Tin Market Rebounds on Tightening Supply & AI-Led Demand Signals

Tin prices stabilize as AI demand and tight supply reshape the market. Exploration firms like Rome Resources gain strategic value amid critical mineral scarcity.

- Tin prices edged up to 291,890 yuan/mt (+0.68%), stabilizing above the 290,000 threshold as tightening ore supply in Yunnan supports near-term price resilience.

- Weakness in traditional electronics demand is being offset by structural growth in AI computing, semiconductor build-outs, and photovoltaic installations, setting the stage for a multi-year demand runway.

- Geopolitical catalysts, including US approval of high-volume AI chip exports to Saudi Arabia and Europe's investment in exascale computing, reinforce tin's role in the global technology arms race.

- Tight supply, fragile smelter margins, and rising geopolitical risk in Myanmar and Indonesia increase the scarcity premium for high-grade tin developers, especially those with by-product copper and zinc exposure.

- Exploration-stage companies such as Rome Resources (tin-copper-zinc, DRC) demonstrate how aligned assets can benefit from macro tailwinds, particularly as the industry faces a shortage of new, high-grade discoveries.

Tin's Price Stabilization Reflects a Market Searching for Direction

The tin market opened the week with the SHFE SN2512 contract closing at 291,890 yuan/mt, a modest 0.68% increase, stabilizing just above the psychologically important 290,000 level. While the move is incremental, it signals growing conviction that the market has likely found a short-term floor amid tightening ore supply and fragile downstream consumption.

Spot trading remains subdued, 10 to 20 mt volumes and cautious procurement behavior, but price weakness has attracted opportunistic buying from specific end-users. The resilience suggests the market is now transitioning from cyclical weakness toward structural tightening, with supply fundamentals offering the strongest near-term support.

The price action reflects broader uncertainty in global metals markets, where monetary policy headwinds intersect with long-term supply constraints. For tin specifically, the ability to hold above 290,000 yuan/mt indicates that buyers recognize the limited availability of high-grade ore and the persistent risk of supply disruptions across key producing regions.

Structural Supply Tightening Across Key Tin Producing Regions

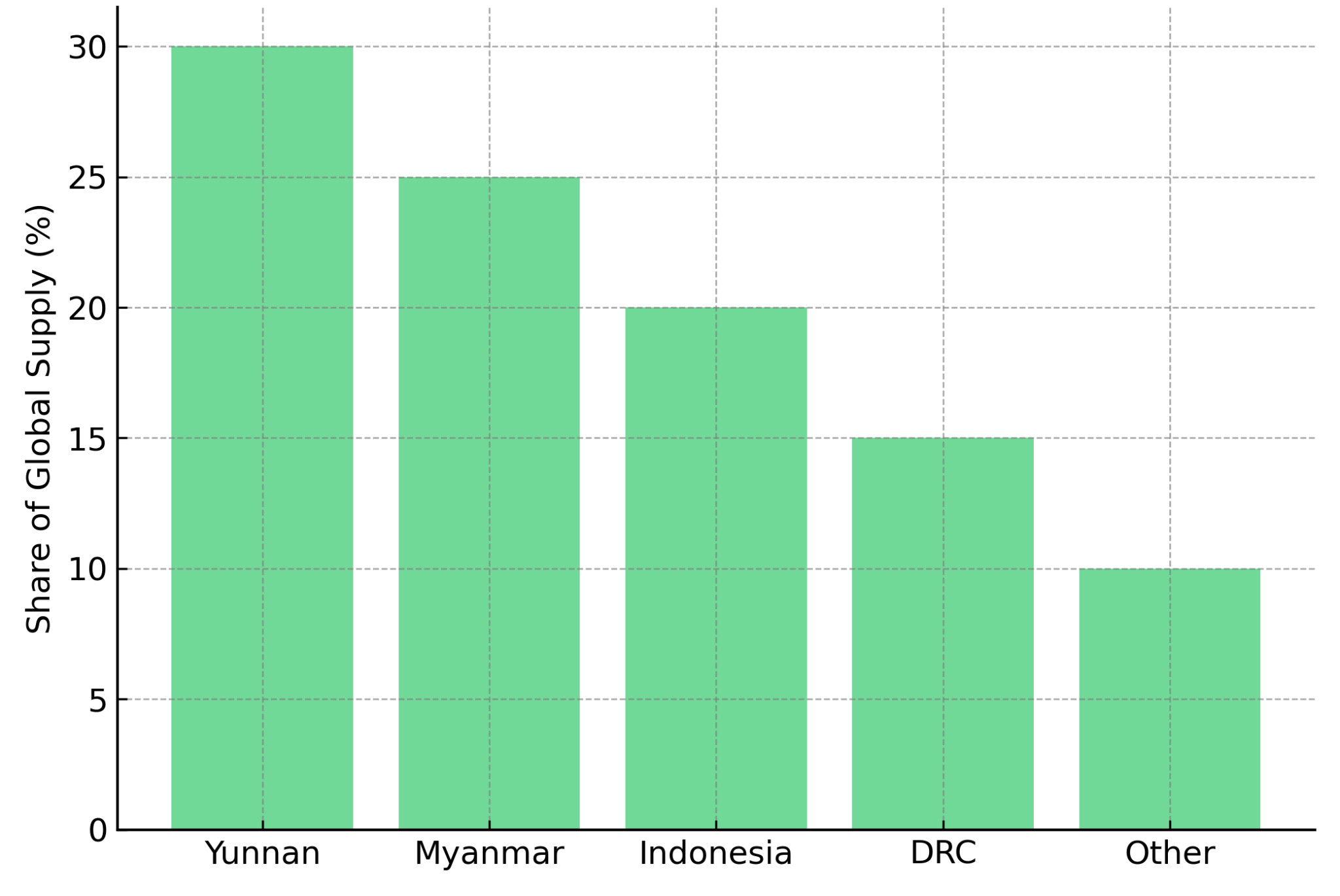

Tin ore supply across major producing regions, including Yunnan, continues to tighten. Most smelters are expected to maintain stable production through November, but ore availability remains a critical constraint. This comes as global supply remains vulnerable to disruptions from Myanmar's political instability and Indonesia's tightening export controls.

High prices have suppressed consumption, but they also reflect the lack of incremental supply. The tin industry has experienced underinvestment in exploration and development, with few new high-grade deposits emerging over the last decade. This scarcity underpins the metal's strategic importance as a critical input for global electronics and advanced computing.

The supply tightness has created a fundamental shift in how market participants value tin exposure. With limited pipeline projects capable of delivering meaningful production within the next five years, exploration-stage assets with credible geological signatures have attracted increased attention from strategic investors seeking long-term exposure to technology-critical metals.

The Scarcity Premium and Strategic Value of High-Grade Assets

Tightening supply enhances the scarcity value of projects with high-grade signatures or polymetallic support. This dynamic is reflected in exploration-stage companies such as Rome Resources, whose Bisie North Project sits only 8 km from Alphamin, the world's highest-grade tin mine.

Recent drilling has revealed new opportunities for resource expansion, particularly on the northeastern flank of Mont Agoma. Paul Barrett, Chief Executive Officer of Rome Resources, described the implications of the findings:

"What we found with hole 30 which is down on the flank is a very good shallow tin zone… This lies outside the geochemical soil tin anomaly so what we were thinking potentially that the limit of the mineralization was basically governed by this soil anomaly actually it isn't. The tin that we found is outside the tin anomaly so we think there's a lot of scope now for the northeast flank of Mont Agoma."

The discovery carries significant implications for resource potential, as it suggests the mineral system extends well beyond the initial target area. For investors evaluating early-stage tin assets, the ability to expand the geological footprint without proportional increases in capital intensity represents a critical valuation differentiator.

Weakness in Legacy Demand, Electronics & Appliances, But Emerging Sectors Begin to Lead

Demand from traditional tin consumers such as consumer electronics and home appliances has weakened sharply. Orders have declined significantly throughout Q4, and downstream procurement remains cautious. High tin prices further suppress actual consumption, preventing a broad-based demand recovery.

However, structural demand is now shifting from these legacy sectors toward high-growth industries with long-term visibility: AI computing infrastructure (soldering for GPUs, advanced circuitry), photovoltaic solar installations, and industrial automation and electric vehicle technologies. These emerging sectors are still not large enough to offset traditional sectors in the near term, but they represent the strongest demand growth trajectory for tin over the next decade.

The bifurcation in tin demand creates a challenging environment for short-term price forecasting but strengthens the long-term investment thesis. While consumer electronics face headwinds from slowing global smartphone and PC shipments, the exponential growth in data center construction and renewable energy deployment provides a durable demand foundation that is less sensitive to cyclical downturns.

The Technology Supercycle and Tin's Role in Advanced Manufacturing

Tin's core application, soldering, makes it indispensable for semiconductors, printed circuit boards, renewable energy components, and exascale computing hardware. The metal is therefore directly tied to the structural growth of artificial intelligence, data center expansion, and green electrification.

Rome Resources' exposure to tin-copper-zinc polymetallic systems positions the exploration-stage company within these macro growth vectors, offering investors a diversified entry point into multiple technology-linked metals. The company's geological model indicates that shear zones control mineralization, with fluid movement depositing tin, copper, and zinc in sequence, a structural framework that supports grade continuity and expansion potential.

Barrett explained the geological controls that underpin the project's development strategy:

"It's really shear zones are the controlling factor… You've had movement throughout geological time and that's brought in the zinc, the copper, the tin, or in reverse order the tin, the copper, and the zinc. It's a zone of weakness that basically has been exploited by the mineral-bearing fluids."

Understanding these structural controls is essential for resource definition and mine planning. For investors, the presence of a well-defined geological model reduces exploration risk and supports more predictable resource growth as drilling progresses.

Geopolitics & the AI Supply Chain Are Rewriting the Tin Demand Outlook

The most significant macro driver for tin demand now sits outside traditional hardware sectors: the geopolitical arms race in artificial intelligence and high-performance computing. Two major developments highlight this shift.

The United States intends to approve the first batch of advanced AI chip exports to Saudi Arabia's Humain, with export volumes expected to reach tens of thousands of semiconductors. Companies such as Nvidia and AMD stand to benefit as Middle Eastern markets expand their high-performance computing capacity. This marks a strategic shift in US technology export policy, driven by the recognition that allied nations require access to advanced computing infrastructure to remain competitive in AI development.

Europe's exascale computing strategy received a major catalyst with a €554 million contract awarded to Eviden (Atos) and AMD to build the Alice Recoque supercomputer. Construction is slated to begin before end-2026, signaling Europe's commitment to accelerating semiconductor and high-performance computing capabilities in response to US and Chinese dominance in the sector.

Both initiatives require massive volumes of tin, given its role in solder and electronic interconnects. As the AI build-out accelerates, tin demand becomes increasingly tied to global geopolitics, specifically, the competition for semiconductor dominance. This creates a fundamental shift in how tin is valued: no longer simply a cyclical industrial metal, but a strategic input for national security and technological sovereignty.

Where Exploration-Stage Companies Fit Into This Global Realignment

Exploration-stage companies such as Rome Resources are increasingly relevant as major economies look to secure stable and diversified supplies of tin. With the International Tin Association forecasting up to 40% demand growth by 2030, new discoveries will be essential to meet the requirements of semiconductor manufacturing, data center construction, and renewable energy deployment.

Rome's Kalayi prospect, featuring high-grade plunging tin shoots comparable to Alphamin's Mpama South (2% tin), illustrates the scarcity and strategic relevance of early-stage tin assets. The company has engaged MSA Group to prepare an inferred resource estimate that will separately report tin, copper, and zinc across its Mont Agoma and Kalayi prospects, providing clarity on the scale and distribution of mineralization.

The decision to report tin, copper, and zinc separately rather than using metal equivalents reflects a commitment to transparency and avoids the misleading valuations that can result from aggregating commodities with vastly different price points. For institutional investors evaluating polymetallic assets, this approach provides clearer visibility into the economic contribution of each metal.

Monetary Policy Uncertainty Adds Complexity but Does Not Alter Structural Tin Demand

The US Federal Reserve has signaled that a December rate cut is "not a done deal," highlighting risks to inflation and employment. Higher-for-longer rates typically pressure metals due to a stronger US dollar and tighter financial conditions, which reduce speculative demand and constrain financing availability for mining projects.

However, tin's structural demand drivers, semiconductor production, AI adoption, photovoltaic growth, remain long-term, capital expenditure-led themes that extend well beyond short-term monetary volatility. Investors must therefore consider both cyclical headwinds and structural tailwinds when evaluating tin exposure.

The divergence between short-term price action and long-term fundamentals creates opportunities for investors with appropriate time horizons. While near-term volatility may persist as markets adjust to evolving monetary policy expectations, the multi-year demand trajectory for tin remains firmly anchored to the growth of advanced technologies that are insensitive to interest rate fluctuations.

How Tin Developers Align With Macroeconomic Tailwinds

Tin's scarcity and critical importance to advanced technologies create a favorable environment for exploration companies with credible geological signatures and catalyst pipelines. Rome Resources provides a representative case study of how early-stage assets can align with macro themes while maintaining operational discipline.

Financial Health and Strategic Positioning

Rome Resources raised £8.2 million through its reverse takeover, with £4.2 million from a strategic investor. The allocation of approximately 49% to project spend indicates strong capital discipline, a critical factor for early exploration companies without revenue. The strategic investor's participation reflects confidence in the project's geological potential and the jurisdiction's stability.

Rome's polymetallic value distribution, weighted toward zinc, copper, and tin in relative value terms, creates an attractive hedge against price volatility. The presence of three metals with distinct end-use applications reduces exposure to any single commodity cycle, while maintaining alignment with long-term electrification and technology trends.

The Democratic Republic of Congo has historically faced investor skepticism due to governance challenges and regional security concerns. However, recent developments, including Alphamin's successful production ramp and its acquisition by International Resources Holding, have demonstrated that well-managed projects can deliver returns in the jurisdiction.

Barrett addressed the jurisdictional considerations and recent positive developments:

"I think the M23 situation has almost in a way entrenched back into Agoma... We had the strategic investor come in in December, obviously liked the project… The US is getting involved as well, and it's all positive actually for DRC critical minerals."

The involvement of sovereign wealth funds and US government interest in critical minerals from the Democratic Republic of Congo represents a fundamental shift in how Western capital views African mining jurisdictions. For early-stage projects with proximity to producing assets, this creates a more favorable financing environment and de-risks permitting and infrastructure development.

Project Milestones and Operational Visibility

Key near-term catalysts for Rome include a maiden resource estimate targeted for June 2025, ongoing follow-up drilling continuing through July 2025, and a 1,000 kg metallurgical sample currently undergoing processing in Canada. These provide strong newsflow visibility, an important consideration for investors benchmarking enterprise value per resource potential or assessing pre-resource exploration risk.

The metallurgical sample is particularly significant, as it will inform processing route selection and recovery estimates for the three target metals. Given the polymetallic nature of the deposit, metallurgical complexity represents a key technical risk that must be addressed before advancing to preliminary economic assessments.

The Investment Thesis for Tin

- Tightening global supply across Yunnan, Indonesia, and Myanmar provides support for tin prices and increases scarcity value for new discoveries, particularly those with high-grade signatures and polymetallic diversification.

- AI compute acceleration, photovoltaic installations, and supercomputing build-outs form long-term structural demand drivers beyond traditional electronics cycles, reducing sensitivity to consumer discretionary spending.

- Geopolitical competition in semiconductors deepens tin's strategic importance, particularly for Western economies seeking non-China-dependent supply chains with diversified sourcing from stable jurisdictions.

- High-grade, polymetallic exploration assets, such as Rome Resources, offer asymmetric upside as part of long-term critical minerals exposure, with reduced single-commodity risk from copper and zinc co-products.

- Limited global project pipeline increases the strategic valuation of credible early-stage tin and polymetallic developers, especially those with proximity to producing mines that validate geological models and infrastructure access.

- Tin's role as an essential input in solder ensures that demand remains correlated with the fastest-growing segments of the global economy: artificial intelligence, cloud computing, and renewable energy infrastructure.

Tin's Repricing Is a Preview of Structural Change

Tin's movement back above the 290,000 yuan/mt level is more than a technical rebound. It reflects the early stages of a fundamental shift in how global markets value technology-critical metals. As traditional demand weakens, structural demand from artificial intelligence, photovoltaics, semiconductors, and high-performance computing infrastructure signals a new era of consumption.

Investors should recognize that supply-side fragility, tight ore availability, limited new discoveries, geopolitical instability, intersects directly with this demand uplift. Exploration-stage companies aligned with these trends, particularly those delivering high-grade, scalable mineral systems with polymetallic optionality, stand to capture meaningful long-term interest.

As the world accelerates toward a more digitized and electrified economy, tin's strategic importance will deepen, and investors positioned early in this transition will be best placed to benefit from the repricing of critical technology metals.

TL;DR

Tin prices have stabilized above 290,000 yuan/mt as tightening ore supply from Yunnan and geopolitical risks in Myanmar and Indonesia create a scarcity premium. While traditional electronics demand weakens, structural growth from AI computing, semiconductors, and photovoltaic installations is driving long-term consumption. Major geopolitical developments—including US AI chip exports to Saudi Arabia and Europe's €554M supercomputer investment—underscore tin's strategic importance. The limited global project pipeline increases the value of high-grade exploration assets like Rome Resources' Bisie North Project in DRC, which offers polymetallic exposure to tin, copper, and zinc. Supply-side fragility combined with technology-driven demand positions tin as a critical metal for the digital economy transition.

FAQs (AI-Generated)

Tin prices are stabilizing due to tightening ore supply from key producing regions like Yunnan, Myanmar, and Indonesia, combined with emerging structural demand from AI computing infrastructure, data centers, semiconductors, and photovoltaic solar installations. While traditional electronics demand has weakened, these new technology sectors provide a durable long-term demand foundation that offsets cyclical downturn

AI drives tin demand through massive data center and high-performance computing infrastructure build-outs. Tin is essential for soldering in GPUs, advanced circuitry, and semiconductor manufacturing. Recent developments like US approval of AI chip exports to Saudi Arabia and Europe's €554M exascale supercomputer project signal exponential growth in tin-intensive computing hardware over the coming decade.

Rome Resources' Bisie North Project is located 8 km from Alphamin, the world's highest-grade tin mine, in the Democratic Republic of Congo. Recent drilling has revealed expansion potential beyond initial targets, with polymetallic exposure to tin, copper, and zinc. This diversification reduces single-commodity risk while aligning with technology and electrification trends. The company targets a maiden resource estimate in June 2025.

The tin market faces chronic underinvestment in exploration, with few new high-grade deposits discovered in the last decade. Key supply risks include political instability in Myanmar, tightening export controls in Indonesia, ore scarcity in Yunnan, and fragile smelter margins. This limited project pipeline increases the scarcity premium for existing high-grade discoveries and exploration-stage assets.

Yes. Tin's role in semiconductor manufacturing, AI infrastructure, and advanced computing has elevated it from a cyclical industrial metal to a strategic input for technological sovereignty. The geopolitical competition between the US, China, and Europe for semiconductor dominance makes tin essential for national security, driving Western governments to seek diversified, non-China-dependent supply chains for critical minerals.

Analyst's Notes

Subscribe to Our Channel

Stay Informed