens, the gold companies that outperform most markedly are the ones that are putting new gold mines into production

CEO Shane Williams and his team have demonstrated how strategic timing and operational expertise can unlock value. The company's PFS Base Case (Jan 2025): NPV: C$496M at US$2,640/oz. Head grade: 8.2 g/t Au. Free cash flow: C$94M/year over 6 years. AISC: US$1,681/oz shows the substantial economics possible in the current gold price environment.

Cabral Gold: District-Scale Potential

Cabral Gold represents the exploration upside available in the sector. Led by CEO Alan Carter, who Co-discovered Tocantinzinho deposit, sold Peregrine Metals for $487M, 35+ years of experience, the company is advancing its Cuiú Cuiú project in Brazil's prolific Tapajós Gold Province. CEO Alan Carter explained:

"The key is being available, boots on the ground, transparent, and in continuous communication with communities and regulators at all levels."

The company's Starter Heap-Leach Operation (PFS, July 2025): After-tax IRR: 78% (at $2,500/oz gold); rises to 139% at $3,340/oz. NPV5: US$74M base case; US$138M at spot ($3,340/oz) demonstrates how current gold prices transform project economics.

i-80 Gold: Building Nevada's Next Mid-Tier Producer

i-80 Gold represents one of the most compelling growth stories in Nevada's gold sector. Under CEO Richard Young's leadership, the company is executing an ambitious plan to build a diversified mid-tier producer targeting ~600,000 ounces annually by the early 2030s.

The company's portfolio spans five brownfield projects across Nevada's proven mining districts, with total resources of 6.5 Moz M&I + 7.5 Moz Inferred gold, plus significant silver at Mineral Point (106.5 Moz M&I + 93.4 Moz Inferred). What sets i-80 apart is its strategic phased approach: Phase 1 (2028-2029) targeting 150k-200k oz through Granite Creek UG, Archimedes UG, and Lone Tree autoclave restart; Phase 2 (2030-2031) scaling to 300k-400k oz by adding Cove UG and Granite Creek OP; and Phase 3 (2032+) reaching 600k+ oz with Mineral Point OP. CEO Richard Young noted:

"i-80 Gold has four past producing properties in Nevada… 14 million ounces of gold and over 200 million ounces of silver, which makes us one of the largest resource holders in Nevada."

The company's portfolio NPV potential ranges from $1.6B at $2,175/oz gold to $4.5B at $2,900/oz, demonstrating substantial leverage to current gold prices. With $133.7M cash and a clear recapitalization strategy including debt financing of $350M-$400M, i-80 Gold is positioned to capitalize on Nevada's tier-1 jurisdiction advantages.

Market Outlook & Price Forecasts

The consensus among major financial institutions points to continued gold strength. Research predicts gold will rise to $3,700 a troy ounce by the end of 2025, representing significant upside from current levels. Research projects a base case of $4,000/oz by mid-2026, with a potential upside nearing $5,000 if dollar assets significantly shift into gold.

These aren't outlier predictions. Analysts offer mixed forecasts for gold prices in 2025. Most of them expect the precious metal to slide to $3,200 by the end of the year. More optimistic estimates suggest that the price will rise to $3,670 in December. Even the more conservative estimates suggest prices well above historical norms.

The longer-term outlook remains bullish. As these trends continue to play out and reshape the global economic order in the coming years, we believe gold has the potential to ascend toward $5,000 per ounce. Analysis suggests this isn't merely cyclical but reflects structural changes in the global monetary system.

Risk Considerations & Market Dynamics

Despite the bullish outlook, investors must consider potential risks. In turn, sustainable conflict resolution and continued rising stock prices could lure more risk on flows and limit gold's appeal. Improved geopolitical conditions or extended equity market rallies could reduce safe-haven demand.

Market positioning also presents risks. Non-commercial futures and option long positions in COMEX gold — the primary futures and options market for trading metals — reached a new high in 2024 in real terms. Excessive bullish positioning could lead to profit-taking corrections.

However, the fundamental drivers remain intact. While some of these drivers are expected to persist, the path forward remains highly dependent on multiple factors including trade tensions, inflation dynamics, and monetary policy. The interconnected nature of these factors suggests continued support for gold.

The Investment Thesis for Gold

- Allocate 5-10% of portfolios to gold exposure through ETFs like GLD or physical holdings, as North American ETF inflows reached $21bn in H1 and remain on pace for record performance.

- Focus on established producers like Newmont, Barrick, and Agnico Eagle, which have demonstrated operational excellence and strong cash generation in the current environment.

- Companies like West Red Lake Gold and Serabi Gold offer compelling growth stories with defined paths to increased production and proven management teams.

- Use any corrections as buying opportunities, given the structural demand from central banks and limited supply growth constraining the market.

- A steep 10% drop in the dollar's value during 2025 underpins gold's gains, making dollar trends crucial for tactical positioning.

- Consider small allocations to companies like Cabral Gold with district-scale potential and experienced management teams for higher-risk, higher-reward exposure.

Gold's New Foundation: From Cyclical Rally to Structural Support

Gold's 2025 performance represents more than a cyclical rally – it reflects fundamental shifts in global monetary policy, central bank strategy, and investor behavior that favor continued strength. The convergence of Fed rate cuts, dollar weakness, persistent geopolitical tensions, and structural central bank buying creates a compelling environment for gold investment.

The mining sector offers multiple ways to access this opportunity, from established producers demonstrating strong cash generation to development companies with compelling project economics at current prices. However, investors should maintain realistic expectations about volatility and consider gold as portfolio insurance rather than a growth vehicle. The most successful approach combines strategic allocation to established miners with selective exposure to quality development stories, while maintaining awareness of the macro factors driving the entire sector.

TL;DR Summary

Gold has surged to unprecedented $3,600+ levels in 2025, driven by Federal Reserve rate cut expectations, dollar weakness, and massive central bank purchases totaling 900 tonnes annually. North American gold ETFs have attracted $22 billion in inflows, positioning for their second-strongest year on record. Mining companies are capitalizing on this environment: Perseus Mining generated $650M cash flow with zero debt, Integra Resources achieved 41% operating margins, while development stories like West Red Lake Gold and i-80 Gold demonstrate substantial project economics at current prices. Supply constraints persist as mine production grows only 1% annually while demand surges from both institutional and retail investors. Analysts predict gold reaching $3,700 by year-end 2025 and $4,000 by mid-2026, supported by structural shifts in global monetary policy and continued central bank diversification away from dollar reserves.

Top 5 FAQs

Disclaimer: These FAQs are AI-generated based on analysis of gold market content and common investor inquiries.

Q1: Why has gold reached record highs above $3,600 in 2025?A1: Gold's surge reflects multiple converging factors: Federal Reserve rate cut expectations reducing opportunity costs for non-yielding assets, a 10% dollar decline, persistent geopolitical tensions, and massive central bank purchases totaling 900 tonnes annually. This combination creates structural support beyond typical cyclical rallies, with North American ETFs seeing $22 billion in inflows through July 2025.

Q2: Which gold mining companies are best positioned for the current bull market?A2: Established producers like Perseus Mining (zero debt, $650M cash flow), Integra Resources (41% operating margins), and development companies like i-80 Gold (targeting 600,000 oz annually) offer different risk-reward profiles. Perseus provides stability with consistent 500,000+ oz production, while development stories like West Red Lake Gold demonstrate how current prices transform project economics with NPVs reaching C$496M.

Q3: How high could gold prices go and what's driving the forecasts?A3: Analysts predict gold reaching $3,700 by end-2025 and $4,000 by mid-2026, with some projections approaching $5,000. These forecasts reflect structural changes including central bank diversification from dollar reserves, persistent monetary easing, and supply constraints as mine production grows only 1% annually while demand surges across institutional and retail segments.

Q4: What makes this gold rally different from previous cycles?A4: Unlike speculative rallies, current strength stems from fundamental shifts: central banks adding 166 tonnes in Q2 2025 alone as part of strategic reserve diversification, tech-driven safe-haven demand amid political uncertainty, and supply-demand imbalances as recycling declines while investment demand surges. This creates multiple structural support layers rather than momentum-driven pricing.

Q5: What are the main risks to the gold bull market outlook?A5: Primary risks include sustainable conflict resolution reducing safe-haven demand, extended equity market rallies encouraging risk-on flows, and excessive bullish positioning in futures markets creating correction potential. However, structural drivers like central bank purchases, dollar weakness, and constrained supply growth suggest corrections would likely represent buying opportunities rather than trend reversals.

Analyst's Notes

Subscribe to Our Channel

Stay Informed