Sulfuric Acid Shortages & Financial Flows Reprice Copper and Shift Capital Toward Low-Cost Producers

Copper is being repriced by sulfuric acid shortages and fund flows, shifting capital toward low-cost, near-term producers despite a physical surplus.

- Wood Mackenzie identifies sulfuric acid availability, smelter economics, trade policy, and fiscal risk as the binding supply-side constraints on copper, displacing declining grades as the operative variable.

- Spot sulfuric acid prices have doubled, with Chinese imports into Chile at a standstill ahead of May 2026 export restrictions, exposing smaller operators on spot procurement to direct margin compression while contract-secured majors remain partially insulated.

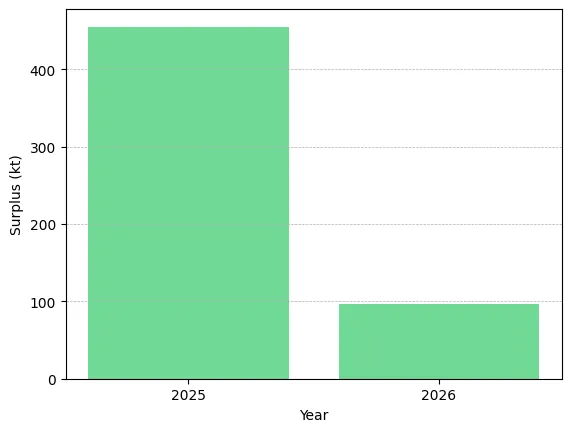

- The International Copper Study Group's April 2026 spring meeting flipped its 2026 balance from a 150,000-tonne deficit to a 96,000-tonne surplus and revised the 2025 surplus to 455,000 tonnes against 1.3 million tonnes of visible exchange inventory.

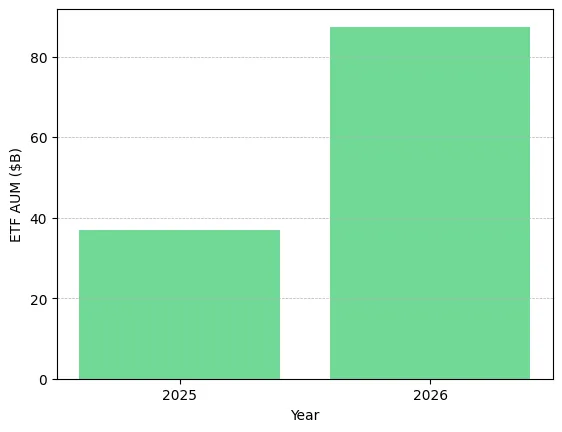

- Mining exchange-traded fund assets under management more than doubled to $87.4 billion from $37 billion a year earlier according to ETFGI data, with money managers net long 59,132 CME copper contracts, the largest bull commitment since mid-January 2026.

- Major mining companies trade at 7 to 8 times enterprise value to earnings before interest, taxes, depreciation, and amortization (EV/EBITDA) versus 14 times during the 2008-2010 boom, leaving capital discipline, infrastructure access, and input security as the primary differentiators among copper equities.

Copper Production Is Shifting from Geological Scarcity to Input Bottlenecks

The International Copper Study Group revised the 2025 surplus to 455,000 tonnes, more than double the 178,000 tonnes implied by its October 2025 forecast, and projects a 96,000-tonne 2026 surplus, with exchange-warehouse inventories at 1.3 million tonnes signalling abundance while LME three-month copper holds near $13,000 per tonne ($5.90 per pound).

Wood Mackenzie identifies sulfuric acid availability, treatment and refining charge (TCRC) compression, trade policy, and fiscal risk as the operative supply constraints. None reside in a resource statement, which means production guidance now depends on inputs and policy regimes that mine geology models do not capture and that can tighten on the timescale of weeks rather than years.

A sulfur shipment delay reduces acid availability at the leach pad within weeks, then reduces cathode output within the same quarter, compressing the lag between geopolitical events and producer earnings. For solvent extraction-electrowinning (SX-EW) operators producing roughly one-quarter of global refined copper, this faster transmission raises the variance on full-year guidance and lifts earnings volatility independent of spot price.

Sulfuric Acid Supply Disruptions Are Now the Binding Constraint on Copper Leach Production

Sulfuric acid is the reagent used to leach copper from oxide ore in heap leach and SX-EW circuits. As a co-product of smelting and oil refining, its supply is set by industries unrelated to copper demand and is largely inelastic to copper price.

The Middle East conflict interrupted sulfur exports to Asian sulfuric acid producers, and China is set to implement sulfuric acid export restrictions from May 2026 to protect domestic smelter feed. Spot acid prices have doubled per the same source, and Chinese acid imports into Chile are at a standstill, with domestic Chilean supply from Noracid, Codelco, and Anglo American covering near-term needs but visibility deteriorating beyond mid-2026.

Chile, the world's largest copper producer, is short of sulfuric acid according to Wood Mackenzie. Smaller Chilean operators on spot procurement face direct margin compression while larger producers with multi-year contracts remain partially insulated. Compounding this, Grupo México's Tía María project in Peru is targeting late-2027 ramp-up with acid procurement starting ahead of first cathode, adding incremental demand to a regional acid market already short on supply.

Developers Are Leveraging Third-Party SX-EW Capacity to Bypass Acid and Capex Constraints

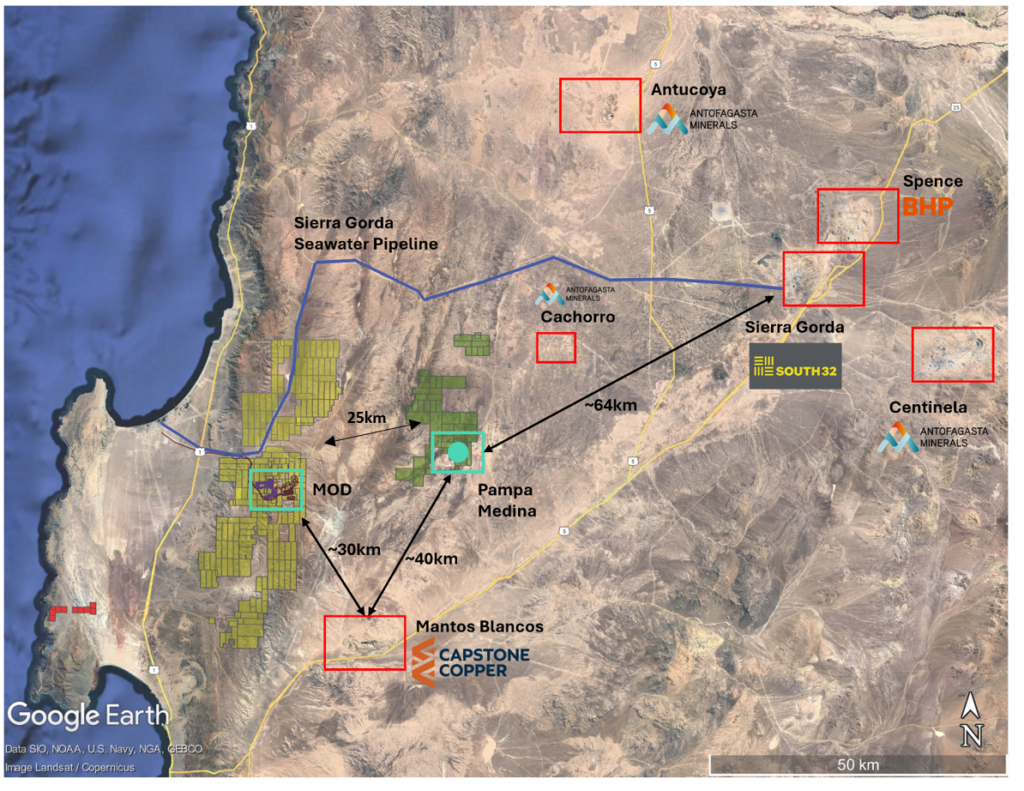

Fitzroy Minerals, an explorer-developer at the Buen Retiro Copper Project near Copiapó in Chile, signed a non-binding Letter of Intent with Sociedad Punta del Cobre (Pucobre) on April 23, 2026 to use Pucobre's Planta Biocobre SX-EW facility, which carries 9,600 tonnes per annum of nameplate cathode capacity 70 kilometres from the project, in place of constructing a standalone processing circuit.

