US Section 301 Trade Pressure on Mexico Threatens 25% of Global Silver Supply

US Section 301 targets Mexico, threatening 25% of global silver supply and creating a valuation premium for US silver producers.

- The US Trade Representative's Section 301 investigations, initiated in March 2026 and targeting Mexico among 16 economies, place approximately 200 million ounces of annual silver supply under direct tariff and regulatory risk, compounding a market entering its sixth consecutive annual structural deficit.

- Fresnillo PLC, the world's largest primary silver producer and a Mexico-only operator, has already cut its 2026 production guidance by 9% on geological grounds before any tariff takes effect, demonstrating that Mexico's silver supply base is contracting from both operational and trade policy risk simultaneously.

- Washington's critical minerals agenda, covering Section 232 reviews and domestic supply chain mandates, is generating a valuation premium for US-domiciled silver and antimony production that did not exist at this scale three years ago.

- Mexico-based silver exploration and development assets must now carry an explicit jurisdictional risk discount in NPV and IRR calculations, while US-based producers with permitted, operating assets are repositioning as dual-purpose commodity and critical infrastructure plays.

- Two silver companies navigating this geographic bifurcation illustrate how the same macro force creates divergent risk-reward profiles: GR Silver Mining Ltd., an exploration-stage company advancing a high-grade epithermal system in Sinaloa, Mexico, and Americas Gold and Silver Corporation, executing a fully funded US$60 to US$80 million growth capital program in Idaho's Silver Valley.

US Trade Policy Turns Silver's Supply Geography Into an Active Investment Variable

The global silver market has spent the past eighteen months absorbing a series of demand-side shocks: record photovoltaic (PV) capacity additions, electric vehicle production, and the emergence of AI data center infrastructure as a new silver-intensive industrial category. Against this backdrop, the supply side has been treated as largely static, growing roughly 1 to 2% annually regardless of price signals, and registering a supply deficit in each of the past six consecutive years.

That assumption is now under active policy stress. The US Trade Representative formally initiated Section 301 investigations on March 11 and 12, 2026, targeting Mexico among 16 economies for alleged excess manufacturing capacity and forced labor violations. A public comment period closed April 15, a formal public hearing is scheduled for May 5, and a USMCA review covering approximately $1.8 trillion in annual bilateral trade follows in July 2026. The regulatory mechanism now targeting the world's largest silver-producing nation is not a background risk. It is an active, time-bound legal process with a defined escalation sequence and quantifiable supply consequences that investors in silver equities need to account for ahead of formal findings.

Mexico's Concentration Risk & the Production Shortfall Already Underway

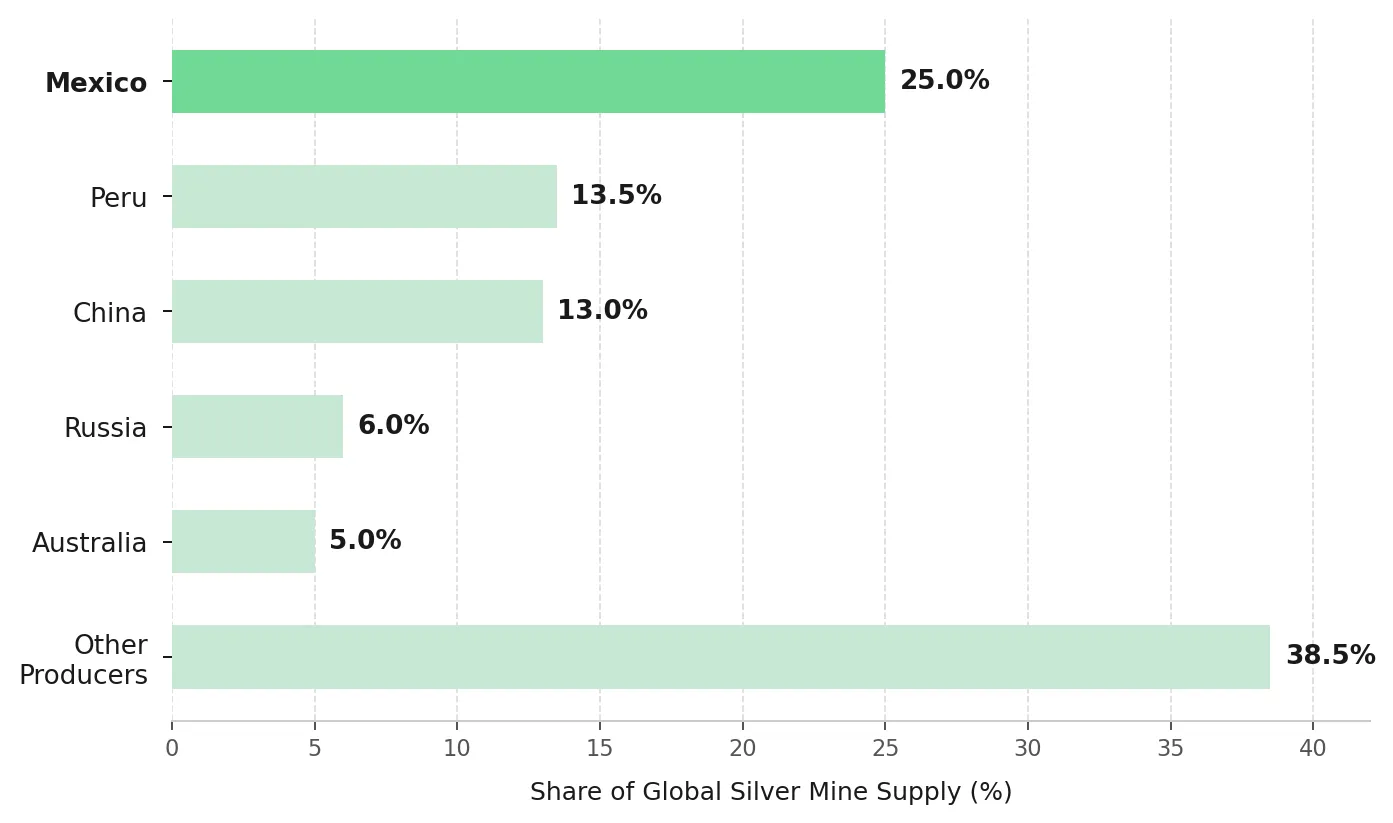

Mexico produces approximately 200 million ounces of silver annually, representing roughly one-quarter of global mine supply in a market the Silver Institute estimates at approximately 1.2 billion ounces of annual consumption. Peru ranks second at approximately 13 to 14% of global output, followed by China, Russia, and Australia. Any meaningful disruption to Mexican silver production carries a disproportionate impact on Western-accessible above-ground supply relative to that country's share of world output.

This concentration is already visible in operational data, independent of any trade policy escalation. Fresnillo PLC, operating exclusively within Mexico as the world's largest primary silver producer, cut its 2026 production guidance by 9% citing geological constraints: narrower vein structures and deteriorating ground conditions at key producing mines. Higher silver spot prices do not accelerate the geological remediation required at Fresnillo's affected operations. That distinction matters directly when assessing how quickly incremental supply can respond to a tariff-driven curtailment. Analyst consensus models for the top three primary silver producers show a combined guidance shortfall of approximately 12 to 20 million ounces against prior market expectations for 2026, before any tariff effect is incorporated.

The Regulatory Timeline & Its Investment Implications

The Section 301 process follows a defined legal sequence under the US Trade Expansion Act of 1962. Formal US Trade Representative findings will follow the May 5 public hearing, and the USMCA review in July 2026 will determine the full scope of bilateral trade exposure. Full escalation to tariff imposition is not a certainty, but it now carries a credible legal pathway and a defined timeline. For investors holding Mexico-based silver equities, the analytically relevant question is not whether tariffs will be imposed, but whether current valuations incorporate the probability-weighted cost of that scenario at an appropriate jurisdictional discount rate applied to NPV and IRR models.

