Lifezone Metals Delivers Robust Economics in Kabanga Initial Assessment with $2.37 Billion NPV, 22-year Mine Life

Lifezone Metals reports $2.37B after-tax NPV and 22.9% IRR for Kabanga Nickel Project, setting stage for Tanzania's largest nickel operation with integrated refinery.

- Lifezone Metals' Initial Assessment for the Kabanga Nickel Project demonstrates strong economics with a $2.37 billion after-tax net present value at 8% discount rate and 22.9% after-tax internal rate of return.

- The vertically integrated development plan includes a 22-year underground mine producing 67.9 million tonnes at 1.93% nickel grade, followed by a hydrometallurgical refinery at Kahama producing battery-grade materials.

- Pre-production capital costs are estimated at $991 million with 16.1% contingency, while total project revenue is projected at $23.68 billion over the mine life.

- The project demonstrates resilience to price volatility, maintaining $1.48 billion NPV and 17.9% IRR even at reduced nickel prices of $7.00 per pound.

- Lifezone expects to complete the Feasibility Study Technical Report Summary in July 2025, focusing specifically on the initial underground mine and concentrator development phase.

Lifezone Metals Limited (NYSE:LZM) is a technology-focused mining company developing sustainable extraction and processing solutions for critical battery metals. The company's flagship asset is the Kabanga Nickel Project in northwest Tanzania, which represents one of the world's largest undeveloped high-grade nickel sulfide deposits. Through its partnership with the Government of Tanzania, Lifezone is positioned to become a significant producer of battery-grade nickel, copper, and cobalt materials essential for the global energy transition.

Project Overview and Technical Specifications

The Initial Assessment utilizes 46.8 million tonnes of attributable Measured and Indicated Mineral Resources grading 2.09% nickel, 0.29% copper, and 0.16% cobalt, plus 11.3 million tonnes of Inferred Mineral Resources grading 2.08% nickel, 0.28% copper, and 0.15% cobalt. Lifezone holds a 69.713% ownership stake in the project.

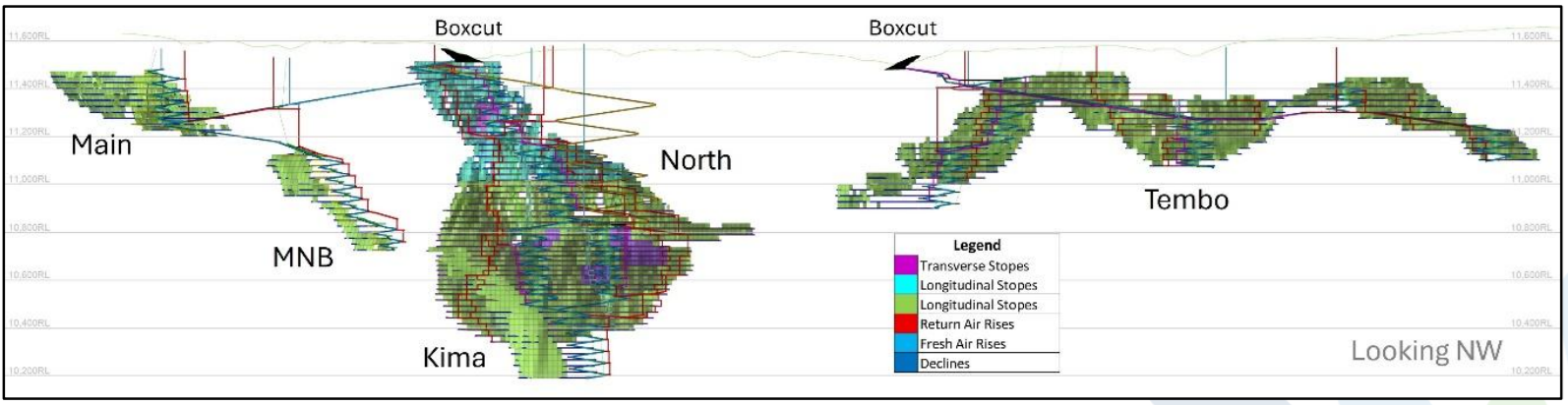

The Kabanga Nickel Project Initial Assessment outlines a comprehensive mining operation spanning 22 years with significant scale and scope. The project encompasses mining zones including Main, MNB, Kima, North, and Tembo, based on the December 2024 Mineral Resource Update.

In the Feasibility Study Technical Report Summary, Chief Executive Officer Chris Showalter emphasized the project's significance, stating:

"The Kabanga Nickel Project represents a rare opportunity to develop a large-scale, high-grade nickel Mineral Resource with robust economics and a clear staged development path to production. The Initial Assessment highlights the project's potential to deliver positive returns over a long life, supported by a low-cost operating profile, with approximately 80% of the project's value attributed to the Kabanga mine and concentrator."

The mining operation will process 3.4 million tonnes per annum through underground methods, producing high-grade concentrate containing 17.3% nickel. Recovery rates are projected at 87.3% for nickel, 95.7% for copper, and 89.6% for cobalt through conventional froth flotation processing.

Integrated Refinery Strategy

A key differentiator for the Kabanga project is the planned hydrometallurgical refinery at Kahama, which will commence operations five years after mine startup. This facility will have production capacity of 50,000 tonnes per annum of battery-grade nickel sulfate, 7,000 tonnes per annum of LME Grade A 99.99% copper cathode, and 4,000 tonnes per annum of cobalt sulfate.

The staged development approach allows Lifezone to generate cash flow from concentrate sales during the initial five-year period while constructing the refinery. This strategy aligns with Tanzania's objectives for in-country beneficiation and value addition.

Source: Lifezone Metals Files Initial Assessment for the Kabanga Nickel Project in Tanzania

Financial Analysis and Capital Requirements

The Initial Assessment's economic analysis demonstrates compelling returns based on long-term consensus metal prices of $8.49 per pound nickel, $4.30 per pound copper, and $18.31 per pound cobalt:

- Total project revenue is estimated at $23.68 billion, generating $8.03 billion in after-tax free cash flow.

- Capital expenditure requirements include $991 million in pre-production costs with a 16.1% contingency, $152 million in capitalized operating expenses, and $751 million in growth capital primarily for refinery construction.

- Sustaining capital over the mine life totals $1.56 billion, including closure costs.

- Operating costs are projected at approximately $90 per tonne processed, covering mining, processing, refining, general and administrative expenses, and logistics.

- All-in sustaining costs for refined nickel average $2.71 per pound, net of copper and cobalt by-product credits.

The project demonstrates robust economics across various price scenarios. Chief Operating Officer Gerick Mouton highlighted the milestone achievement:

"This marks a significant and historic milestone in the nearly five-decade journey of the Kabanga Nickel Project. For the first time, Lifezone has successfully completed and publicly disclosed a technical-economic Initial Assessment in accordance with U.S. SEC Regulation S-K 1300."

Sensitivity analysis reveals the project maintains viability even under stressed conditions. At $7.00 per pound nickel pricing, the project retains an after-tax NPV of $1.48 billion and IRR of 17.9%, demonstrating downside protection for investors.

The economic resilience stems from the high-grade mineral resource, valuable by-product credits from copper and cobalt, low all-in sustaining costs, and efficient capital deployment. The payback period from final investment decision is projected at 9.8 years, including the 2.5-year construction period.

A scenario excluding Inferred Mineral Resources still generates attractive returns with an after-tax NPV of $2.02 billion and IRR of 23.0%, reflecting higher average feed grades but lower total tonnage. This provides additional confidence in the project's fundamental economics.

Environmental and Social Considerations

The project incorporates sustainable tailings management aligned with Global Industry Standard on Tailings Management and Australian National Committee on Large Dams best practices. Approximately 52% of non-pyrrhotite tailings will be returned underground as paste aggregate fill, while remaining tailings will be stored in a fully lined facility designed to accommodate 50 million tonnes and withstand extreme weather events.

The design has undergone review by an Independent Tailings Review Board, Government of Tanzania regulators, and industry experts, providing additional validation of the environmental management approach.

Development Timeline and Next Steps

Lifezone expects to complete the Feasibility Study Technical Report Summary in July 2025, focusing specifically on the underground mine and concentrator development phase. This study will provide more detailed engineering and cost estimates to support project financing and construction decisions.

Mouton emphasized the development approach:

"Through disciplined engineering and extensive analysis, the Lifezone team has systematically de-risked the development of the underground mine and concentrator. The adopted staged development approach provides a high level of confidence in our ability to deliver a project that is both economically resilient and operationally robust."

The company has scheduled to File the Kabanga Nickel Project Feasibility Study Technical Report Summary Before Market Open on July 18th 2025.

Investment Conclusion

The Kabanga Nickel Project Initial Assessment presents a compelling investment opportunity in the critical battery metals sector. With robust economics, proven management execution, and strategic positioning in Tanzania's mining sector, Lifezone Metals offers investors exposure to high-grade nickel resources with integrated processing capabilities.

The project's strong financial metrics, including the $2.37 billion NPV and 22.9% IRR, combined with demonstrated price resilience and staged development approach, position Lifezone as a potential leader in sustainable nickel production. The upcoming Feasibility Study will provide additional clarity on near-term development plans and capital requirements.

For investors seeking exposure to the energy transition metals theme, Lifezone Metals represents a development-stage opportunity with significant scale, strategic government partnerships, and a clear path to production in a politically stable jurisdiction. The company's focus on responsible development and long-term value creation aligns with evolving ESG investment criteria while addressing growing global demand for battery-grade materials.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed