Escalating Security Negotiations in Eastern DRC Reshape Critical Minerals Supply & Jurisdictional Risk Premiums

DRC conflict disrupts tin & critical minerals supply chains. M23 advances increase jurisdictional risk premiums. Diplomatic frameworks offer long-term hope but limited near-term relief for miners.

- Intensifying conflict in Eastern DRC and fragile ceasefire negotiations have reshaped jurisdictional risk for tin and battery metals supply chains.

- Peace frameworks, the DRC-Rwanda agreement, Doha negotiations, and Regional Economic Integration Framework, signal long-term de-escalation potential but offer limited near-term security relief.

- UN liquidity stress and MONUSCO movement restrictions undermine operational predictability for mining companies in North and South Kivu.

- ESG risk has risen materially as human rights investigations expand, increasing scrutiny from institutional investors with mandatory ESG compliance.

- Exploration companies operating near Tier-1 districts, such as Rome Resources, must demonstrate rigorous risk management to remain investable under shifting geopolitical conditions.

How DRC Geopolitics Became a Critical Variable for Global Tin & Critical Minerals Markets

The Democratic Republic of Congo produces approximately 70% of the world's cobalt, according to 2024 industry data, and ranks among the world's leading suppliers of tin, copper, and tantalum. This concentration of critical minerals in a single jurisdiction means that political volatility in the country's eastern provinces directly affects global supply chains, inventory planning, and pricing mechanisms for metals essential to electrification, semiconductor manufacturing, and defense applications.

The escalation of conflict in North and South Kivu, driven by M23 territorial advances, regional force deployments, and shifting international mediation efforts, has materially increased risk premiums embedded in project valuations. Investors now treat DRC jurisdictional risk as a continuum tied to peace progress, troop movement restrictions, and diplomatic coordination. Discount rates have risen, permitting expectations have been recalibrated, and capital allocation frameworks now incorporate security scenario modeling as a standard analytical input.

For mining companies operating in or near conflict zones, operational continuity depends on factors beyond their direct control: ceasefire durability, UN peacekeeping capacity, regional diplomatic alignment, and community stability. Institutional investors now require visibility into how management teams model these variables, allocate risk capital, and maintain operational flexibility under deteriorating security conditions. The result is a structural repricing of critical minerals assets based on jurisdictional exposure, with lower-risk deposits commanding valuation premiums and high-risk projects requiring material discount rate adjustments.

The Security Deterioration: M23 Advances & the Erosion of Operational Predictability

Recent M23 territorial advances in North and South Kivu have disrupted ground logistics, contractor mobility, and exploration camp access. The expansion of contested territory has created operational unpredictability for mining companies, forcing them to implement contingency protocols that increase costs and delay project timelines.

MONUSCO, the UN peacekeeping force in the DRC, has faced significant movement restrictions imposed by the Congolese government, reducing its capacity to monitor conflict zones and protect civilian infrastructure. These restrictions limit the organization's ability to secure supply routes, conduct reconnaissance, and provide evacuation support, services that mining companies historically relied upon when operating in high-risk regions.

Infrastructure continuity has been compromised by offensive operations. Power lines serving mining districts have been damaged, supply convoys have been delayed or rerouted, and airborne logistics have become more expensive due to elevated insurance premiums and limited airstrip access. Exploration companies must now factor in higher contingency costs for security personnel, alternative transportation routes, and emergency evacuation planning.

Diplomatic Efforts Offer Long-Term Hope but Limited Short-Term Relief

Multiple diplomatic initiatives have been launched to address the DRC security crisis, each offering frameworks for long-term stability but limited immediate relief for operational conditions on the ground.

The DRC–Rwanda Peace Agreement & Regional Security Mechanisms

The DRC-Rwanda peace agreement, signed on June 27 under US auspices in Washington, established the Joint Security Coordination Mechanism to facilitate cross-border military cooperation and intelligence sharing. The agreement includes a Concept of Operations (CONOPS) that outlines phased disarmament protocols and coordinated targeting of armed groups such as the Democratic Forces for the Liberation of Rwanda. The Regional Economic Integration Framework (REIF), initialled on November 7, was introduced to incentivize cross-border trade and create economic interdependencies that support peace dividends.

While these frameworks create the structural conditions for stability, enforcement remains uneven. Joint patrols have been limited by logistical constraints, intelligence sharing has been inconsistent, and disarmament timelines have been repeatedly extended.

Doha Negotiations Between the Congolese Government & M23

The Doha negotiations between the Congolese government and M23, facilitated by Qatar, produced the Doha framework for peace signed on November 15. The agreement outlines a phased approach to ceasefire implementation, political integration, and territorial restitution. Implementation challenges have delayed progress, with verification disputes stalling withdrawal schedules and transitional governance structures lacking operational funding.

For mining companies, peace agreements influence permitting confidence but rarely change ground risk within short time horizons. Companies must continue to operate under conservative security assumptions, even as diplomatic progress unfolds.

Paul Barrett, Chief Executive Officer of Rome Resources, notes external confidence in DRC stability is gradually improving:

"The IR acquisition of Alphamin is showing that the outside world, I went to see the IR guys in Abu Dhabi in December and they said, 'DRC, we're not bought into it yet.' Clearly they are now… I think the US getting involved as well is all positive for DRC minerals, critical minerals."

UN Peacekeeping Constraints & Liquidity Crisis Reshape the Risk Landscape

The United Nations peacekeeping mission in the DRC (MONUSCO) faces structural constraints that have weakened its capacity to provide security and civilian protection in conflict zones. Budget cuts driven by UN liquidity pressures have forced the repatriation of several peacekeeping contingents, reducing operational footprint in North and South Kivu.

Reduced peacekeeping presence has direct implications for mining operations. Road access reinstatement becomes more difficult without UN convoy security, evacuation planning becomes more complex, and insurance premiums increase as underwriters adjust risk models. The liquidity crisis also undermines disarmament, demobilization, and reintegration programs designed to reintegrate former combatants into civilian economies.

ESG Flashpoints Intensify: Human Rights Investigations & Investor Scrutiny

The United Nations Human Rights Council's Independent Commission of Inquiry into human rights conditions in North and South Kivu has intensified ESG scrutiny for companies operating in or near conflict zones. The investigation focuses on civilian displacement, resource-related violence, and exploitation of informal mining networks, issues that directly affect mining companies' social license, financing access, and regulatory compliance.

Institutional investors increasingly rely on ESG scoring frameworks such as MSCI, Sustainalytics, and Principles for Responsible Investment compliance standards when evaluating resource sector allocations. Heightened human rights scrutiny in Eastern DRC has triggered downward ESG score revisions for companies with operational exposure to conflict zones, creating financing constraints and off-take negotiation delays.

Investor expectations have shifted from passive ESG compliance to active risk management. Companies must demonstrate alignment with the UN Voluntary Principles on Security and Human Rights, provide transparent reporting on security partnerships, and implement independent monitoring systems for community impact and human rights safeguards.

The Implications for Critical Minerals Supply: Tin, Copper & Strategic Metals Under Constraint

