One Month Into Tariffs: How Nickel Supply Chains & Investor Sentiment Have Shifted

U.S. tariffs reshape nickel supply chains as investors pivot to secure jurisdictions. Class 1 premiums widen while Canada emerges as strategic alternative.

- U.S. tariffs of 25%-40% on metal imports from over 150 countries, effective August 1, 2025, have disrupted nickel supply chains and reshaped trade flows

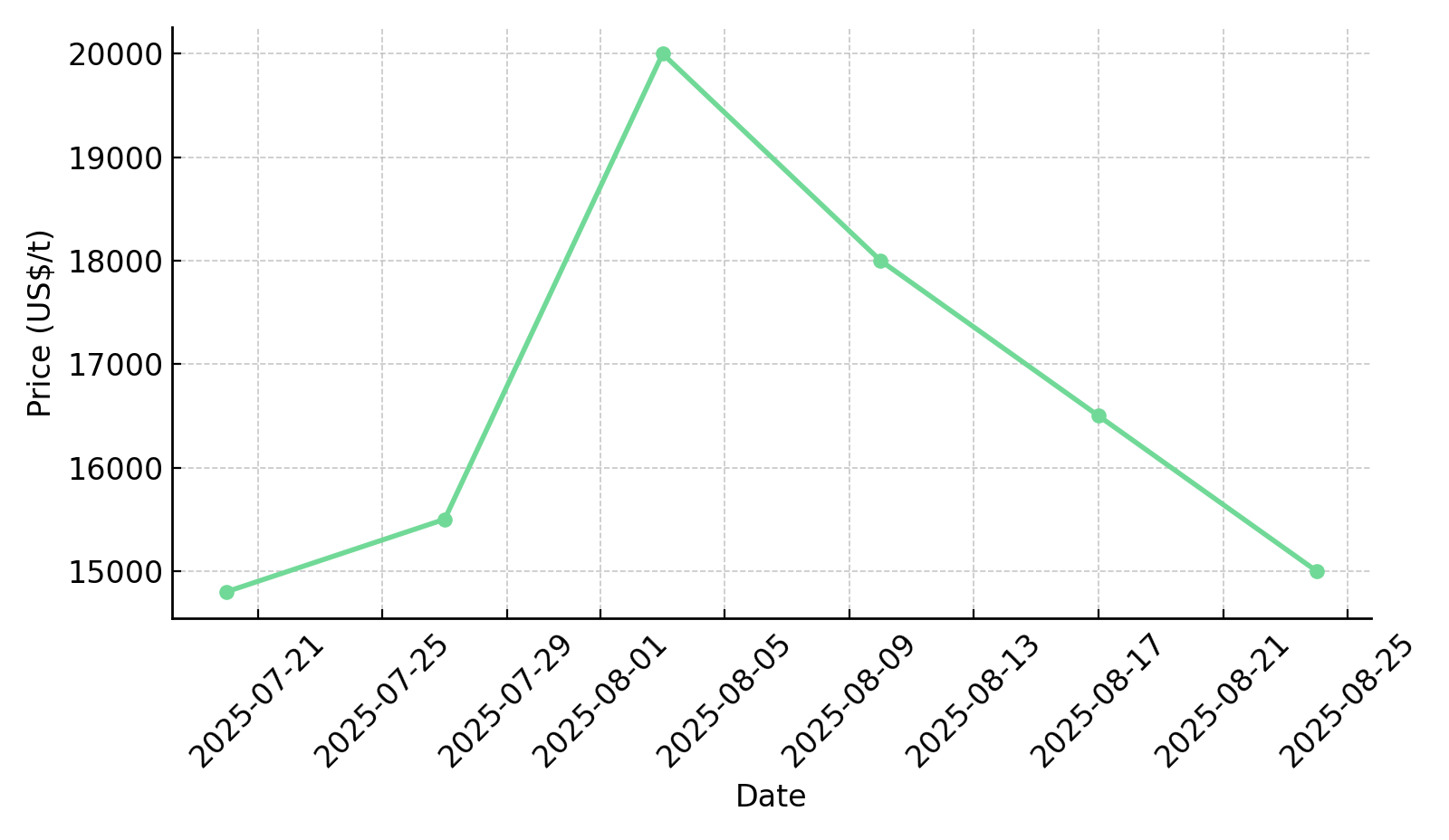

- Nickel prices fell back to approximately US$15,000/t after a brief rebound, pressuring global producers while strengthening demand for Class 1 material

- Producers in Indonesia, Russia, and the Philippines face uncertain export pathways, while China accelerates stockpiling and BRICS explore alternative trade frameworks

- Investors are rotating into jurisdictionally secure, ESG-compliant projects in North America and Australia, with Canada Nickel's Crawford Project emerging as a benchmark

- The next 6-12 months will test whether tariffs accelerate strategic decoupling or collapse under negotiation pressure, but the investment case for secure, low-carbon nickel is strengthening

Shock & Policy Scope

The implementation of comprehensive U.S. metal tariffs on August 1, 2025, represents the most significant trade policy shift in critical minerals since the 1971 Nixon Shock. The tariff structure imposes rates of 25%-40% on nickel imports from over 150 countries, with the highest rates targeting primary producers in Indonesia, Russia, and the Philippines. The policy framework includes a 90-day negotiation window that allows for potential rate adjustments, though early diplomatic signals suggest limited appetite for compromise from either side.

The tariff implementation aligns with broader U.S. strategic objectives outlined in the National Defense Authorization Act and the CHIPS and Science Act, prioritizing domestic critical minerals security and reducing dependence on adversarial nations. Legal challenges through the World Trade Organization have been filed by affected countries, though precedent suggests resolution timelines extending well beyond the immediate market impact period.

The scope extends beyond simple trade protection, incorporating national security determinations that classify nickel as a critical defense material. This designation enables the administration to invoke emergency powers under Section 232 of the Trade Expansion Act, providing legal cover for sustained implementation despite WTO challenges. Treasury officials have emphasized that the policy represents a fundamental shift toward economic security rather than traditional trade balance considerations.

Administrative complexity has emerged as tariffs are applied selectively based on origin classification, purity grades, and end-use applications. Class 1 nickel faces different treatment than nickel pig iron, creating arbitrage opportunities and supply chain distortions that market participants are still navigating.

Market Reaction & Price Signals

Nickel futures experienced immediate volatility following the tariff announcement, with London Metal Exchange contracts initially surging to US$20,000/t before retracing to approximately US$15,000/t by late August. This price action reflects the market's struggle to price both supply disruption risks and demand destruction from higher input costs.

Dollar strength has compounded pricing pressure, with the Federal Reserve's latest policy stance showing inflation persistence at 2.7% headline and 2.9% core Consumer Price Index readings. Market expectations for rate cuts have shifted from 65% probability to 58%, supporting continued dollar strength that pressures commodity prices denominated in the currency.

The spread between Class 1 nickel and Class 2 nickel pig iron has widened significantly, reflecting quality premiums as battery manufacturers prioritize supply security over cost optimization. London Metal Exchange Class 1 premiums now trade at US$800-1,200/t above Shanghai Futures Exchange nickel pig iron contracts, compared to historical spreads of US$300-500/t.

Volatility indicators suggest sustained uncertainty, with implied volatility on three-month LME nickel options reaching levels not seen since the Russian invasion of Ukraine in 2022. This elevated volatility environment has prompted many mining companies to reassess production decisions, with industry analysts estimating that over 50% of global nickel output becomes uneconomic at sustained prices below US$15,000/t.

Trading volumes have increased 40% above seasonal averages as market participants reposition portfolios and hedge exposure to ongoing policy uncertainty. The disconnect between physical and financial markets has widened, with spot premiums for immediate delivery reaching US$200-300/t above futures contracts.

Supply Chain Disruptions & Adjustments

U.S. manufacturers have initiated emergency procurement protocols to secure alternative nickel supply sources, with Canada and Australia emerging as preferred origins despite significantly higher freight costs and longer lead times. Battery manufacturers report procurement teams working around-the-clock to renegotiate contracts and establish new supply relationships ahead of potential further policy escalation.

Stockpiling activity ahead of the August 1 tariff deadline created artificial demand spikes that distorted normal trading patterns through July. Import data shows nickel imports increased 340% month-over-month in July as buyers accelerated shipments to avoid tariff exposure, followed by a sharp contraction in August as inventories normalized.

Freight and insurance costs have increased substantially for alternative routing, with shipping rates from Australian ports to U.S. destinations increasing 25-30% due to vessel scarcity and extended voyage times. Insurance premiums for nickel shipments have risen 15-20% as underwriters price political and operational risks associated with supply chain realignment.

China has responded by doubling Class 1 nickel reserve accumulation through state-owned enterprises, signaling long-term strategic positioning rather than short-term arbitrage. Chinese stainless steel producers report securing six-month forward contracts at advantageous pricing, potentially creating supply constraints for Western markets as Chinese buyers lock in available material.

Substitution accelerations are becoming evident across end-use applications, with lithium iron phosphate battery adoption increasing in China as manufacturers reduce nickel intensity. Recycling capacity utilization has increased to near-maximum levels as processors prioritize secondary nickel recovery to offset primary supply constraints.

Producer & Exporter Responses

Indonesia has implemented several policy adjustments that signal confidence in maintaining market influence despite tariff pressure. The government shortened export quota periods from three years to one year, undermining long-term investment certainty while maintaining operational flexibility. Despite official production cuts announced in June, Indonesian smelters continue operating at near-full capacity, suggesting political rhetoric differs from operational reality.

The Philippines has emerged as a relative beneficiary of Indonesian supply tightening, with ore export volumes increasing 15% month-over-month as buyers seek alternative feedstock sources. Philippine nickel ore prices have reached levels not seen since October 2023, providing windfall profits for local producers while creating input cost pressures for Chinese smelters.

Russian producer Nornickel has maintained confidence in its ability to sell output despite sanctions and tariffs, with management emphasizing reorientation toward Chinese and Indian markets. The company's substantial cash position and low-cost production profile provide operational flexibility during market disruption, though access to Western technology and services remains constrained.

The August BRICS Summit in Kazan produced the Rio Declaration emphasizing alternative trade frameworks and local currency settlements for commodity transactions. While lacking immediate operational impact, the declaration signals coordinated policy development aimed at reducing dollar dependence in critical minerals trade. Mark Selby, Chief Executive Officer of Canada Nickel, noted the macroeconomic shift:

"Nickel's been out of favor here for the last couple years but this is a pivot year where Indonesia is going to become supportive to the nickel market as opposed to having a negative impact on the market as it flexes its muscle as the OPEC of nickel."

Investor Sentiment & Capital Flows

Institutional capital allocation has shifted markedly toward jurisdictionally secure nickel assets, with hedge funds reducing exposure to volatile Class 2 supply chains in favor of Class 1 projects in allied jurisdictions. Fund managers report increased due diligence focus on permitting certainty, ESG compliance, and long-term supply security rather than traditional cost-curve positioning.

Private equity and sovereign wealth funds have accelerated evaluation timelines for North American and Australian nickel projects, with several funds establishing dedicated critical minerals strategies. The jurisdictional premium for secure supply has created equity re-rating potential for companies demonstrating low All-In Sustaining Costs, robust Internal Rate of Return and Net Present Value metrics, and clear permitting pathways.

ESG-compliant projects are commanding valuation premiums as institutional investors prioritize carbon-neutral production methods and community engagement standards. This trend particularly benefits projects incorporating carbon capture technologies or demonstrating negative carbon footprints through innovative processing methods.

Risk-off sentiment has pressured near-term exploration and development funding, though strategic investors are demonstrating increased willingness to fund late-stage projects with proven economics and secure jurisdiction positioning. Debt markets remain accessible for projects with strong credit profiles and government backing, though terms have tightened and due diligence periods extended.

A leading fund manager specializing in critical minerals commented: "The tariff environment has fundamentally altered risk-return calculations. Investors are willing to accept higher development costs in exchange for supply security and regulatory predictability."

Canada Nickel & the Jurisdictional Premium

Canada Nickel's Crawford Project exemplifies the strategic positioning that institutional investors increasingly prioritize in the current policy environment. The project represents the second-largest global nickel reserve and resource base while unlocking the broader Timmins Nickel District potential.

Tier-1 Asset Quality & Scale

The Crawford Project anchors what may become the world's largest nickel sulfide district, with nine separate resources planned for publication by year-end. The scale advantage provides operational flexibility and capital efficiency that smaller, standalone projects cannot match. Man West deposit alone delivered initial resources exceeding one billion tons containing two million tons of nickel and nearly one million ounces of platinum group metals.

Crawford's sulfide resource base supports Class 1 nickel production specifically designed for battery applications, avoiding the purity challenges that affect nickel pig iron products. The resource quality enables selective mining approaches that optimize grade and recovery while minimizing environmental impact.

Economics & Scarcity Value

Front-End Engineering Design results demonstrate robust project economics with US$2.8 billion Net Present Value, 17.6% Internal Rate of Return, and C1 costs of US$0.68/lb with All-In Sustaining Costs of US$1.54/lb. These metrics position Crawford in the bottom quartile of the global cost curve while delivering premium pricing for Class 1 output.

Carbon-negative production through IPT Carbonation technology enables annual sequestration of 1.5 million tons of CO₂, creating additional revenue streams through carbon credit markets while addressing regulatory requirements for low-carbon production.

Strategic Positioning

NetZero Metals development represents North America's largest planned nickel processing hub, positioning Canada Nickel to benefit from Inflation Reduction Act incentives and European Union Critical Raw Materials Act preferences. The integrated approach reduces transportation costs and processing risks while maximizing value capture across the supply chain.

Institutional support includes strategic partnerships with Agnico Eagle, Samsung SDI, Anglo American, and Export Development Canada letter of intent backing. This diversified support base provides both financial backing and offtake security for long-term production planning. Mark Selby emphasized the financing strategy:

"For that billion dollar project level investment we qualify for $600 million in refundable tax credits from the government for carbon capture and for critical minerals so that's 60 cents of that dollar of equity that we need."

Forward-Looking Risks & Opportunities

Legal challenges through the World Trade Organization present the primary risk to tariff sustainability, though precedent suggests resolution timelines extending 18-24 months. Political risks include potential policy reversal following electoral cycles, though bipartisan support for critical minerals security suggests sustained commitment regardless of administration changes.

Expiring U.S. electric vehicle tax credits combined with proposed policies may create short-term demand disruption as consumers delay purchases pending policy clarity. However, medium-term electrification trends remain intact with 12-20% compound annual growth rates projected through 2030.

Tariff-induced cost increases may raise electric vehicle battery costs 3-7%, testing price parity assumptions with internal combustion engines. This dynamic could temporarily slow adoption rates while manufacturers absorb costs or pass them through to consumers.

Strategic Investment & Infrastructure Development

Long-term opportunities include accelerated investment in domestic and allied nickel supply sources, supported by government incentives and strategic partnerships. The Inflation Reduction Act and European Union Critical Raw Materials Act provide sustained policy support for jurisdictionally secure supply development.

Infrastructure investment in North American processing capacity may create lasting competitive advantages as supply chains regionalize around security rather than cost optimization. This trend particularly benefits integrated producers with both mining and processing capabilities.

The Investment Thesis for Nickel

- Jurisdictional premium positioning strengthens as secure supply in Canada and Australia gains strategic value while Indonesia and Russia face sustained trade barriers and political risk

- Structural demand growth from electric vehicle adoption and grid storage expansion ensures long-term Class 1 nickel consumption increases despite short-term price volatility

- Capital flow redirection toward projects demonstrating low cost curves, robust Internal Rate of Return and Net Present Value metrics, and comprehensive ESG compliance creates sustained valuation support

- Policy framework alignment through Inflation Reduction Act and European Union frameworks incentivizes allied sourcing while creating enduring demand preferences for North American and Australian supply

- Contrarian opportunity emerges from depressed nickel prices and broader market sentiment toward base metals creating attractive entry points for forward-looking institutional capital

- Operational advantages accrue to integrated producers with both mining and processing capabilities as supply chains prioritize security over traditional cost optimization

- Environmental differentiation through carbon-negative production technologies creates additional revenue streams while meeting increasingly stringent regulatory requirements for low-carbon supply chains

Tariffs as a Gamechanger for Strategic Repricing

One month into comprehensive U.S. metal tariffs, market participants have moved beyond initial price volatility toward fundamental reassessment of supply chain security and jurisdictional risk. The policy framework has accelerated investor recognition that traditional cost-curve analysis inadequately captures political and regulatory risks in critical minerals markets.

For institutional investors, the near-term pressure from depressed nickel prices obscures the strategic opportunity in secure, ESG-aligned assets positioned for long-term electrification demand. The tariff environment has permanently altered risk-return calculations, creating sustained premiums for projects demonstrating jurisdictional security, operational flexibility, and environmental compliance.

Canada Nickel and similarly positioned North American and Australian projects have emerged as central beneficiaries of this strategic repricing, offering institutional investors exposure to critical minerals growth while minimizing political and regulatory risks that increasingly define market outcomes in the evolving trade environment.

Analyst's Notes

Subscribe to Our Channel

Stay Informed