Stable Rutile Prices & Jurisdictional Premium: Why Sovereign Metals’ Kasiya Matters Now

Rutile prices hold at $1,825/t amid African mine closures and Australian suspensions. Malawi's Kasiya project offers low-cost, dual-commodity exposure in stable jurisdiction.

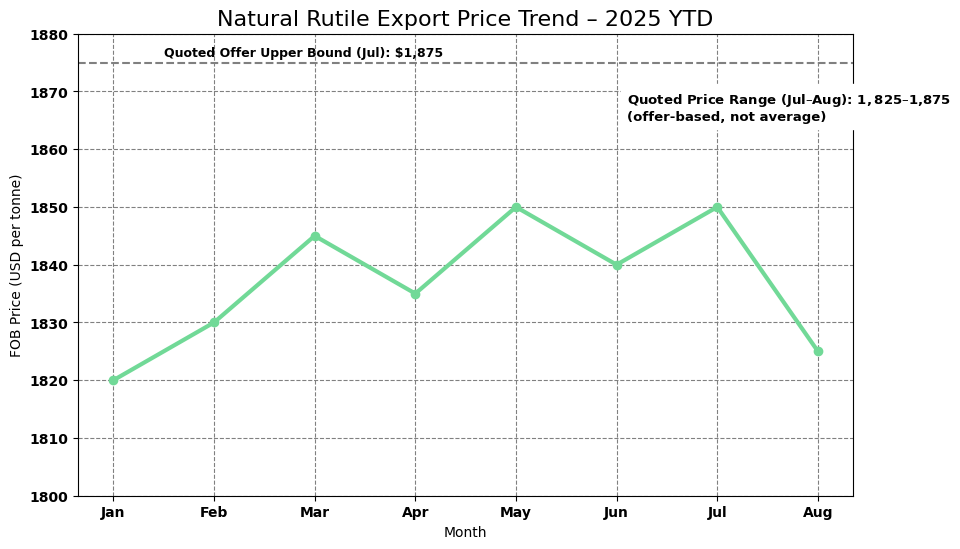

- Rutile export prices remain anchored in a $1,825–1,900/t band in late 2025, reflecting constrained natural supply rather than demand weakness.

- African legacy supply closures, including Base Resources' Kwale shutdown, and regulatory hurdles in Australia raise the scarcity premium for projects in stable jurisdictions.

- Trade policy shifts, especially Chinese output cuts and tariffs on synthetic graphite, intensify investor focus on ex-China critical mineral projects.

- Sovereign Metals' Kasiya project exemplifies the type of low-cost, stable, ESG-aligned project likely to attract premium investor valuation.

- Kasiya's definitive feasibility study in Q4 2025, offtake or financing deals, and evolving export and trade regulation out of China and Africa.

Price Stability Signals Supply Constraint, Not Demand Strength

Rutile export prices remain anchored near $1,825 per tonne FOB in mid-August 2025, with July export quotes ranging between $1,825 and $1,875 per tonne in Chinese sourcing reports. This stability occurs despite weak downstream titanium dioxide and pigment volumes globally, suggesting that price firmness reflects supply constraints rather than robust end-use demand. Rutile serves as the primary feedstock for titanium dioxide production, which accounts for approximately 95% of global titanium consumption across pigments, aerospace alloys, and defense applications.

The rutile market operates with limited transparency following the discontinuation of reliable pricing indices. Bilateral contracts and opaque spot trades now dominate price discovery, creating information asymmetries that favor established suppliers with long-term relationships. This pricing environment rewards projects capable of securing anchor offtake agreements and demonstrates resilience in contract negotiations.

The stability in natural rutile pricing should not be mistaken for oversupply, particularly given weak downstream titanium dioxide and pigment volumes globally. Instead, the price floor reflects structural tightness in natural rutile supply chains, where production curtailments and mine closures have removed significant capacity from the market. The current pricing dynamic signals that natural rutile maintains value support even during periods of industrial demand softness, positioning well-capitalized projects to capture margin expansion when end-use markets recover.

Legacy Mine Depletion Meets Regulatory Headwinds in Core Provinces

Natural rutile supply faces mounting pressure from the depletion of legacy African deposits and operational suspensions in Australia. Base Resources' Kwale mine in Kenya closed in 2024, withdrawing approximately 90,000 tonnes per annum of natural rutile from the global supply pool. Other aging African operations face declining ore grades, deeper mining benches, and rising strip ratios that limit economic expansion. These constraints reflect the maturity of established rutile provinces and the difficulty of replacing depleted tonnage with new discoveries.

Australian supply dynamics add further complexity to the global balance. Iluka Resources announced the suspension of its Cataby mine for approximately 12 months and halted its Synthetic Rutile Kiln SR2 for roughly six months starting December 1, 2025. Iluka cited weak demand, low downstream orders, and uncertain forecasting as drivers for these suspensions. While these actions respond to near-term demand conditions, they also highlight the sensitivity of high-cost producers to margin compression and the extended lead times required to restart idled capacity.

The combined effect of African mine depletion and Australian operational flexibility creates a bifurcated supply landscape. Fewer new entrants, longer permitting windows, and the exhaustion of easily extractable orebodies elevate the strategic premium for secure, scalable assets in stable jurisdictions. Projects capable of delivering large-scale, low-cost production over multi-decade mine lives command growing investor attention as replacement supply becomes increasingly scarce.

Chinese Production Discipline & Trade Policy Create Ex-China Premiums

Chinese titanium dioxide producers have implemented production cuts to defend margins amid weak global demand, with monthly contractions including a 1.06% month-over-month decline in July 2025. These volume adjustments demonstrate disciplined supply management rather than market flooding, supporting price stability in both domestic and export markets. In August 2025, Chinese producers increased domestic rutile and anatase prices by RMB 800 per tonne, with export prices rising by $80 per tonne, signaling coordinated efforts to protect profitability.

Broader trade policy shifts reinforce investor preference for ex-China supply chains in strategic minerals. The United States, European Union, and Australia have implemented or expanded tariff structures favoring domestic and allied-nation sourcing. The synthetic graphite sector provides a relevant analog, where 93.5% anti-dumping tariffs on Chinese imports have created supply bifurcation that benefits producers in transparent jurisdictions. Similar policy frameworks for titanium feedstocks and battery materials are under active consideration across multiple jurisdictions.

These policy dynamics create structural incentives for offtakers and end users to diversify supply away from concentrated sources. Projects in countries with stable mining codes, transparent environmental regulation, and established infrastructure access benefit from reduced counterparty risk premiums. This translates into improved contract terms, higher willingness-to-pay from strategic buyers, and enhanced project valuations relative to geopolitically exposed alternatives.

Industrial Recovery Trajectories Support Multi-Year Demand Base

Recent upgrades to gross domestic product forecasts for major economies including the United States, India, United Kingdom, and Brazil support medium-term industrial and infrastructure expansion. These revisions reflect improved fiscal positions, ongoing energy transition investments, and post-pandemic normalization in manufacturing sectors. A modest weakening of the US dollar expected in late 2025 and into 2026 would benefit commodity exporters by improving margins for non-dollar-denominated cost structures and enhancing purchasing power for global importers.

Rutile demand drivers remain concentrated in aerospace, defense titanium metal production, and specialty pigments for medical and electronics applications. These end uses demonstrate resilience to economic cycles and benefit from secular trends including defense modernization, commercial aircraft production recovery, and advanced manufacturing expansion. While short-term volatility in industrial activity creates pricing fluctuations, the underlying demand profile for high-purity titanium dioxide feedstocks remains structurally supported.

For graphite, battery and electric vehicle demand tailwinds persist despite near-term inventory adjustments in the automotive sector. Energy storage deployments, grid-scale battery projects, and diversification of battery supply chains underpin multi-year growth trajectories. Investors should view stable end-use demand across both rutile and graphite markets as providing downside protection during commodity price cycles, particularly for projects offering dual commodity exposure with differentiated cost positions.

Opaque Markets Reward Scale & Supply Reliability Over Spot Optimization

The absence of transparent benchmark pricing for natural rutile has fundamentally altered contract structures and risk allocation between producers and consumers. Bilateral negotiations dominate price discovery, with contracts often incorporating complex formulas, volume commitments, and quality specifications that remain confidential. This opacity widens bid-ask spreads during periods of market uncertainty and increases the value of long-term supply relationships.

Buyers increasingly demand supply assurance through extended contract durations, take-or-pay provisions, and prepayment structures. Traditional hedging mechanisms available in more liquid commodity markets remain largely inaccessible for rutile, forcing end users to accept price floors, collars, or fixed-price arrangements over multi-year periods. These contract structures transfer price risk but provide volume certainty, creating natural advantages for projects capable of demonstrating production reliability.

Projects in stable jurisdictions with established infrastructure and transparent regulatory frameworks can negotiate premium pricing or more favorable contract terms. The scale, geological simplicity, and processing advantages of large deposits enable producers to offer volume certainty and product consistency that command higher values in bilateral negotiations. As supply constraints tighten and offtakers prioritize security over spot price optimization, this contract premium environment favors well-capitalized projects with clear execution pathways.

Kasiya: Where Geology, Economics & Partnership Meet

The Kasiya project in Malawi represents a convergent set of attributes that align with evolving investor preferences for critical mineral projects. Sovereign Metals discovered the deposit in 2018, and subsequent exploration has defined it as the largest rutile deposit ever discovered and the second-largest natural graphite deposit globally. The mineralization covers over 200 square kilometers and occurs as blanket-style mineralization, providing scalability advantages relative to structurally complex or narrow-vein deposits.

Rio Tinto established a strategic partnership with Sovereign Metals in mid-2023, ultimately investing A$60 million to acquire a 19.9% shareholding. The project is now overseen by a joint Sovereign-Rio technical committee, with Rio Tinto subject matter experts providing engineering, metallurgical, and development support. This partnership provides validation of the project's technical merit and offers access to Rio Tinto's global supply chain relationships and project execution capabilities. Ben Stoikovich, Chairman of Sovereign Metals, underscores the strategic significance of this alliance:

"Rio Tinto is a 19.9% shareholder in Sovereign and a strategic partner in the Kasiya project."

Weathered Saprolite Geology Eliminates Conventional Mining Costs

Kasiya hosts 17.9 million tonnes of contained rutile and 24.4 million tonnes of flake graphite within weathered saprolite material. This geological setting eliminates the need for drill-blast-crush-grind processing sequences typical of fresh rock deposits, enabling simpler metallurgical circuits with lower capital and operating costs. The soft, friable ore allows for free-dig extraction, reducing mining equipment requirements and energy consumption.

The weathered nature of the ore preserves flake size distribution, with approximately 70% of graphite production falling into medium, large, and jumbo flake categories that command prices up to $1,200 per tonne. Low sulfur content below 0.02% enhances suitability for battery anode applications, where high sulfur levels create processing challenges and impurity concerns. Test work has demonstrated product suitability for 94% of graphite end uses, including the higher-value refractories and expandables markets. Stoikovich articulates how the geological advantages translate into processing economics:

"The Kasiya deposit occurs as blanket-style mineralization hosted in a soft, friable saprolite. The ore is free dig and has very low levels of sulfur."

Byproduct Cost Allocation Delivers Bottom-Quartile Global Position

The optimized pre-feasibility study completed in January 2025 reported a pre-tax net present value of $2.3 billion at an 8% discount rate, with an internal rate of return of 27% and annual average earnings before interest, taxes, depreciation, and amortization of over $400 million. Operating margins of 64% reflect the dual revenue streams from rutile and graphite, with the project structured to treat rutile as the primary product and graphite as a byproduct.

This product hierarchy creates favorable cost allocation dynamics. The incremental cost to produce graphite as a byproduct is approximately $241 per tonne FOB, comparing favorably to China's weighted average C1 cost near $257 per tonne. This cost positioning enables Kasiya to maintain profitability across a wide range of graphite price scenarios, including during periods of Chinese production expansion or global oversupply.

The byproduct cost structure positions Kasiya at the bottom end of the global graphite cost curve, enabling the project to compete effectively even in challenging market conditions. Ben Stoikovich quantifies the competitive advantage:

"Our incremental cost to produce a tonne of graphite as a byproduct from the Kasiya project will only be $241 US per tonne… Kasiya is right at the bottom end of the global cost curve and we'll always be able to sell graphite into the market at healthy margins."

DFS Completion & Offtake Negotiations Define Near-Term Value Path

The joint Sovereign-Rio technical team is advancing the definitive feasibility study for completion in Q4 2025. Pilot testing has validated processing flows and confirmed concentrate grades of 96-98% carbon for graphite and high-purity specifications for rutile. The project benefits from established logistics infrastructure through the Nacala railway and port corridor, reducing transportation costs and providing access to Asian and European markets. Ben Stoikovich outlines the development timeline:

"The joint Sovereign-Rio team is now cracking on with a definitive feasibility study, which we aim to complete during Q4 this year."

Key execution risks include permitting timelines within Malawi's regulatory framework, social license maintenance across a large operational footprint, and currency volatility in the Malawian kwacha. However, Malawi's established mining sector, transparent licensing processes, and government support for large-scale mining projects mitigate some jurisdictional concerns. Offtake negotiations and project financing represent critical near-term milestones that will determine development timelines and capital structure.

The opaque nature of rutile and graphite markets creates challenges in contract negotiations, though Kasiya's scale provides leverage in discussions with strategic buyers. Foundation customer agreements that provide volume commitments and pricing certainty will be essential to advancing project financing and construction decisions. Sensitivity to global titanium dioxide demand cycles and potential Chinese policy reversals remain external factors beyond management control.

Vertical Integration & ESG Standards Reshape Valuation Frameworks

Vertical integration trends in the graphite supply chain, where battery manufacturers and automakers acquire or invest directly in mining projects, compress demand for spot market graphite. This dynamic makes primary graphite producers in stable jurisdictions more attractive to independent buyers seeking reliable supply outside captive chains. Similarly, synthetic rutile production, which grows at approximately 3-4% compound annual growth rate, provides substitutability upside but requires higher energy inputs and generates elevated carbon dioxide emissions relative to natural rutile.

Environmental, social, and governance metrics increasingly influence project valuations as end users face regulatory requirements and investor pressure to decarbonize supply chains. Low-carbon, low-impact mines in stable regimes command valuation premiums over projects with higher environmental footprints or uncertain permitting trajectories. This trend favors deposits with simple metallurgy, established infrastructure access, and transparent stakeholder engagement frameworks.

Jurisdictional risk has evolved from a secondary consideration to a primary valuation input. Investors systematically discount projects in countries with opaque licensing processes, corruption concerns, or histories of resource nationalism. The premium for de-risked, scalable projects should widen over 2026-2028 as supply gaps emerge and offtakers prioritize security over marginal cost advantages. This structural shift benefits projects like Kasiya that combine scale, cost competitiveness, and jurisdictional stability.

The Investment Thesis for Rutile & Graphite

- Rutile prices holding in the $1,825-1,900 per tonne band signal that structural supply constraints are anchoring value despite weak downstream demand, creating a floor for well-positioned producers.

- Jurisdictional stability in Malawi, combined with transparent mining regulation and established infrastructure, provides a competitive edge over projects facing permitting uncertainty or political risk.

- Dual commodity exposure to both rutile and graphite enables diversified revenue streams that reduce single-commodity price volatility and capture value across distinct end-use markets.

- Low-cost leadership positions Kasiya's incremental graphite cost of approximately $241 per tonne favorably against Chinese production benchmarks, ensuring margin resilience across price cycles.

- Scale and execution optionality from a world-class deposit size support tier-one production ambitions and provide negotiating leverage in offtake discussions and strategic partnership formations.

- Policy and trade tailwinds including ongoing export controls and supply security initiatives favor ex-China producers in transparent jurisdictions with established ESG frameworks.

- Catalyst-rich development pathway through the definitive feasibility study in Q4 2025, foundation offtake agreements, project financing, and potential premium contract structures creates multiple value inflection points over 12-24 months.

Strategic Minerals Enter the Supply Security Era

Rutile's seeming price stability in late 2025 masks deeper structural forces: supply attrition in legacy mines, regulatory friction in major suppliers, and rising scrutiny on critical mineral supply chains. In this context, jurisdictional security, ESG integrity, and scalable economics are no longer optional, they are primary value drivers commanding measurable premiums in project valuations and contract negotiations.

Malawi's Kasiya project highlights low cost, high scale, dual-commodity optionality, and stable execution in a de-risked regime. As markets bifurcate between high-risk and premium supply sources, projects demonstrating these attributes may command outsized valuations relative to peers with comparable resource endowments but elevated execution risks.

The next 12-24 months of definitive feasibility study execution, offtake negotiations, and trade policy developments will likely separate winners from the rest of the field. Rutile and graphite are no longer niche industrial minerals, they are strategic levers in the evolving global energy transition and supply security narrative, warranting systematic exposure in portfolios positioned for the critical minerals cycle.

Analyst's Notes

Subscribe to Our Channel

Stay Informed