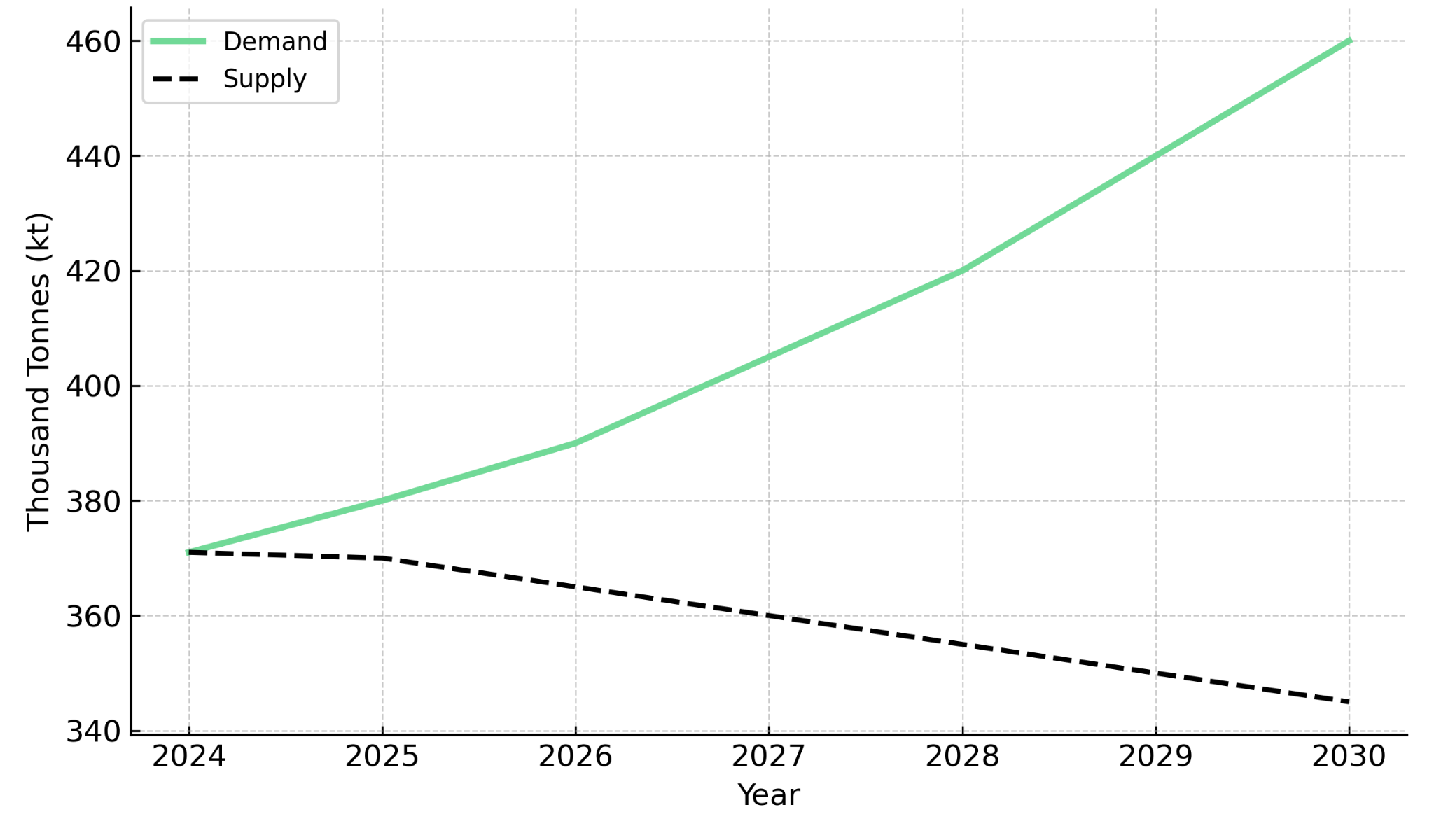

Eastern DRC instability affects global supply-chain resilience for multiple critical minerals, with tin facing particularly acute constraints. Tin is essential for solder in electronics, renewable energy technologies, and semiconductor manufacturing. A 2018 study by the Massachusetts Institute of Technology and Rio Tinto identified tin as the metal most impacted by new technologies due to potential demand growth in electrical and energy storage applications relative to current market size.

The International Tin Association forecasts global demand for tin to increase by up to 40% by 2030 as solar panel production, electric vehicle manufacturing, and AI infrastructure deployment accelerate. Global refined tin production reached 371,200 tonnes in 2024, according to the International Tin Association, representing a decline from 2023 due to supply disruptions in Myanmar and Indonesia.

Instability in Eastern DRC tightens expected supply by reducing output from existing operations, delaying exploration programs, and constraining investment in new capacity. Copper faces similar constraints. The International Energy Agency warns that the copper project pipeline could cover only about 70% of projected 2035 demand, implying a roughly 30% supply shortfall.

For investors, these dynamics require re-evaluation of valuation models for companies with exposure to Eastern DRC geology. Discount rates must be adjusted upward to reflect jurisdictional risk, and risk-adjusted net asset value calculations must incorporate scenario analysis for peace implementation timelines.

Case Example: Exploration Upside Amid Geopolitical Risk

Rome Resources holds exploration assets in the DRC that illustrate how companies navigate security constraints while advancing geological programs. The company's portfolio includes the Mont Agoma and Kalayi prospects, both featuring polymetallic mineralization spanning tin, copper, zinc, and silver.

Asset Quality & Geological Potential

High-grade tin mineralization at Mont Agoma occurs in similar geological settings to Alphamin's Mpama South deposit, a high-grade tin producer in the region. Alphamin, now majority owned by Abu Dhabi-based International Resources Holding, produced 17,324 tonnes of contained tin in 2024, representing about 6% of global mined tin supply. Polymetallic systems offer diversified revenue streams and reduce commodity price volatility risk.

Operational Strategy in a High-Risk Jurisdiction

Rome Resources completed second-phase resource drilling in late 2024, with three drilling units operating on site. Metallurgical testing programs have been initiated to assess concentrate quality, recovery rates, and processing economics, critical inputs for feasibility assessments and potential off-take negotiations.

The company's assets are located approximately 8 kilometers from Alphamin's Mpama South mine site, potentially reducing stranded asset risk by situating the project near established mining infrastructure. Management's long-standing local experience provides operational advantages in navigating community relationships and security coordination. Mark Gasson, Chief Operating Officer, brings 20 years of DRC experience, while Exploration Manager Jamie Anderson has 15 years of DRC experience including 7 years working in tin.

The Investment Thesis for Tin

- Tin offers compelling investment characteristics driven by structural supply deficits, jurisdictional risk premiums, and macro tailwinds from electrification and technology manufacturing.

- Tin supply is expected to tighten and may enter structural deficit as demand grows 20 to 30% by 2030 with limited mine supply, supporting upside for high-grade deposits that could reach commercial production within the next five to seven years.

- Jurisdictional risk premiums embedded in Eastern DRC instability increase global supply tightness and support higher long-term incentive prices, creating favorable pricing environments for deposits in lower-risk jurisdictions and operational resilience premiums for companies that can navigate high-risk environments effectively.

- Tier-1 adjacent exploration opportunities near established producing districts may offer asymmetric upside if security conditions stabilize, permitting timelines compress, and infrastructure access improves through shared facilities and regional development coordination.

- Macro tailwinds from electrification, semiconductor manufacturing, artificial intelligence infrastructure, and solar panel production are all tin-intensive industries experiencing accelerating demand growth that exceeds current supply forecasts.

- Valuation gaps exist for exploration companies with high-grade potential but low market capitalizations, creating opportunities for investors who can assess geological merit, model jurisdictional risk appropriately, and identify derisking events such as mineral resource estimates, metallurgical results, or peace agreement implementation that could trigger valuation rerating.

Why DRC Will Remain a Determining Factor for Critical Mineral Pricing

Eastern DRC remains one of the world's most geologically endowed but geopolitically volatile regions. The concentration of critical minerals in a single jurisdiction creates structural supply constraints that elevate global pricing, increase strategic value for secure supply sources, and generate investment opportunities for companies capable of navigating jurisdictional risk. Peace processes under development, including the DRC-Rwanda agreement, Doha negotiations, and Regional Economic Integration Framework, offer pathways to long-term stability but will require years to structurally alter operational risk. In the interim, instability continues to increase supply tightness and amplify the strategic value of high-grade deposits capable of achieving commercial production despite security challenges.

Sophisticated investors model higher risk premiums in NAV calculations, adjust discount rates to reflect security costs and permitting uncertainty, and require transparency into operational resilience and risk management protocols. Producers and developers with secure supply may attract higher strategic interest from downstream buyers seeking supply-chain diversification away from conflict-affected regions, while exploration companies that demonstrate operational continuity, geological quality, and adaptive risk management can remain investable despite elevated jurisdictional risk. Jurisdictional risk in the DRC is not merely a political story, it is a defining variable shaping the future of tin, copper, and critical minerals pricing globally. Investors who understand this dynamic, model risk appropriately, and identify companies with exceptional asset quality and operational resilience are positioned to capture asymmetric returns as supply constraints intensify and strategic buyers seek secure access to critical mineral supply chains.

TL;DR

Eastern DRC conflict has materially increased jurisdictional risk premiums for critical minerals supply chains, with the region producing approximately 70% of global cobalt and significant tin, copper, and tantalum. M23 territorial advances have disrupted operations while UN peacekeeping constraints and liquidity pressures reduce security capacity. Multiple diplomatic frameworks—including the DRC-Rwanda peace agreement, Doha negotiations, and Regional Economic Integration Framework—signal long-term stability potential but offer limited near-term operational relief. ESG scrutiny has intensified through UN human rights investigations, constraining financing access. Tin faces particularly acute supply constraints with demand projected to grow 20-30% by 2030 amid global production declines. Companies like Rome Resources, which secured £4.2 million strategic investment in December 2024, demonstrate that sophisticated investors view exceptional asset quality and operational resilience as sufficient to justify elevated jurisdictional risk exposure in high-grade tin exploration opportunities adjacent to established producing districts.

FAQs (AI-Generated)

The Democratic Republic of Congo produces approximately 70% of the world's cobalt and ranks among leading global suppliers of tin, copper, and tantalum. This concentration means political volatility in North and South Kivu directly affects supply chains for metals essential to electrification, semiconductor manufacturing, and defense applications. Conflict-driven supply disruptions increase risk premiums embedded in project valuations, elevate global pricing, and force institutional investors to recalibrate discount rates and incorporate security scenario modeling into capital allocation frameworks.

Three major frameworks are in development: the DRC-Rwanda peace agreement signed June 27, 2024, establishing a Joint Security Coordination Mechanism for cross-border military cooperation; the Doha negotiations between the Congolese government and M23, which produced a November 15, 2024 framework for phased ceasefire implementation; and the Regional Economic Integration Framework initialled November 7, 2024, designed to incentivize cross-border trade. While these create structural conditions for long-term stability, enforcement remains uneven and implementation timelines face repeated delays, offering limited near-term operational relief for mining companies.

Tin faces particularly acute constraints as Eastern DRC instability reduces output from existing operations, delays exploration programs, and constrains new capacity investment. Global refined tin production reached 371,200 tonnes in 2024, representing a decline from 2023 due to supply disruptions. The International Tin Association forecasts global demand to increase up to 40% by 2030 driven by solar panel production, electric vehicle manufacturing, and AI infrastructure. This supply-demand imbalance supports higher long-term incentive prices and creates favorable pricing environments for deposits capable of reaching commercial production.

The investment thesis centers on structural supply deficits, jurisdictional risk premiums that support higher long-term pricing, and macro tailwinds from electrification and technology manufacturing. High-grade deposits adjacent to established producing districts may offer asymmetric upside if security conditions stabilize and infrastructure access improves. Valuation gaps exist for exploration companies with exceptional geological potential but low market capitalizations, creating opportunities for investors who can appropriately model jurisdictional risk and identify derisking events such as mineral resource estimates, metallurgical results, or peace agreement implementation that could trigger valuation rerating.

The UN Human Rights Council's Independent Commission of Inquiry into human rights conditions in North and South Kivu has intensified ESG scrutiny for companies operating near conflict zones. Institutional investors increasingly rely on ESG scoring frameworks when evaluating resource sector allocations, and heightened human rights scrutiny has triggered downward ESG score revisions for companies with conflict zone exposure, creating financing constraints and off-take negotiation delays. Investor expectations have shifted from passive compliance to active risk management, requiring companies to demonstrate alignment with UN Voluntary Principles on Security and Human Rights, provide transparent reporting on security partnerships, and implement independent monitoring systems for community impact and human rights safeguards.

Analyst's Notes

Subscribe to Our Channel

Stay Informed