Battery Pack Prices Fall to $108/kWh & the Strategic Repricing of Transition Metals

Battery pack prices hit $108/kWh in 2025, accelerating EV adoption while shifting mining investment toward low-cost, first-quartile assets with jurisdictional advantages.

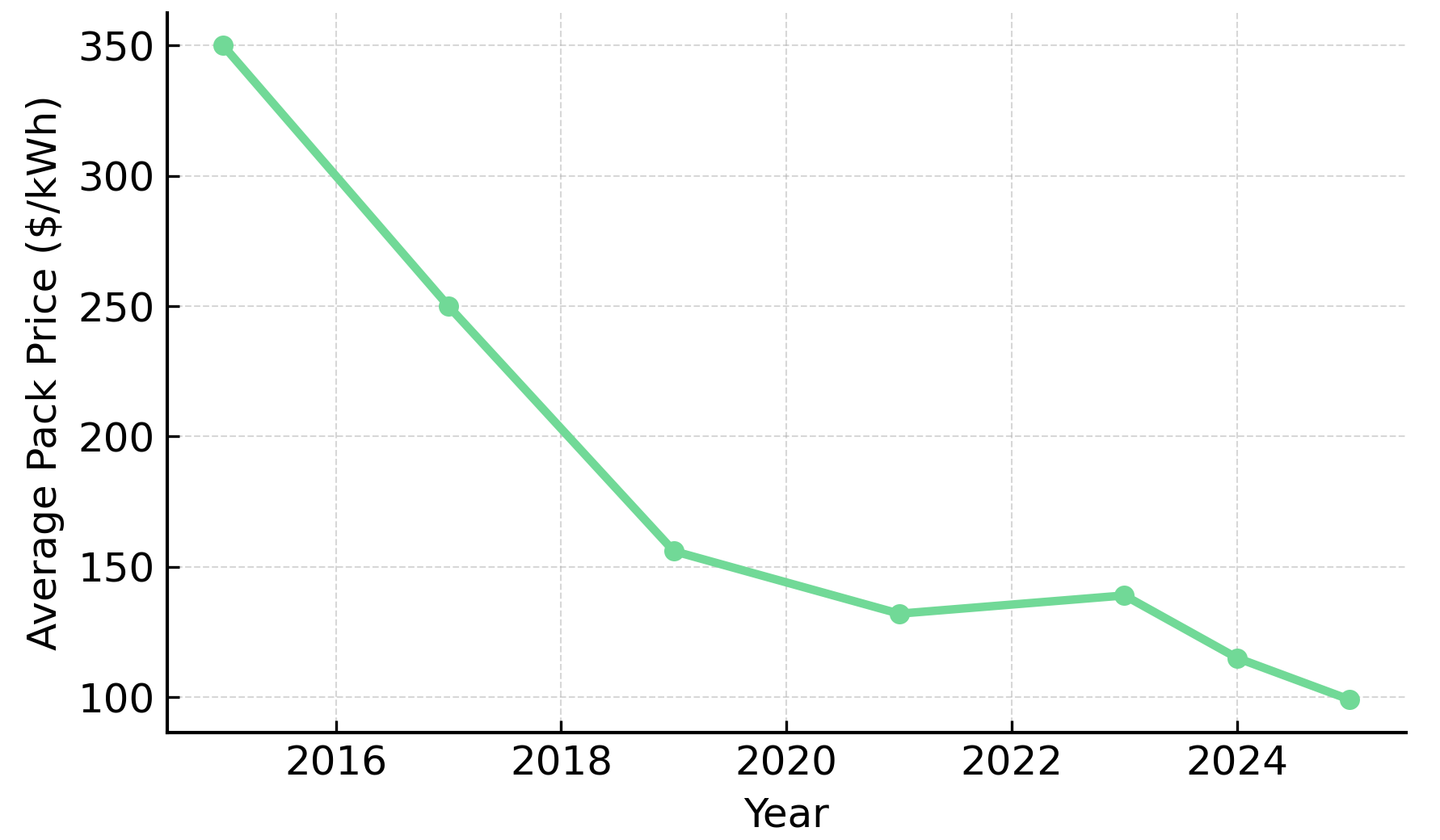

- Lithium-ion battery pack prices fell to $108/kWh in 2025, despite higher underlying metal prices, reinforcing the structural momentum of global electrification rather than signaling demand weakness.

- Cost deflation is being driven by manufacturing overcapacity, chemistry shifts toward LFP, and competitive pressure, pushing adoption thresholds lower across EVs and grid-scale storage.

- Downstream industries are absorbing metal price inflation through chemistry substitution, long-term contracts, and hedging, limiting pricing pass-through to miners.

- This dynamic structurally raises the bar for mining investment, favouring high-grade, low-AISC assets capable of generating margins across price cycles.

- Case studies across nickel, tin, graphite, and rutile illustrate how jurisdiction, cost position, and development stage increasingly determine capital access and valuation resilience.

Battery Cost Deflation Signals Demand Acceleration, Not Weakness

Battery pack prices reaching $108/kWh represent a critical macro inflection point rather than a cyclical anomaly. Historically, sub-$100/kWh pricing has been viewed as the threshold for mass EV adoption; in 2025, BEV packs already averaged $99/kWh, while stationary storage costs fell even faster. This price compression is occurring despite rising prices for key battery metals, underscoring that electrification economics are now being driven by industrial scaling and chemistry evolution, not commodity deflation.

The implications extend beyond automotive markets. Lower system costs accelerate EV penetration, grid-scale storage deployment, and energy infrastructure investment. Electrification demand becomes less sensitive to short-term commodity price volatility, embedding volume growth for transition metals structurally into energy and transport systems. For mining investors, this represents a fundamental shift: the downstream adoption curve has decoupled from metal price cycles, creating sustained demand visibility even as pricing power compresses.

This environment rewards miners capable of delivering volume at competitive costs rather than those positioned solely for price leverage. The margin opportunity increasingly lies in operational efficiency and asset quality, not commodity beta. As battery pack economics continue improving, the structural tailwind for transition metals strengthens, but the operational bar for miners rises correspondingly.

The Chemistry Shift Is Reshaping Metal Demand, Not Reducing It

The widespread shift toward lithium iron phosphate (LFP) batteries has been central to cost deflation. LFP packs averaged $81/kWh, materially below nickel-rich NMC chemistries. For investors, the critical distinction is that chemistry substitution changes the mix of metals, not the existence of demand. LFP reduces reliance on nickel and cobalt per unit but does not eliminate structural growth in copper, tin, graphite, and grid-scale metals. Stationary storage, where energy density is less critical, has become the fastest-growing deployment segment.

This reinforces a bifurcation within battery metals. Bulk, infrastructure-linked metals such as copper, tin, and graphite benefit from electrification volume growth, while higher-cost or geopolitically concentrated metals face pricing volatility and policy risk. The shift does not reduce total metal intensity, it redistributes it. A metric ton of LFP batteries still requires copper for wiring, graphite for anodes, and tin for battery management systems.

The investment implication is clear: portfolios must differentiate between metals exposed to chemistry risk and those serving as foundational inputs across all battery architectures. Copper demand, for instance, remains insensitive to cathode chemistry choices. Similarly, natural graphite demand continues expanding regardless of whether cells use NMC or LFP chemistries, as both require graphite anodes. Investors seeking exposure to electrification fundamentals should prioritize assets serving structural, non-substitutable demand drivers rather than chemistry-specific niches.

Rising Metal Prices Without Pricing Power Raises the Cost Bar for Miners

Despite higher battery metal prices in 2025, cell and pack prices did not rise, indicating downstream absorption of input cost inflation. This has direct implications for mining investment. Margin expansion cannot rely solely on commodity price upside. Projects must compete on AISC, grade, scale, and by-product credits. Capital increasingly flows toward first-quartile cost assets with long reserve lives.

This environment structurally favours large-scale sulphide systems with low unit costs, polymetallic deposits where credits reduce net cash costs, and assets capable of sustaining margins through price cycles. Canada Nickel highlights this dynamic with its Crawford project expected to deliver first-quartile net cash costs and a large reserve base designed to withstand price volatility. The project targets low-cost production from scale and metallurgical simplicity, positioning the asset to generate margins even in depressed pricing environments.

The competitive threshold for new supply has effectively risen. Developers cannot assume favourable pricing environments will persist through multi-year construction timelines. Instead, projects must demonstrate economic resilience at conservative price assumptions.

That execution focus, rooted in cost discipline and scale, reflects the reality that optionality without deliverability no longer commands valuation premiums. In a world where downstream industries control pricing, miners must deliver absolute cost competitiveness, not relative leverage to commodity cycles.

Jurisdictional Risk Is Now Explicitly Priced Into Battery Metals

BloombergNEF explicitly linked DRC cobalt export quotas to higher battery metal prices in 2025, validating that policy and security risks now directly transmit into global pricing. For investors, this reinforces the need to apply jurisdiction-adjusted discount rates to asset valuation, differentiate between geological quality and sovereign risk, and assess operational continuity alongside grade and economics.

Rome Resources operates in Eastern DRC, where tin supply concentration intersects with geopolitical risk. The proximity of Bisie North to an operating, high-grade tin mine underscores geological potential, while policy volatility traditionally elevated execution risk. However, capital market perspectives toward DRC assets have evolved. Paul Barrett, Chief Executive Officer of Rome Resources, notes shifting investor sentiment:

"I went to see the IR guys in Abu Dhabi in December (2024) and they said, DRC, we're not bought into it yet, clearly they are now."

That shift reflects growing recognition that critical mineral scarcity creates tolerance for higher jurisdictional risk, provided operators demonstrate local experience and operational continuity. In contrast, Canada Nickel benefits from permitting transparency and tax incentives within a stable regulatory framework. Mark Selby, Chief Executive Officer of Canada Nickel, highlights the strategic reorientation of Canadian policy:

"The Carney government's been very focused on what we need as Canadians to focus on what we're good at, which is oil and gas and critical minerals."

Lifezone Metals operates under a structured public-private partnership in Tanzania, where the government holds a 16% equity interest in the Kabanga project. Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, describes the partnership dynamic:

"The government is a very good partner with us. They own 16% in the project but they have been an enabler of the project."

These jurisdictional variations underscore that political risk is no longer a tail scenario, it is a pricing factor embedded in valuation multiples, capital access, and offtake negotiations. Investors must assess not just ore grade and economics, but also regulatory predictability, infrastructure availability, and sovereign alignment with Western supply chain priorities.

Low-Cost Projects Are the Structural Winners in a Deflationary Downstream World

As downstream industries capture efficiency gains, mining projects increasingly compete on absolute cost position rather than optionality. Lifezone Metals demonstrates this with Kabanga's projected first-quartile positioning on the global cost curve, based on its July 2025 bankable feasibility study. Hofmaier quantifies the asset's economic positioning:

"Our all-in sustaining costs are $3.36 net of byproduct credit, well below current and relatively low nickel prices."

That cost structure, combined with 4.1% copper-equivalent grade, positions Kabanga to generate margins across commodity cycles. The project's scale and by-product credits create resilience that pure-play nickel assets lack. Hofmaier emphasizes the grade advantage:

"That's 4.1% of copper equivalent grade that's significantly higher than a deposit like Resolution or Kamoa-Kakula."

Sovereign Metals offers a parallel case in graphite, where the mineral functions as a by-product rather than the primary value driver. Ben Stoikovich, Chairman of Sovereign Metals, describes the cost advantage:

"Our incremental cost to produce a ton of graphite as a byproduct from the Kasiya project will only be $241 US per ton."

That cost position is competitive with Chinese supply, providing margin resilience without exposure to downstream processing risk. Stoikovich further highlights the project's unique economics:

"It's the only known deposit where graphite is a byproduct."

This model aligns with the macro reality that miners must deliver resilience, not just leverage. Capital favours assets that work at conservative price assumptions, with margin structures capable of absorbing input cost inflation or pricing pressure. Rome Resources pursues a similar philosophy at Bisie North, where high-grade tin mineralization reduces unit costs and enhances economic robustness. Barrett describes recent drilling results that expand the mineralized footprint:

"What we found with hole 30, which is down on the flank, is a very good shallow tin zone."

The discovery extends mineralization beyond previously mapped soil anomalies, suggesting larger-scale potential. Barrett notes:

"This lies outside the geochemical soil tin anomaly. What we were thinking potentially is that the limit of the mineralization was basically governed by this soil anomaly. Actually, it isn't."

These examples illustrate a common theme: in a deflationary downstream environment, first-quartile cost assets with geological scale command valuation premiums. Projects dependent on elevated metal prices to achieve economic returns face structural headwinds as downstream industries optimize costs and absorb input inflation.

Project Maturity & Execution Visibility Matter More Than Ever

In a macro environment defined by stable electrification demand, volatile metal prices, and heightened jurisdictional scrutiny, investors increasingly prioritise execution visibility. Key differentiators include clear permitting timelines, defined development schedules, and funded pathways to construction or final investment decision (FID).

That coordinated approach reduces permitting risk and accelerates timelines. The Crawford project has been designated a National Priority Project, with the funding package targeting US$2.5 billion including $600 million in investment tax credits.

Lifezone Metals is targeting FID in 2026 with bridge financing completed in September 2025. The company closed a $60 million bridge loan facility to advance development activities. Hofmaier describes the project finance process:

"Through the Mineral Security Partnership we are very well advanced in due diligence exercises with several of them as the DFC is public, Exim Bank is public."

The company has secured an anchor expression of interest from the U.S. Development Finance Corporation (DFC), with U.S. EXIM and multiple Development Finance Institutions actively engaged in the financing process led by Societe Generale.

Sovereign Metals is targeting DFS completion in Q4 2025, backed by Rio Tinto as a 19.9% strategic shareholder. Stoikovich describes the partnership:

"Rio Tinto is a 19.9% shareholder in Sovereign and a strategic partner in the Kasiya project."

Rome Resources is advancing resource definition work following completion of second-phase resource drilling. Barrett outlines upcoming milestones:

"They'll come up with an inferred resource number for the tin, copper and zinc."

These milestones reflect disciplined project sequencing and capital deployment. In a selective funding environment, execution visibility increasingly determines which projects attract capital and which remain stranded at the feasibility stage.

The Investment Thesis for Battery Metals

- Electrification economics are locked in, with battery costs below adoption thresholds regardless of metal price volatility, creating sustained demand visibility for infrastructure-linked metals across chemistry architectures.

- Downstream cost deflation structurally favours low-AISC miners, increasing the valuation premium for first-quartile assets capable of generating margins through commodity cycles rather than relying on price leverage.

- Jurisdictional risk is now a pricing factor embedded in valuation multiples and capital access, raising the importance of political stability, permitting clarity, and alignment with Western supply chain priorities.

- Polymetallic and by-product models offer margin resilience when pricing power is constrained, as credits and diversified revenue streams reduce net cash costs and smooth earnings volatility.

- Advanced developers with clear milestones, funded pathways to construction, and strategic partnerships are best positioned to attract capital in a selective funding environment where execution visibility commands premium valuations.

Cost Deflation Sharpens the Investment Lens

The fall in lithium-ion battery pack prices to $108/kWh is not a signal of weakening fundamentals but a confirmation that electrification has entered a self-reinforcing growth phase. As adoption accelerates, the burden of cost discipline shifts upstream. For mining investors, the implication is clear: quality, cost position, and jurisdiction now matter more than price optionality alone.

The next cycle will reward assets that can generate durable margins across volatile commodity markets, not those dependent on favourable pricing environments. Downstream industries have demonstrated their ability to absorb input cost inflation through efficiency gains, chemistry substitution, and competitive pressure. Miners lacking first-quartile cost structures or jurisdictional advantages will struggle to attract capital, regardless of geological endowment.

TL;DR

Battery pack prices falling to $108/kWh in 2025 signal demand acceleration, not weakness. This cost deflation—driven by manufacturing scale, LFP chemistry adoption, and competitive pressure—locks in electrification economics regardless of metal price volatility. For mining investors, the implications are significant: downstream industries are absorbing metal price inflation, limiting pricing pass-through to miners. This structurally raises the investment bar, favouring high-grade, low-AISC assets capable of generating margins across price cycles. Jurisdictional risk is now explicitly priced into valuations, while polymetallic deposits with by-product credits offer margin resilience. Projects with execution visibility, funded pathways, and strategic partnerships are best positioned to attract capital.

FAQs (AI-Generated)

Cost deflation is driven by manufacturing overcapacity, competitive pressure, and the shift toward cheaper LFP battery chemistries. Downstream industries are absorbing metal price inflation through chemistry substitution, long-term contracts, and hedging rather than passing costs to consumers.

Sub-$100/kWh pricing has historically been viewed as the mass adoption threshold. With BEV packs averaging $99/kWh in 2025, electrification economics are now locked in, making EV penetration and grid-scale storage deployment less sensitive to short-term commodity price volatility.

LFP reduces reliance on nickel and cobalt per unit but doesn't eliminate overall metal demand—it redistributes it. Copper, tin, and graphite remain essential across all battery architectures, benefiting from volume growth regardless of cathode chemistry choices.

First-quartile cost assets with low all-in sustaining costs, high-grade deposits, polymetallic revenue streams, and long reserve lives are structurally favoured. Projects must demonstrate economic resilience at conservative price assumptions rather than relying on commodity price upside.

Policy and security risks now directly transmit into global pricing, as seen with DRC cobalt export quotas. Investors must apply jurisdiction-adjusted discount rates, assessing regulatory predictability, infrastructure availability, and alignment with Western supply chain priorities alongside geological quality.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed