Critical Mineral Security: The New Investment Supercycle Begins

Battery metals demand exploding as CATL invests €7.3B in European plant. Supply chain localization driving government-backed infrastructure. Quality assets in stable jurisdictions command premiums.

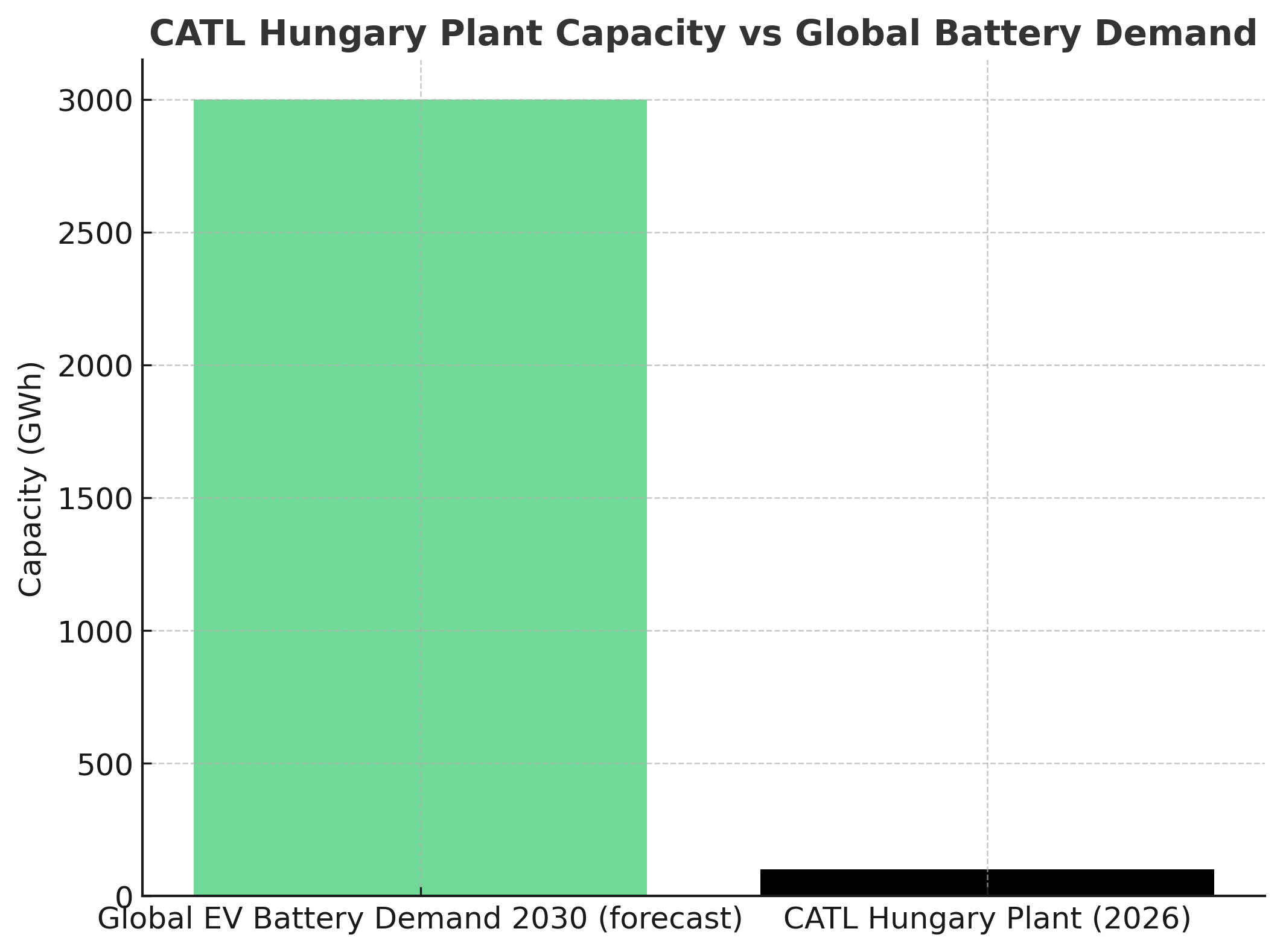

- CATL's €7.3 billion Hungarian plant (100 GWh annually by 2026) represents a 38% global battery market leader scaling European operations, driving unprecedented demand for lithium, nickel, cobalt, and graphite across localized supply chains.

- Japan's $7 billion Nacala Corridor investment and Canada's flow-through critical minerals tax incentives signal government-backed infrastructure development to secure critical Mineral supply chains outside China-dominated networks.

- Canada Nickel's Reid project extensions (1,018-meter mineralized intervals) & Sovereign Metals' Japanese-backed infrastructure access demonstrate how new discoveries and transport solutions are unlocking previously uneconomic critical mineral deposits.

- Flow-through critical minerals expenditures and strategic government partnerships are channeling billions into exploration and development, with CAD $22.5 million Gladiator Metals raising exemplifying institutional appetite for early-stage critical mineral exposure.

- Projects in stable jurisdictions (Canada, Malawi via Japanese backing) with verified specifications (Toho Titanium validation) command premium valuations as ESG-conscious battery manufacturers prioritize supply chain security over lowest-cost sourcing.

Critical Minerals: The Essential Investment Theme for the Next Decade

The global transition to electric vehicles isn't just reshaping the automotive industry—it's creating the largest commodity supercycle in modern history. As battery manufacturers race to meet exploding EV demand, the critical minerals that power these energy storage systems have become the new oil of the 21st century. Recent developments across the critical mineral supply chain reveal why savvy investors are positioning themselves in this transformative sector.

The Scale of Opportunity: Unprecedented Demand Growth

The critical mineral investment thesis begins with simple mathematics: every electric vehicle requires substantial quantities of lithium, nickel, cobalt, graphite, and manganese. With global EV sales projected to reach 30 million units annually by 2030, the mineral requirements are staggering.

CATL's recent announcement of its Hungarian facility perfectly illustrates this demand explosion. The Chinese battery giant, commanding a 38% share of the global EV battery market, is investing €7.3 billion in a single European plant capable of producing 100 gigawatt-hours annually by early 2026. To put this in perspective, this single facility will require thousands of tons of battery-grade lithium, nickel, and graphite each year—equivalent to the entire output of several medium-sized mines.

"CATL expects its Hungarian production to start by early 2026," according to recent company statements, with the facility designed to serve European automakers including BMW, Stellantis, and Volkswagen. This timeline compression—moving ahead of original end-2025 projections—reflects the urgent demand from automotive partners who cannot afford battery supply bottlenecks.

The implications extend far beyond a single plant. CATL's European expansion represents the beginning of a massive industrial buildout that will replicate across multiple continents. Tesla's Gigafactories, CATL's facilities, and emerging players like QuantumScape are all racing to secure long-term battery metals supply agreements, creating a seller's market for quality producers.

This supply-demand imbalance is further exacerbated by the broader challenges facing the mining industry. As Merlin Marr-Johnson, CEO of Fitzroy Minerals, explains:

"Mineral deposits are deeper and lower grade; the majors are spending more just to stand still—and the demand trend is shifting up with AI and electrification. That's why the long-term slide in copper's real price cannot continue."

This insight applies equally to other critical minerals, where easily accessible, high-grade deposits are increasingly rare while demand continues its exponential growth.

Supply Chain Localization: The New Strategic Imperative

Perhaps the most significant trend reshaping battery metals investment is the urgent push toward supply chain localization. The COVID-19 pandemic and subsequent geopolitical tensions have made clear the risks of over-dependence on single-country supply chains, particularly for materials as strategically important as critical minerals.

Japan's commitment of $7 billion to develop the Nacala Corridor through Malawi, Mozambique, and Zambia exemplifies this strategic shift. This infrastructure investment, combining $5.5 billion through the African Development Bank and $1.5 billion in public-private partnerships, is specifically designed to secure Japanese access to critical minerals outside traditional supply chains.

Sovereign Metals' Kasiya project stands to benefit directly from this infrastructure development. The company's rutile and graphite deposits in Malawi will gain access to deep-water port facilities at Nacala, dramatically reducing transportation costs and logistics risks. Toho Titanium, a major Japanese industrial company, has already confirmed that Kasiya's natural rutile meets specifications for high-performance titanium metal production, providing crucial market validation.

CEO Frank Eagar emphasizes the strategic significance of this development:

"Japan's commitment to the Nacala Corridor infrastructure validates our strategic positioning and creates powerful opportunities for Kasiya's development."

This government-backed infrastructure investment transforms what might otherwise be a stranded asset into a commercially viable operation with reliable export routes to key markets.

The localization trend is equally pronounced in North America. Canada's flow-through critical minerals tax incentives are channeling substantial investment capital into domestic exploration. Gladiator Metals' recent CAD $22.5 million private placement, specifically structured to fund "flow-through critical mineral mining expenditures" in Yukon Territory, demonstrates how policy frameworks are accelerating capital deployment.

These aren't isolated examples but part of a coordinated strategy across developed economies to establish reliable, geographically diversified critical minerals supply chains. The European Union's Critical Raw Materials Act, the United States' Inflation Reduction Act, and similar initiatives in Australia and Canada all prioritize domestic or allied-nation sourcing of battery materials.

Best Critical Mineral Companies: Quality Assets in Stable Jurisdictions

The investment landscape in battery metals is rapidly stratifying between companies with quality assets in stable jurisdictions and those facing regulatory, political, or technical challenges. Recent developments highlight which characteristics institutional investors are prioritizing.

Canada Nickel exemplifies the premium placed on Tier-1 jurisdictions with scalable resources. The company's Reid Nickel Sulphide Project, located just 39 kilometers northwest of Timmins, Ontario, has reported remarkable exploration success. Recent drilling has extended nickel mineralization 300 meters deeper than previously known, with one exceptional interval of 1,018 meters grading 0.28% nickel, including higher-grade sections of 0.42% nickel over 45 meters.

The Reid project's December 2024 resource estimate already showed substantial scale: 0.59 billion tonnes indicated at 0.24% nickel (approximately 1.4 million tonnes of contained nickel) and 0.99 billion tonnes inferred at 0.23% nickel (approximately 2.2 million tonnes contained nickel). The exploration target suggests potential for an additional 0.9 to 2.1 billion tonnes at 0.20-0.22% nickel grades.

CEO Mark Selby's confidence in the project's trajectory is evident in his recent comments:

"Reid continues to deliver, with today's results confirming its substantial potential size and scale… We look forward to further demonstrating Reid's scale with an updated resource by year-end."

Selby positions Reid as potentially exceeding their flagship Crawford project in scale. The company's "NetZero Nickel" branding reflects growing demand from battery manufacturers for sustainably produced materials with verified low carbon footprints.

Similarly, Sovereign Metals benefits from strategic government backing for its Malawi operations. The company's relationship with Mitsui & Co. through existing memorandums of understanding provides market access certainty, while Japanese government infrastructure investment reduces project development risks.

Top Cricial Mineral Stocks: Positioning for Multiple Growth Vectors

The current market environment offers multiple pathways to critical mineral exposure, each with distinct risk-return profiles suited to different investor objectives.

Major diversified miners like BHP Billiton, Vale, and Glencore provide battery metals exposure through existing nickel and cobalt operations while offering portfolio diversification. These companies have the capital resources to expand production rapidly as demand accelerates.

Companies like Canada Nickel, Sovereign Metals, and similar developers offer direct exposure to specific battery metals with significant operational leverage to commodity price increases. These companies typically carry higher risk but proportionally higher potential returns as projects advance through development stages.

Early-stage companies like Gladiator Metals provide the highest-risk, highest-potential-reward exposure. Gladiator's focus on Yukon Territory exploration, backed by flow-through financing structures, offers investors tax-advantaged exposure to discovery upside in an under-explored jurisdiction.

Companies providing processing, refining, or logistics services for battery metals offer exposure to sector growth without direct commodity price risk. The development of North American lithium processing facilities and battery materials refining capacity creates opportunities in this segment.

Critical Mineral Investment Strategy: Risk-Managed Exposure

Successful battery metals investing requires understanding the sector's unique characteristics. Unlike traditional commodities, critical minerals often require specific technical specifications, long-term supply agreements, and complex processing capabilities. This creates both opportunities and risks that investors must navigate carefully.

The technical specifications requirement creates barriers to entry that can protect established suppliers. Toho Titanium's validation of Sovereign Metals' rutile quality exemplifies how meeting precise industrial specifications provides competitive advantages. Similarly, battery-grade lithium requires substantially higher purity levels than traditional industrial lithium, limiting the number of qualified suppliers.

Long-term supply agreements provide revenue visibility but can also limit upside participation if spot prices rise dramatically. CATL's approach of securing multi-year agreements with automakers creates predictable demand but also constrains pricing flexibility. Investors should evaluate how potential investments balance contract security with price participation.

Processing and refining capabilities often determine whether raw material producers can capture value-added margins. Canada Nickel's integrated approach, potentially producing finished nickel products rather than concentrate, could significantly enhance project economics compared to traditional mining models.

Geopolitical considerations are increasingly important in battery metals investment decisions. Projects in stable jurisdictions with supportive regulatory frameworks command premium valuations, while operations in politically uncertain regions face discount pricing regardless of resource quality.

Critical Minerals Market Outlook: Structural Growth Drivers

Multiple converging factors support a multi-year growth cycle for critical minerals demand, creating favorable conditions for well-positioned investments.

Automotive electrification remains the primary demand driver, but energy storage applications are emerging as equally significant. Grid-scale battery storage requirements for renewable energy integration could ultimately consume as much battery capacity as transportation applications, effectively doubling long-term mineral requirements.

Battery chemistry evolution affects specific metal demand patterns but unlikely to eliminate any major battery metals entirely. While lithium iron phosphate (LFP) batteries reduce nickel and cobalt requirements per unit, their lower energy density means larger batteries for equivalent performance, potentially maintaining or increasing total mineral consumption.

The replacement cycle for first-generation EV batteries will create substantial recycling feedstock beginning around 2030, but recycling cannot meet primary demand growth. New mine development remains essential, supporting continued investment in exploration and development companies.

Government policy support appears durable across political cycles due to energy security, climate change, and industrial competitiveness considerations. The bipartisan nature of critical minerals policy in the United States, cross-party support in Canada, and strategic consensus in Europe and Japan suggest continued policy support regardless of electoral outcomes.

The Investment Thesis for Battery Metals

- Allocate 40% to established producers, 35% to advanced developers, 25% to exploration plays to balance current income with growth potential while maintaining discovery upside.

- Focus investments on projects in Canada, Australia, Chile, and select African countries with strong Japanese/European backing, avoiding single-country political risk concentration.

- Target companies with verified product quality from end-users like Toho Titanium validation, as meeting exact technical requirements creates competitive moats and pricing power.

- Use lithium price volatility and broader market selloffs to accumulate quality assets, as underlying EV adoption trends remain intact despite short-term fluctuations.

- Emphasize companies with established sustainability credentials and low-carbon production methods, as battery manufacturers increasingly require verified supply chain ESG compliance.

- Utilize flow-through share structures and tax-advantaged investment vehicles where available, as governments are subsidizing critical minerals exploration and development through favorable tax treatment.

The battery metals sector represents one of the clearest structural growth opportunities in global commodities markets. The convergence of massive demand growth from EV adoption, urgent supply chain localization requirements, and supportive government policies creates a favorable investment environment for quality companies with the right assets in stable jurisdictions.

Investors should approach the sector with a portfolio strategy that balances established producers offering near-term cash flows with development companies providing operational leverage to rising commodity prices and exploration plays offering discovery upside. The key to success lies in understanding that battery metals are not just commodities but strategic materials requiring technical precision, supply chain security, and long-term thinking.

The companies and projects highlighted in recent developments—CATL's European expansion, Japan's Nacala Corridor investment, Canada Nickel's resource growth, and policy-supported exploration financing—demonstrate that the sector is moving beyond speculative investment toward industrial-scale development backed by major corporations and governments. This maturation process creates opportunities for investors who can identify and support the companies best positioned to serve this massive and growing market.

Analyst's Notes

Subscribe to Our Channel

Stay Informed