Surging Industrial Demand Tightens Silver Supply, Triggering Strategic Repricing in 2025

Silver's 206Moz deficit drives structural repricing as solar demand surges. Industrial scarcity meets monetary hedge appeal in 2025 investment thesis.

- Silver is experiencing a deepening structural supply deficit, with projected shortfalls exceeding 200 Moz in 2025, driven by industrial demand growth in solar, electronics, and EVs.

- Despite rising prices, mine supply remains inelastic, as 70% of silver is produced as a byproduct, constraining the market’s ability to respond to demand surges.

- Silver’s dual identity as an industrial metal and monetary asset is reinforcing investor interest amid macro volatility, FX pressure, and Fed policy ambiguity.

- Companies like Americas Gold & Silver, Cerro de Pasco, Vizsla Silver, and GR Silver Mining are strategically positioned to benefit from this demand imbalance through low-cost production, scalable assets, and unique exposure models.

- With continued inflows into silver ETPs, and strong pricing fundamentals, investors may increasingly prioritize operational readiness and jurisdictional safety in silver-focused portfolios.

Supply Constraints Meet Accelerating Demand

Silver's market is approaching a critical juncture. The projected 206 million ounce supply deficit for 2025 marks the eighth consecutive year of market imbalance, according to CPM Group, fueled largely by industrial end-use demand. Despite silver prices hovering near decade highs of approximately $38 United States Dollars per troy ounce, new primary silver production is lagging due to permitting delays, capital intensity, and declining ore grades.

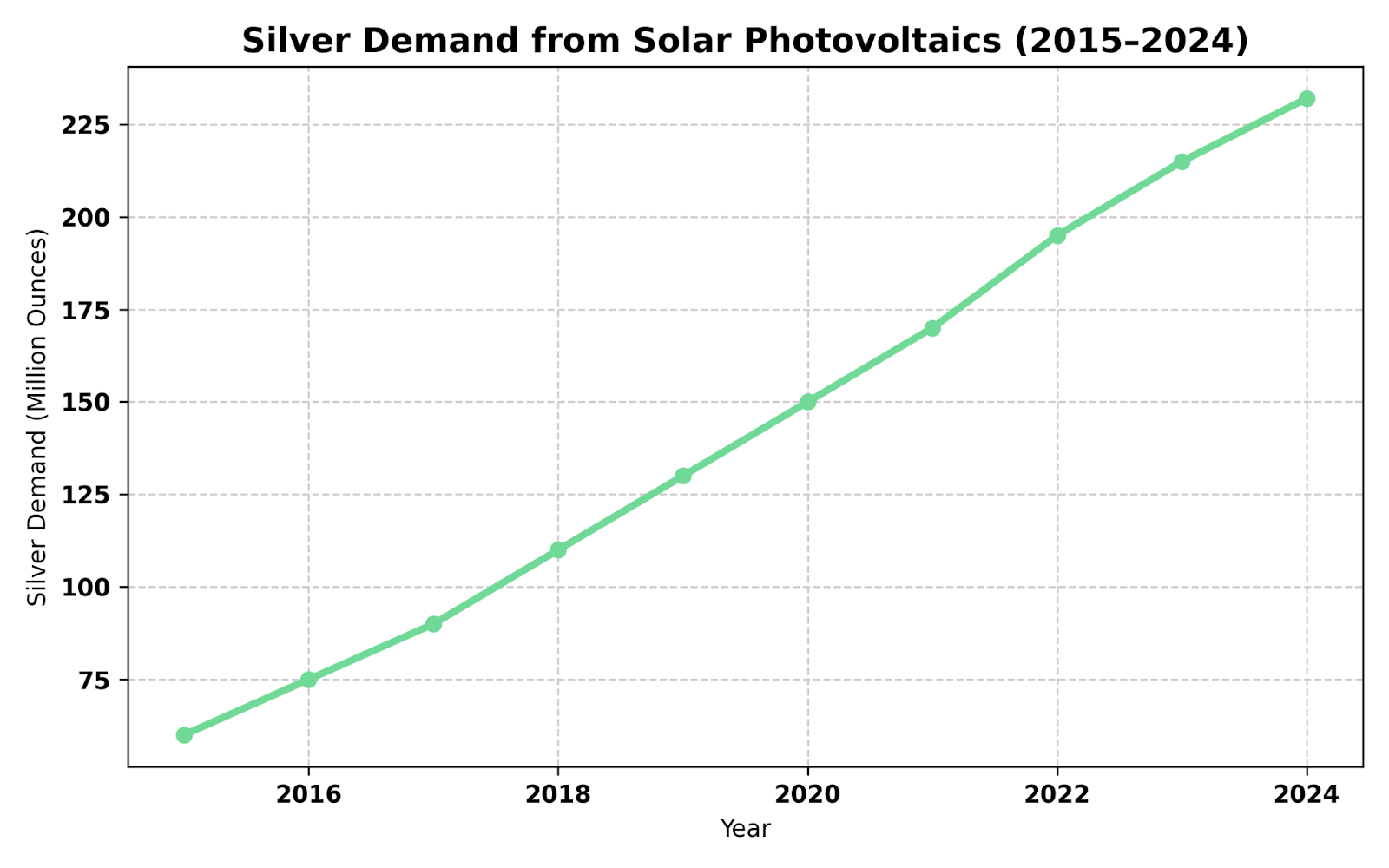

With approximately 70% of silver production coming as a byproduct, price signals alone are not sufficient to prompt fast supply response, especially as base metal producers continue to prioritize copper, lead, and zinc. The consequence is inelastic mine supply in the face of record silver consumption across photovoltaics, electronics, and electric vehicle manufacturing. In 2024, solar alone absorbed 232 million ounces, up from just 60 million ounces in 2015, according to the Silver Institute.

Americas Gold & Silver exemplifies how established producers are adapting to this environment. The company's Cosalá Operations are optimized to deliver approximately 2.5 million ounces annually by 2026, supported by all-in sustaining costs of $10.80 per ounce and revenue alignment toward 80% silver exposure by 2025. This revenue profile makes the company uniquely sensitive to price upside driven by industrial demand acceleration.

The fundamental challenge facing the silver market is the disconnect between demand visibility and supply responsiveness. While industrial applications provide clear demand forecasting, particularly in solar where installation commitments extend years into the future, mine supply cannot pivot quickly enough to address shortfalls. This structural mismatch is creating persistent pricing pressure and investment opportunities for companies with existing production capacity or near-term development pathways.

Demand Acceleration: Photovoltaics & Electrification

The green energy transition has transformed silver's demand profile fundamentally. Solar photovoltaic production has become the single largest industrial driver, but silver's role spans across electric vehicles, semiconductors, 5G infrastructure, and medical applications, creating persistent multi-sector demand that reinforces consumption growth beyond any single industry cycle.

While some substitution and thrifting have occurred within specific applications, aggregate volume growth in solar deployment is outpacing those efficiency gains. The International Energy Agency projects massive expansion in global solar capacity, underpinned by United States Inflation Reduction Act credits and European Union Green Deal funding, sustaining strong silver pull-through into the 2030s.

The electrification theme extends beyond solar into electric vehicle battery systems, charging infrastructure, and grid modernization, all requiring significant silver content per unit. This creates compounding demand pressure as multiple green technologies scale simultaneously. Unlike cyclical industrial metals, silver's green energy applications represent secular demand shifts with limited substitution potential, particularly in high-conductivity applications where performance cannot be compromised.

Market participants are beginning to recognize that silver's industrial demand is less price-sensitive than traditional commodity applications. Solar manufacturers and electric vehicle producers prioritize supply security and performance over marginal cost differences, creating more stable demand even during price volatility. This dynamic supports sustained consumption even as silver prices appreciate, distinguishing it from other industrial metals where demand destruction typically occurs at elevated price levels.

Silver as an Inflation Hedge & Strategic Asset

Beyond industrial applications, silver has reclaimed visibility as a monetary hedge, especially amid renewed interest in precious metals exchange-traded funds. With $40 billion in exchange-traded product assets under management and over 95 million ounces of inflows in 2025, institutional sentiment toward silver is accelerating at unprecedented levels.

This rotation reflects a pricing divergence between silver and gold that sophisticated investors are beginning to exploit. Despite silver's similar macro behavior during periods of currency volatility and inflation uncertainty, the gold-to-silver ratio remains stretched at approximately 1:90, prompting long-term investors to reallocate portions of precious metals exposure toward silver. Moreover, silver's greater volatility and percentage upside potential in bull cycles make it attractive for inflation-hedging and strategic repositioning within diversified portfolios.

The monetary aspects of silver are being reinforced by central bank diversification strategies and sovereign wealth fund allocation patterns. As traditional reserve assets face debasement risk and geopolitical complications, silver provides exposure to monetary themes while maintaining industrial utility. This dual functionality creates unique investment appeal during periods of macro uncertainty, where both defensive positioning and growth exposure are valued simultaneously.

Silver's performance during inflationary periods historically outpaces gold on a percentage basis, making it an attractive hedge for institutional investors seeking leverage to monetary themes. The current supply-demand imbalance amplifies this dynamic, as monetary demand compounds industrial scarcity rather than competing with it.

Companies to Watch: Development & Exploration Opportunities

The silver development landscape presents compelling opportunities for investors seeking exposure to supply-side solutions. Three companies demonstrate distinct approaches to addressing silver's structural deficit through innovative development strategies and strategic positioning.

Vizsla Silver: Tier-1 Asset Development & Funding

Vizsla Silver is developing Mexico's next tier-one silver deposit through its Panuco Project, which hosts 361 million ounces of silver equivalent inferred and indicated resources. The company has progressed rapidly from early-stage exploration to approaching feasibility study completion and project finance phases. With a preliminary economic assessment demonstrating all-in sustaining costs of $9.40 per ounce and a post-tax net present value of $1.1 billion, Vizsla represents scalable, low-cost silver exposure.

Vizsla Silver Chief Executive Officer Michael Konnert emphasizes the company's production trajectory:

"The faster we can get into cash flow the better and once we're in that construction period it is a relatively short construction period following that we'll be producing 20 million ounces of silver equivalent in those first two years as per the preliminary economic assessment"

The company recently raised $100 million in a bought deal financing, bringing total cash on hand to over $200 million United States Dollars. This funding positions Vizsla to advance through construction without dilutive financing during the critical development phase. Management expects to maintain the 20 million ounce annual production profile beyond the initial two-year period, potentially extending into years three and four of operation.

Cerro de Pasco Resources: Unique Above-Ground Resource & Remediation

Cerro de Pasco Resources owns mineral rights to what may be the largest above-ground mineral resource globally, 423 million ounces of silver equivalent contained in tailings and stockpiles from historical mining operations.

The project offers exceptional economics with processing costs of approximately $1 per ton and projected profits of $39 per ton. Beyond silver, the tailings contain significant gallium concentrations averaging 30 grams per ton, with recent drilling returning up to 86 grams per ton in southern areas. This creates exposure to critical minerals demand alongside silver, as gallium is essential for semiconductor and solar panel manufacturing.

The company's approach is committed to responsible mining practices and partnering with local stakeholders, a model that aligns with environmental, social, and governance priorities while accessing low-cost silver production. With Eric Sprott owning 22% of the company, institutional backing provides credibility and financial support for development activities.

GR Silver Mining: Mexico Mining Outlook & Consolidation Strategy

GR Silver Mining is advancing its Plomosas Project in Sinaloa, Mexico, which contains 134 million ounces of indicated and inferred silver equivalent resources across two distinct zones. The project benefits from existing infrastructure, including 7.4 kilometers of underground development and established permitting, significantly reducing development timelines and capital requirements.

GR Silver Mining Chief Executive Officer Eric Zaunscherb outlines the consolidation opportunity:

"The market wants right now is consolidation in the silver space and what we're going to see is the creation of new strong players in the silver space"

Recent drilling at the San Marcial zone returned exceptional results, including 102 meters averaging 308 grams per ton silver, demonstrating the project's scalability potential. The company recently completed a $2.4 million financing and eliminated working capital deficits, providing operational flexibility during the development phase. Management is positioning GR Silver as a consolidation platform, seeking to create a mid-tier silver producer with market capitalization exceeding $200 million Canadian and multiple development assets.

The company's valuation of approximately $0.65 per ounce in the ground places it within the middle range of Mexican peers, despite hosting district-scale mineralization with significant exploration upside. This valuation gap reflects the broader discount applied to development-stage silver assets, creating potential re-rating opportunities as projects advance toward production decisions.

Capital Barriers, Permitting Risk & Environmental, Social, and Governance Headwinds

Despite favorable pricing and institutional inflows, new silver project development remains constrained by structural challenges that extend beyond simple economics. Long lead times of seven to ten years, permitting delays, and rising environmental, social, and governance scrutiny complicate new mine approvals across multiple jurisdictions.

Jurisdictions with established regulatory frameworks, Mexico, Peru, Idaho, are gaining investor favor, as project timelines are more predictable and infrastructure more accessible. The role of community agreements, water access, and tailings solutions has grown more central in capital formation decisions. Investors increasingly evaluate projects based on permitting risk rather than purely geological merit, creating valuation premiums for assets in stable jurisdictions.

The capital intensity required for new silver mines has increased substantially due to environmental compliance costs, community investment requirements, and enhanced safety standards. This creates natural barriers to entry that benefit existing producers and advanced development projects with established permitting positions. Companies that secured land positions and community agreements before recent regulatory changes maintain competitive advantages in development timelines and capital efficiency.

Environmental, social, and governance considerations are reshaping silver project evaluation criteria. Investors now prioritize projects with demonstrable community benefits, environmental remediation components, and transparent stakeholder engagement processes. This shift favors innovative development models that align economic returns with social and environmental outcomes.

Jurisdictional Exposure & Resource Security

In a world of resource nationalism and trade friction, jurisdictional exposure matters more than ever for silver investors. Mexico remains the top silver-producing nation and hosts eight of the fourteen largest silver districts globally. However, investors increasingly favor United States and Canada-based projects due to security of tenure and stable permitting frameworks that reduce development risk.

For silver projects in Latin America, proactive community engagement and infrastructure investment are critical de-risking strategies. Companies operating in Peru and Mexico have responded by integrating long-term social contracts and multi-decade land agreements that provide operational stability. The recent change in Mexican presidential leadership toward more pragmatic mining policies has reduced the jurisdictional discount previously applied to Mexican silver assets.

Americas Gold & Silver benefits from this jurisdictional diversification through operations in both Idaho and Sinaloa. The Idaho-based Galena Complex provides exposure to United States strategic mineral priorities, including antimony, while the Mexican operations offer access to world-class silver districts with established infrastructure. This geographic spread reduces regulatory risk while maintaining access to high-grade silver resources.

The strategic importance of reliable silver supply chains is growing as electric vehicle adoption accelerates and solar deployment expands. Countries are increasingly viewing silver as a critical mineral for energy security, creating policy support for domestic production and strategic partnerships with allied nations. This trend favors silver projects in stable jurisdictions with established trade relationships and predictable regulatory environments.

The Investment Thesis for Silver

Silver's investment thesis in 2025 hinges on structural scarcity, industrial resilience, and monetary alignment. As mine supply struggles to match demand, investors are seeking companies with near-term catalysts, jurisdictional strength, and cost leverage that can capitalize on sustained pricing strength.

- Supply-demand mismatch creates persistent deficits exceeding 200 million ounces annually, with inelastic supply and byproduct constraints limiting production response to price signals.

- Industrial momentum from solar, electric vehicles, and semiconductors reinforces consumption growth through 2030 and beyond, supported by policy frameworks and technological adoption curves.

- Macro hedge characteristics resurge amid inflation uncertainty, United States interest rate risk, and currency volatility, positioning silver as both defensive and growth-oriented allocation.

- Project readiness advantages companies with near-term production capabilities or scalable development assets that can respond quickly to sustained demand strength.

- Cost advantage positioning through low all-in sustaining cost assets and low-capital expenditure development models creates margin expansion potential during price appreciation cycles.

- Exploration optionality provides potential re-rating opportunities through district-scale discovery success and resource expansion in established mining regions.

- Jurisdictional diversification reduces regulatory risk while maintaining access to high-grade silver resources in stable, mining-friendly environments.

- Environmental, social, and governance alignment creates competitive advantages for projects that integrate community benefits and environmental remediation with economic returns.

Strategic Allocation Amid Silver's Secular Repricing

The silver market's structural deficit represents a systemic outcome of underinvestment, industrial evolution, and constrained supply chains rather than a temporary cyclical imbalance. Investors are beginning to recognize silver's dual role as both industrial input and monetary asset, responding with capital flows into both physical and equity assets that reflect this fundamental shift in market dynamics.

As prices remain elevated and institutional interest deepens, silver miners with the right combination of scalability, cost structure, and jurisdictional security are increasingly differentiated from their peers.

Whether through near-term production optimization, low-cost reprocessing innovation, or district-scale discovery potential, these firms reflect a market recalibrating around real assets, real returns, and real scarcity. The investment opportunity in silver extends beyond simple commodity exposure to encompass strategic positioning within a transforming global economy increasingly dependent on reliable silver supply chains for critical technologies and monetary diversification strategies.

Analyst's Notes

Subscribe to Our Channel

Stay Informed