Tariff Truce & Copper's Repricing Path: How US-China Trade Easing Resets the Market's Risk Premium

US-China tariff cuts restore copper market confidence, but structural supply deficits persist. Goldman Sachs projects $10-11K/mt through 2027 amid energy transition demand.

- The US-China tariff rollback (cutting duties from 57% to 47%) and China's rare earth export pause mark a turning point in trade diplomacy, restoring investor confidence in industrial metals.

- Copper markets have rebounded from supply disruptions and tariff-driven distortions, but lingering demand uncertainty in China and overextended inventories in the US temper upside momentum.

- Price forecasts from Goldman Sachs ($10,000–$11,000/mt through 2026-2027) and the World Bank ($9,700/mt in 2025) suggest sustained strength, underpinned by the energy transition and AI-led infrastructure growth.

- Exploration and development-stage copper companies, such as Gladiator Metals, Marimaca Copper, and Fitzroy Minerals, are strategically positioned to benefit from investor rotation into supply-constrained jurisdictions.

- The key investor question: does the tariff expiry remove structural bottlenecks or merely postpone the next supply shock?

The Policy Reset: Tariff Expiry & Its Geopolitical Context

The October 30, 2025, meeting between US President Donald Trump and Chinese President Xi Jinping in Busan marked the most significant policy easing since the onset of the trade war. Under the agreement, the US trimmed tariffs on Chinese imports to 47% from 57%, while Beijing pledged to curb fentanyl exports, resume US soybean purchases, and pause export controls on rare earths for one year. The agreement broadly returned bilateral ties to their status before the tit-for-tat escalation in April 2025.

While copper was not explicitly included in the tariff rollback, the reduction of policy friction directly impacts investor sentiment and trade liquidity. Elevated uncertainty had suppressed risk appetite across base metals, widening the COMEX–LME copper spread and distorting pricing mechanisms since mid-2025.

The détente's immediate effect is psychological, lower risk premiums and improved trade confidence. Medium-term, it restores predictability to supply chains, particularly for semi-finished copper and intermediate goods that faced higher tariff rates in prior months. However, the agreement remains what analysts characterize as a fragile truce, with potential for re-escalation depending on enforcement outcomes. For copper investors, this policy normalization window offers a tactical opportunity to reassess exposure across jurisdictions and development stages.

Market Response: Copper Price Stabilization & Tariff Lag Effects

Following the announcement, copper prices rallied modestly, extending gains from Q3 2025's recovery phase. The near-term drivers were twofold: accelerated importer activity before tariff implementation, and subsequent supply normalization as trade costs fell.

Leading up to the US tariffs, accelerated shipments to the US lifted onshore inventories and caused the price spread between the COMEX and LME exchanges to widen. This artificial tightening lifted sentiment but masked underlying demand weakness in manufacturing sectors sensitive to higher borrowing costs and slowing industrial output. Goldman Sachs noted that excess US inventory could quickly rebalance the market if LME spreads tighten.

An accident at one of the world's largest copper mines in September 2025 further spiked copper prices, demonstrating the market's sensitivity to supply disruptions even amid elevated inventory levels. The temporary inventory buildup created pricing dislocations that sophisticated investors have begun to arbitrage, particularly through the COMEX–LME spread.

The easing of tariffs removes cost friction but not structural supply risks. The broader market repricing will depend on China's industrial recovery trajectory and new mine development timelines. Current data suggests Chinese property sector weakness continues to constrain copper demand growth, while manufacturing indicators show only marginal improvement. The removal of tariff-induced volatility improves visibility for project financing and merger activity, particularly in jurisdictions offering regulatory transparency and infrastructure proximity.

The Macro Framework: Copper's Structural Tightness Beyond Policy Cycles

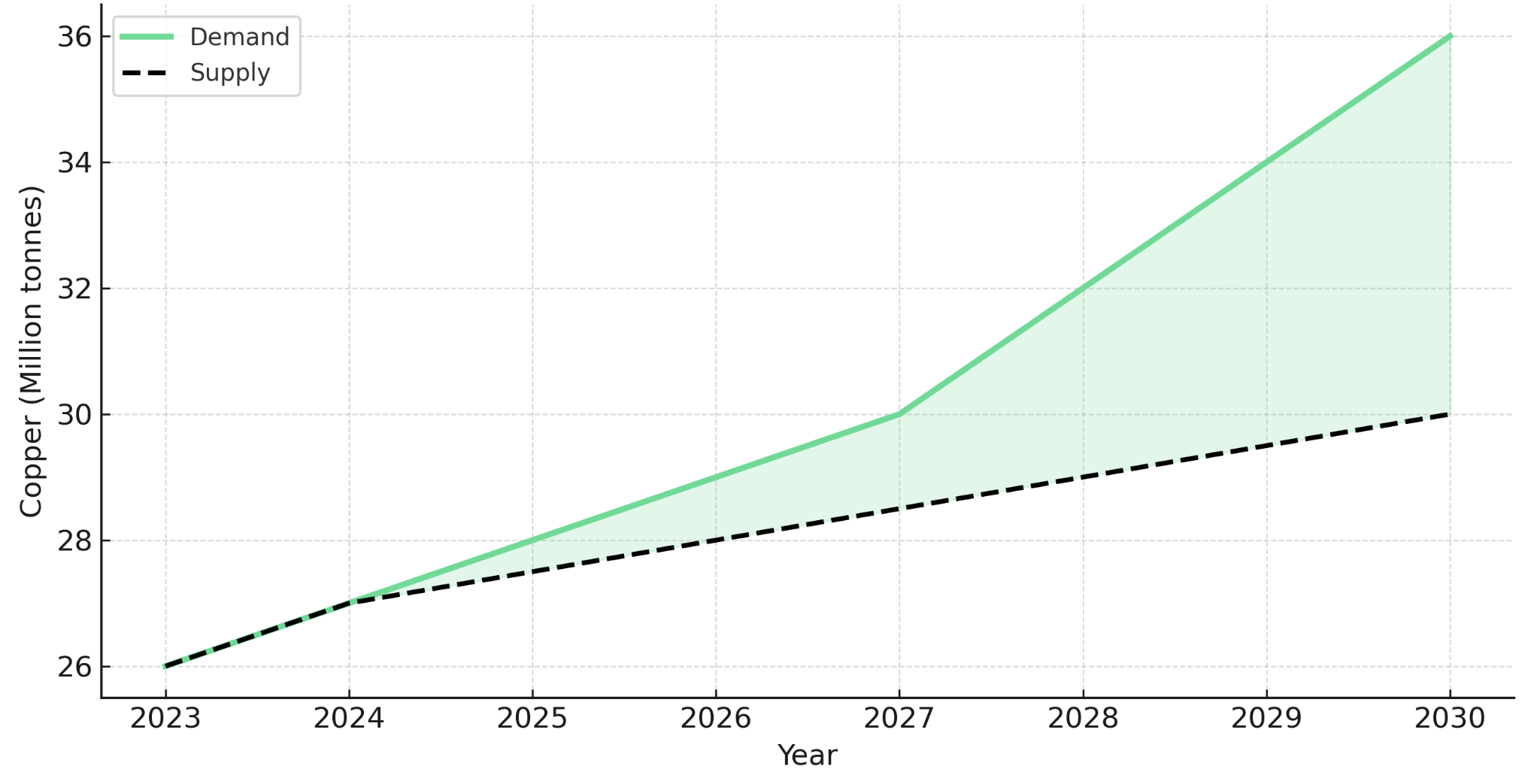

Even with tariffs easing, copper remains anchored by long-term supply constraints and energy transition demand. Goldman Sachs, in an October 11, 2025 forecast, expects copper prices to stay in a range of $10,000–$11,000 per metric ton during 2026-2027, reflecting durable supply constraints and energy transition demand despite near-term headwinds.

The World Bank's Commodity Markets Outlook (October 2025) reinforces this trajectory, projecting a 6.1% copper price increase in 2025 to $9,700/mt. Despite interim surpluses created by temporary demand weakness, structural deficits are expected from 2028 onward as grid electrification, electric vehicle manufacturing, and AI data center buildouts accelerate. The International Energy Agency estimates that achieving net-zero emissions by 2050 requires a doubling of copper supply by 2040, a target that current project pipelines appear insufficient to meet without significant price incentives.

Key analytical contrasts frame the investment landscape. Upside potential stems from AI infrastructure deployment, renewable energy installations, and transmission grid upgrades that collectively represent multi-decade demand tailwinds. Downside risk centers on China's slowing property sector, weaker global industrial output, and the potential for demand destruction if copper prices sustain elevated levels for extended periods. The policy easing between Washington and Beijing reduces one source of volatility but does not alter the fundamental supply-demand imbalance driving copper's structural repricing.

Investor Positioning: Policy Easing Meets Energy Transition Demand

Copper's dual exposure to industrial policy and technological innovation—makes it the most geopolitically sensitive of base metals. As tariff barriers lower, institutional investors are reallocating toward jurisdictionally secure and capital-efficient projects that offer exposure to structural demand growth without execution risk inherent in less established mining regions.

Western diversification strategies away from Chinese supply chains increase demand for assets in Canada, Chile, and Australia. Infrastructure-related copper usage in renewables, electric vehicle charging networks, and AI-driven data centers continues to offset weak manufacturing demand, though Goldman Sachs cautions that data center copper intensity may be overstated in some bullish forecasts.

Marimaca Copper's development-stage project in Chile exemplifies capital efficiency in established mining jurisdictions. The company's definitive feasibility study, announced August 25, 2025, confirms a post-tax net present value of US$1.1 billion at an 8% discount rate and an internal rate of return of 39% at $5.05/lb copper. Hayden Locke, President and Chief Executive Officer of Marimaca Copper, emphasizes the project's competitive positioning:

"It confirms that we are in the bottom decile of capital intensity for copper projects, new development-stage copper projects globally. We're sub $12,000 a ton of copper equivalent production, which is a very nice place to be."

The project's capital intensity of under $12,000 per ton of annual copper production places it among the most efficient new developments globally. Additionally, according to the company's definitive feasibility study, Marimaca's heap leach processing route is 38% less carbon intensive than traditional processing methods, aligning with investor mandates for low-carbon copper supply.

The scarcity of actionable development-stage copper projects amplifies strategic value for advanced assets. Locke notes the competitive landscape:

"What we know is there are very few actionable copper projects in the near term that can become a reasonably significant producer of copper."

This scarcity dynamic underpins merger and acquisition activity across the sector. As of September 11, 2025, Marimaca's major shareholders include Greenstone (22.3%), Assore (16.3%), Ithaki Limited (14.1%), and Mitsubishi Corp. (4.0%)—institutional backing that provides development financing capacity and strategic support. The tariff détente improves financing conditions for development-stage assets, potentially accelerating timelines for projects with pre-construction readiness and institutional support.

Supply Fragility: Beyond Tariffs, the Real Constraint Is the Ore Body

While tariffs influence near-term pricing, structural scarcity remains the defining driver of copper's investment thesis. The copper supply chain is heavily concentrated in Chile, Peru, and the Democratic Republic of Congo, regions subject to regulatory evolution, labor negotiations, and environmental considerations. Chile, the world's largest copper producer, faces declining ore grades at legacy operations and significant capital requirements to maintain current output levels.

Gilberto Schubert, Chief Operating Officer and Country Manager of Fitzroy Minerals, quantifies this challenge:

"Most of the investment in Chile today, there's a huge amount of money that's going to be invested in the coming years just to keep the production as it is because of the lower grades, the deeper mines."

This capital intensity to sustain existing production creates opportunities for new discoveries that can deliver meaningful incremental supply. Even modest disruptions can catalyze outsized price reactions, as demonstrated by the September 2025 mine accident in Indonesia that spiked copper prices despite broader inventory conditions.

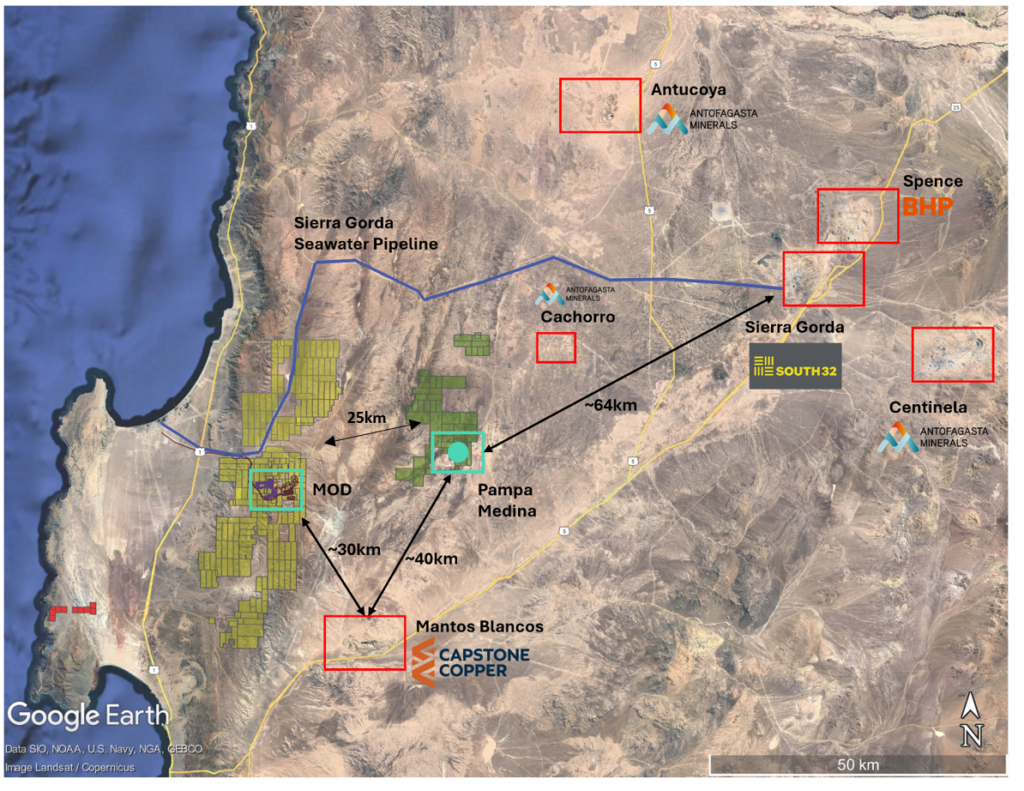

Fitzroy Minerals' exploration portfolio in Chile and Argentina represents exposure to early-stage iron oxide copper gold systems with discovery potential in Chile's mining belt. The company's Buen Retiro prospect intersected 110 meters at 1.94% copper, while the Caballos target returned 200 meters at 0.81% copper equivalent. Phase 2 drilling programs exceeding 8,000 meters are in progress at Buen Retiro, with additional work planned at Caballos. Schubert emphasizes the project's locational advantages:

"We are close to Copiapó, one of the main mining towns in Chile, close to the Pan- American Road, to the main power grids of Chile, 40 kilometers to the coast in the middle of the desert. This type of location makes the projects easier and faster to be built."

The project sits 5 kilometers from the Pan-American Highway and existing transmission lines, and 60 kilometers from Copiapó, proximity that reduces potential development costs, though grid connections and infrastructure agreements would require future permitting and capital expenditure. The company is evaluating low capital intensity development strategies, including pregnant leach solution trucking to nearby processing facilities. Additionally, Fitzroy has established a partnership opportunity with Pucobre S.A., which holds a 30% clawback right on the Buen Retiro option.

Exploration Leverage: Jurisdictional Quality & Resource Scalability

The tariff détente creates favorable conditions for exploration-stage investments in established mining jurisdictions. Canada's Yukon Territory offers transparent regulations, established infrastructure, and proximity to North American markets increasingly focused on supply chain security.

Gladiator Metals' Whitehorse Copper Belt project demonstrates institutional interest in scalable, high-grade exploration opportunities in secure jurisdictions. The company is conducting advanced exploration work with the objective of defining a significant copper system. Jason Bontempo, Chief Executive Officer and Director of Gladiator Metals, outlines the exploration vision:

"Our view is that we are targeting over 100 million tons at above 1% copper, not including any credits. If we can deliver high-grade surface copper tons of anywhere from 1 to 2% copper from surface, and we're ranging in plus 20 million tons at each of these areas, it certainly becomes very attractive."

Gladiator is targeting pre-resource delivery at Cowley Park in 2026 and is working toward a Class 3 permit approval (a five-year drilling permit) in Q1 2026. As of October 2025, the company maintains a cash position of approximately $27 million with drilling programs planned through December 2025.

Bontempo emphasizes the project's infrastructure advantages and community engagement progress:

"This project is right next to the best infrastructure. I would much rather engage in positive community engagement and acceptance and social license than be remote and have overbearing capital requirements or other challenges with what being remote brings."

Infrastructure proximity and established community relationships reduce permitting risk and capital intensity, factors that directly influence project valuations. For institutional investors seeking early-stage copper exposure, Gladiator's combination of exploration potential, jurisdictional quality, and infrastructure access offers entry into a commodity where supply scarcity is increasingly priced into forward curves.

Market Repricing: Copper's New Normal & Investor Risk Calibration

As tariffs expire, copper's risk premium gradually compresses. But investors should not conflate temporary price normalization with structural equilibrium. The realignment of capital flows toward lower-risk jurisdictions reflects a strategic repricing of geopolitical considerations rather than pure demand growth.

The COMEX–LME price spread is expected to narrow as US inventory positions normalize and trade flows adjust to the new tariff regime. Medium-term investment flows will prioritize projects with defined permitting timelines and pre-construction readiness. Companies with institutional backing gain traction as investors seek copper exposure that offers leverage to rising prices without operational complexity.

The tariff expiry functions as a confidence catalyst, but one that rewards project execution discipline over speculative momentum. Companies demonstrating capital efficiency, jurisdictional quality, and alignment with institutional environmental, social, and governance mandates command attention relative to peers lacking clear development pathways.

The Investment Thesis for Copper

Copper remains the most structurally constrained industrial metal, policy easing amplifies, rather than negates, its long-term investment case. The following factors support strategic accumulation of copper exposure across the development and exploration spectrum:

- Policy normalization through the US-China tariff détente lowers trade friction and volatility, improving project financing conditions and removing uncertainty that previously constrained strategic planning and capital allocation decisions.

- Energy transition demand from electrification infrastructure, electric vehicle adoption, and AI-driven data center construction continues to anchor multi-year copper consumption growth despite near-term headwinds from Chinese property sector weakness.

- Supply scarcity driven by limited new discoveries, declining ore grades at major producing mines, and capital discipline among major producers constrains long-term supply growth and supports sustained price strength through the remainder of the decade.

- Capital rotation toward established mining jurisdictions with environmental, social, and governance credentials and infrastructure readiness favors companies operating in Canada, Chile, and Australia, where regulatory transparency and permitting predictability reduce execution risk.

- Valuation upside potential exists for development-stage projects with low all-in sustaining costs and strong internal rates of return that are positioned to capture rerating potential as copper reprices toward the $10,000–$11,000/mt range projected by Goldman Sachs for 2026-2027.

- Exploration leverage in geologically prospective belts with established infrastructure access offers risk-adjusted exposure to future supply growth in jurisdictions increasingly favored by supply chain diversification strategies and Western capital allocation frameworks.

A Fragile Peace in a Tight Market

The October 30, 2025 tariff rollback is less an endgame and more a reset of global trade expectations. While it alleviates short-term pressure on supply chains, copper's price trajectory remains driven by the intersection of policy stability and structural scarcity. The fundamentals supporting copper's investment thesis, energy transition demand, supply constraints, and declining ore grades, persist regardless of tariff regimes.

For investors, this détente offers a window to accumulate exposure to jurisdictionally advantaged, capital-efficient copper developers before the next cycle of supply constraints emerges. The market's recalibration underscores one clear message: policy may fluctuate, but the physics of electrification, and the scarcity of copper, remain immutable.

TL;DR

The October 2025 U.S.-China tariff rollback from 57% to 47% marks a pivotal shift in trade policy, reducing volatility in copper markets. While this détente improves short-term supply chain predictability, it does not resolve copper's fundamental scarcity. Goldman Sachs forecasts prices at $10,000-$11,000/mt through 2026-2027, supported by energy transition demand and declining ore grades at major mines. Institutional investors are rotating capital toward development and exploration companies in jurisdictions like Canada, Chile, and Australia that offer regulatory transparency and infrastructure proximity. The policy normalization creates a window for strategic accumulation before structural supply deficits emerge from 2028 onward, driven by electrification infrastructure, electric vehicle adoption, and AI data center expansion.

FAQs (AI-Generated)

The tariff reduction from 57% to 47% lowers trade friction and removes a risk premium from copper pricing. While copper was not explicitly included in the agreement, reduced policy uncertainty improves investor confidence and supply chain predictability. However, the impact is primarily psychological and medium-term rather than structural. Goldman Sachs projects copper prices will remain in the $10,000-$11,000/mt range through 2026-2027, driven by energy transition demand and supply constraints rather than tariff policy.

Long-term copper demand is anchored by the energy transition, including grid electrification, electric vehicle manufacturing, renewable energy installations, transmission upgrades, and AI-driven data center construction. The International Energy Agency estimates that achieving net-zero emissions by 2050 requires a doubling of copper supply by 2040. These structural demand tailwinds persist regardless of short-term tariff policies or cyclical manufacturing weakness in regions like China's property sector.

Copper supply faces multiple constraints: declining ore grades at major producing mines, limited new discoveries, capital discipline among major producers, and concentration in regions subject to regulatory evolution and labor negotiations. Chile, the world's largest producer, requires significant capital investment simply to maintain current production levels as mines deepen and grades decline. Current project pipelines appear insufficient to meet projected demand without significant price incentives.

Institutional investors favor established mining jurisdictions including Canada, Chile, and Australia, which offer regulatory transparency, permitting predictability, established infrastructure, and environmental, social, and governance credentials. These regions reduce execution risk and align with supply chain diversification strategies moving away from Chinese-dominated supply chains. The tariff détente amplifies this rotation toward jurisdictionally secure and capital-efficient projects.

Development-stage copper projects with completed feasibility studies, low capital intensity (under $12,000 per ton of production), strong internal rates of return, and institutional backing offer leveraged exposure to rising copper prices without operational complexity. The scarcity of actionable near-term copper projects—those that can become significant producers within reasonable timelines—creates competition among major producers seeking to replace depleting reserves, driving merger and acquisition activity in the sector.

Analyst's Notes

Subscribe to Our Channel

Stay Informed