Washington's Critical Minerals Agenda Creates a Valuation Premium for US Silver & Antimony Producers

The Section 301 investigation is one component of a broader federal critical minerals strategy. Section 232 reviews of mineral imports, Inflation Reduction Act domestic content provisions, and executive directives to reshore strategic supply chains have collectively elevated the value of US-domiciled mineral production. Silver has entered this policy architecture through two specific channels: its byproduct relationship with copper and lead-zinc mining, both officially designated critical minerals, and the Galena Complex in Idaho's emergence as the nation's largest producing antimony mine, a formally designated critical mineral with documented defense and semiconductor supply chain applications.

The investment consequence is a valuation premium now being applied to US-domiciled silver assets that was absent three years ago. Permitted, operating silver mines on US soil function as dual-purpose assets: commodity producers and critical supply chain infrastructure nodes. Americas Gold and Silver Corporation’s Galena Complex in Idaho's Silver Valley and its recently acquired Crescent Mine together sit at the convergence of the domestic production premium and the critical minerals policy tailwind. In February 2026, the company formed a 51/49 joint venture with US Antimony to build a vertically integrated mine-to-finished-product antimony processing hub at Galena, at a moment when domestic antimony supply carries explicit national security significance.

Oliver Turner, Executive Vice President of Corporate Development at Americas Gold and Silver, frames the competitive value of the company's producing antimony output:

"If you want exposure to antimony in your portfolio, Galena is the largest producing antimony mine today. These aren't future products. This isn't a future project. This is something that's coming out of the ground today."

Funded Capital Programs & Near-Term Production Milestones Support Re-Rating

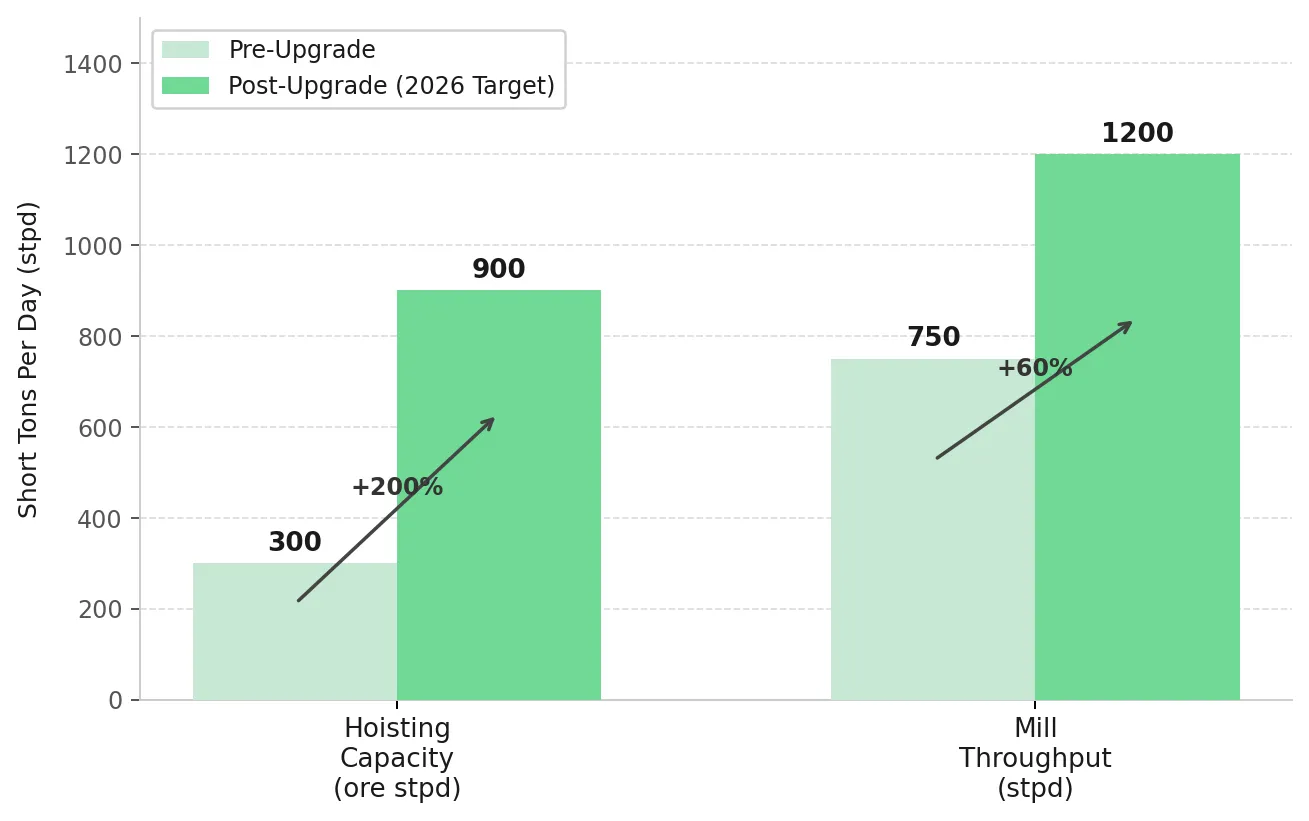

A US$60 to US$80 million growth capital program executing at Galena in 2026 provides the operational specificity behind the strategic positioning. Six simultaneous workstreams are underway: No. 3 Shaft Phase 2 hoisting upgrades targeting mid-May 2026 completion, increasing total hoisting capacity 150% to approximately 105 short tons per hour; paste backfill plant commissioning in Q4 2026, reducing backfill cycle time by approximately 250%; mill capacity expansion from 750 to 1,200 short tons per day; Galena Shaft repurposing; mine-wide fiber optic communications; and Crescent Mine resource drilling. Each milestone represents a discrete inflection point for AISC improvement and throughput within a single fiscal year, giving investors a time-bound catalyst calendar against which to track execution.

Turner addresses the per-unit cost consequence of the shaft upgrades and mining method transition:

"You're going to see anywhere from about 40 to 50% per ton cost reductions on the mining front."

Tightening Silver Supply Deficit Magnifies Price Impact of Mexican Output Disruptions

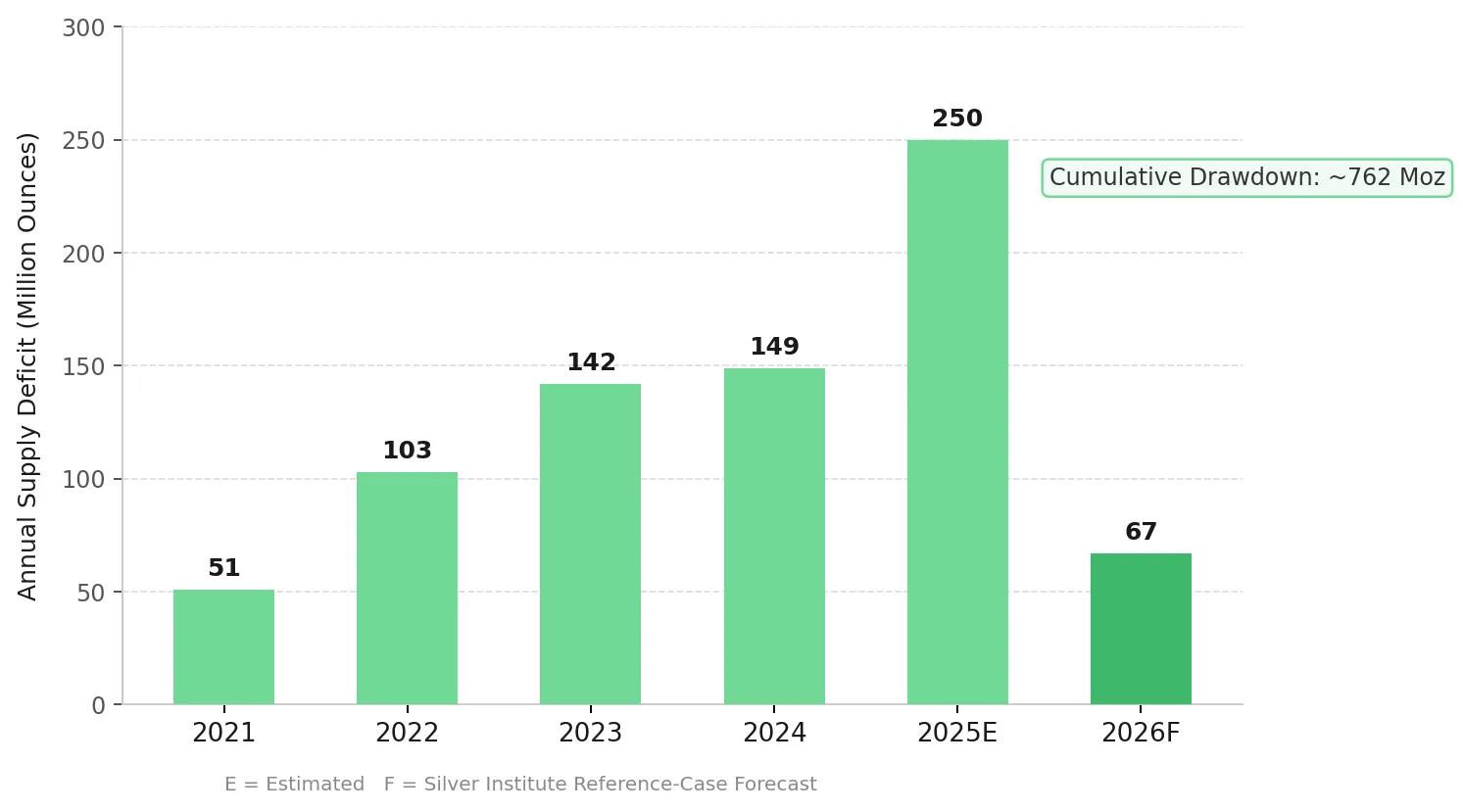

Since 2021, the global silver market has drawn down approximately 762 million ounces from above-ground stockpiles, a cumulative shortfall representing nearly a full year of global production. The Institute's 2026 reference-case deficit projection of 67 million ounces assumes no tariff escalation on Mexican mineral exports and geological production consistent with current revised guidance. In a scenario where Section 301 advances to tariff imposition, a 10% curtailment of Mexican silver output would add approximately 20 million ounces to the annual structural shortfall, pushing the 2026 deficit toward 85 to 90 million ounces. COMEX registered silver inventory data shows a delivery coverage ratio below stress thresholds for six consecutive months as of April 2026. When coverage ratios reach levels at which open interest materially exceeds available registered metal, the mechanisms that normally re-anchor paper and physical prices become impaired, increasing the probability of delivery-driven price dislocations on a non-linear basis.

Section 301 Exposure Bifurcates Silver Equity Risk Between Mexican Explorers & US Producers

The supply geography disruption playing out in 2026 does not affect all silver companies uniformly, and two companies operating on opposite sides of the geographic divide illustrate the practical investment differentiation.

GR Silver Mining Ltd. operates within the direct perimeter of the Section 301 investigation. The company's San Marcial discovery provides the technical quality required to compete against an elevated jurisdictional discount rate. The most recent 2026 step-out drilling returned 15.6 meters at 351 g/t silver, including 2.5 meters at 1,395 g/t silver in drill hole SMS26-03, and 6.45 meters at 498 g/t silver, including 1.2 meters at 1,618 g/t silver in SMS26-01, confirming continuous high-grade mineralization to 500 meters depth in an intermediate to low-sulfidation epithermal breccia system assessed as open for at least a further 100 meters below current intercepts.

Eric Zaunscherb, Executive Chair of GR Silver Mining, ties the current drilling results directly to the H2 2026 Mineral Resource Estimation update:

"These results strengthen our confidence in the continuity of the silver-mineralized system at San Marcial at depth in the SE Area. The successful targeting of these new high-grade intervals has been guided by our technical team's geological work and 3D modelling and provides further support and confidence for the upcoming Mineral Resource Estimation update in the second half of 2026."

Jurisdictional Risk vs. Asset Quality

An active Section 301 investigation increases the discount rate applied to projected cash flows, reducing NPV even as the underlying resource quality improves. GR Silver's existing permits, inherited from the Plomosas underground mine operated by Grupo Mexico from 1985 to 2000, reduce the magnitude of this jurisdictional premium compared to a new concession in Mexico's post-2023 mining law reform, though they do not eliminate it. The 20,000-metre 2026 step-out drilling program and the planned H2 2026 MRE update will be the primary determinants of whether the asset quality case overrides the jurisdictional headwind in institutional valuation models.

The Investment Thesis for Silver

- Investors holding Mexico-exposed silver equities should apply an explicit jurisdictional risk discount to NPV and IRR calculations consistent with standard institutional practice when sovereign or trade risk becomes active in a producing jurisdiction, regardless of the underlying asset's technical quality.

- US-domiciled silver production now carries a policy premium generated by Section 232 reviews, critical minerals designations, and domestic content mandates, creating a valuation floor for permitted, operating producers on US soil that functions independently of spot silver price movements.

- A silver market drawing down over 67 million ounces annually from finite above-ground stockpiles responds to incremental supply curtailment in a non-linear fashion, where a 10% reduction in Mexican output alone adds approximately 20 million ounces to the structural deficit, amplifying the supply impact of tariff escalation beyond its proportional share of global production.

- Exploration-stage developers in jurisdictions under active trade investigation face a dual test in which resource quality measured by grade, width, depth continuity, and scale potential must demonstrably exceed the jurisdictional risk premium at institutional discount rates, with systems supported by existing permit standing and established infrastructure occupying the strongest risk-adjusted position.

- Operating producers executing fully funded capital programs in politically stable jurisdictions represent the lowest-risk, highest-visibility silver equity exposure available in the current environment, with milestone-rich catalyst calendars and critical mineral alignment reducing commodity price dependency in a way exploration-stage assets cannot replicate.

The US Trade Representative’s Section 301 investigation subjects 200 million ounces of annual silver supply to direct tariff risk. This mechanism targets 25% of global mine supply as the market enters its sixth consecutive annual deficit of 67 million ounces. Fund managers are targeting explicit jurisdictional risk discounts in Net Present Value (NPV) and Internal Rate of Return (IRR) models for Mexico-based assets to account for trade escalation following the July 2026 USMCA review. Consequently, Fresnillo PLC has cut its 2026 production guidance by 9% on geological grounds, while COMEX delivery coverage ratios have remained below stress thresholds for six consecutive months.

Washington’s critical minerals agenda and Section 232 reviews are yielding a valuation premium for US-domiciled producers with permitted, operating assets. These assets are targeting a dual-purpose classification as commodity producers and critical infrastructure nodes, creating a valuation floor independent of spot price volatility. By Q4 2026, Americas Gold and Silver is targeting a 150% hoisting capacity increase at the Galena Complex to 105 short tons per hour, converting jurisdictional stability into a per-unit cost reduction of 40% to 50%. For investors, jurisdictional positioning is the primary mechanism for NAV preservation in the 2026 trade cycle.

TL;DR

The US Trade Representative's Section 301 investigation targeting Mexico places approximately 200 million ounces of annual silver supply under direct tariff risk, compounding a sixth consecutive structural deficit already running at 67 million ounces in 2026. Fresnillo PLC has cut production guidance by 9% on geological grounds before any tariff takes effect, while COMEX delivery coverage ratios have remained below stress thresholds for six consecutive months. Washington's critical minerals agenda is simultaneously generating a measurable valuation premium for US-domiciled silver and antimony producers. Mexico-based silver assets now require an explicit jurisdictional risk discount in NPV and IRR models, while permitted, operating US producers with critical mineral alignment represent the most defensible silver equity positioning available in the current environment.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed