Indonesia's Nickel Supply & The Global Price Slump: What the Market Sell-Off Signals for Investors

Nickel prices hit 4-year lows as Indonesia floods the market. Despite quota cuts, oversupply persists. Western sulphide projects gain strategic value amid EV demand growth.

- Nickel has fallen to $14,550/t, near its four-year low, as Indonesia's refinery buildout floods the market.

- LME inventories surged by 90,000 tonnes in 2025, reinforcing a persistent oversupply and weakening near-term price momentum.

- Market skepticism persists despite Indonesia's planned 120–150Mt quota cuts; investors doubt the reductions will materially tighten supply.

- Structural demand from EV batteries provides long-term support, but muted stainless steel demand continues to weigh on global prices.

- Development-stage Western sulphide projects, such as Canada Nickel's Crawford project in Ontario, offer strategic exposure outside the Indonesia-China supply chain.

Understanding Nickel's Price Breakdown & Why It Matters for Investors

Nickel's decline to $14,532–$14,550 per tonne in November 2025 puts the metal within sight of its four-year low of $13,900, reinforcing a bearish cycle driven almost entirely by supply-side imbalances. Over the past month, nickel has lost 4.57%, and over the past year, it has fallen 8.05%, significantly underperforming copper, zinc, and other base metals.

The intensity of the price drop reflects the sector's chronic oversupply, an environment created not by weakening demand, but by structural overproduction in Indonesia, whose output now exceeds the concentration OPEC held over oil in the 1970s. For institutional investors, this is not just a pricing story; it is a structural risk case study, with implications for capital allocation, jurisdictional exposure, project cost curves, and long-run feasibility of laterite-based supply expansion.

Price malaise extends beyond spot weakness, it reflects deeper structural questions about whether Indonesian supply discipline can realistically materialize, and whether Western sulphide developers can gain meaningful market share in an environment dominated by low-cost laterite production.

Indonesia's Supply Surge: The Primary Driver Behind Nickel's Underperformance

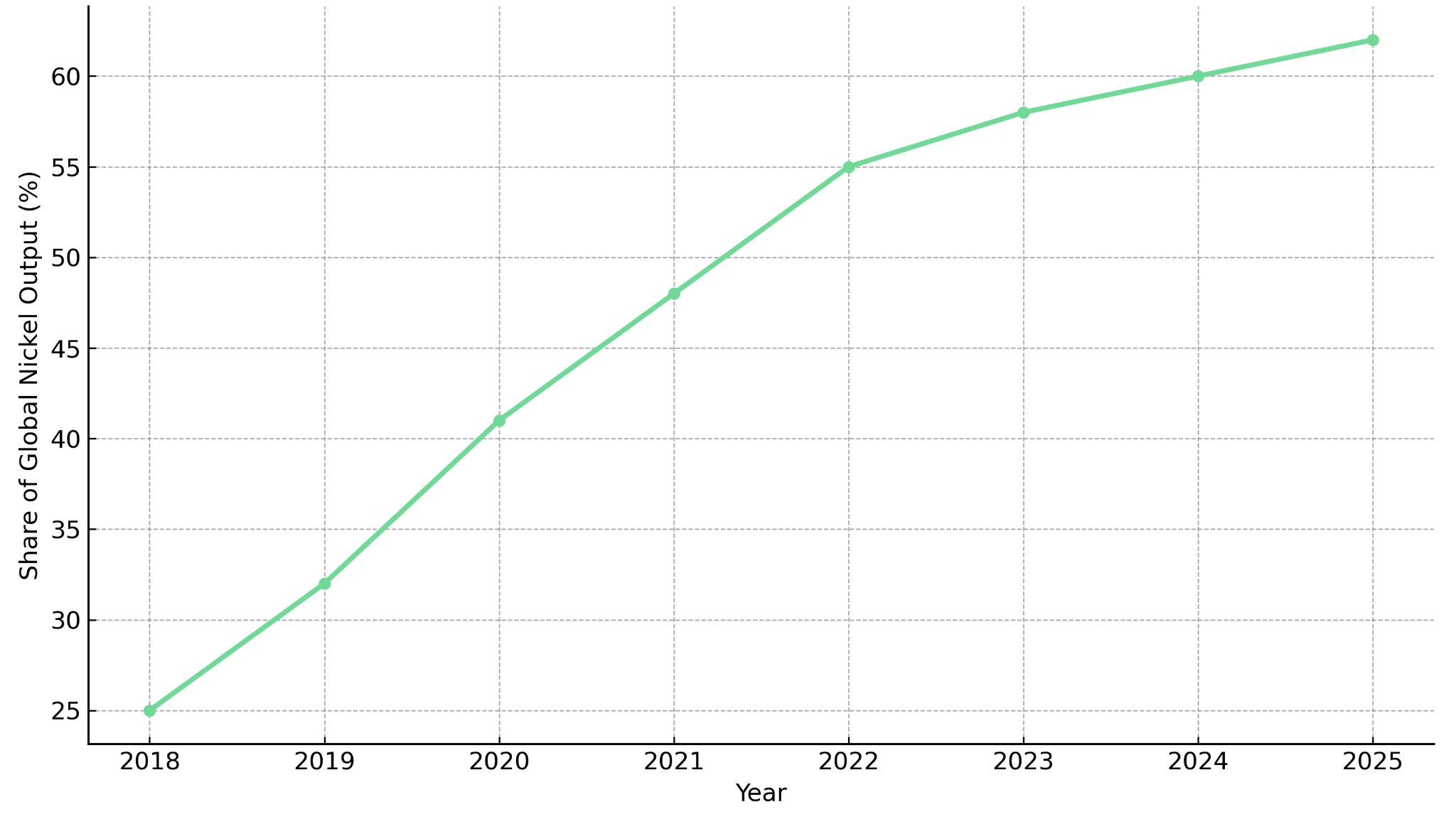

Indonesia remains the uncontested force reshaping global nickel markets. The country's 2020 ban on raw ore exports triggered an unprecedented wave of foreign direct investment, prompting major stainless steel and battery manufacturers to build refining and high-pressure acid leaching (HPAL) capacity domestically. This created a highly scalable, vertically integrated supply chain now responsible for over 60% of global nickel output.

Refinery Expansion & the Scale of the Surplus

LME warehouse inventories rising to over 250,000 tonnes, including a 90,000-tonne increase in 2025, illustrate the speed at which Indonesian nickel pig iron (NPI) and mixed hydroxide precipitate (MHP) production is outpacing global consumption. Even as spot bidding prices weakened, smelters continued ramping output, reinforcing the structural imbalance.

The inventory surge represents not just cyclical destocking, but the result of sustained overbuilding across Indonesian refining infrastructure. Even as spot bidding prices weakened, smelters continued ramping output, reinforcing the structural imbalance and creating a feedback loop that has kept prices suppressed for months.

Market Skepticism Toward Indonesia's Quota Cuts

Indonesia's announced mining quota reduction, cutting 120–150 million tonnes of nickel ore, was interpreted by markets as an acknowledgment of oversupply. However, nickel prices failed to respond meaningfully. Institutional analysts note that the reductions would theoretically reduce global supply by approximately 35%, but past quota cuts did not translate into effective output reduction. Refinery expansions and stockpile drawdowns can offset mining cuts, and integrated producers often maintain production to prevent revenue loss.

This skepticism reinforces the structural nature of the current price slump. Investors evaluating long-term supply must now distinguish between policy announcements and enforceable production declines. Until there is visible evidence of refinery curtailments or permanent capacity closures, the market is unlikely to price in meaningful supply tightening.

Demand Stabilizing but Not Enough to Absorb Excess Supply

Demand trends reveal a market that is firm but insufficient to absorb Indonesia's expansion. Stainless steel, the metal's traditional end market, has faced muted purchasing levels, particularly in Europe and China. This has reduced spot buying activity, with mills destocking rather than increasing procurement.

The weakness in stainless steel has been only partially offset by growth in battery-grade nickel consumption. While electric vehicle production continues to expand globally, the pace of that growth has not yet reached the scale necessary to absorb the tonnage being added by Indonesian laterite operations.

EVs Provide Secular Growth, but Timing Mismatch Persists

The structural story for nickel remains intact: EV batteries continue to drive multi-year demand growth as original equipment manufacturers (OEMs) scale high-nickel cathode production. However, the ramp-up is not fast enough to relieve today's oversupply pressures.

Despite persistent bearish sentiment around EV adoption rates, the data tells a different story. Global EV sales expanded 24% year-to-date through September across China, Europe, and North America, with underlying growth expected to continue at 15-20% annually. Battery chemistry trends favor high-nickel NMC formulations, with nearly all new battery plant additions targeting high-nickel cathode production.

Investors must therefore separate cyclical weakness from secular strength: short-term price softness driven by oversupply, long-term demand anchored by EV and energy storage systems, and inventories expected to remain elevated through 2026. This combination explains why nickel has become bifurcated between near-term bearish sentiment and long-term strategic importance for battery supply chains.

Implications for Cost Curves, Capital Flows & Western Supply Chains

Nickel's price slump has direct implications for cost curves and capital discipline. Many existing laterite projects, particularly HPAL operations, operate at higher all-in sustaining cost (AISC) levels, making them increasingly sensitive to prolonged price weakness. Sustained pricing near $14,500/t could force capital expenditure deferrals, production cutbacks by high-cost operators, and financing challenges for new laterite projects.

The bifurcation in the market is creating a strategic opening for projects with fundamentally different cost structures and jurisdictional profiles. Western sulphide developers, particularly those with large-scale resources and first-quartile cost positioning, are beginning to attract renewed attention from OEMs and governments seeking supply-chain diversification.

Why Western Sulphide Projects Gain Strategic Value

Sulphide projects, known for simpler metallurgy, lower carbon footprints, and lower long-term operating costs, are increasingly viewed as critical to diversifying supply away from Indonesia and China. As geopolitical tensions around critical mineral supply intensify, Western governments have begun to prioritize domestic and allied-nation supply chains.

The strategic imperative extends beyond economics. National security considerations now drive mineral policy in ways that were uncommon a decade ago. Mark Selby, Chief Executive Officer of Canada Nickel, underscored the shift in government policy frameworks:

"Critical minerals are a national security issue."

He elaborated on the G7's coordinated response to supply concentration risks:

"This G7 critical minerals initiative... the realization and the importance is that Germany, France, the other G7 nations are saying look, we want these minerals. We realize they're only going to come from a couple countries so how can we collectively help finance and advance these projects to get the minerals that we need."

The result is an emerging policy framework where Western governments are actively supporting critical minerals development through targeted financing mechanisms and streamlined permitting processes. For investors, this represents a fundamental shift in how Western sulphide projects should be valued relative to Indonesian laterite operations.

Case Study: Canada Nickel & the Reshaping of Western Nickel Supply

Canada Nickel's Crawford project represents a case study in how Western sulphide assets are being repositioned within a supply landscape dominated by Indonesian laterite production. The company is advancing the Crawford Nickel Sulphide Project toward construction in Ontario's Timmins region, where it has consolidated over 20 ultramafic targets encompassing 42 square kilometers of geophysical footprint.

How Crawford Fits into the Structural Supply Gap

The six published resources in the Timmins Nickel District contain 9.2 million tonnes of measured and indicated nickel and 9.5 million tonnes of inferred nickel, more contained nickel than the Sudbury Basin. According to Wood Mackenzie and company filings, Crawford contains the world's second-largest nickel reserve by contained metal in the proven and probable category, based on the October 2023 Bankable Feasibility Study.

The project's scale is significant not just in absolute terms, but relative to the limited pipeline of new Class-1 nickel projects outside Indonesia. With few large-scale sulphide developments advancing globally, Crawford represents one of the few near-term opportunities to materially shift the geographic distribution of battery-grade nickel supply.

Cost Structure & Decarbonization as Strategic Differentiators

Global OEMs and battery manufacturers are increasingly prioritizing low-carbon supply chains. The October 2023 Bankable Feasibility Study projects life-of-mine average net C1 cash costs of US$0.39/lb, positioning Crawford in the first quartile of the global cost curve. The 41-year mine life, based on metal price assumptions of $15,650/t nickel, provides long-term supply visibility.

Crawford's potential to achieve zero-carbon or net-negative emissions, through carbon sequestration systems targeting storage of up to 1.5 million tonnes of carbon dioxide per year from carbonation testwork, with potential expansion to 10-15 million tonnes annually through the NetCarb Alliance process, aligns with Western industrial policy and automaker procurement trends. The project incorporates three separate pathways for carbon sequestration, utilizing tailings directly from the mineral processing circuit.

Financing, Permitting & Market Visibility

Canada Nickel has secured a Letter of Interest from Export Development Canada (EDC) to serve as Mandated Lead Arranger for a US$500 million debt facility. The company also maintains strategic shareholder support from Agnico Eagle (10.0%), Samsung SDI (7.2%), Taykwa Tagamou Nation (7.1% on conversion), and Anglo American (6.3%), as of October 30, 2025.

The company is targeting receipt of federal permits and full financing package in 2026, construction start by year-end 2026, and first production by year-end 2028. The Environmental Impact Statement was filed in November 2024, and the project has been referred to the Major Projects Office by the Government of Canada. Major support infrastructure including roads, power, water, and rail connection is in place.

North American demand alone presents a compelling regional opportunity. The read-through for North American nickel demand from EV production growth represents approximately 300,000-400,000 tonnes of nickel for high-nickel batteries as domestic battery manufacturing scales.

Key Risks Investors Must Monitor in a Depressed Price Environment

Despite the long-term strategic case for nickel, near-term risks remain substantial. Investors must weigh project-level fundamentals against a macro backdrop that continues to favor supply over demand.

Prolonged Oversupply & Price Volatility

If Indonesian production does not slow meaningfully, nickel could remain depressed into 2026–2027, affecting capital costs, valuation multiples, and project timelines. The risk is not hypothetical: refinery capacity continues to expand, and integrated producers have demonstrated willingness to operate through weak pricing environments to preserve market share.

HPAL Cost Inflation & Operating Risk

Laterite processing remains technically complex. Although Indonesia has reduced unit costs through scale, HPAL operations globally face risks in acid consumption, waste handling, ramp-up delays, and tailings management. These operational challenges create downside risk to cost assumptions and production ramp schedules.

Permitting Windows & Political Cycles in the West

For Western developers, regulatory windows and shifting political priorities may extend timelines. Ontario and federal Canada have established programs supporting critical minerals development, but investors must monitor changes in clean-energy incentive structures, permitting queue congestion, and environmental consultation timelines. Regulatory risk in Western jurisdictions is often underestimated relative to operational risk in emerging markets.

The Investment Thesis for Nickel

Nickel's investment case sits at the intersection of structural demand growth and cyclical pricing distress. The following points summarize the core investor takeaways:

- Oversupply is the dominant near-term risk, but also sets the stage for future supply discipline as high-cost operators struggle at sub-$15,000/t pricing.

- EV-driven Class-1 nickel demand remains structurally positive, with long-term deficits expected once Indonesian growth moderates and battery production scales across North America and Europe.

- Western sulphide projects offer strategic scarcity value, particularly those with low-cost profiles and strong environmental, social, and governance credentials aligned with OEM procurement requirements.

- Canada Nickel's Crawford project demonstrates long-term supply-chain diversification potential, offering first-quartile cost positioning and carbon sequestration capabilities outside the Indonesia-China supply chain.

- Policy incentives and government financing support in Canada position Western nickel developers to capture future market share once the current oversupply cycle normalizes.

- Capital will increasingly flow toward projects that can compete on cost, carbon intensity, and jurisdictional predictability as OEMs and governments prioritize supply-chain resilience over lowest-cost sourcing.

Nickel's Sell-Off Signals a New Phase of Strategic Differentiation

Nickel's price weakness is not merely a cyclical downturn, it reflects an industry reshaped by Indonesia's unprecedented supply expansion. For investors, the divergence between depressed prices today and structurally rising demand over the next decade creates an inflection point. Capital will increasingly flow toward projects that can compete on cost, carbon intensity, and jurisdictional predictability.

While the market may remain oversupplied in the near term, nickel's role in energy systems, electrification, and industrial decarbonization ensures its long-term relevance. Companies positioned outside Indonesia, particularly sulphide developers with scalable resources and environmental, social, and governance alignment, will be central to the next phase of global supply-chain diversification. For patient investors, this macro environment offers both caution and opportunity.

TL;DR

Nickel has plunged to $14,550/tonne, approaching four-year lows, as Indonesia's refinery expansion creates massive oversupply despite announced quota cuts. LME inventories surged 90,000 tonnes in 2025, with markets skeptical that production will actually decline. While stainless steel demand remains weak, EV battery growth provides long-term support—though not enough to absorb current excess supply. This creates a bifurcated market: near-term bearish pricing versus long-term strategic importance. Western sulphide projects like Canada Nickel's Crawford are gaining attention as governments prioritize supply-chain diversification away from Indonesia-China dominance. First-quartile cost structures and carbon sequestration capabilities position these projects as strategic alternatives, though oversupply may persist through 2026-2027.

FAQs (AI-Generated)

The primary driver is Indonesia's massive refinery buildout, which now controls over 60% of global nickel output. Following a 2020 ban on raw ore exports, Indonesia triggered unprecedented foreign investment in refining capacity. LME inventories surged by 90,000 tonnes in 2025, and despite Indonesia announcing quota cuts of 120-150 million tonnes, markets remain skeptical these will translate to actual production reductions. Refinery expansions and stockpile drawdowns can offset mining cuts, keeping prices suppressed near $14,550/tonne.

Market skepticism is high. While the quota reductions would theoretically reduce global supply by approximately 35%, past quota announcements haven't resulted in effective output reductions. Integrated producers often maintain production to prevent revenue loss, and refinery expansions can offset mining cuts. Until there's visible evidence of refinery curtailments or permanent capacity closures, the market is unlikely to price in meaningful supply tightening.

Despite near-term oversupply, structural demand from EV batteries provides strong long-term support. Global EV sales expanded 24% year-to-date through September 2025, with underlying growth expected at 15-20% annually. Battery chemistry trends favor high-nickel NMC formulations, with nearly all new battery plant additions targeting high-nickel cathode production. However, this growth isn't fast enough to absorb current Indonesian output, creating a timing mismatch between supply expansion and demand growth.

Western sulphide projects offer strategic diversification away from Indonesia-China supply chain dominance. They typically have simpler metallurgy, lower carbon footprints, and lower long-term operating costs than laterite operations. Geopolitical concerns and national security considerations are driving G7 governments to support domestic critical mineral development through financing mechanisms and streamlined permitting. Projects like Canada Nickel's Crawford offer first-quartile cost positioning (US$0.39/lb net C1 cash costs) and carbon sequestration capabilities that align with OEM procurement requirements

The timeline remains uncertain. If Indonesian production doesn't slow meaningfully, nickel could remain depressed into 2026-2027. Recovery depends on several factors: high-cost operators curtailing production at sustained sub-$15,000/tonne pricing, EV battery production scaling sufficiently to absorb excess supply, and potential enforcement of production discipline. Long-term deficits are expected once Indonesian growth moderates and battery manufacturing scales across North America and Europe, but near-term oversupply is the dominant risk investors must navigate.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed