Gold at $4,000: The Continued Rise of the All-Occasions Safe Haven & Its Implications for Mining Investors

Gold hits $4,000 as structural demand from central banks and ETFs drives all-weather performance. Low-cost miners in premier jurisdictions gain unprecedented margins.

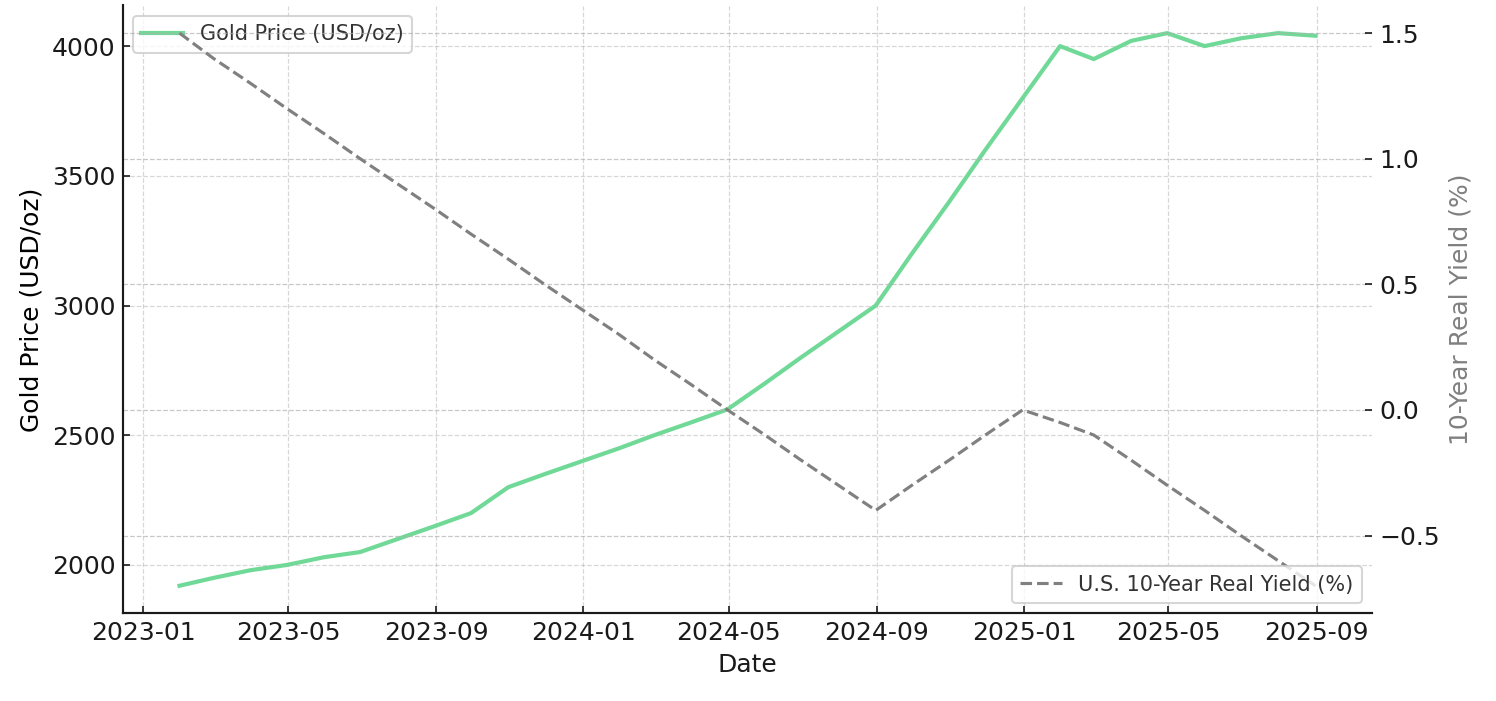

- Gold's rally to $4,000 per ounce marks a structural shift in which the metal now performs during both risk-on and risk-off market phases, breaking historical correlations with equities and real yields.

- The shift reflects five converging forces: monetary easing expectations, equity market volatility, geopolitical fragmentation, currency weakness, and renewed institutional flows into gold-backed products.

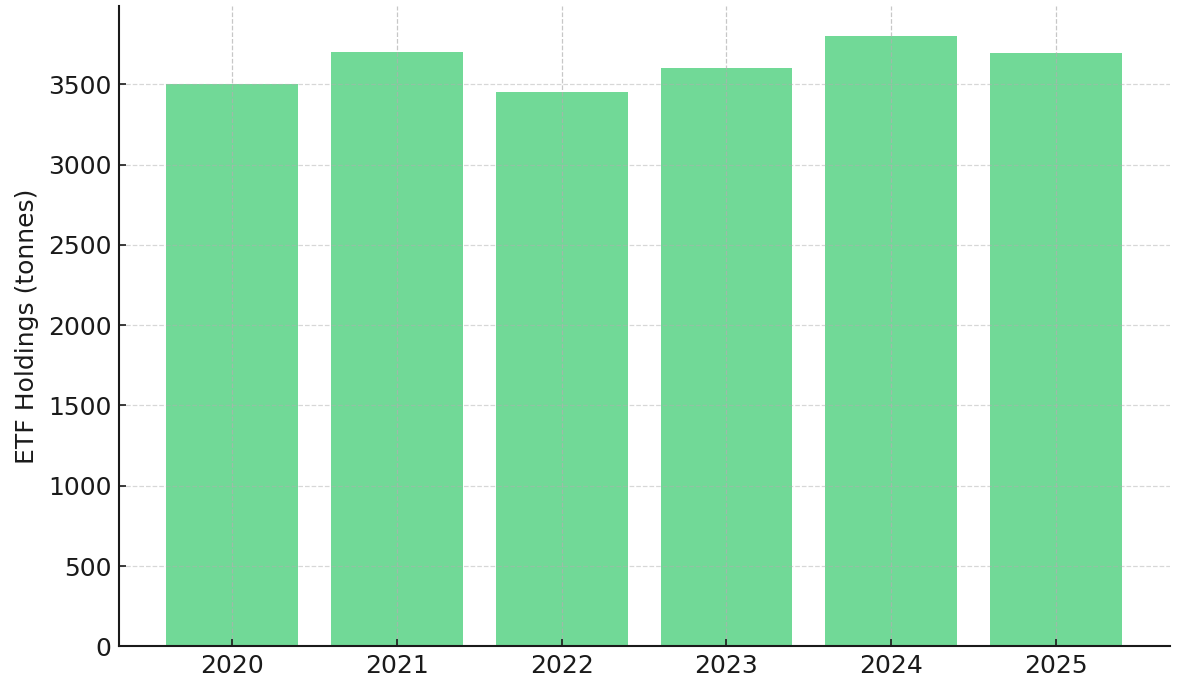

- Exchange-traded fund inflows of 638 tonnes as of October 2025 and record central bank buying underscore that the accumulation cycle remains in its early innings, with structural demand far from exhaustion.

- Elevated prices are widening profit margins for low all-in sustaining cost producers and fast-tracking funding for permitted developers, creating differentiated performance across the mining sector.

- Premier jurisdictions like Nevada and Canada, alongside improving regions such as Brazil's Tapajós gold belt, are attracting disproportionate capital as investors prioritize security of tenure, scalability of assets, and self-funding operational models.

Gold's Structural Repricing: A Metal No Longer Bound to Crisis

Gold's rise to $4,000 per ounce represents more than speculative momentum. It signifies a systemic repricing of risk tolerance across global portfolios. Once relegated to the role of crisis refuge, gold now outperforms during both tightening and easing cycles, defying historical inverse correlations with equities and real yields.

This transformation is supported by macro data showing gold appreciating even as the S&P 500 and Nasdaq reach new highs, indicating that institutional capital now views gold as a complementary rather than oppositional asset to risk assets. The metal's ability to deliver positive returns in diverse market environments reflects a fundamental reassessment of portfolio construction principles among sophisticated allocators.

The implications extend beyond simple correlation analysis. Portfolio managers are increasingly recognizing that traditional diversification through bonds has diminished in efficacy as monetary policy becomes more difficult to predict and fiscal deficits constrain central bank independence. Gold fills this diversification gap, offering liquidity, transparency, and no counterparty risk in an environment where credit quality and political stability can no longer be assumed.

Jeff Quartermaine, Chief Executive Officer and Managing Director of Perseus Mining, observes the operational impact of this sustained price environment:

"Not only have we enjoyed the continuing elevated gold prices which is very important, but the business has run extremely well as well. That combination of things has meant that our cash margins are up, our earnings are up, as I say we've had a very good year."

The Five Forces Driving Gold's Revaluation

Monetary Policy Fatigue & Falling Real Yields

The market's anticipation of continued Federal Reserve rate cuts has compressed real yields, supporting long-duration assets like gold. Dollar softness amplifies this dynamic, prompting capital outflows into commodities that provide inflation protection and currency diversification. Real yields, measured as nominal Treasury yields minus inflation expectations, have declined substantially from their 2023 peaks, removing a key headwind that historically pressured gold prices.

Perseus Mining highlights how low-cost producers thrive under monetary easing cycles. With September 2025 Quarter all-in site costs of 1,463/oz and zero debt, the company captures substantial margins even amid cost inflation pressures. This operational efficiency allows producers to generate free cash flow that can be returned to shareholders or reinvested in growth initiatives without compromising financial stability.

Jeff Quartermaine quantifies the margin environment:

"Every day we're producing at a margin depending on where the gold price is, but it's $1,400 to $1,500 an ounce."

Geopolitical Fragmentation & Policy Instability

From escalating trade tensions between the United States and China to renewed sanctions on Russia, investors are confronting multi-polar risk that traditional portfolio hedges struggle to address. Gold's neutrality makes it the only major reserve asset immune to sanctions, capital controls, or jurisdictional disputes. This characteristic becomes increasingly valuable as geopolitical fault lines deepen.

U.S. Gold Corp's fully permitted CK Gold Project in Wyoming illustrates investor appetite for domestically secure jurisdictions. The project secured all major permits including mining and operating permits, water discharge permits, and air quality permits in November 2024, positioning it as one of the fully permitted projects in North America held by a junior company ready for development.

Luke Norman, Executive Chair of U.S. Gold Corp, emphasizes the jurisdictional premium:

"We received permits end of November last year, fully permitted to mine… One of the only permitted projects in North America in a junior's hands that's ready to go, there's a lineup of capital."

Equity & Bond Market Correlation Breakdown

Gold's concurrent rise with equities underscores its growing cross-asset appeal. As bond returns lag due to persistent inflation concerns and stock valuations stretch to historical extremes, institutional allocators are raising gold exposure for correlation balance. This portfolio rebalancing represents a structural rather than cyclical phenomenon, as the traditional 60/40 stock-bond portfolio has delivered suboptimal risk-adjusted returns in recent years.

i-80 Gold's strategic positioning in Nevada demonstrates how brownfield asset portfolios can provide exposure to gold upside through infrastructure leverage. The company is advancing its hub-and-spoke processing model centered on the Lone Tree autoclave facility. Near-term production is driven by Granite Creek Underground, ramping up in H2 2025 toward steady-state in H1 2026, with the strategic pathway targeting 600,000-plus ounces of annual production by 2032.

Paul Chawrun, Chief Operating Officer of i-80 Gold, quantifies the opportunity cost of delayed production:

"We are losing the margin of $1,000 to $1,200 per ounce that we could be getting once Lone Tree is in operation."

Central Bank & ETF Accumulation

With 638 tonnes added as of October 2025, exchange-traded funds are re-entering a growth phase not seen since 2020. Central banks in China, India, and Germany continue to increase reserves, reinforcing structural demand that is distinct from speculative flows. This institutional accumulation provides a demand floor that supports prices even during periods of profit-taking by tactical traders.

New Found Gold's preliminary economic assessment demonstrates the leverage explorers have to sustain inflows. The company's July 2025 assessment shows a 197% internal rate of return at $3,300 per ounce, illustrating how high-grade discoveries benefit disproportionately from elevated prices. The Phase 1 strategy involves a small high-grade open pit operation producing an average 69,300 ounces in Years 1 to 4 planned to fund Phase 2.

Fiscal Expansion & Currency Debasement

Persistent fiscal deficits and structural debt imply sustained long-term support for gold as governments across developed and emerging markets face limited options to reduce debt burdens without inflating them away. This drives institutional rebalancing into hard assets, particularly those with high operating leverage to price increases.

Cabral Gold’s updated prefeasibility study for the Cuiú Cuiú project in Brazil highlights developer-level torque when capital costs remain modest. With initial capital requirements of $37.7 million and all-in sustaining costs of $1,210 per ounce, the project shows a 139% after-tax internal rate of return at $3,340 per ounce gold.

Alan Carter, President and Chief Executive Officer of Cabral Gold, quantifies the margin opportunity:

"Now we're in a gold price environment which is way above $2,500 an ounce… You're looking at a $3,000 margin here, profit margin on every ounce we produce."

Profitability Reaches Historical Highs: How Producers & Developers Are Positioned

With spot prices at approximately $4,000 per ounce, operational leverage is unprecedented for producers maintaining costs below $1,500 per ounce. Serabi Gold operates the established Palito Complex in Brazil's Tapajós region, reporting consolidated all-in sustaining costs of US$1,792 per ounce in the second quarter of 2025. The company is advancing the Coringa development project, which feeds ore to the Palito processing facilities.

Mike Hodgson, Chief Executive Officer of Serabi Gold, describes the cash-generating capacity:

"That's the power of being a producer in a really quite exciting gold market at the moment right now… We're generating so much money and even with all we're doing in exploration as much as we can."

De-Risked Developers Move to Forefront

Projects with existing permits and regulatory certainty are outperforming peers that face permitting uncertainty or require substantial capital for greenfield development. U.S. Gold Corp's CK Gold Project in Wyoming, with a February 2025 prefeasibility study showing $937 per gold equivalent ounce all-in sustaining costs, typifies how construction-ready assets in premier jurisdictions command premium valuations due to scarcity of new projects with regulatory clarity.

Integra Resources demonstrates how cash-generating assets can fund development pipelines without equity dilution. The company's Florida Canyon Mine in Nevada produced approximately 72,000 ounces in 2024, with 2025 guidance of 70,000 to 75,000 ounces at mine-site all-in sustaining costs of $2,450 to $2,550 per ounce. This production funds advancement of the flagship DeLamar development project, which is progressing toward a feasibility study completion in 2025.

George Salamis, President and Chief Executive Officer of Integra Resources, notes the financial impact:

"We got into this acquisition with the view that if it generated $20 to $30 million a year free cash flow that was good enough, now it's doing much more than that, and it's paying the bills across the board."

Exploration Leverage & New Discoveries

High-grade discoveries like New Found Gold's intercepts in Newfoundland and Cabral Gold's oxide systems in Brazil provide leverage to price momentum without production risk, positioning explorers as optionality plays in the current cycle. These discoveries benefit from multiple valuation catalysts, including resource expansion, metallurgical testing, and strategic interest from larger producers seeking to replenish reserves.

Keith Boyle articulates the cash flow advantage of high-grade assets:

"For us that cash flow of 70,000 ounces a year, at $2,000 that's $140 million, well add another thousand to that and you got over $200 million. That pays for a lot of project development and exploration."

Geographic Capital Rotation & Jurisdictional Premiums

North America: Capital Favors Low-Risk Growth

The United States and Canada dominate new capital flows as investors reward companies with advanced permitting, infrastructure readiness, and clear environmental, social, and governance credentials. Regulatory transparency and established mining codes reduce execution risk, making North American assets particularly attractive during periods of geopolitical uncertainty.

West Red Lake Gold Mines' restart of the Madsen Mine in Ontario's Red Lake District demonstrates how inherited infrastructure reduces capital intensity, as approximately C$350 million invested prior to WRLG's purchase reduced the capital burden and mitigated risk. The existing infrastructure includes a mill with a Pre-Feasibility Study (PFS) base capacity of 800 tonnes per day. The company is currently in the ramp-up phase towards achieving commercial production, and has produced 12,800 ounces of gold between Q1 and Q3 2025.

Gwen Preston, Vice President of Communications at West Red Lake Gold Mines, describes the market opportunity:

"The companies that are generating new gold production outperform the rest of the gold equities in gold bull markets… We want to offer new gold production to investors and chart a path to become a mid-tier gold miner, a producer of scale."

Africa: Diversified Production Base as a Hedge

Perseus Mining's operations across Ghana and Côte d'Ivoire, combined with the Nyanzaga development project in Tanzania targeting first production in January 2027, demonstrate how multi-jurisdictional exposure can act as a natural geopolitical hedge. This geographic diversification mitigates country-specific risks while maintaining exposure to jurisdictions with substantial resource endowments.

Risks & Tactical Volatility in a $4,000 Market

Short-term risks include technical overextension and potential profit-taking by institutional investors who have accumulated substantial gains. The rapid 36-day climb from $3,500 to $4,000 per ounce, reaching the milestone on October 8, 2025, contrasts with historical 1,000-day cycles for equivalent price moves, raising the likelihood of temporary pullbacks as momentum exhausts.

Technical analysis as of late October 2025 identifies key levels including the $4,192 pivot resistance, $4,000 as initial support, and $3,846 to $3,741 as deeper support zones. These levels provide reference points for position sizing and risk management, particularly for investors using leveraged exposure through mining equities.

Liquidity risks merit consideration as well. Margin calls or credit squeezes in other asset classes could trigger liquidation across high-performing assets, including gold, as investors raise cash to meet obligations. While gold's safe-haven characteristics typically protect it during such episodes, extremely rapid deleveraging can create temporary dislocations.

George Salamis describes Integra Resources' risk management approach:

"We're covered on the downside. We have puts down to $2,750, that basically locks in a margin for us which guarantees the cash flows to go back into the operation to make it self-sustaining and grow."

The Investment Thesis for Gold

- Structural repricing of gold from crisis hedge to core allocation is supported by long-term geopolitical fragmentation, fiscal deficits across developed markets, and declining confidence in traditional portfolio diversification through bonds.

- Early-stage accumulation cycles are evident in exchange-traded fund and central bank buying patterns that remain well below prior peaks despite price appreciation, implying continued inflows as institutional investors rebalance portfolios toward hard assets.

- Margin resilience among established producers like Perseus Mining sustains strong free cash flow yields even under cost inflation, enabling dividend programs and growth reinvestment without external capital requirements.

- Scarcity of new supply persists as exploration-to-development conversion remains slow due to extended permitting timelines, favoring permitted developers such as U.S. Gold Corp that can reach production within compressed timeframes.

- Jurisdictional premiums for North American operations alongside improving regions such as Brazil's Tapajós gold belt offer defensible valuations, with regulatory transparency and established frameworks reducing execution risk for sophisticated investors.

- Development-stage leverage is amplified in high-grade projects like New Found Gold and Cabral Gold, where economic assessments show internal rates of return exceeding 130% at elevated gold prices, providing asymmetric upside to sustained price strength.

- Infrastructure advantages benefit companies like West Red Lake Gold Mines and i-80 Gold that can utilize existing processing facilities and established mining districts, reducing capital intensity and accelerating paths to cash flow generation.

A Redefined Safe Haven for the Modern Portfolio

Gold's 2025 breakout reflects more than investor anxiety. It represents a recalibration of what constitutes safety in a multi-polar world where debt burdens continue rising, geopolitical alliances fracture along new fault lines, and fiat currency credibility faces persistent questions from both institutional and retail investors.

The beneficiaries of this shift are capital-disciplined miners and developers positioned in stable jurisdictions, backed by efficient cost structures and scalable production potential that can respond to demand without compromising financial stability. As the metal transitions from niche allocation to foundational portfolio component, the next phase of performance will be defined not by speculative demand but by sustained capital rotation into tangible, margin-protected assets that can deliver returns across diverse market conditions.

Mining investors face a landscape of differentiated opportunities across the development spectrum. Established producers with low all-in sustaining costs and debt-free balance sheets provide exposure to margin expansion and free cash flow generation. Permitted developers in premier jurisdictions offer leverage to production growth without exploratory risk. High-grade explorers deliver option value on discoveries that can reach production quickly using conventional processing methods.

The structural forces supporting gold's revaluation show no signs of abating. For investors seeking exposure to these trends, the gold mining sector offers differentiated access points calibrated to risk tolerance and investment horizon, with the current price environment creating opportunities across the quality spectrum that were unavailable during prior cycles.

TL;DR

Gold's rise to $4,000 per ounce marks a fundamental shift from crisis hedge to core portfolio allocation, performing strongly in both risk-on and risk-off environments. This structural repricing is driven by monetary easing expectations, geopolitical fragmentation, central bank accumulation, and record ETF inflows of 638 tonnes through October 2025. Low-cost producers are capturing margins exceeding $1,400 per ounce, while permitted developers in stable jurisdictions like Nevada, Canada, and Brazil's Tapajós region are attracting premium capital. The accumulation cycle remains early-stage despite elevated prices, with mining companies offering differentiated exposure across producers, developers, and high-grade explorers. Traditional portfolio diversification through bonds has weakened, positioning gold as an essential asset for managing multi-polar geopolitical risk and currency debasement concerns.

FAQs (AI-Generated)

Gold has transitioned from a pure crisis hedge to a core portfolio asset, benefiting from monetary policy uncertainty, geopolitical fragmentation, and declining real yields regardless of equity market direction.

Low-cost producers with all-in sustaining costs below $1,500/oz and permitted developers in stable jurisdictions like the U.S., Canada, and Brazil capture the highest margins and fastest funding access.

Yes, central banks in China, India, and Germany continue increasing reserves, while ETFs added 638 tonnes through October 2025, indicating the accumulation cycle remains in early stages.

Short-term risks include technical overextension after rapid price appreciation, potential profit-taking by institutional investors, and liquidity-driven selloffs if credit markets experience stress.

Mining equities amplify gold's performance through operational leverage—each dollar increase in gold price flows directly to margins, with low-cost producers and high-grade developers offering the greatest sensitivity to price movements.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed