Americas Gold and Silver's 98% Surge in Silver Output Signals Operational Turnaround & Strategic Leverage to North American Supply Deficits

- Americas Gold and Silver delivered a 98% year-on-year increase in quarterly silver production to 765,000 ounces in Q3 2025.

- Operational improvements at the Galena Complex in Idaho and Cosalá Operations in Mexico drove record efficiency gains despite a planned 10-day shutdown.

- The company's position as the only current producer of antimony in the United States offers critical mineral leverage amid rising geopolitical supply risk.

- Backed by a robust balance sheet with $39 million cash as of September 30, 2025, and $50 million undrawn credit facility, the company is fully funded for growth.

- The 98% output surge validates management turnaround strategy under Chief Executive Officer Paul Huet, reinforcing Americas' emerging re-rating potential.

From Turnaround to Traction

The sharp improvement in Americas Gold and Silver's production profile reflects a broader shift underway in the silver sector, where capital discipline and operational optimization are overtaking expansion narratives as key investment drivers.

In Q3 2025, the company delivered a 98% increase in silver output compared to Q3 2024, alongside 2.3 million pounds of lead production, marking a clear inflection point in its multi-year turnaround strategy. The gains came despite a planned 10-day shutdown in September to complete Phase 1 upgrades to the Galena Number 3 Shaft, highlighting both execution depth and asset resilience.

For investors, the significance extends beyond quarterly data. The results demonstrate that Americas is now entering the cash-flow scaling phase, leveraging operational stability, ownership consolidation completed on December 19, 2024, and exposure to critical minerals to reposition as a mid-tier North American producer.

The Market Context: Tight Silver Supply Meets Strategic Metals Policy

Silver's sustained market deficit has sharpened investor focus on producers with scalable output and jurisdictional safety. Primary producers like Americas Gold and Silver stand to capture asymmetric upside when price elasticity fails to trigger supply response from base metal by-product operations.

The metal's dual role as both an industrial input and monetary hedge has intensified demand dynamics. Solar panel manufacturing, electric vehicle components, and electronics fabrication continue to drive structural consumption growth, while investment demand remains sensitive to monetary policy uncertainty.

United States & Allied Push for Critical Mineral Independence

Parallel to silver, antimony has re-entered strategic relevance lists across the United States and Europe due to its defense, semiconductor, and energy storage applications. Over 90% of global antimony supply is imported, mainly from China, Russia, and Tajikistan.

Americas Gold and Silver's Galena Complex in Idaho represents the only current producer of antimony in the United States, with zero operating primary antimony mines elsewhere domestically. This positions the company at the intersection of silver leverage and strategic-metal scarcity.

Operational Execution: Galena Complex Performance

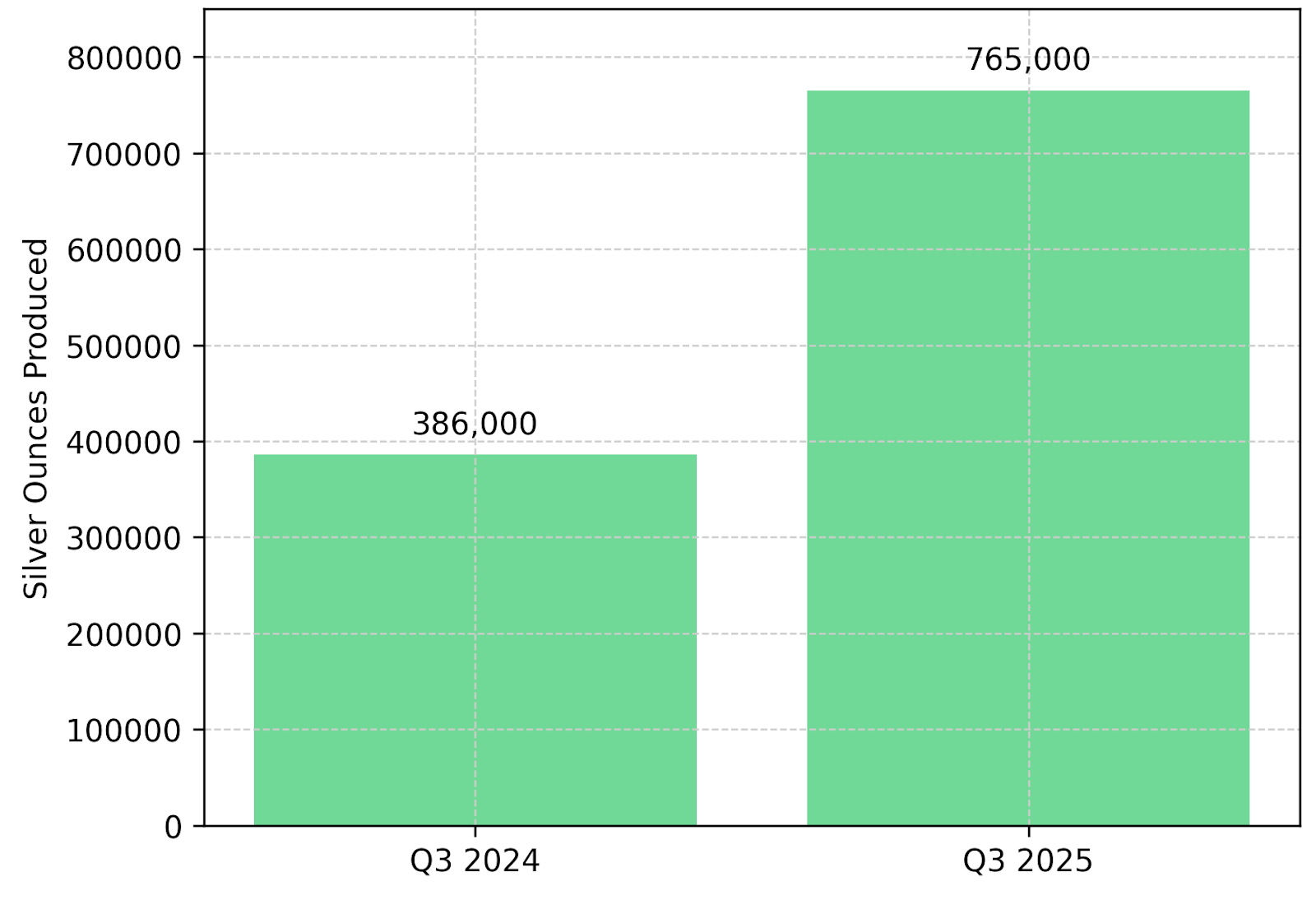

At the Galena Complex, production rose sharply due to systematic underground upgrades and process optimization. Q3 2025 marked 765,000 ounces of silver output, representing a 98% increase compared to 386,000 attributable ounces in Q3 2024. The year-over-year comparison reflects both operational improvements and the company's increased ownership stake from 60% to 100% following consolidation completed on December 19, 2024.

Silver Production YoY (Q3 2024 vs Q3 2025).The production gains were underpinned by the reintroduction of long hole stoping, new underground fleet deployment, and Phase 1 upgrades to the Number 3 Shaft completed in September 2025. The planned 10-day shutdown in September to complete these upgrades did not prevent sequential quarter-on-quarter growth, demonstrating operational discipline.

Oliver Turner, Executive Vice President of Corporate Development of Americas Gold and Silver, detailed the shaft upgrade impact:

"We've replaced the hoist motor on top of the Number 3 Shaft with a 2,250 horsepower motor. That's about a 500 horsepower increase over the 1,750 horsepower motor that was there before. That allows us to hoist faster and hoist heavier loads. We've had some record days in terms of hoisting."

The Phase 1 shaft upgrades doubled skipping capacity from 40 tons per hour to 80 tons per hour. Engineering specifications indicate that once Phase 2 upgrades are complete, the system is expected to achieve approximately 118 tons per hour. Phase 2 plans include brake upgrades and hoisting speed increases from 690 feet per minute to between 1,200 and 1,400 feet per minute.

Ownership Consolidation & Long-Term Upside

The company's consolidation to 100% ownership of Galena on December 2024, enhances operational control, mine planning efficiency, and attributable cash flow. The mine, with an average grade of 480 grams per tonne silver, ranks as the third highest-grade silver mine globally according to company analysis.

Recent drilling results demonstrate exploration upside. On April 2025, drill hole 52-583 intersected 983 grams per tonne silver and 0.74% copper over 3.44 meters in the high-grade 034 vein. On August 22, 2025, drill hole 43-317 identified 24,913 grams per tonne silver and 16.9% copper over 0.21 meters in the 149 vein extension.

Cosalá Operations: Low-Cost Silver Growth

The Cosalá Operations in Sinaloa, Mexico, complement Galena's output with stable production. The transition to the high-grade EC120 zone targets expected cash costs of approximately $9.60 per silver ounce and all-in sustaining costs of $10.80 per ounce. By utilizing established processing infrastructure including the Los Braceros mill, Americas Gold and Silver minimizes new capital expenditures.

Management plans to increase annual silver production to approximately 2.5 million ounces over five years at the targeted cost level. This production profile provides cash flow stability and operational diversification, reducing dependence on any single asset.

Critical Metals Leverage

Americas Gold and Silver's Galena Complex is currently the only producer of antimony in the United States. Through the first three quarters of 2025, Galena produced 447,466 pounds of antimony and 615,817 pounds of copper. Consolidated lead production for Q3 2025 was 2.3 million pounds.

Antimony is essential in flame retardants, lead-acid batteries for defense applications, semiconductor manufacturing, and energy storage technologies. With over 90% imported mainly from China, Russia, and Tajikistan, Western governments have designated antimony as a critical mineral requiring domestic production capacity.

Turner emphasizes:

"This is actually the only producing antimony mine in the United States of America. Galena is the only producing source of antimony in the United States. That cannot be understated."

Unlocking Value Through Metallurgy

Metallurgical testing completed on September 8, 2025, demonstrated 99.8% antimony recovery from copper concentrate flotation extraction, advancing from earlier May 2025 testwork that achieved 90% recovery rates. The breakthrough testwork positions the company to advance toward commercial recovery evaluation and refining options.

An offtake agreement secured with Ocean Partners in June 2025 provides commercial certainty for 100% of Galena concentrates at Teck's Trail Operations, ensuring capacity for silver, lead, and critical metals.

Turner quantified the revenue opportunity:

"We're getting 99% recoveries of antimony… Not only are we an expanding silver producer, we're an expanding antimony producer. Production is going to be going up over the next several years… What does that mean for shareholders? It means significantly larger by-product credits. You're expanding your margin."

Financial Health & Capital Deployment

Americas Gold and Silver maintains a robust financial position enabling continued investment without near-term dilution risk. As of September 30, 2025, the company reported $39 million in cash, with $50 million remaining undrawn on its credit facility. A $100 million debt package finalized in May 2025 and closed in June 2025, provided non-dilutive funding, with $50 million received at closing and two subsequent $25 million tranches available.

With 272 million common shares outstanding as of September 26, 2025, and over 60% held by institutions and insiders, alignment between management and shareholders remains high. Eric Sprott holds approximately 20%, while institutional ownership stands at 31%.

Turner addressed the investment timing:

"There was a significant amount of investment required to get there, which is why we raised the $50 million in October and the $100 million of debt in June of this year... This year has been investment in equipment… The cash flow generation inflection point after this year of investment, 2026 is going to be a fantastic year."

Management Execution & Strategic Track Record

Chief Executive Officer Paul Huet brings a demonstrated record of transforming underperforming assets. At Klondex Mines, the team delivered a sale to Hecla Mining for C$740 million in 2018. At Karora Resources, the team executed a merger with Westgold valued at C$2.1 billion in 2024.

Huet's team is replicating the operational transformation formula through tightened cost control, upgraded infrastructure, and production growth aligned with balance sheet strength. The approach emphasizes systematic execution over promotional narratives.

Market Comparison & Valuation Implications

Compared with North American peers including Hecla Mining, First Majestic Silver, and Aya Gold & Silver, Americas Gold and Silver trades at a discount on enterprise value metrics relative to its asset quality. The company's high-grade profile at Galena, ranked third globally at 480 grams per tonne, provides structural cost advantages not fully reflected in current valuations.

Several near-term catalysts could drive valuation uplift. Completion of Phase 2 shaft upgrades will demonstrate full throughput capacity. Advancement toward commercial-scale antimony recovery will add income streams highlighting the strategic mineral premium. Sustained production growth will establish the company as a mid-tier producer attracting broader institutional attention.

The Investment Thesis for Silver & Strategic Metals

The investment case for Americas Gold and Silver combines operational execution, strategic positioning, and financial discipline:

- Proven operational turnaround with Q3 2025 results validating management execution capability and systematic achievement of production targets, demonstrating transition from restructuring to scaling phase.

- High-grade silver leverage through Galena Complex, ranked third globally among silver mines by grade at 480 grams per tonne, providing direct exposure to silver price appreciation with scalable volume upside as infrastructure upgrades unlock throughput expansion.

- Exclusive United States antimony production positioning the company as the only current domestic producer of antimony, introducing scarcity premium aligned with Western critical minerals policy and supply chain security initiatives.

- Fully funded growth trajectory with $39 million cash as of September 30, 2025, $50 million undrawn credit facility, and $100 million debt package eliminating short-term equity dilution risk and supporting organic expansion.

- Institutional investor confidence reflected in over 60% institutional and insider ownership led by Eric Sprott's approximate 20% stake as of September 26, 2025, anchoring alignment between management strategy and shareholder value creation.

- Potential for valuation re-rating with current metrics appearing disconnected from operational improvements and strategic positioning, offering leveraged upside as production milestones translate into sustained cash flow generation.

A Re-Rating Story Built on Execution

Americas Gold and Silver's Q3 2025 performance underscores a turning point from operational rehabilitation to consistent, scalable production growth. The 98% increase in quarterly silver production, achieved despite planned maintenance downtime, demonstrates that the multi-year turnaround strategy has transitioned from planning to measurable execution.

With high-grade silver assets ranked third globally, strategic critical mineral leverage as the only current United States antimony producer, and full funding visibility through non-dilutive capital sources, the company's operational fundamentals now align with market conditions favoring disciplined producers. The combination of proven management, institutional shareholder support including Eric Sprott's significant position, and systematic achievement of production milestones positions Americas as a differentiated investment opportunity.

TL;DR

Americas Gold and Silver's Q3 2025 results represent a decisive operational inflection point, with 98% year-over-year silver production growth to 765,000 ounces validating a multi-year turnaround under Chief Executive Officer Paul Huet. The company consolidated 100% ownership of Idaho's Galena Complex on December 19, 2024, which now ranks as the third highest-grade silver mine globally at 480 grams per tonne. Phase 1 shaft upgrades completed September 16, 2025, doubled hoisting capacity from 40 to 80 tons per hour despite a 10-day shutdown. As the only current U.S. antimony producer, Americas offers unique critical mineral exposure, with September 8, 2025, breakthrough metallurgical testing demonstrating 99.8% antimony recovery. The company maintains $39 million cash as of September 30, 2025, $50 million undrawn credit, and $100 million debt financing closed June 2025, fully funding the pathway to anticipated 2026 cash flow inflection.

FAQs (AI-generated)

Americas Gold and Silver operates the only current producer of antimony in the United States at its Galena Complex in Idaho, with zero other operating primary antimony mines domestically. With over 90% of global antimony supply imported mainly from China, Russia, and Tajikistan, Western governments have designated antimony as a critical mineral essential for defense applications, semiconductors, and energy storage technologies. The company's September 8, 2025, breakthrough metallurgical testing demonstrated 99.8% antimony recovery rates from copper concentrate flotation extraction, advancing from earlier May 2025 testwork that achieved 90% recovery. An offtake agreement secured with Ocean Partners in June 2025 provides commercial certainty for 100% of Galena concentrates at Teck's Trail Operations, positioning the company to monetize this strategic mineral as production scales.

Phase 1 upgrades to the Galena Number 3 Shaft, completed on September 16, 2025, doubled skipping capacity from 40 tons per hour to 80 tons per hour. The hoist motor was upgraded from 1,750 horsepower to 2,250 horsepower, enabling faster hoisting speeds and heavier loads. Engineering specifications indicate that once Phase 2 upgrades are complete, the system is expected to achieve approximately 118 tons per hour from the deepest loading pockets. Phase 2 plans include brake upgrades and hoisting speed increases from 690 feet per minute to between 1,200 and 1,400 feet per minute. Combined with the reintroduction of long hole stoping and new underground fleet deployment, these improvements enable expansion from current operational levels of 300-350 ore tons per day toward substantially higher throughput supporting management's stated production targets.

The Cosalá Operations in Sinaloa, Mexico, target expected cash costs of approximately $9.60 per silver ounce and all-in sustaining costs of $10.80 per ounce over the planned five-year production period of approximately 2.5 million ounces annually. At the Galena Complex, substantial by-product credits from antimony, copper, and lead reduce the effective cost of silver production and provide margin expansion independent of silver price movements. The company's high-grade position at Galena, ranked third globally at 480 grams per tonne silver according to company analysis, provides structural cost advantages through higher metal content per ton of ore processed. The combination of low-cost Mexican operations and high-grade Idaho production positions Americas competitively within its peer group as infrastructure upgrades complete and production scales.

Americas Gold and Silver reported $39 million in cash as of September 30, 2025, with $50 million remaining undrawn on its existing credit facility. The company secured a $100 million long-term debt package that was finalized in May 2025 and closed in June 2025, receiving $50 million at closing with two subsequent $25 million tranches available for deployment into Galena growth initiatives. This capital structure provides non-dilutive funding for Phase 2 shaft upgrades and ongoing operational investments while protecting existing shareholders from near-term equity issuance. With 272 million common shares outstanding as of September 26, 2025, and over 60% held by institutions and insiders including Eric Sprott's approximate 20% stake, the ownership structure demonstrates alignment between management and shareholders while maintaining balance sheet strength to execute the multi-year growth plan through the anticipated 2026 cash flow inflection point.

Several near-term catalysts could support valuation convergence as the company transitions from turnaround to steady-state production. Successful completion of Phase 2 Galena shaft upgrades will demonstrate full throughput capacity and validate the production scaling trajectory. Advancement toward commercial-scale antimony recovery and monetization, building on the September 8, 2025, breakthrough testwork showing 99.8% recovery rates, will add a differentiated income stream highlighting the strategic mineral premium embedded in the asset base. Sustained production growth supported by long hole stoping implementation and infrastructure optimization will establish the company as a mid-tier producer with scale sufficient to attract broader institutional investor attention. Demonstrated cost performance as operations reach target levels will support margin expansion and cash flow visibility. Additional catalysts include continued high-grade drilling results building on the April 22 and August 22, 2025, discoveries in the 034 and 149 veins, which support resource expansion potential and mine life extension at Galena's third-ranked global grade profile of 480 grams per tonne silver.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).jpg)

Stay Informed