Atlas Salt: De-Risking North America's Next Major Salt Mine as Supply Tightens

Atlas Salt advances North America's newest salt mine in 30 years with $920M NPV, strategic location, and de-risked development targeting import-dependent markets.

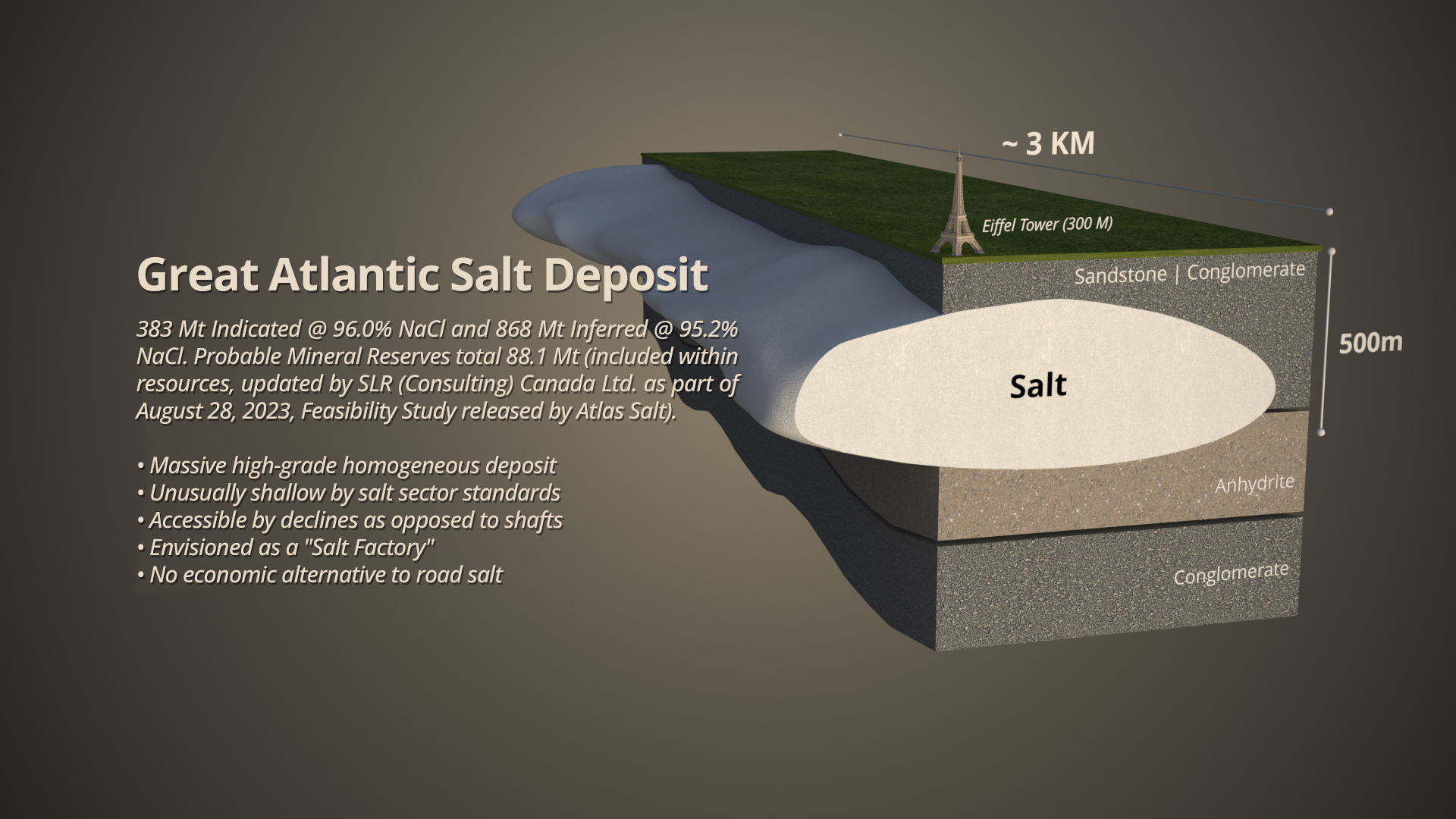

- Atlas Salt is developing the Great Atlantic Salt Project in Newfoundland, Canada, North America's first new salt mine in nearly three decades with 4 Mtpa nameplate production capacity targeting the import-dependent de-icing market.

- The 2025 Updated Feasibility Study demonstrates compelling economics: after-tax NPV8 of $920 million, 21.3% IRR, 4.2-year payback, and average annual post-tax cash flow of $188 million over a 24.3-year mine life.

- Strategic location in top-tier jurisdiction provides competitive advantages including proximity to 11-16 Mtpa Atlantic Canada and US East Coast market, lower transportation costs, clean hydropower access, and shallow mining depth reducing capital intensity.

- North American de-icing salt market valued at $2.3-2.9 billion annually faces 8-10 Mtpa import dependence, with legacy mines aging and recent closures removing domestic supply amid rising demand.

- Project de-risked through environmental assessment approval, strategic partnerships with Scotwood Industries (1.25-1.5 Mtpa offtake MOU) and Sandvik ($73 million equipment agreement), with production targeted by 2030.

Why Investors Should Consider Atlas Salt as North America's De-Icing Market Faces Supply Constraints

North America's reliance on imported salt for winter road maintenance has created a strategic opportunity for domestic producers as aging infrastructure and geopolitical supply chain pressures reshape the commodity landscape. Atlas Salt Inc. (TSXV:SALT) is positioned to capitalize on this market dynamic with its Great Atlantic Salt Project in Newfoundland, a world-class, high-grade deposit that represents the continent's first major new salt mine development in approximately 30 years.

The company's 2025 Updated Feasibility Study confirms robust project economics with an after-tax net present value of $920 million at an 8% discount rate, internal rate of return of 21.3%, and average life-of-mine annual post-tax cash flow of $188 million. With environmental approvals secured, strategic partnerships advancing, and a clean balance sheet supporting project development, Atlas Salt offers investors exposure to an essential industrial commodity with structural demand drivers and limited new supply competition.

The investment case extends beyond financial metrics to strategic positioning: the project's shallow depth (approximately 180 meters versus 600+ meters for legacy North American salt mines), proximity to import-dependent markets, and access to clean hydroelectric power create meaningful cost and sustainability advantages. As legacy salt mines face operational challenges and environmental scrutiny, with notable closures removing millions of tonnes of annual domestic supply, Atlas Salt's greenfield development addresses a genuine market need while offering institutional-grade economics.

Company Overview: Strategic Asset in Top-Tier Jurisdiction

Atlas Salt controls 2P Reserves of 95.0 million tonnes at 95.9% NaCl grade, representing one of North America's highest-purity salt deposits. The Great Atlantic Salt Project benefits from ideal geological characteristics: a homogeneous, shallow resource with average thickness of 200 meters (ranging 68-340 meters) accessible via decline mining rather than costly shaft sinking. This deposit geometry translates directly to capital efficiency and operational simplicity compared to traditional deep-shaft salt mining operations.

Newfoundland and Labrador's mining jurisdiction credentials strengthen the investment proposition. The province ranked 9th globally in Fraser Institute's 2025 mining investment attractiveness assessment based on mineral content and government policy alignment. Recent institutional capital flows into the region underscore its appeal: Equinox Gold's acquisition of Calibre Mining (owner of the Valentine Gold Project), Eldorado Gold's joint venture with Tru Precious Metals, FireFly Metals' $100 million raise with BMO, and Eric Sprott's continued support of New Found Gold demonstrate sophisticated investors' confidence in Newfoundland's mining framework.

The project site leverages established infrastructure including proximity to Turf Point deep water port (2 kilometers from site), Trans-Canada Highway access, and St. George's electrical substation (1.4 kilometers away). This existing infrastructure foundation significantly reduces pre-production capital requirements while enabling efficient logistics, critical factors given salt's relatively low value-to-weight ratio that makes transportation economics paramount to project viability.

Market Context: Structural Deficit Amid Import Dependence

The global salt market reached $26 billion in 2024 with projected 4.2% compound annual growth, while the North American de-icing segment represents an estimated 28.5-36 million tonnes annually valued at $2.3-2.9 billion. This market concentration in winter road safety creates predictable, weather-driven demand that municipal and state transportation departments must fulfill regardless of economic cycles. Unlike discretionary industrial minerals, de-icing salt represents essential infrastructure spending with limited substitution risk.

North America currently imports 8-10 million tonnes of de-icing salt annually, with 67.5 million tonnes imported to the United States from 2020-2023 primarily from Chile (29%), Canada (27%), Mexico (14%), and Egypt (8%). This import dependence creates supply chain vulnerabilities amplified by geopolitical tensions and logistics disruptions. The "Buy North American" sentiment gaining traction in procurement policies favors domestic producers like Atlas Salt, particularly for government entities prioritizing supply security over marginal cost differentials.

Recent industry consolidation and capacity exits intensify supply pressures. Cargill's 2021 closure of its Avery Island, Louisiana mine, North America's first-ever salt mine dating to the mid-1800s, removed 2.5 million tonnes per year of domestic supply to US East Coast de-icing markets. Additionally, Cargill's remaining salt assets in New York and Cleveland have remained unsold since a 2023 divestiture process began due to environmental risks, potentially removing approximately 2 million tonnes per year of additional supply.

Project Economics: Institutional-Grade Returns With De-Risked Profile

The 2025 Updated Feasibility Study demonstrates meaningful improvements over the 2023 baseline study. The updated study shortened mine life to 24.3 years from 34 years by pulling forward production and cash flow realization to achieve 4 Mtpa nameplate capacity, reducing reliance on long-term price forecasts while increasing NPV8 by 66% to $920 million. This strategic decision prioritizes near-term value capture over extended-duration projections, addressing a common investor concern regarding development-stage mining assets' reliance on distant assumptions.

Cost metrics reveal competitive positioning. Average life-of-mine all-in sustaining costs of $34.90 per tonne shipped represent an 18% improvement from the 2023 study, while gross margins per tonne increased 5% to $74.50. These unit economics compare favorably to industry benchmarks: Mosaic Company's Q3 2025 cash production cost of approximately $71 per tonne and Nutrien's Q1 2024 controllable cash cost of $56 per tonne provide relevant fertilizer mineral context for cost structure.

Capital efficiency merits investor attention. Pre-production capital expenditure of $589 million generates $4.6 billion in cumulative post-tax cash flow over the mine life, representing a 7.8x multiple on initial investment. The project achieves initial capital payback by Year 5 of production, creating a de-risked return profile once production commences.

Strategic Partnerships: Validating Commercial Viability

Atlas Salt executed a Memorandum of Understanding with Scotwood Industries for targeted volumes of 1.25-1.5 million tonnes per year, representing 31-38% of planned production capacity. Scotwood's position as the largest distributor of packaged retail de-icing salt in the United States provides immediate market access and volume visibility that de-risks commercial ramp-up assumptions. This partnership validates third-party willingness to commit to offtake based on the project's strategic value proposition.

Equipment financing and technical collaboration further advance project readiness. A memorandum of understanding with Sandvik for provision of mining equipment and engineering support valued at $73 million demonstrates equipment manufacturer confidence in the project's technical design while potentially providing vendor financing to reduce upfront capital requirements. Sandvik's global reputation in mining equipment and its willingness to provide both capital and technical resources represents meaningful third-party validation beyond equity investors.

The project's design validation through operational precedent reduces execution risk. Atlas Salt's mine design has been proven at Irish Salt Mining's Kilroot Mine, providing empirical evidence of the mining method's viability rather than relying solely on engineering studies.

Competitive Advantages: Location, Costs, & Sustainability

Geographic proximity to end markets creates structural cost advantages. Atlantic Canada, Quebec, and the US East Coast consume 11-16 million tonnes per year of road salt, with shipping time from the Great Atlantic Salt Project to Boston of approximately 3 days versus more than 14 days from Egypt or Chile. This transportation differential translates to both cost savings (reducing the CIF-FOB spread through shorter distances) and commercial advantages including faster order fulfillment and reduced working capital tied to inventory in transit.

The project's shallow mining depth provides capital and operating cost benefits compared to legacy North American operations. The Great Atlantic deposit sits approximately 180 meters from surface, compared to depths of approximately 600 meters for the world's largest salt mine at Goderich, Ontario. Shallow-depth mining enables decline access rather than shaft sinking, reduces ventilation costs, shortens haulage distances, and simplifies emergency egress, all translating to lower sustaining capital and operating expenses.

Environmental performance increasingly influences procurement decisions and regulatory approval timelines. The project's Scope 1 greenhouse gas emissions of 79 tonnes per year is comparable to just 4 Newfoundland households, with projected GHG intensity among the lowest in global mining at approximately 950 tonnes CO2-equivalent per million tonnes of ore production. Access to clean hydroelectric power, no tailings generation, no chemical processing, and minimal surface disturbance create a sustainability profile that aligns with government and corporate ESG procurement mandates.

The Investment Thesis for Atlas Salt

- Structural market deficit: Import dependence of 8-10 Mtpa and recent domestic capacity closures create immediate absorption capacity for new supply entering the North American de-icing market.

- Institutional-grade economics: After-tax NPV8 of $920 million, 21.3% IRR, and 4.2-year payback with $188 million average annual post-tax cash flow represents compelling risk-adjusted returns.

- Geographic and cost advantages: Shallow 180-meter depth, 3-day shipping to Boston versus 14+ days for imports, and access to clean hydropower create sustainable competitive positioning.

- Regulatory and technical de-risking: Environmental approval secured, proven mine design validated at comparable operations, and strategic partnerships reduce execution uncertainties.

- Near-term value catalysts: Project financing completion, engineering firm selection, additional offtake agreements, and equipment procurement announcements provide multiple re-rating opportunities.

- Limited new supply competition: No other North American salt mines or comparable expansion projects announced creates protected competitive position for multi-year period post-commissioning.

Atlas Salt represents differentiated exposure to North America's de-icing salt market at an inflection point where aging domestic infrastructure, import dependence, and recent capacity closures create structural supply tightness. The Great Atlantic Salt Project offers institutional-grade economics with after-tax NPV8 of $920 million and 21.3% IRR, underpinned by world-class geology, strategic location advantages, and cost competitiveness from shallow mining depth and clean power access. Environmental approval, strategic partnerships with Scotwood and Sandvik, and an experienced management team with aligned ownership reduce key development risks while preserving meaningful upside as the project advances toward 2030 production.

For investors, the investment case centers on multiple expansion potential as development milestones de-risk production assumptions. Current enterprise value of $69 million represents substantial discount to net asset value, with catalysts including project financing completion, additional offtake agreements, engineering firm selection, and equipment procurement providing re-rating opportunities. The commodity's essential-use demand profile and limited new supply competition create favorable long-term fundamentals, while the company's clean balance sheet, insider alignment, and no warrant overhang support patient capital deployment toward value-accretive milestones.

The salt market's projected growth, North America's import reliance, and Atlas Salt's strategic positioning create a compelling narrative for long-term investors seeking exposure to industrial minerals with predictable demand drivers and supply constraints. As the project advances through financing and into construction, investors should monitor execution against development timeline, capital efficiency relative to feasibility study estimates, and commercial agreements that validate market positioning.

TL;DR

Atlas Salt is developing the Great Atlantic Salt Project in Newfoundland, North America's first new major salt mine in approximately 30 years, with 4 Mtpa production capacity targeting the import-dependent de-icing market. The 2025 Updated Feasibility Study demonstrates after-tax NPV8 of $920 million, 21.3% IRR, and $188 million average annual post-tax cash flow over 24.3-year mine life. Strategic advantages include shallow 180-meter mining depth, 3-day shipping to Boston versus 14+ days for imports, clean hydropower access, and high-grade 95.9% NaCl reserves. North America currently imports 8-10 Mtpa of de-icing salt, with recent domestic mine closures removing 4.5 Mtpa of capacity while legacy operations face operational challenges. Environmental approval secured, strategic partnerships with Scotwood Industries and Sandvik advance commercial and technical readiness, with production targeted by 2030.

FAQs (AI-Generated)

The Great Atlantic deposit sits at shallow 180-meter depth versus 600+ meters for legacy mines like Goderich, enabling decline access rather than costly shaft sinking while maintaining high 95.9% NaCl grade across 95 million tonne 2P reserves.

The project is located 3 days shipping time to Boston versus 14+ days from Chile/Egypt, directly serving the 11-16 Mtpa Atlantic Canada and US East Coast market while reducing transportation costs and carbon footprint.

Atlas Salt has engaged Endeavour Financial as project finance advisor to structure the $589 million pre-production capital requirement, with strategic partnerships providing revenue visibility and vendor financing to support debt capacity.

The 2025 study shortened mine life to 24.3 years from 34 by pulling forward production to 4 Mtpa nameplate capacity, reducing long-term forecast reliance while increasing NPV8 by 66% to $920 million.

Immediate catalysts include project financing completion, selection of lead engineering firm, additional offtake agreements beyond Scotwood MOU, equipment procurement announcements with Sandvik, and achievement of construction-ready status.

Analyst's Notes

Subscribe to Our Channel

Stay Informed