EMX Royalty (TSX-V: EMX) - Revenue Deceptively Good

Interview with David Cole, President and CEO of EMX Royalty Corp. (TSX-V:EMX, NYSE:EMX)

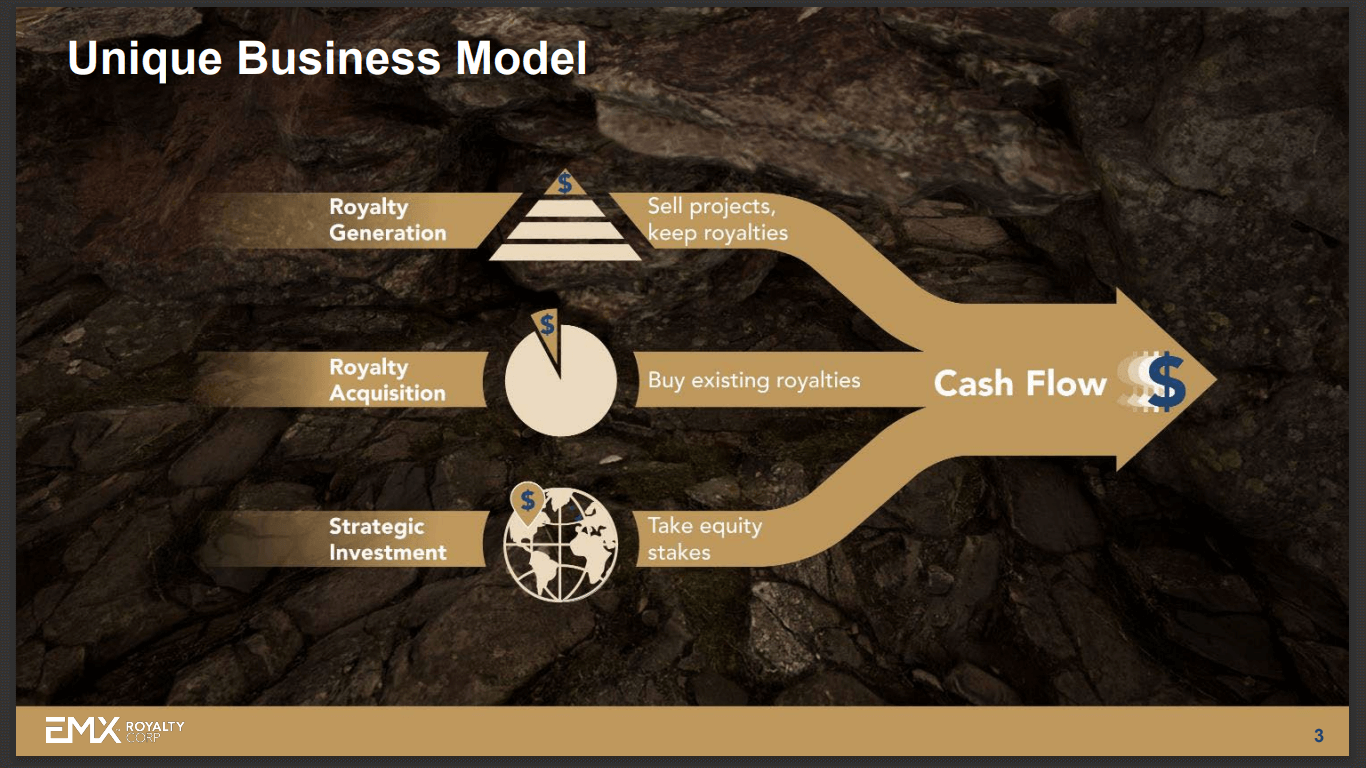

EMX Royalty Corp. is a Canada-based precious, base, and battery metals royalty company. The company has a track record of success in exploration, discovery, royalty generation, and strategic investments across 5 continents. The company organically generates royalties through low-cost property acquisition and early-stage exploration to build value.

Matt Gordon caught up with David Cole, President, CEO, and Director, EMX Royalty. David has over 3 decades of industry experience, coming to EMX from Newmont Mining Corp. At Newmont, he held a number of management and senior geologic positions, gaining extensive global experience as a project, mine, and generative exploration geologist in Nevada, Southeast Asia, South America, Europe, and Central Asia. David’s success as part of Newmont’s exploration team includes contributions to the world-class Carlin Trend, Yanacocha, and Minahasa mines. Subsequently, he established and managed Newmont’s exploration programs in Turkey while also identifying early-stage acquisition targets in Eastern Europe. He specialises in developing new exploration ideas and opportunities, based on solid technical expertise coupled with a keen business sense. He studied under Dr. Tommy Thompson at Colorado State University, earning an M.S. in Geology.

Company Overview

EMX Royalty Corp. was founded in 1996 and is headquartered in Vancouver, British Columbia. It is listed on the Toronto Stock Exchange (TSX-V: EMX), the New York Stock Exchange (NYSE: EMX), and the Frankfurt Stock Exchange (FSE: 6E9). Vlad Royalties AB, Bullion Monarch Mining Inc, Waikato Gold Limited, EMX Scandinavia AB, Dourave-Bullion Joint Venture LP, EMX- NSW1 Pty Ltd, EMX Finland OY, Azur Medencilik Ltd. Sirketi, Dedeman Madencilik Sanayi Ve Ticaret Anonim Sirketi, Boreal Battery Metals Scandinavia AB, Eurasian Royalty Madencilik AS, EMX Properties (Canada) Inc, EMX Broken Hill Pty Ltd, EMX Australia Pty Ltd, Phelps Dodge Exploration Sweden AB, Eurasian Minerals Cooperatief U.A., EMX Chile SpA, Eurasia Madencilik Ltd. Sti, EV Metals AB, Minera Tercero SpA, and Bronco Creek Exploration, Inc are the company’s subsidiaries.

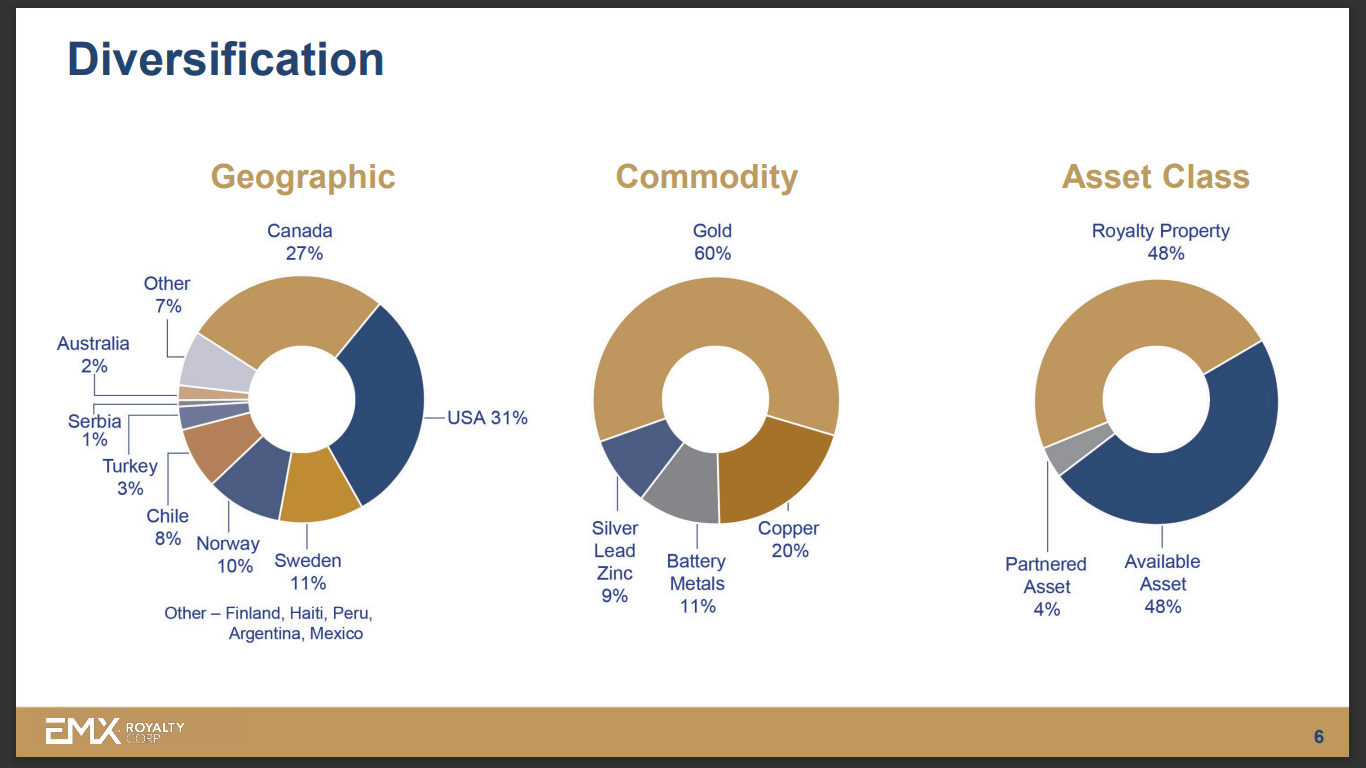

EMX Royalty accumulates royalties on mining projects around the world. The company has built a highly-successful portfolio over the last 19.5 years that comprises nearly 5M acres of mineral rights.

Cash Position

In Q2 2022, EMX Royalty reported a net loss of $4.1M. Almost the entire amount comprised non-cash items that were accounting-related. This includes the adjustment of the portfolio of shares that were paid to the company, along with part and parcel for deals conducted. The company’s portfolio is valued at about $20M in assets. It has to be marked to market every quarter. The $4M loss was due to the adjustment of the value that is marked to the market.

The remainder of the loss comes from the currency exchange rates. The company’s debt is in US dollars, while its accounting is carried out in Canadian Dollars. Each quarter, there is a small move in the CAD-USD exchange rate, that needs to be adjusted. It is important to note that despite the numbers, there wasn’t any material impact on the business. In fact, the company posted record revenue of over USD$12M for the second quarter of 2022. The company’s EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) was CAD$6.1M.

The company carried out all its options issuance in the second quarter of 2022, amounting to $2.7M. The amortization and depletion accounted for $1.3M, while the finance charges were $1.7M. The figures were in actual cash and weren’t included in the EBITDA. The fair value adjustments of $4.4M along with the $4M currency adjustments could lead the numbers into negative territory largely due to the non-cash issues. It is important to note that these do not affect the core business.

At the same time, the company posted a positive EBITDA of CAD$6.1M for the second quarter on a CAD$12M record revenue. The company continues to increase its cash flow. Coming into 2023, it will start receiving revenues from the Gediktepe royalty, and the Balya North royalty property.

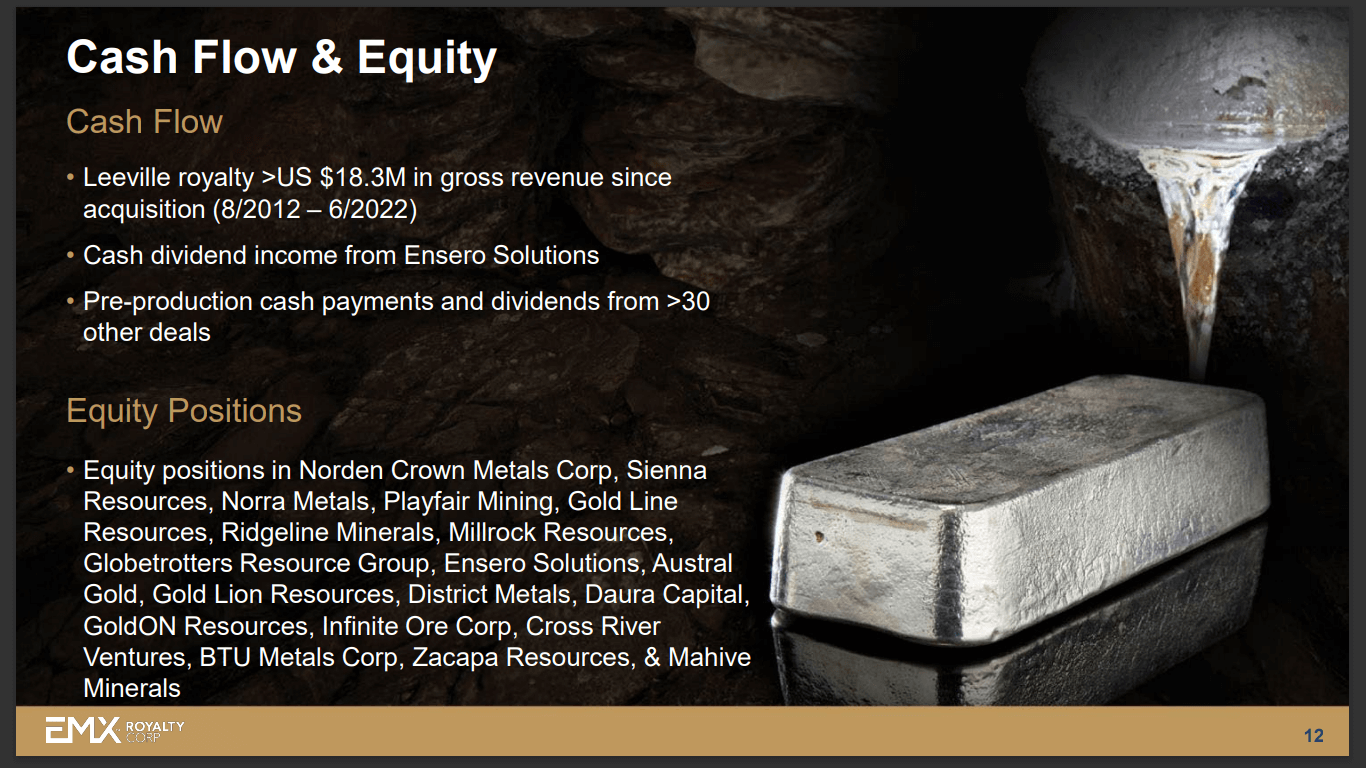

The company is also generating a substantial cash flow from Caserones royalty, the copper-molybdenum mine in Chile. It is receiving about $7.5M after tax that is repatriated to Canada. The company owns under 50% of the shares. It has to carry out equity accounting on the cash flow on a monthly basis. As a result, the numbers are not included in the official top-line number. This quarter, the company earned CAD$3.1M. The adjusted number for the top-line revenue is $12M.

The reporting is done in accordance with the law. The law states that the company has to mark its entire portfolio to the market. Even though this is an investment portfolio, the vast majority of the shares in the portfolio are paid to the company on a no-cost basis.

The company’s deal flow comprises selling assets around the world to junior companies that pay it in shares and annual payments. As a result, the company has a stock portfolio, which is one of its key assets. The stock is commonly sold to the market over time in order to capture the value for shareholders and reinvest the capital in different places.

EMX Royalty needs to mark to the market its entire portfolio each quarter. Since the natural resource capital markets have been hammered over the last quarter, the company’s securities portfolio went down by USD$4M.

Company Evaluation

EMX Royalty has an adjustment in place with respect to shared payments that are used during internal NAV (Net Asset Value) calculations. The company looks at the history of the shares that have been paid to it and compares it to the amount that could be generated had the shares been sold to the market. Next, the company comes up with a ratio and takes a conservative outlook at around 80% for internal analysis. Essentially, the company gets about 80% of the value of the stock that’s been paid.

There are often times when EMX Royalty gets over 100% in stock value if the companies are doing really well. The company ensures that this value is captured. Over the course of the last 19 years, the company has fared really well with the share payments for the sold assets, utilising the funds to create new royalties. There are also the aspects of optionality and upside for the shareholders that originate from portfolio management.

The ounce depletion reporting for royalties is done on a per-deal basis. For instance, the company’s amortization of depletion on the Caserones royalty is associated with the tax payments, which were negative CAD$1.4M for Q2 2022.

Business Strategy

It is important to note that EMX Royalty’s GNA (Good Neighbour Agreement) is higher than the competition. The company achieves this by utilising the cash flow towards growing its royalty portfolio and running the business. All the money spent acquiring prospective mineral rights, adding value, collecting soil and rock samples, and marketing the assets to the industry is expensed. The company capitalises the expenditures so that they no longer show up as expenses. On the books, these show up as capitalised expenditures. This is one of the major reasons that the company’s quarterly results look starkly different from its competition.

For example, a royalty company named X would buy a portfolio of royalties that were generated in Nevada by a private company. The portfolio would be included in X’s books. Hypothetically, if it was 12 royalties, the company ends up owning all 12. The shares and cash that was paid to buy these royalties are considered as a share transaction that goes into X’s books as an asset. Since the asset is capitalised, it does not show up in the quarter as an expense.

EMX Royalty’s business strategy is to organically grow all 12 assets over time at a fraction of the cost that was paid by company X. EMX Royalty manages its expenses every month and every quarter. This goes into the company’s GNA because a significant portion of the expense comprises employing smart people to acquire prospective mineral rights and add value by way of good geology. The accounting variance is representative of how the company conducts its business compared to the competition.

For resource depletion, when something is capitalised, it needs to be depleted over time and is eventually worked off through the books. However, country-specific rules state that a company does not need to deplete the ounces until it starts generating a cash flow. In the case of company X, the 12 Nevada royalties sit on the books without generating cash flow, and the company does not need to deplete it, even though the money is long gone.

Direct Tax Management

EMX Royalty is a dynamic company that operates across 13 countries. The company is always planning ahead for success with respect to how the assets are developed in Turkey, Chile, and other countries. It is important to note that most countries have tax treaties with Canada. For instance, there is a tax treaty between Canada and Chile, and between Canada and Turkey. As a result, if a company is paying taxes in Turkey, it does not need to pay them again in Canada, or it only has to pay the Canadian tax. It always looks to ensure that things are designed in a tax-efficient manner in order to avoid being double taxed. Taking into account all of these factors, the company ended up posting record revenues for the second quarter of 2022.

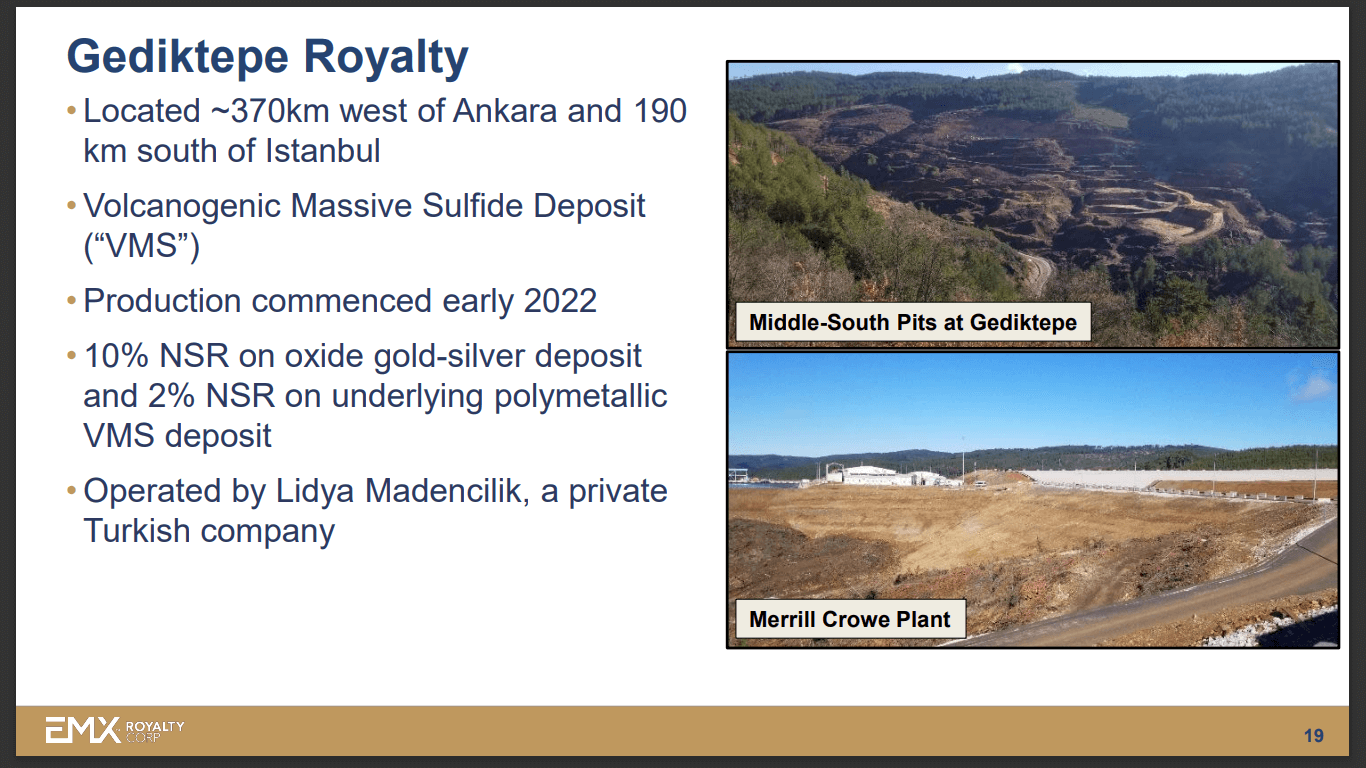

The Gediktepe royalty

Gediktepe is a polymetallic VMS (Volcanogenic Massive Sulphide) mining operation located in western Turkey, owned and operated by Lidya Madencilik, a private Turkish company. EMX Royalty has two NSR (Net Smelter Return) royalties on Gediktepe consisting of a perpetual 10% NSR royalty over metals produced from the oxide zone (predominantly gold and silver) after cumulative production of 10,000 gold-equivalent ounces, and a perpetual 2% NRS royalty over metals producers from the sulphide zone (predominantly copper, zinc, lead, silver, and gold), payable after cumulative production of 25,000 gold-equivalent ounces. Gold-equivalent is as referenced from an underlying 2019 Share Purchase Agreement. Lidya is also responsible for a series of pre-production milestone payments payable to EMX Royalty.

The Gediktepe deposit has 2 major components, the upper oxide zone where the deposit has been oxidized through geologic time, and the upper zone which is enriched in gold and silver but does not contain base metals. The upper zone has a 10% royalty, which applies to the ores that go through the oxide circuit due to the difference in the metallurgy. The counter-party has designed a completely different circuit to recover the gold and silver in the outside zone. The counterparty is looking to recover all the metals in the sulphide zone. The oxide zone has robust economics and it carries a 10% royalty. It is important to note that this is a 10% gross royalty.

The counter-party makes money on the ore’s head grade that is currently being stockpiled. The ore that is being put onto the pads is very high grade, over 2g/t. The counter-party did have some chemistry problems on the pad that slowed down operations for a bit. Temporary slowdowns were also caused due to high rainfall this year. However, since then, the counter-party has caught up and is back on schedule. The asset has produced 10,000oz of gold, officially entering commercial production.

The counterparty is currently calculating the royalty to be paid, and EMX Royalty is expecting the funds in the coming days. There’s an additional $4M payment to be made on the commercial production. The counter-party will pay EMX Royalty the funds 12 months after reaching commercial production. These funds have already been booked as per the accounting rules. EMX Royalty will receive $4M in 11 months’ time.

Every time the counter-party sells bullion, it would need to pay 10% of the gross value to the company. As per the contract, every time the counter-party makes a bullion shipment and gets paid, it needs to pay 10% of the gross value in royalty. EMX Royalty is expecting around $7M-$8M in royalty payments along with the $4M payment in 11 months, bringing the total generated revenue to $11M-$12M in the first year. The company has excellent communication with Lidya Madencilik, the counterparty.

EMX Royalty anticipates that the production at Gediktepe is going to be fairly steady for the first three years, and by the time it starts to tail off, the oxide zone will be done in about five years’ time. In the meantime, the counterparty is developing a sulphide circuit in parallel. Interestingly, the sulphide circuit also has deferred incremental payments in addition to a 2% royalty on the sulphide zone, which has a longer mine life. The zone has close to a 10-year mine life and the mineralization is open-ended at depth. It is likely that the counter-party will be able to add additional resources over time. This would be a cheap 2% royalty where the economics are driven by copper and zinc, along with some good gold and silver credit as well. The company is expecting production to commence in late 2023 for the sulphide zone.

The Caserones Copper-Molybdenum Mine

The Caserones open-pit mine is developed on a porphyry copper-molybdenum deposit in the Atacama Region of the northern Chilean Andean Cordillera. The mine has been in operation since 2014 and is owned and operated by SCM Minera Lumina Copper Chile SpA, which is indirectly 100% owned by JX Nippon Mining & Metals Corporation of Japan. EMX Royalty has an effective 0.7335% NSR royalty on Caserones and is receiving quarterly payments from the operation.

The mine produces copper and molybdenum concentrates from a conventional crusher, mill, and flotation plant, as well as copper cathode from a dump leach, solvent extraction, and electrowinning plant. In 2021, the mine produced 94,846 tons of fine copper in concentrate, 2,287 tons of fine molybdenum in concentrate, and 14,829 tons of fine copper in cathodes.

Caserones is located at the southern end of the Maricunga mineral belt and occurs as an Early-Miocene porphyry system. The deposit has a well-developed supergene enrichment profile of oxide copper and secondary chalcocite that overlies hypogene sulphide mineralization. In addition to currently defined zones of mineralization, considerable upside exists on the Caserones property, and exploration for additional resources and reserves has been ongoing.

EMX Royalty contributed CAD$3.1M to acquire 50% of the Casernoes Copper-Molybdenum Mine. Notably, the counter-party had decreased production through 2020 and 2021 due to covid-related issues. However, over the past few months, production is increasing at a consistent basis. In a case where the counter-party reaches nameplate capacity for the on-site infrastructure, the project will have an even stronger upside. Notably, 2022 is the 16th year of operation for the Caserones mine. The mine life has been successfully increased from 17 to 28 years. EMX Royalty pays taxes in Chile, and there’s no further tax owed in Canada. The company is looking to generate between USD$7M-$8M in post-tax revenue that will be repatriated to Canada from Chile from the copper and molybdenum sales.

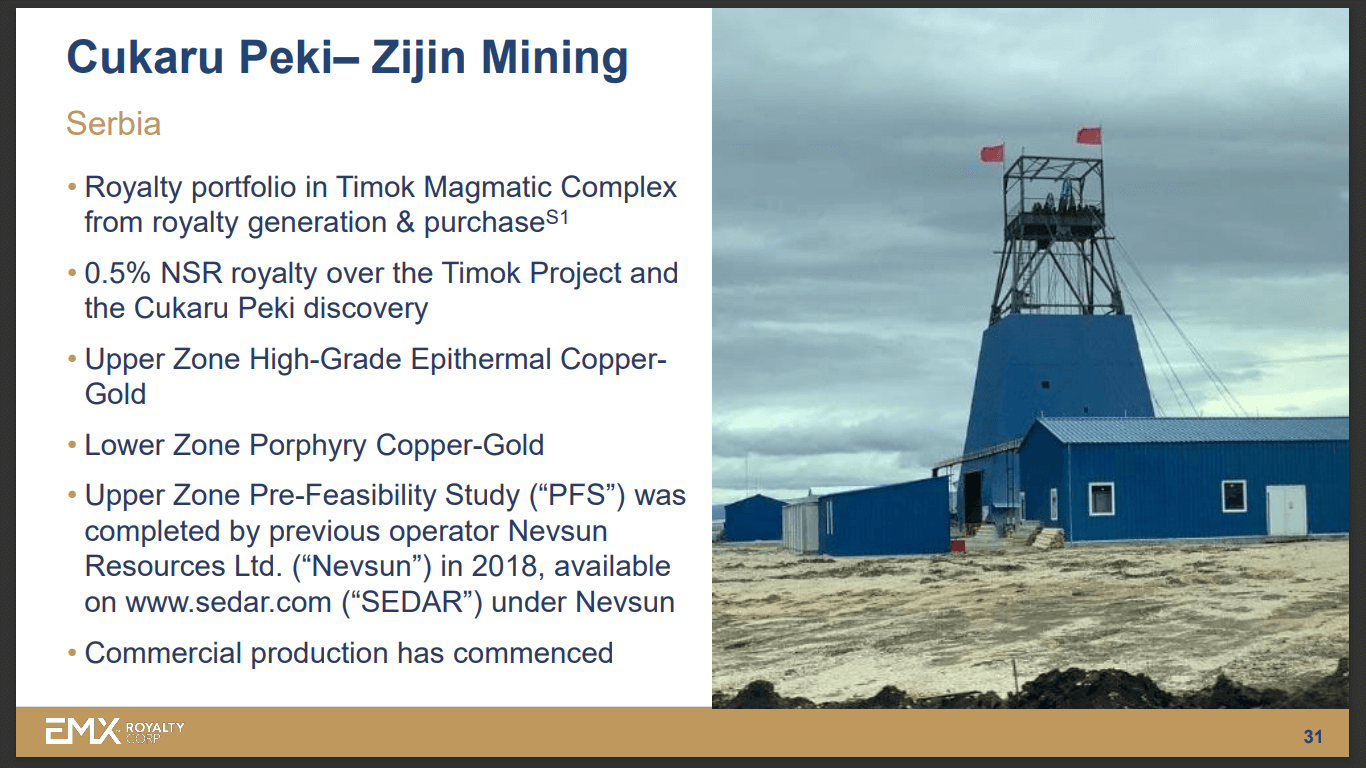

The Timok Project

EMX Royalty’s portfolio in Serbia initially resulted from prospect generation and organic royalty growth via the 2006 sale of its properties, including Brestovac West, for uncapped NSR royalties of 2% for gold and silver and 1% for all other metals. In 2013, EMX Royalty acquired 0.5% NSR royalty interests covering the Brestovac and Durlan Potok properties, which along with Brestovac West, are included in the Timok Project, which is now controlled by Zijin Mining Group Co. Ltd.

The Timok Project’s Cukaru Peki deposit, which is covered by the Bretovac NSR royalty, includes the Upper Zone underground mine which consists of high-grade, epithermal-style copper-gold mineralization, and the Lower Zone project which consists of a deeper body of porphyry-style copper-gold mineralization.

EMX Royalty continues to work with Zijin on the Timok Project. Both parties have a strong working relationship. EMX Royalty’s lawyers are working diligently to write a non-disputable royalty agreement. The resolution is expected to be announced in the near future. Both parties are focused on getting the royalty agreement done properly as opposed to the speed of execution. It is important to note that EMX Royalty will be paid for the royalties at the new agreed-upon rates for the production that has already occurred.

The Queensland Gold Royalty

EMX Royalty’s organically generated Queensland Gold exploration-stage royalty property is located in the Yarrol Province of the Tasman Orogenic Zone, which hosts significant operating gold mines and exploration projects in Queensland, Australia. Queensland Gold is under option to Many Peaks Gold Limited for pre-production payments, work commitments, and a retained 2.5% NSR royalty interest.

The Queensland Gold property encompasses a 46,400-hectare area covering historical gold mines, gold occurrences, drill-defined zones of gold mineralization, and multiple gold geochemical anomalies. Diverse styles of mineralization have been identified on the property including intrusion-related gold (IRGS), skarn, reef-type veins, and sediment-hosted copper. The styles of mineralization are similar to those seen at the nearby Mount Rawdon gold mine.

EMX Royalty has continued to map the zone and it is collecting additional samples at the Queensland Gold royalty. What differentiates it from the competition is the fact that the company also finds its own assets and works on prospecting. It is currently in the process of determining the size and importance of the zone. According to a press release published a few months back, it is a very high-grade and large cobalt system. Previously, the asset was largely unknown, but now, it has become a high-prospect asset for the company’s portfolio. While the company is yet to determine the exact business model for the asset, it is likely that it will follow the traditional model where it will sell the asset for a combination of cash, shares, and royalties. The company is also looking at other potential alternatives. The company’s current annualised run rate is a bit under $50M in revenue. For 2023, the company is expecting between $25M-$30M in revenue.

The Balya North Royalty

The Balya North royalty property is located in the historical Balya lead-zinc-silver mining district in northwestern Turkey. EMX Royalty holds an uncapped 4% NSR royalty on Balya North, which is operated by Eczacibaşi Endüstriyel Hammaddeler San. ve Tic. A.Ş. (Esan), a private Turkish company. Esan operates a lead-zinc mine and flotation mill on the property immediately adjacent to EMX Royalty’s Balya North royalty property.

Esan proceeded with underground development of the Balya North Deposit and on-site infrastructure with mining commencing in late 2021. Zinc-lead-silver mineralized material has been stockpiled on-site in preparation for processing at the Esan mill. Esan has advised EMX Royalty that it will likely be processing the material in mid-2022.

The Balya North royalty is in a similar situation as Gediktepe. The asset is currently in commercial production, which continues to increase. The company anticipates that the production will continue to grow over the course of the next five years. This project is expected to pay out hundreds of thousands of dollars in 2022, which can increase to about $1M/year over the course of the next five years. The counter-party is increasing production from underground headings. It is gaining access to the mineralized zones using a spiral decline, then increasing the number of working headings within the zone, and simultaneously increasing the mill throughput.

According to Esan Eczacibasi, the counter-party, about 70% of the mill capacity will be dedicated towards the royalty-encumbered ground. While it would take years for the counter-party to ramp up production to these levels, the exploration results continue to provide additional ounces.

Targets 2022 and Beyond

According to EMX Royalty, royalties are great assets in inflationary times. However, there is a significant difference between how the market values royalty companies and how the royalties perform themselves. The company is trading sideways in recent times, while many of its competitors have gone down even more. Its performance during this challenging timeframe has been quite good. However, there are some key catalysts, such as the settlement of the Timok issue, that will help the company achieve its targets. The company is currently in a risk-off environment in the capital markets.

The company is focused on settling the Timok issue. It is looking forward to the gold and royalty cheques from the huge mine. The Gediktepe cheques will start coming in the next few days. Caserones is already paying royalty, while Balya is expected to pay in the next few weeks. EMX is transforming from a junior company building a royalty portfolio to a mid-tier company with strong cash flow. As per the company, this is the right time to buy before the market recognizes the portfolio potential.

To find out more, go to the EMX Royalty website

Analyst's Notes

Subscribe to Our Channel

Stay Informed