US to Classify Silver as a Critical Mineral Signals Strategic Shift for Investors

US proposes silver as critical mineral for first time, creating policy tailwinds for producers amid 14-year price highs and strategic supply concerns.

- The US Geological Survey's 2025 draft list proposes adding silver as a critical mineral for the first time, reframing its role from a precious hedge to a strategic industrial asset.

- If finalized later this year, the designation would unlock stockpiling, permitting support, and potential tax incentives, shifting long-term supply-demand dynamics.

- Silver's industrial uses in solar, EVs, semiconductors, and defense technologies make its supply security a national priority, especially given US reliance on imports and Chinese refining capacity.

- Global supply chains face mounting pressure: Mexico and Peru eye higher royalties, while stable jurisdictions like the US and Canada stand to benefit from policy-driven investment flows.

- With silver prices near 14-year highs, investors are increasingly looking to producers, developers, and explorers with secure, low-cost projects to gain leverage to both policy and price upside.

Policy Shift: Silver Proposed for US Critical Minerals List

The US Geological Survey's 2025 draft critical minerals list marks a fundamental shift in how policymakers view silver. For the first time, the white metal appears alongside lithium, cobalt, and rare earth elements as materials deemed essential to US economic and national security. This inclusion, pending finalization later this year, legally mandates government focus on securing domestic supply chains through enhanced permitting, subsidies, and strategic stockpiling.

The historical context underscores the significance of this change. Previous USGS lists excluded silver, treating it primarily as a monetary asset or jewelry commodity. The new classification acknowledges silver's irreplaceable role in critical technologies from solar photovoltaic cells to defense systems demanding ultra-reliable conductivity. This recognition signals that industrial demand has reached a threshold where supply security becomes a matter of national interest.

The policy shift creates a structural demand layer beyond traditional supply-demand fundamentals. Critical mineral designation historically drives sustained government intervention, as seen with uranium stockpiling and rare earth supply chain initiatives. The implications extend beyond immediate price support to encompass accelerated permitting for domestic projects, tax incentives for production, and potential trade measures protecting strategic supply sources.

National Security & Industrial Demand Drivers

Silver's proposed critical mineral status reflects its expanding role across defense, energy transition, and advanced technology sectors. Defense applications include satellite systems, missile guidance electronics, and high-reliability military communications equipment where silver's superior conductivity and thermal properties are irreplaceable. The metal's antimicrobial properties also make it essential for medical devices and water purification systems used by armed forces.

The energy transition amplifies silver's strategic importance through solar photovoltaic installations, electric vehicle components, and battery technologies. Each solar panel requires approximately 20 grams of silver, while electric vehicles use twice the silver content of conventional vehicles through electrical systems and charging infrastructure. Semiconductor manufacturing depends on silver for high-frequency applications, 5G networks, and artificial intelligence hardware where performance tolerances demand the highest-grade materials.

This industrial demand occurs as the United States imports over 70% of its silver consumption, with significant refining capacity concentrated in China. The geopolitical vulnerability becomes apparent when considering that silver-intensive technologies underpin everything from renewable energy infrastructure to advanced military systems. Critical mineral designation acknowledges that supply disruptions could compromise both climate goals and national defense capabilities.

Stockpiling & Strategic Supply Security

Historical precedent suggests that critical mineral designation triggers sustained government intervention in silver markets. The Strategic Petroleum Reserve, uranium stockpiles, and rare earth supply initiatives demonstrate how national security considerations create durable demand floors. For silver, potential pathways include direct government purchases for strategic reserves, production subsidies for domestic operations, and trade measures securing reliable supply sources.

The stockpiling mechanism operates through multiple channels. The Defense Logistics Agency maintains strategic inventories of materials essential to military operations, while the Department of Energy can authorize purchases supporting clean energy infrastructure. Congressional appropriations for critical mineral stockpiles have historically created multi-year procurement programs that establish price floors and reduce market volatility for strategic commodities.

Global implications extend beyond US policy as allied nations mirror American initiatives. The European Union's Critical Raw Materials Act and Japan's mineral security strategies suggest coordinated efforts to reduce dependency on potentially hostile suppliers. This multilateral approach could tighten global silver markets as governments compete for secure supply sources, creating sustained upward pressure on prices and valuations for producers in stable jurisdictions. The policy framework particularly benefits producers already generating critical metals alongside silver production. Paul Huet, Chief Executive Officer of Americas Gold & Silver, quantifies this strategic positioning:

"We're the only producer of it [antimony]. Everybody around me has got grants. I'm the only one producing it, so you think that's not an opportunity for us?"

Global Supply Risks & Jurisdictional Premiums

Resource nationalism intensifies across major silver-producing jurisdictions as governments seek greater economic benefits from mineral extraction. Mexico's proposed mining reforms target higher royalty rates and increased state participation, while Peru evaluates tax regime changes affecting mining operations. These policy shifts create operational uncertainty and potentially higher costs for producers, amplifying the value premium attached to jurisdictionally stable projects.

Supply-side headwinds compound jurisdictional risks through declining ore grades, higher capital expenditure requirements for new mines, and extended permitting timelines. The average silver grade of global mines has decreased approximately 30% over the past decade, requiring greater volumes of ore processing to maintain equivalent metal output. New mine development faces capital intensity challenges, with recent projects requiring 500-800 million dollars in initial investment for large-scale operations.

Investor capital increasingly demands jurisdictional stability alongside economic returns. Projects in Canada, Australia, and stable US states command valuation premiums reflecting reduced political risk and predictable regulatory environments. This premium widens during periods of resource nationalism, as institutional investors prioritize secure cash flow visibility over potentially higher-return but politically vulnerable assets. The strategic reality creates distinct investment categories within silver equities, with secure-source producers trading at enterprise value per ounce premiums reflecting supply chain reliability.

Financial Strength & Operational Catalysts

Capital markets reward silver companies with robust balance sheets and near-term operational visibility as institutional investors seek exposure to the sector's fundamental drivers. Key financial metrics include All-in Sustaining Costs below 15 dollars per ounce, debt-to-equity ratios under 30%, and cash positions sufficient to fund development through production without dilutive equity raises. These criteria separate well-positioned companies from those vulnerable to commodity price volatility or financing constraints.

Net Present Value calculations increasingly incorporate policy upside from critical mineral designation, with discount rates reflecting jurisdictional stability and operational risk profiles. Internal Rate of Return thresholds range from 15-25% depending on political risk, while Enterprise Value per ounce metrics vary significantly between development stages and jurisdictions. Market capitalization relative to resources guides valuation efficiency, with institutional investors favoring companies trading below replacement cost for similar-quality projects.

Development timelines aligned with multi-year demand growth trends create catalyst-driven investment opportunities. Feasibility studies, construction decisions, and production ramp-ups provide defined inflection points for equity performance. Companies with fully funded development plans through first production avoid execution risk associated with commodity price-dependent financing, particularly valuable during volatile market conditions. Vizsla Silver exemplifies systematic development execution with a comprehensive approach to de-risking. Jesus Velador, Vizsla Silver Vice President of Exploration, outlines the operational strategy:

"Our strategy is a dual strategy. We have the plan of developing the mine in Copala Napoleon this year. We started already with a test mine."

Market Repricing at 14-Year Highs

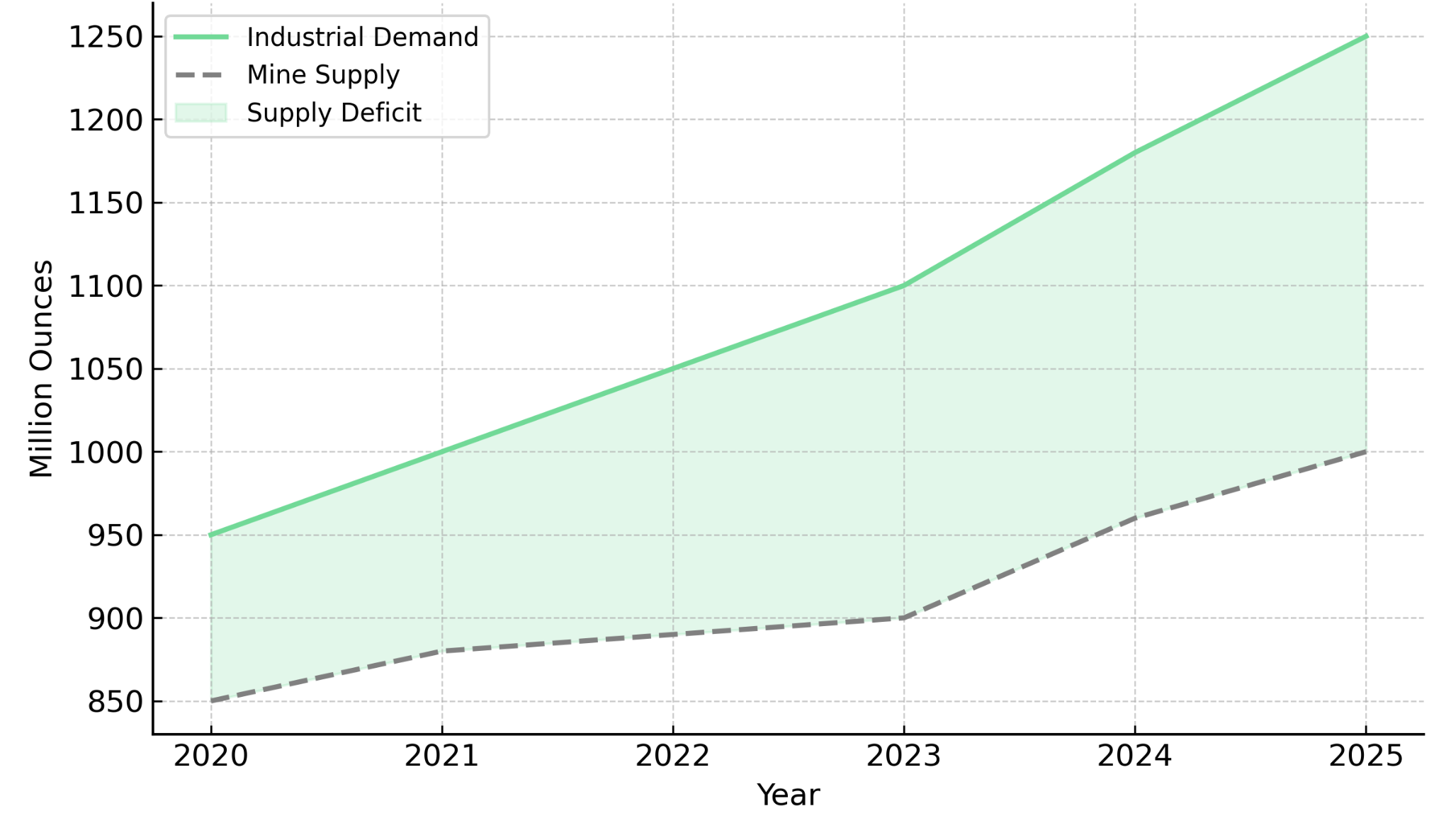

Silver prices reaching 31-34 dollars per ounce reflect persistent supply deficits coinciding with accelerating industrial demand growth. The Silver Institute estimates annual deficits exceeding 200 million ounces through 2025, driven by photovoltaic installations, electric vehicle production, and semiconductor manufacturing expansion. These structural imbalances occur as mine production growth stagnates due to grade decline, permitting delays, and capital allocation challenges across the mining sector.

Exchange-traded product inflows signal institutional rotation into physical silver exposure as investors position for both monetary debasement and industrial demand themes. Global silver ETF holdings approach 1 billion ounces, representing approximately 40% of annual mine production. This financial demand layer adds price sensitivity to supply disruptions, as liquidation becomes necessary during physical shortages affecting industrial consumers.

Dollar weakness amplifies international silver demand as emerging market buyers increase precious metals allocations. Central bank diversification away from dollar reserves creates secondary demand for monetary metals, while inflation expectations drive retail investment in tangible assets. The combination of monetary and industrial demand creates dual support mechanisms rarely seen in commodity markets.

Alternative Supply Pathways & Resource Innovation

Traditional mining faces increasing cost pressures and environmental scrutiny, creating opportunities for innovative extraction methods. Reprocessing historical tailings and stockpiles offers lower-risk pathways to metal production, particularly where previous operations discarded valuable byproducts due to technological limitations or unfavorable commodity prices. These alternative approaches eliminate exploration risk while accessing proven resources at fraction of conventional development costs.

The technical advantage of reprocessing operations extends beyond cost savings to encompass reduced environmental impact and accelerated production timelines. Surface-based extraction avoids underground mining complexities while utilizing existing infrastructure and established metallurgical processes. This operational efficiency becomes particularly valuable during periods of heightened regulatory scrutiny and extended permitting timelines affecting traditional mining projects.

Companies pursuing reprocessing strategies demonstrate exceptional resource grades that justify capital investment and operational focus. Historical tailings from polymetallic operations often contain silver grades exceeding current underground mines, reflecting past processing limitations rather than geological constraints. Modern recovery techniques can extract previously uneconomical metals, creating additional revenue streams that improve project economics and reduce commodity price sensitivity. Alternative supply pathways demonstrate exceptional resource quality that supports sustained production profiles. Cerro de Pasco Resources has identified historical tailings with extraordinary silver content, as explained by Guy Goulet, Cerro de Pasco Resources Chief Executive Officer:

"These tailings are the richest in the world. You take the average of the tailing, the polymetallic, you put that in silver equivalent, it's more than the average of the underground mine on the planet, and it's above ground."

High-Grade Resource Expansion & Exploration Upside

Exploration success in established silver districts provides leverage to rising commodity prices while demonstrating resource expansion potential beyond initial feasibility studies. High-grade intersections in epithermal systems indicate robust mineralization that can support long-term mining operations and justify capital investment in processing infrastructure. Recent drilling results across various projects suggest that systematic exploration in proven geological environments continues to yield significant discoveries.

The geological characteristics of epithermal silver systems support continued resource expansion through step-out drilling and deeper exploration targets. Boiling textures and mineral assemblages indicate proximity to feeder zones that typically host higher grades and broader mineralization widths. These geological indicators guide exploration programs toward areas with greatest discovery potential, maximizing return on exploration investment while building confidence in long-term resource sustainability.

Market recognition of exploration success creates valuation upside as institutional investors seek exposure to resource growth potential in established mining districts. Companies demonstrating consistent drilling success attract premium valuations reflecting both current resource estimates and blue-sky exploration potential. This valuation framework rewards systematic exploration programs that expand resources while maintaining grade quality and metallurgical characteristics suitable for efficient processing. GR Silver Mining's recent drilling results demonstrate the discovery potential within established epithermal systems. Marcio Fonseca, Chief Executive Officer of GR Silver Mining, highlights the geological significance:

"The most recent news release, which was the 75 meters at 293 grams per ton of silver equivalent at the San Marcial area…This hole brought up fresh information about the epithermal system, boiling textures that carry a lot of silver, kilos of silver."

The Investment Thesis for Silver

- Policy Tailwind Alignment: Proposed US critical mineral designation unlocks government stockpiling, accelerated permitting, and production subsidies that create sustained demand increments beyond traditional market fundamentals.

- Industrial Demand: Clean energy infrastructure, electric vehicle adoption, and defense technology expansion anchor multi-year silver consumption growth that exceeds current mine production capacity.

- Jurisdictional Premium Recognition: Producers and developers in stable regulatory environments command valuation premiums as resource nationalism increases operational risk in major mining jurisdictions.

- Operational Leverage Optimization: Companies maintaining All-in Sustaining Costs below 12 dollars per ounce with funded development catalysts provide amplified exposure to price appreciation and policy-driven demand growth.

- Catalyst Pipeline Monetization: Feasibility studies, construction decisions, and production ramp-ups create defined inflection points for equity performance while exploration success provides blue-sky upside potential in an underexplored commodity sector.

Silver at the Intersection of Policy & Market Forces

The US Geological Survey's proposal to designate silver as a critical mineral represents a paradigm shift from monetary asset to strategic industrial commodity. This recognition, pending finalization later in 2025, acknowledges silver's irreplaceable role in national security technologies, clean energy infrastructure, and advanced manufacturing systems that underpin economic competitiveness.

Policy support, structural supply deficits, and accelerating industrial demand create unprecedented investment dynamics in silver markets. Government stockpiling, production incentives, and supply chain security measures provide sustained demand growth independent of economic cycles, while traditional precious metals investors add industrial demand themes to their positioning rationale.

For institutional investors, positioning in secure, well-funded silver equities offers leveraged exposure to both policy implementation and commodity price appreciation. Companies operating in stable jurisdictions with low-cost production profiles and funded development catalysts provide optimal risk-adjusted returns in an increasingly strategic sector. The dual nature of silver as both monetary hedge and industrial necessity creates unique value propositions rarely available in commodity markets, positioning the sector for sustained outperformance as policy frameworks evolve to address supply security imperatives.

TL;DR

The US Geological Survey's 2025 draft proposal to classify silver as a critical mineral marks a paradigm shift from precious metal to strategic industrial asset. This designation, pending finalization later this year, would unlock government stockpiling, production subsidies, and accelerated permitting for domestic projects. Silver's essential role in solar panels, electric vehicles, semiconductors, and defense systems makes supply security a national priority, especially given 70% import dependence and Chinese refining dominance. With prices at 14-year highs and annual deficits exceeding 200 million ounces, investors are positioning in well-funded silver producers and developers with secure jurisdictions and low-cost operations. The policy creates structural demand beyond traditional market fundamentals while addressing geopolitical vulnerabilities in critical technology supply chains.

FAQs (AI-Generated)

Critical mineral status would unlock government stockpiling, production subsidies, and accelerated permitting, creating sustained demand beyond traditional market cycles while potentially establishing price floors through strategic purchases.

Silver's expanding role in clean energy, electric vehicles, semiconductors, and defense technologies has reached a threshold where supply disruptions could compromise national security and climate goals, prompting government recognition of its strategic importance.

Companies with domestic US production, low-cost operations in stable jurisdictions, and funded development projects would benefit most, as they align with supply chain security objectives while offering operational leverage to policy-driven demand.

Industrial applications now consume over 50% of silver supply through irreplaceable uses in solar panels (20g each), electric vehicles, and high-frequency electronics, creating inelastic demand unlike jewelry or investment applications.

The proposal requires finalization later in 2025 and faces potential political opposition, budget constraints for stockpiling programs, and competition from other strategic priorities in government resource allocation.

Analyst's Notes

Subscribe to Our Channel

Stay Informed