Kodiak Copper Approaches Critical Resource Milestone with Strong M&A Potential

Kodiak Copper nears maiden resource (Q4 2025) for 300M+ ton copper-gold porphyry. High-grade zones, M&A target potential, trading at 5-6x discount to peers.

- Kodiak Copper is releasing its first comprehensive resource estimate in Q4 2025, comprising seven mineralised zones with the first four zones showing ~300 million tons at 0.42% copper equivalent (indicated) and 0.33% (inferred)

- The company has consolidated a mining district in southern British Columbia over six years, completing 90,000 meters of drilling with significant potential for resource expansion across multiple open zones

- Management expects major mining companies to show increased interest following the maiden resource release, as this typically triggers acquisition activity in the copper porphyry space

- Recent drilling has identified high-grade copper zones near surface, including 27 meters at 1.62% copper, which could serve as potential starter pits for future mining operations

- Beyond the flagship MPD project, Kodiak owns the undeveloped Mohave copper-molybdenum project in Arizona's established porphyry district, providing additional optionality

Kodiak Copper Corp, led by President and CEO Claudia Tornquist and Chairman Chris Taylor, represents a interesting proposition in the copper-gold porphyry exploration space. The company has systematically built a district-scale position in southern British Columbia's established mining region, consolidating properties and conducting extensive drilling programs over the past six years. With copper prices remaining elevated and institutional interest returning to the mining sector, Kodiak is positioned to capitalise on the growing demand for critical minerals.

The company's approach reflects a disciplined strategy of district consolidation followed by systematic resource delineation. As Tornquist explained,

"We have a property that has significant historic drilling that we consolidated, put together in the district and we have now drilled 90,000 meters over the last six years."

This extensive drilling campaign has been designed to demonstrate the potential for a major porphyry mine, setting the stage for the upcoming maiden resource estimate.

Maiden Resource Estimate as Critical Inflection Point

The release of Kodiak's maiden resource estimate represents the most significant catalyst in the company's development trajectory. The first phase, released in June 2025, delivered approximately 300 million tons at grades of 0.42% copper equivalent for indicated resources and 0.33% for inferred resources across four of seven identified mineralised zones. This initial resource announcement generated positive market response, with the company experiencing a notable share price increase.

The completion of the full maiden resource, expected in Q4 2025, will incorporate the remaining three zones that were drilled during the summer exploration program. Early results from these zones have already been well-received by the market, suggesting the final resource could demonstrate the project's potential to rank among comparable advanced development projects. Tornquist noted the significance of this milestone:

"The maiden resource is a start not an end. All these zones are open in multiple directions and we know already that we will do more drilling and there's a lot of potential to grow the resource substantially."

Grade Quality with Economic Potential

The grade profile of Kodiak's MPD project positions it competitively within the porphyry copper sector, particularly given the near-surface, high-grade zones that could serve as potential starter pits. Recent drilling results have highlighted the project's economic potential, with Taylor emphasising recent success:

"We just put out a hole from the Adit zone which was like about 70 or 80 meters of 0.7% copper equivalent, and the bottom part of it was 1.62% copper over 27 meters at the end of the hole."

These high-grade intersections near the surface are particularly valuable for project economics, as they could provide early cash flow generation to support broader mine development. The presence of both copper and gold mineralization adds another dimension to the project's value proposition, especially with gold prices reaching new highs. Taylor highlighted this dynamic:

"We've seen that about 25% of the value of the project comes from gold. But if you look at the resource reporting that we did, that was at $2,600 an ounce. So we're sitting at $3,600 an ounce currently."

Interview with Claudia Tornquist, CEO & Chris Taylor, Chairman of Kodiak Copper

Development Strategy for Capital Allocation

Kodiak's development strategy reflects industry best practices for advancing large-scale porphyry projects. The company has recently completed a financing round with Canaccord, providing adequate capital for the next phase of development activities. Management plans to focus drilling efforts on expanding known high-grade zones while also testing the 30 additional targets identified across the property.

The logical progression from resource definition to preliminary economic assessment (PEA) represents the next major milestone. Tornquist indicated that

"The next step ... is a PEA, and we could certainly embark on that in the nearer term and right I guess the earliest would be next year."

Strategic Value through M&A Potential

Management's perspective on ultimate project development reflects realistic expectations about capital requirements and industry dynamics. Tornquist acknowledged that

"I don't think there's a single porphyry project that was developed by the junior who did the initial exploration. Very likely at some stage a major will take interest."

This positions Kodiak as an acquisition target rather than an operator, which is typical for large-scale porphyry developments requiring substantial capital investment. The maiden resource serves as a critical catalyst for potential M&A activity, as major mining companies typically prefer to evaluate projects with established resources rather than exploration prospects. Tornquist noted:

"From that perspective, a resource is an important milestone because that really is often where you then start M&A activity getting sort of started and heating up."

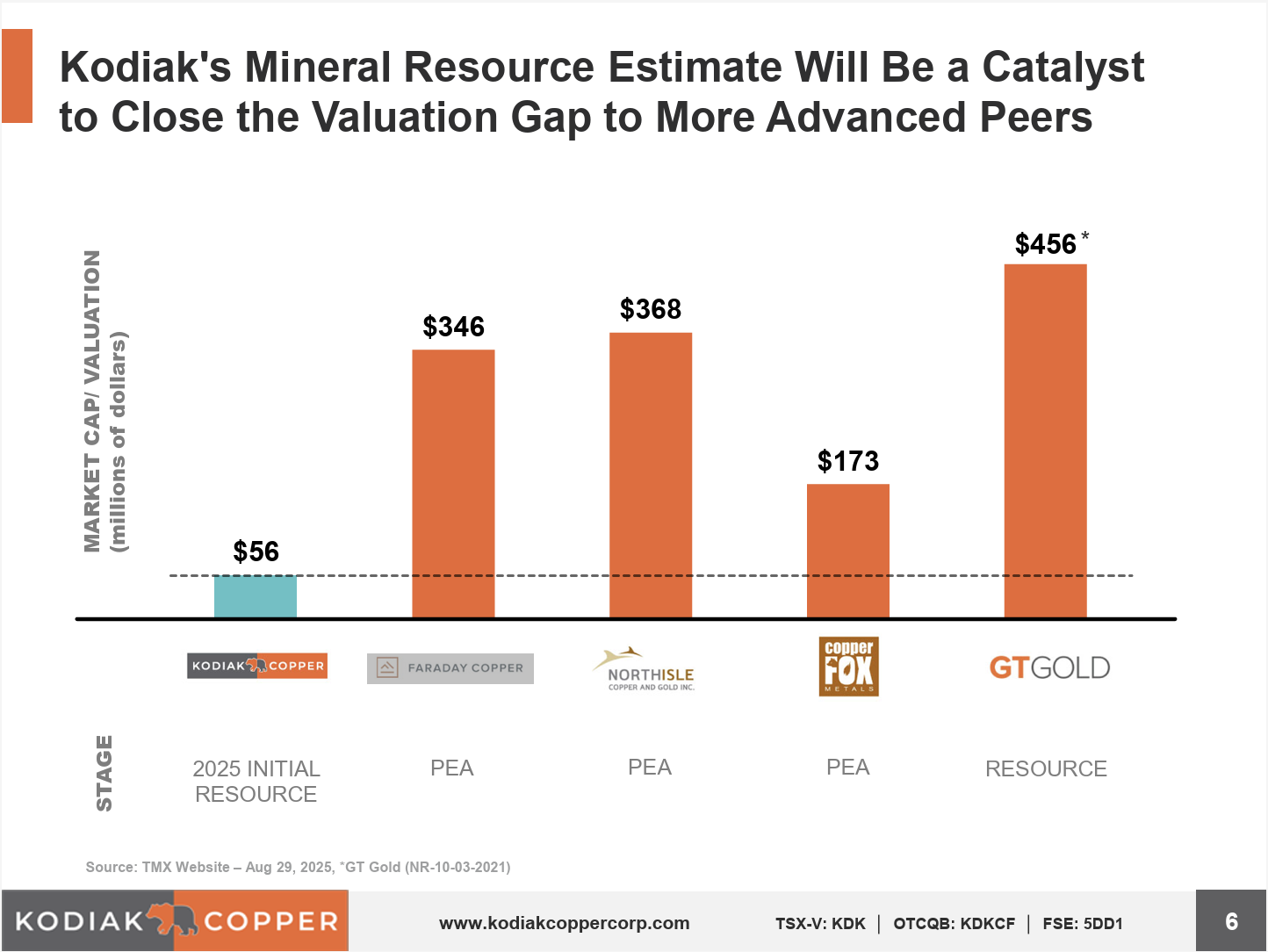

Valuation Gap in Market Positioning

Current market valuation suggests significant upside potential relative to more advanced peers in the porphyry copper sector. Management identified comparable companies trading at $300-400 million market capitalisations, representing five to six times Kodiak's current valuation despite having similar asset quality and development potential. Tornquist emphasized the valuation disconnect:

"What has held back Kodiak's share price in the last year or two is simply that it was very hard for investors to really see what we have. We had six years of drill results, but what does it actually all amount to?"

The maiden resource should provide the clarity needed to close this valuation gap and attract institutional investment interest.

The Investment Thesis for Kodiak Copper

- District-Scale Resource Potential: Consolidated mining district with 90,000 meters of drilling demonstrating significant resource expansion potential across seven mineralized zones

- Near-Term Catalysts: Full maiden resource estimate due Q4 2025 will provide comprehensive view of project scale and economics, likely triggering institutional interest and potential M&A activity

- High-Grade Starter Pit Potential: Near-surface, high-grade zones (including 27m at 1.62% copper) could provide early cash flow generation and improve project economics

- Valuation Gap Opportunity: Trading at significant discount to comparable peers (5-6x lower market cap) despite similar asset quality and development potential

- Strategic Acquisition Target: Management acknowledges likely major mining company interest post-resource, positioning shareholders for potential premium exit

- Dual-Commodity Exposure: Copper-gold project benefits from both critical mineral demand and gold's recent price strength (25% of project value from gold)

- Experienced Management Team: Proven track record in porphyry development with clear understanding of value creation milestones and exit strategies

- Additional Asset Optionality: Mohave project in Arizona provides portfolio diversification and potential value unlock opportunities

Macro Thematic Analysis

The global transition to renewable energy and electrification is driving unprecedented demand for copper, with supply constraints creating a structural deficit expected to persist through the decade. Porphyry copper deposits, which account for approximately 60% of global copper production, are becoming increasingly valuable as grades decline at existing operations and new discoveries remain limited. Kodiak's position in an established mining district with demonstrated mineralization addresses the critical need for new copper supply sources.

The convergence of elevated copper prices, returning institutional interest in mining investments, and the strategic imperative for major mining companies to replenish reserves creates an optimal environment for junior developers with quality assets. Gold's concurrent strength to multi-decade highs adds another dimension to multi-commodity projects like MPD, where precious metal credits can significantly enhance project economics and reduce development risk.

TL;DR

Kodiak Copper is approaching a critical inflection point with its maiden resource estimate due Q4 2025, positioning the company for significant valuation re-rating relative to advanced peers. The MPD project's combination of scale potential, high-grade near-surface zones, and strategic location in an established mining district creates compelling M&A optionality. With experienced management, adequate financing, and clear development milestones ahead, Kodiak offers leveraged exposure to the copper supply shortage while trading at a substantial discount to comparable companies.

FAQ's (AI Generated)

Q: What makes the maiden resource estimate so significant for Kodiak's valuation?

The resource crystallises six years of drilling into quantifiable tonnage and grades, providing institutional investors the clarity needed to value the asset against comparable peers trading at 5-6x higher valuations.

Q: How realistic is the M&A timeline management suggests?

Very realistic - porphyry projects typically attract major company interest post-resource due to capital requirements. Management's acknowledgment that "majors let juniors do exploration then buy the project" reflects industry norms.

Q: What differentiates Kodiak from other copper exploration companies?

District-scale consolidation, 90,000 meters of systematic drilling, near-surface high-grade zones for potential starter pits, and dual copper-gold exposure in an established mining jurisdiction with infrastructure access.

Q: What are the key development milestones investors should watch?

Q4 2025 maiden resource completion, followed by potential PEA in 2026, continued high-grade zone drilling, and increasing strategic interest from major mining companies as development advances.

Q: How sustainable is the current copper price environment for project development?

Structural supply deficits, declining ore grades, and electrification demand support elevated copper prices. Porphyry projects like MPD are essential for addressing the supply gap over the next decade.

Q: What role does the Arizona Mohave project play in the investment thesis?

Currently non-core but provides additional optionality and potential shareholder value through strategic alternatives. Management hints at potential spin-out or joint venture opportunities to unlock separate value streams.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed