Oil M&A Crashes 60% Creating Value Opportunities as Producers Generate Record Cash at Breakeven Costs

Oil & gas offers compelling value through enhanced capital discipline, favorable supply-demand dynamics, and strategic energy transition positioning.

- US upstream oil & gas dealmaking fell 60% in H1 2025 to $30.5 billion, driven by commodity price volatility and market uncertainty, with oil prices swinging from $57 to $75 per barrel in Q2/25.

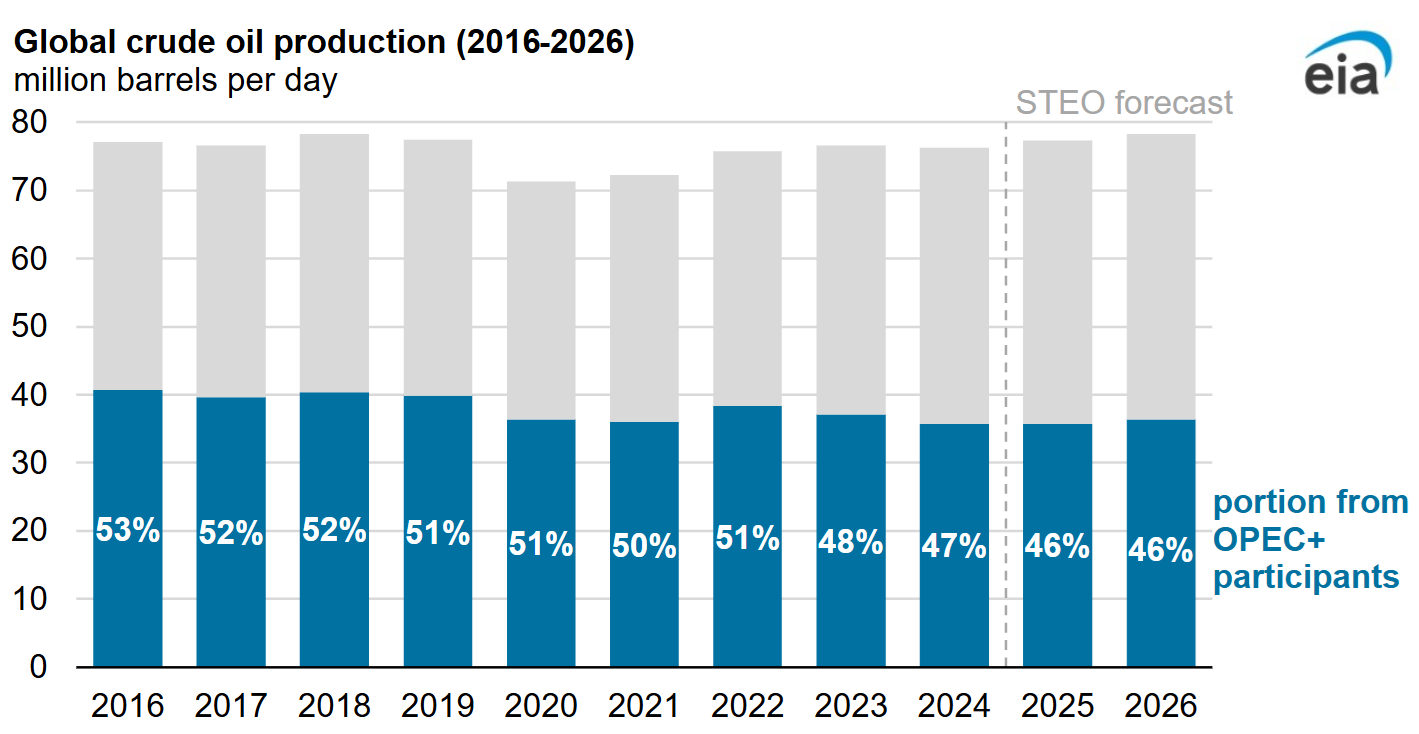

- Global oil supply is expected to outpace demand through 2030, with supply growth of 1.8 mb/d in 2025 versus demand growth of just 700,000 b/d, creating potential for stable pricing and operational flexibility.

- Australian unconventional gas advancements continues as Beetaloo Energy completed the longest fracture stimulation in the Beetaloo Basin (2,955 meters, 67 stages), while Elixir Energy launched a three-phase strategic plan targeting 2P reserves conversion and production by late 2027 in Queensland's Taroom Trough.

- Natural gas liquids driving growth: NGLs are emerging as a major supply driver, with output forecast to rise by 2 mb/d to 15.5 mb/d by 2030, supported by rising petrochemical feedstock demand and unconventional production growth.

The global oil & gas sector presents compelling investment opportunities despite recent market volatility, as major operators demonstrate enhanced capital discipline while positioning for long-term energy transition participation. Current market dynamics, characterized by supply-demand imbalances and strategic corporate transformations, create attractive entry points for investors seeking exposure to essential energy infrastructure and cash-generative assets.

Oil Market Fundamentals & Pricing Dynamics

The oil & gas market has experienced significant volatility throughout 2025, with Brent crude prices fluctuating between $57 and $75 per barrel during the second quarter alone. This volatility, driven by geopolitical tensions, trade policy uncertainties, and OPEC+ production decisions, has created both challenges and opportunities for sector participants.

The International Energy Agency projects global oil supply growth of 1.8 million barrels per day in 2025, substantially exceeding expected demand growth of 700,000 barrels per day, suggesting potential for market stabilization as excess supply provides a buffer against geopolitical shocks.

Natural gas markets have shown resilience, with prices recovering from early-year lows as seasonal demand patterns and infrastructure constraints provided support. The sector benefits from structural changes in global energy consumption, particularly the transition from coal to natural gas in power generation and the growing importance of liquefied natural gas in international trade. Natural gas liquids represent a particularly attractive growth segment, with global oil production capacity forecasted to rise by more than 5 million barrels per day to 114.7 mb/d by 2030 driven by rising petrochemical feedstock demand.

Recent market conditions have impacted merger and acquisition activity, with US upstream dealmaking declining 60% in the first half of 2025 to $30.5 billion compared to the same period in 2024.

"Volatility in commodity and equity markets raised a major yellow flag for M&A, slowing the pace of dealmaking. That added an additional barrier to a market that was already challenged by the lack of remaining attractive opportunities for public E&Ps, especially in the Perman Basin" - Andrew Dittmar, Principal Analyst at Enverus Intelligence Research

However, this reduction in acquisition activity may benefit existing operators by reducing competition for assets and potentially creating value opportunities for well-positioned companies.

Operational Efficiency and Cost Management

Leading oil & gas operators have demonstrated significant improvements in operational efficiency and cost management, creating sustainable competitive advantages.

Shell has streamlined its operational focus from over 70 targets to eight key metrics, contributing to structural cost reductions with targeted operational expenditure savings of $5-8 billion between 2022 and 2028. The company's upstream expansion plans with over one million barrels per day of additional production capacity planned through 2030 at an average breakeven cost of $35 per barrel provides resilience against oil price volatility while maintaining attractive margins across various price scenarios. The focus on deep-water assets that produce lower CO2 emission barrels aligns with environmental considerations while maintaining commercial viability.

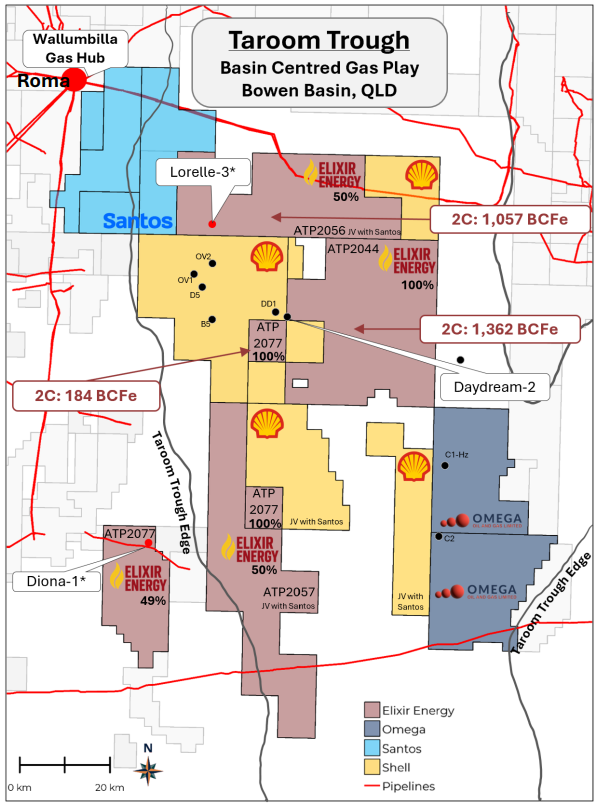

Infrastructure advantages play a crucial role in operational efficiency, particularly in emerging unconventional gas regions. Australian unconventional gas development represents a significant growth opportunity, with recent technical achievements demonstrating commercial viability.

The Taroom Trough in Queensland, where multiple operators including Shell and Elixir Energy are active, benefits from proximity to the Wallumbilla Gas Hub and established pipeline infrastructure. This positioning provides direct access to critically undersupplied East Coast energy markets and approximately 25 million tonnes per annum of LNG liquefaction capacity, reducing development costs and time-to-market for new projects.

Elixir Energy launched a three-phase strategic plans to secure the long-term retention of its highly prospective Taroom Trough acreage. The company holds over 2,000 square kilometers of prospective acreage. The company capitalizes nearby developments and ongoing investment activity to accelerate its own progress, aiming to commence gas production and convert over 150 billion cubic feet of contingent resources into proven and probable reserves by the end of 2027.

Meanwhile, Beetaloo Energy (formerly Empire Energy) successfully completed hydraulic stimulation of its Carpentaria-5H well, achieving the longest fracture stimulation in the Beetaloo Basin with 2,955 meters of horizontal length across 67 stages. In a company release, Managing Director of Beetaloo Energy Alex Underwood emphasized the significance of this achievement:

"The stimulation of Carpentaria-5H over a 2,955 metre horizontal section with 67 stages successfully placed is the longest fracture stimulation completed in the Beetaloo Basin. This is a historic event for Beetaloo Energy Australia and for the basin."

The technical success included achieving pump rates exceeding 100 barrels per minute on multiple stages and completing the first 24-hour stimulation operation for Beetaloo Energy, with more than five stages per day achieved on multiple days during the campaign. These operational achievements demonstrate the commercial scalability of unconventional gas development in the region, with flow testing results expected by the end of September providing crucial data for resource evaluation.

Commercial Realism on Energy Transition

While U.S. tariffs and the blurry sanctions on Russia are still on heat, strong cash flow generation capabilities position leading oil & gas operators to deliver attractive shareholder returns while maintaining investment flexibility. Shell's diversified business model, incorporating substantial downstream and trading operations that operate largely independently of oil price fluctuations, provides more resilience to price volatility compared to upstream-focused peers.

According to the IEA Oil Market Report (OMR),

"US gas liquids inventories rose by 79 mb in 2Q25, buoyed by robust US NGL supply and lower exports due to a temporary export license requirement for ethane."

"China’s new policies aimed at improving its energy security are positioning oil companies as long-term strategic storage partners for the government, effectively removing these volumes from the global market."

The sector's enhanced capital discipline, demonstrated through improved project selection criteria and operational efficiency initiatives, addresses historical performance issues that previously justified valuation discounts. Shell's historical challenges with capital allocation, including approximately $45 billion in capital employed generating poor or negative returns, have been addressed through enhanced discipline and internal competition for investment resources.

The integration of traditional oil & gas operations with energy transition technologies creates optionality for operators to participate in emerging markets as they become commercially viable. Shell's global retail network of approximately 45,000 service stations provides infrastructure for electric vehicle charging deployment, leveraging existing customer relationships while adapting to changing mobility patterns. The company has observed that EV customers tend to have higher wallet sizes per visit, partially offsetting different usage patterns compared to traditional fuel customers.

The sector's approach to energy transition emphasizes commercial viability over ideological positioning, creating sustainable pathways for traditional operators to participate in evolving energy markets.

The Investment Thesis for Oil & Gas

- Enhanced Capital Discipline Creates Value: Leading operators have implemented rigorous return thresholds (10-15% IRR requirements) and streamlined operations, with Shell reducing focus from 70+ targets to 8 key metrics while targeting $5-8 billion in structural cost savings through 2028.

- Supply-Demand Fundamentals Support Pricing: Global oil supply growth of 1.8 mb/d versus demand growth of 700,000 b/d in 2025 creates potential market surplus, providing pricing stability and operational flexibility for disciplined producers with low-cost asset bases.

- Natural Gas Liquids Offer Premium Growth: NGLs production forecast to grow 2 mb/d to 15.5 mb/d by 2030, driven by petrochemical feedstock demand, with Asia accounting for 65% of LPG demand growth led by China and India.

- Unconventional Resources Demonstrate Commercial Viability: Recent technical achievements in Australian basins, including Beetaloo Energy's record 2,955-meter stimulation and Elixir Energy's 2.6 TCFe of contingent resources, validate commercial potential in infrastructure-advantaged regions.

- Integrated Business Models Provide Defensive Characteristics: Companies with downstream, trading, and retail operations (like Shell's 45,000 service stations) offer oil price resilience while maintaining upside exposure and transition optionality.

- Aggressive Shareholder Return Programs: Shell's 14 consecutive quarters of $3+ billion buybacks reducing share count by 22%, with potential for 50% total reduction, demonstrates cash flow strength and management commitment to shareholder value.

- Strategic Positioning for Energy Transition: Commercial realism approach requiring competitive returns on low-carbon investments ensures sustainable participation in evolving energy markets without sacrificing current cash flows.

- Reduced M&A Competition Creates Opportunities: 60% decline in US upstream dealmaking to $30.5 billion in H1 2025 reduces asset competition while potentially creating acquisition opportunities for well-capitalized operators.

The oil & gas sector presents compelling investment opportunities through a combination of enhanced operational discipline, favorable supply-demand dynamics, and strategic positioning for energy transition participation. Leading operators have demonstrated significant improvements in capital allocation, operational efficiency, and shareholder return programs while maintaining commercial viability across commodity price cycles.

Recent technical achievements in unconventional resource development, particularly in infrastructure-advantaged regions like Australia's gas basins, validate the commercial potential of new supply sources. While market volatility has reduced M&A activity and created valuation opportunities, the sector's focus on competitive advantages and disciplined execution suggests sustainable pathways for value creation. Investors seeking exposure to essential energy infrastructure, attractive cash yields, and optionality in evolving energy markets should consider the sector's current strategic positioning and operational improvements as compelling reasons for allocation.

References:

- International Energy Agency Oil Market Report (OMR) - July 2025

- Mccartney, G. (July 2025). Reuters Dealmaking in US Upstream Oil and Gas Tumbles as Volatility Rattles Investors

- Lawler, A. (July 2025). Reuter World Oil Market May Be Tighter Than It Looks, IEA Says

Analyst's Notes

Subscribe to Our Channel

Stay Informed