Merlin Marr-Johnson, President and Chief Executive Officer of Fitzroy Minerals, articulates the capital-intensity advantage that infrastructure leverage delivers in an acid-constrained jurisdiction:

“We have started a PEA, and we are working on terms with Pucobre to establish a heap leach joint venture. That operation gives us the potential for near-term, non-operated cash flow, which we believe will distinguish us from many other explorers in the market.”

ETF Inflows and Speculative Positioning Are Sustaining Copper at $5.90/lb Despite Surplus

Copper traded at $5.90 per pound, against a 96,000-tonne 2026 surplus forecast and 1.3 million tonnes of exchange inventory according to the International Copper Study Group. The disconnect between physical balance and price is being closed by financial flows, not industrial demand.

Mining exchange-traded fund assets under management more than doubled to $87.4 billion at March 31, 2026 from $37 billion a year earlier according to the ETFGI data, with first-quarter 2026 inflows of $8.24 billion reversing $2.52 billion of outflows in first-quarter 2025. Money managers held 59,132 net long contracts on the CME copper contract, the largest bull commitment since mid-January 2026.

Copper now functions as both an industrial commodity and a macro hedge against inflation and geopolitical conflict, which means price volatility is increasingly driven by positioning unwinds rather than smelter outages. Investors underwriting copper equities at $5.90 per pound need to separate the price floor set by marginal cost from the price premium set by financial flows: the former supports long-duration project economics, the latter near-term equity beta.

China’s Policy Distortions and Cost Inflation Are Redefining Copper Demand Signals and Price Floors

The International Copper Study Group cut its 2026 copper usage forecast to 1.6% from 2.1%, citing the Iran crisis as likely to weaken global growth. Pre-holiday restocking ahead of Labor Day has supported physical premiums in Shanghai, while stricter Chinese invoicing rules have slowed spot trading as specified by ING on April 30, 2026.

Stricter value-added-tax invoicing enforcement is reducing intermediaries' willingness to hold inventory, producing uneven warehouse drawdowns and complicating real-demand signal extraction, while pre-holiday restocking provides a near-term price floor independent of speculative positioning. The net effect is a narrower window for reading Chinese physical data cleanly, with copper exposed to policy headlines on the same axis as industrial production.

Acid prices doubling, energy cost increases, and logistics disruption are lifting the marginal cost floor that anchors long-term copper price expectations. All-in sustaining costs (AISC) are moving higher across the producing universe, compressing margins for operators without long-term input contracts and raising the bar new projects must clear to attract capital.

Lower Capital Becoming the Key Differentiator in Copper Project Development

Marimaca Copper's 2025 feasibility study shows the project can be built for just under $600 million to produce 50,000 tonnes of copper per year, which translates into a relatively low upfront cost per unit of output. The mine plan requires removing only 0.8 tonnes of waste to access 1 tonne of ore, versus 2 to 4 tonnes at many comparable projects, which directly lowers mining costs per tonne and reduces fuel, labor, and equipment intensity. This cost advantage drives a capital intensity of about $11,700 per tonne, well below the $15,000 to $25,000+ typical for peers, implying more efficient capital deployment and faster payback. At a copper price of $4.30 per pound, the project delivers a 39% internal rate of return, indicating strong margins and resilience even without relying on higher copper prices.

With the company having raised C$80 million in April 2026 from Australian, Canadian, and US institutional investors and targeting construction commencement by the end of 2026, Hayden Locke, President and Chief Executive Officer of Marimaca Copper, frames the operability discipline that protects those economics:

"We're going to take our time and we're going to increase the level of maturity of the project to make sure that we minimize the level of variations that come through as we go into the execution phase. We're going to resist the temptation to just jump head first into this, we want to get it right the first time."

Capital Is Shifting to Low-Cost Copper Projects with Clear Paths to Production

Capital is migrating toward low capital-intensity projects, infrastructure-leveraged projects, and staged pathways where cash flow from a first asset funds a second. Major mining companies trade at 7 to 8 times EV/EBITDA versus 14 times during the 2008-2010 boom, indicating that a marginal-cost-floor reset combined with disciplined capital deployment is the upside thesis being underwritten by generalist funds returning to the sector.

Discovery upside has not lost strategic value, but capital is increasingly discounting exploration results unless a credible, financed pathway to production exists. Resource size, grade, and metallurgy remain necessary but no longer sufficient screens.

Equity Backing Signals Which Exploration Projects Attract Institutional Capital

Abitibi Metals, with the B26 polymetallic deposit in Quebec hosting 12.96 million tonnes indicated at 2.08% copper equivalent and 12.34 million tonnes inferred at 2.20% copper equivalent per the November 1, 2024 NI 43-101 Technical Report by SGS Canada, secured a C$30.75 million investment from Discovery Silver on April 23, 2026 representing approximately 9.9% of issued shares on a non-diluted basis. The financing is structured to fund 80,000-plus metres of drilling through 2027 with no warrants issued, preserving the existing capital structure through the targeted preliminary economic assessment milestone.

Jonathon Deluce, President and Chief Executive Officer of Abitibi Metals, identifies why producer-level validation matters as a forward signal for institutional capital:

"We've now attracted, upon closing, a world-class producing partner that will have a 9.9% stake in the company. This provides a stamp of approval that I think we will see continued interest from some of the larger generalist funds."

Selkirk Copper is advancing the Minto Mine restart in Yukon with 12.6 million tonnes indicated at 1.2% copper, 0.46 g/t gold, and 4.27 g/t silver, targeting a PEA by mid-2026 and construction decision in H2 2027, focusing on a capital-efficient transition to production. Over C$300 million of sunk infrastructure including a 4,100-tonne-per-day mill eliminates greenfield capex risk, while bankruptcy-cleared stream and offtake agreements preserve full economics. The Selkirk First Nation holds 18.9% equity, providing social license stability in a jurisdiction that elected a pro-mining government in November 2025.

The Investment Thesis for Copper

- Sulfuric acid availability is a structural rather than cyclical constraint according to Wood Mackenzie's April 30, 2026 outlook, supporting margin difference between contract-secured majors and spot-exposed smaller operators across Chile and Peru.

- The International Copper Study Group's 2026 surplus forecast of 96,000 tonnes against $5.90 per pound copper indicates that financial flows rather than physical balance are setting the marginal price, which supports near-term equity beta but introduces positioning-driven downside risk on unwind.

- Mining exchange-traded fund assets at $87.4 billion as of March 31, 2026 represent a generalist rotation into hard assets that has not been priced into mining equities trading at 7 to 8 times EV/EBITDA against the 14 times multiple of the 2008-2010 cycle peak.

- Capital intensity below the $15,000 to $25,000-plus per tonne peer range, infrastructure leverage, and producer-level validation differentiate developers underwriting through current cost-curve inflation.

Copper's investment case has shifted from how much resource exists to who can produce reliably under input, policy, and capital constraints. The International Copper Study Group's 96,000-tonne 2026 surplus forecast, 1.3 million tonnes of exchange inventory, and $5.90 per pound spot copper confirm that the market is not physically short, yet $87.4 billion in mining exchange-traded fund assets, doubled sulfuric acid prices, and halted Chinese acid exports into Chile are doing the pricing work that fundamentals once did. Resource size remains a necessary screen but is no longer sufficient. Input security, capital intensity below the $15,000 per tonne peer range, infrastructure access, and producer-level validation now determine which copper equities convert macro tailwinds into delivered cash flow.

TL;DR

Copper markets are no longer driven by geological scarcity but by input constraints and financial flows. Despite a projected surplus and high inventories, prices remain near $5.90/lb due to sulfuric acid shortages, disrupted trade flows, and strong ETF-driven positioning. This shift is compressing margins for spot-exposed producers while rewarding those with secured inputs and infrastructure access. At the same time, capital is rotating toward low-capex, buildable projects with clear paths to production, and institutional funding is increasingly contingent on producer validation rather than exploration upside alone.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed