Analyst's Notes: When Facts Change, Change Your Mind

This week, we have chosen to focus on companies we have previously analysed to see if new data will change our conclusions.

We are committed to helping investors come to grips with the resources sector and learn how to interpret news releases made by companies. In these Analyst’s Notes, we illustrate how news from companies affects the investment case for the stock, and how it can affect peers as well. The topics are selected based on what the analysts think is both relevant and informative to you, the investor.

Before making comments, please ensure you have read the whole article and the FAQs at the bottom.

This week, we have chosen to focus on companies we have previously analysed to see if new data will change our conclusions.

Introduction

John Maynard Keynes (English economist) famously said, “When the facts change, I change my mind. What do you do?”.

Given that there have been a number of news releases on companies that have been covered in previous Analyst’s Notes, we thought it sensible to review the data and see whether we needed to revise our conclusions. Or not, as the case might be.

- Here we check in on Victoria Gold, to see how gold production at the Eagle heap leach mine has fared over the winter.

- In January we took a lot of flak from Excelsior Mining shareholders for daring to point out the Gunnison ISM copper project had run into technical difficulties, so it is worth seeing if the company is proving us wrong.

- Finally, we went back to look at New Found Gold Corporation, as the share price goes from strength to strength on news flow.

General Conclusions

We keep looking for good projects in which to put our money. We do not get it right all of the time, but we know what we like: good geology, sensible management, a decent plan, and a valuation that has not run too far ahead already. Is that too unreasonable? Sadly, this update notes that the latter two do not match these criteria.

Victoria Gold

Having reviewed all of the new information, we note that the Eagle Mine is well on the way up in the Yukon. As expected, the winter months caused a drop (37% q-o-q) in production but steady stacking rates should lead to production increases ahead. The share price has risen by 19% since our note in late January, versus a 5% drop in the gold price, and a 1% rise in the GDX index. Markets are forward-looking, and the company now has a market capitalisation of C$968 million. Punchy.

Excelsior Mining

Excelsior Mining has yet to produce an operational update to show that it has solved its technical problems and that the sunny uplands of commercial and profitable production have been reached.

New Found Gold

New Found Gold alarms us. The share price has gone up on what has been taken by the market to be good exploration news. Unfortunately, a close look at the data (you’re welcome) highlights extremely difficult geology, and the releases carry a whiff of smearing and selective reporting, which is not a Good Thing.

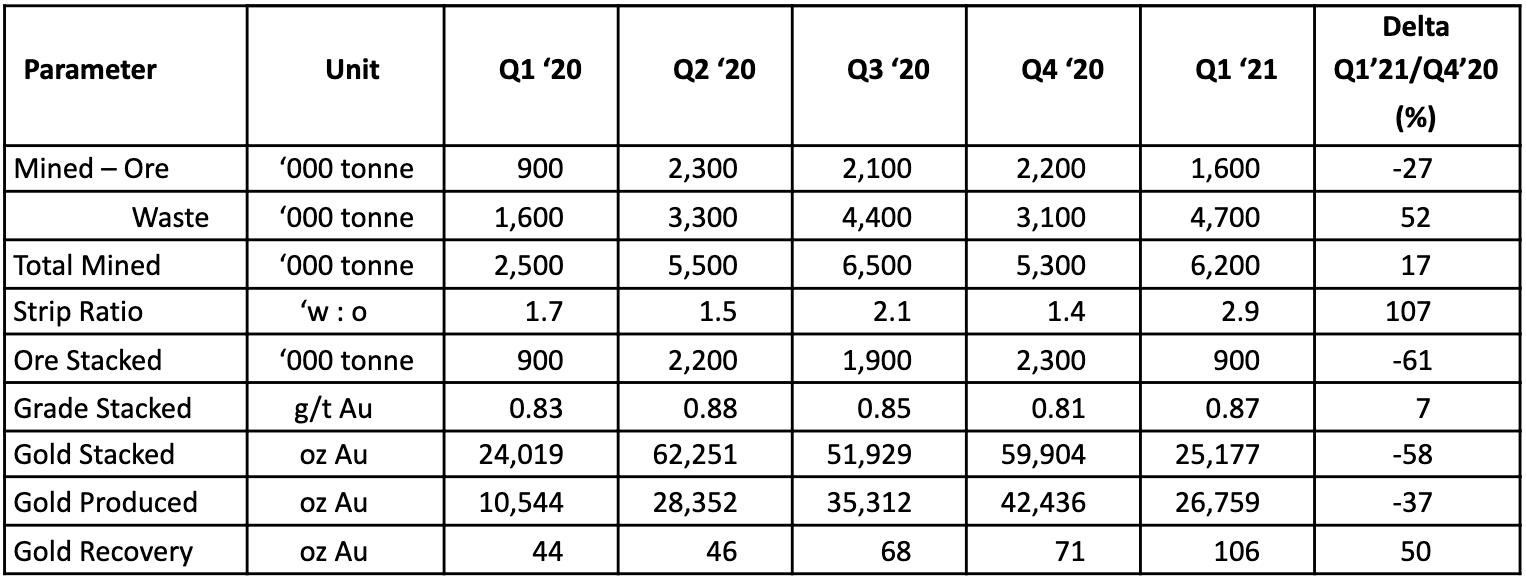

Victoria Gold Production Performance

Table 1 shows Q1 2021 production numbers from the Eagle Mine, relative to last years’ production figures.

The changes in comparison to Q4 2020 show:

- Total mine production increased further by 17%, but focusing on waste stripping, probably to minimise on future ore rehandling by avoiding unnecessary stockpile built-up. This caused the strip ratio to more than double.

- Stacking fell more than 60%, which was expected as the company planned to stop stacking in the coldest months to prevent freezing of the leach solution. In fact, the amount stacked was better than expected with “ore stacking resuming ahead of schedule”.

- The stacked grade in the first quarter grade was slightly higher than the preceding quarter so the fall in stacked gold is less than 60%. Because leached gold arrives at the plant with some delay, the recovery in Q1 2021 was 107%, which reflects the recovery of some of the gold stacked in Q4 2020. The corollary is that recovery in Q2 will be slightly below normal as some of the gold stacked in the quarter not yet available for precipitation.

- The overall effect has been a drop in gold produced of 37% compared to Q4 2020. In the first Analyst’s Notes published on 21 January 2021 we warned that this would happen and may well disappoint shareholders. However, from now on the steady-state stacking rate can be expected with much higher gold production in the coming months.

The share price has risen by 19% since our note in late January, versus a 5% drop in the gold price, and a 1% rise in the GDX index. Markets are forward looking, and the company now has a market capitalisation of C$968 million. Punchy.

Excelsior Mining Production Performance

The Analyst’s Notes dated 27 January 2021 warned readers that the announcement of first cathode production at Gunnison was more of a marketing ploy than an indication of technical success. The note pointed to a number of high-risk factors that should be of concern, which drew the ire of online commentators.

In particular, the conclusions came under heavy criticism by a “Mr Goldfinger” on 4 February on CEO.CA. We wrote a subsequent rebuttal (Analyst’s Notes, 8 February 2021) and it included the statement that “If management feels the need to clear up any misunderstanding in the public market now, it can publish updates about copper production and what the inputs and costs for the first couple of months of production have been”.

No production numbers have been published, but the company completed in February a C$31.7 million capital raise that was flagged in December. We await a technical update from the company with interest.

New Found Gold Drill Results

The third Analyst’s Note, published on 8 February 2021, reviewed the Queensway project of New Found Gold, with one cross-section updated for drill results released on 11 February 2021.

The company had reported spectacular grade intercepts, particularly for the Keats zone. It had caused the share price to dramatically increase in a couple of months with the market capitalisation reaching C$0.51 billion by publication date. This converted to an estimated US$1,000/oz of the gold content based on a back of an envelope estimation, which would even be high for Measured and Indicated Resources. We therefore questioned whether the market had not got ahead of itself.

Since 11 February New Found has drilled at least 26 additional holes and released assay results for 34 drillholes, more than doubling the results available at the publication date of the first report and again with some phenomenal grade intercepts. It managed to further excite the market, increasing the share price for a market capitalisation of C$0.94 billion on 27 April 2021.

We have since reviewed the new information to determine whether or not we should revise our conclusion about the market getting ahead of itself. The review also brings up a number of issues referred to the Analyst’s Notes published on 16 February 2021 about “How to Read Drill Results and Things to Watch Out for”:

- Gaps in drillhole numbering.

- Drilling holes very close to a previous hole with good intersection.

- Projecting the extent of mineralised zones in an exaggerated fashion.

- Smearing of short high-grade intercepts.

Geological Background of the Keats Zone of the Queensway Project

Figure 1 shows the exploration targets of the Queensway project to illustrate that, according to New Found Gold, the mineralisation is very much controlled by structure.

On a macroscopic scale, the intersections of the ENE and NNE faults with the Appleton Fault Zone and JBP (Joe Batts Pond) Fault Zone identified on the map have historically shown to be favourable locations for gold mineralisation. The location of the Keats Zone is shown as being on such an intersection and one would expect the drill results to also reflect an ENE control in addition to NNE control.

Drill Results for the Keats Zone

This section will only review the results announced by New Found Gold (TSX: NFG) for the Keats Zone as other attractive results, especially for Lotto, do not yet amount to a substantial target.

However, identification of holes drilled at targets other than Keats is still important as New Found Gold does not in its drill hole numbering distinguish at what target it was drilled. Rather than having in its numbering a prefix identifying the target, and keeping the numbering sequentially for each target, the company chose to number the holes sequentially, irrespective where drilled. Nothing inherently wrong with that, but it does make it harder for analysts to figure out.

Please stick with us for this next bit – it is boring but important. If you feel your eyes glaze over, just think of your wallet. These tables and graphs could be the difference between you making or losing money if you are prepared to digest them.

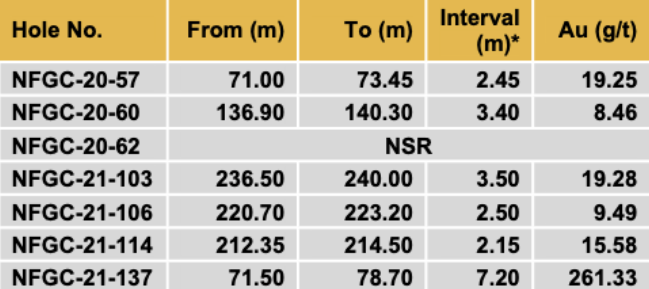

Table 2 includes all drillholes reported by New Found Gold at all targets (irrespective of drilling year). All holes have been included to enable the identification of gaps in the numbering. The highest drillhole number we could find is from a longitudinal section provide by New Found Gold in the press release dated 20 April 2021. The same section was used to identify holes drilled with assay results pending.

.png)

Apart from its length, we can see some key features in this table. Here is what you should pay attention to:

Limited strike extent

Apart from two isolated drillholes 63 and 88, all other drillholes have been drilled over a limited strike extent of less than 300 m (between 4625 m north and 4900 m north).

Missing drill results

Drillhole results have been consistently reported up to hole 46. No results could be found for hole 48, but it is reflected as a low-grade interception on the longitudinal section.

Numerous pending results

There are numerous holes that we could identify on the latest available longitudinal section but for which results are apparently pending. The hole numbers highlighted yellow-brown are those that could not be identified on any of the illustrations which could mean that they have been drilled at any of the other targets, or New Found Gold did not bother to plot these yet.

Noticeable is the increasing frequency of yellow-brown highlighted cells. Does this mean New Found Gold is refocusing elsewhere (which in itself would be not a positive signal)?

Large gaps in results

After hole 57 there are large gaps in reported results with the latest hole for which laboratory results have been reported being hole 137. Given how much time must have elapsed between drilling hole 59 and hole 137, this is worrying.

It raises the possibility that New Found has learnt how to tell which holes carry gold (it can be easy if gold comes with gaudy sulphides and strong alteration), and they are ‘managing’ the batches of samples that are sent for assay. There is a distinct impression of mixing spectacular results for more recent holes with poor to mediocre results for older holes.

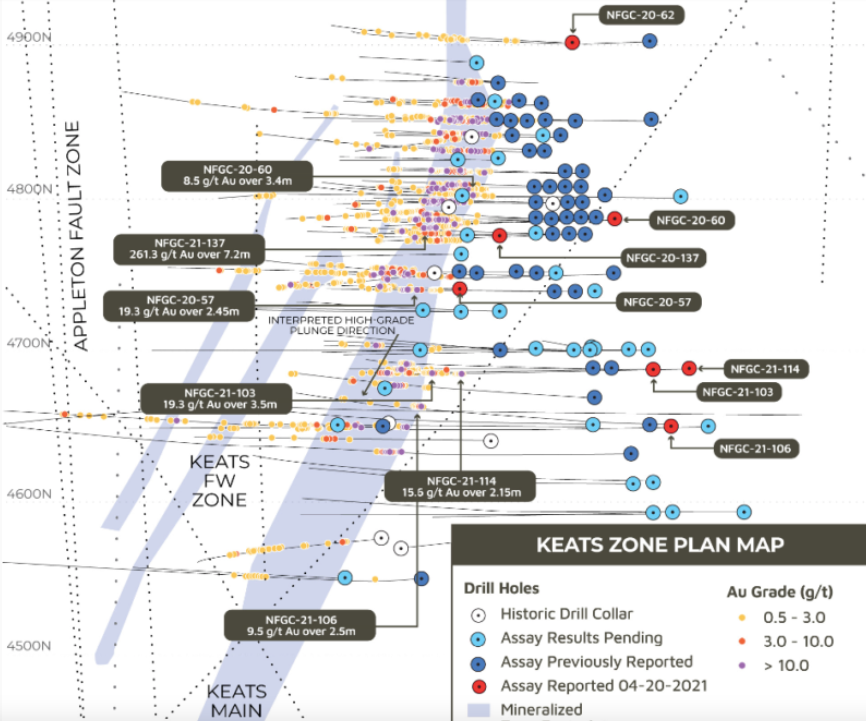

Have a look below at Figure 2 which shows results reported on 20 April.

Dense drilling

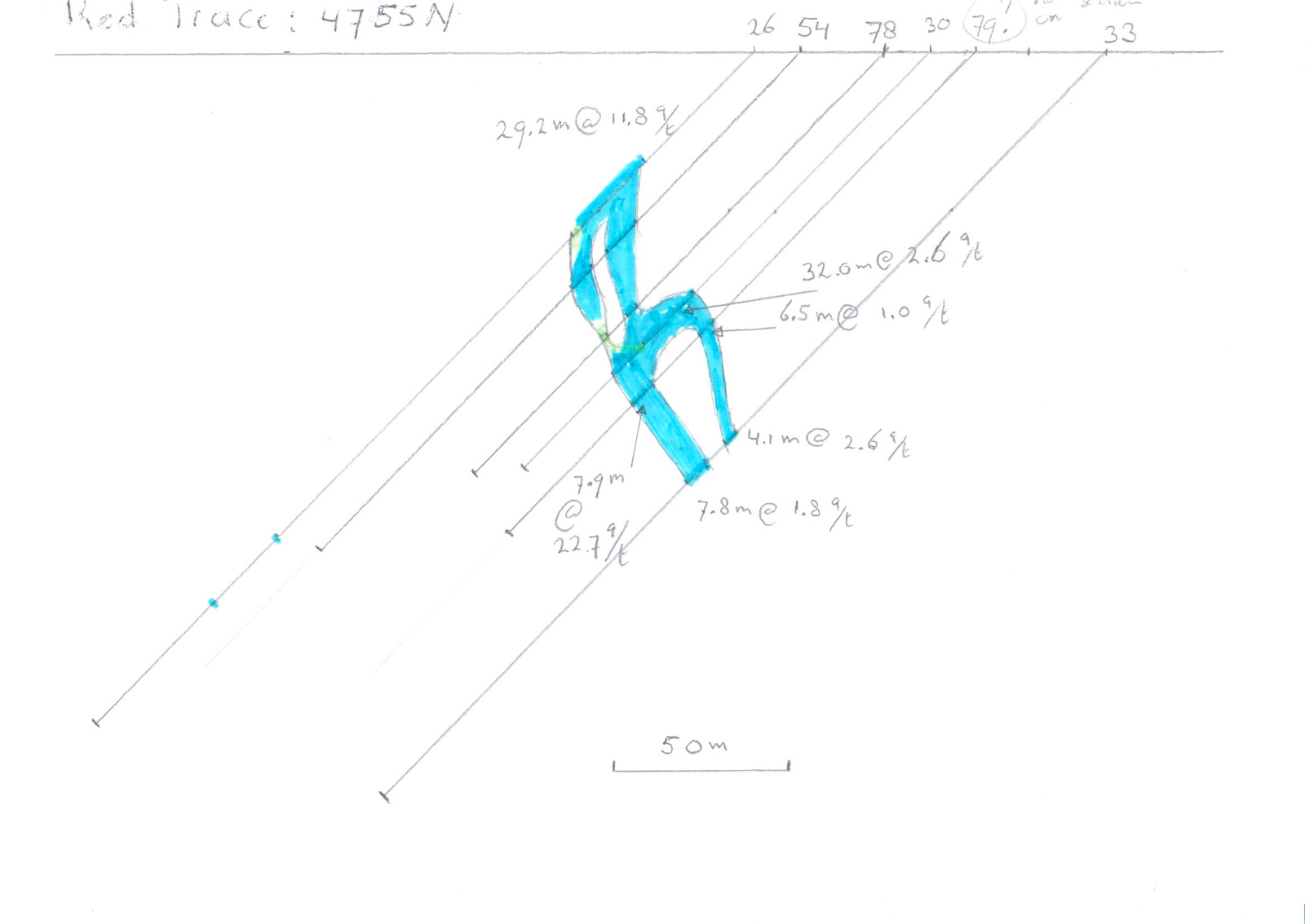

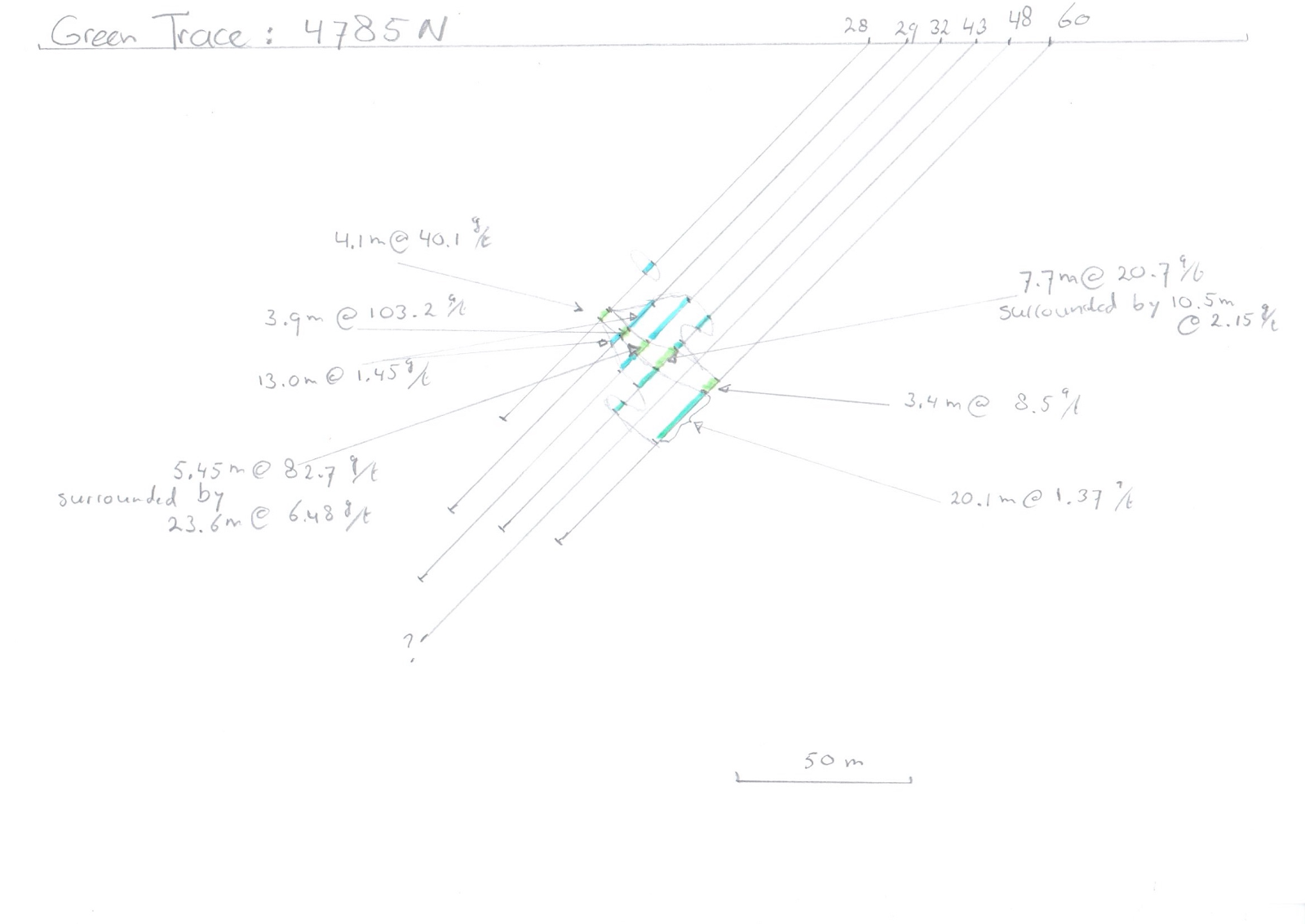

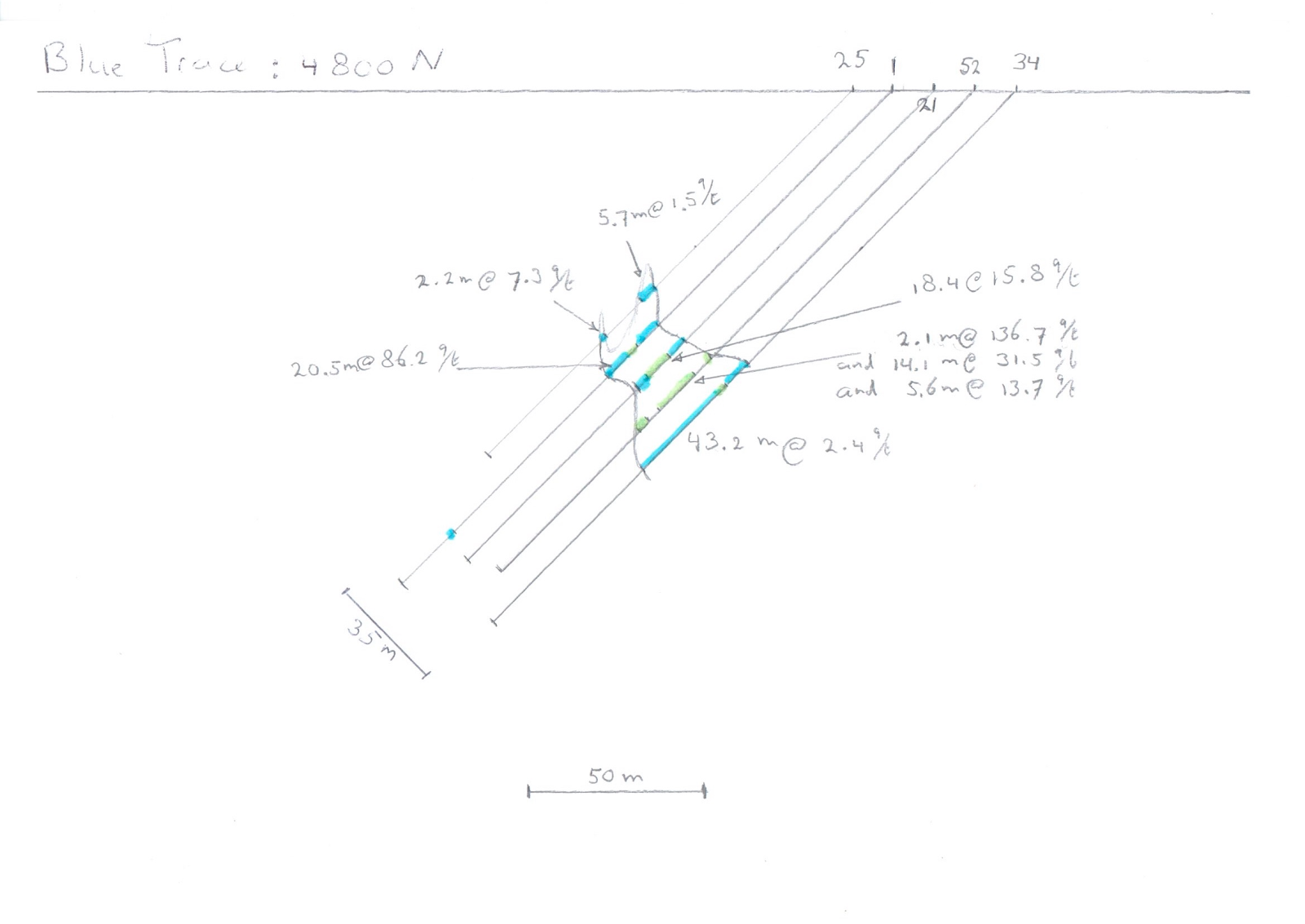

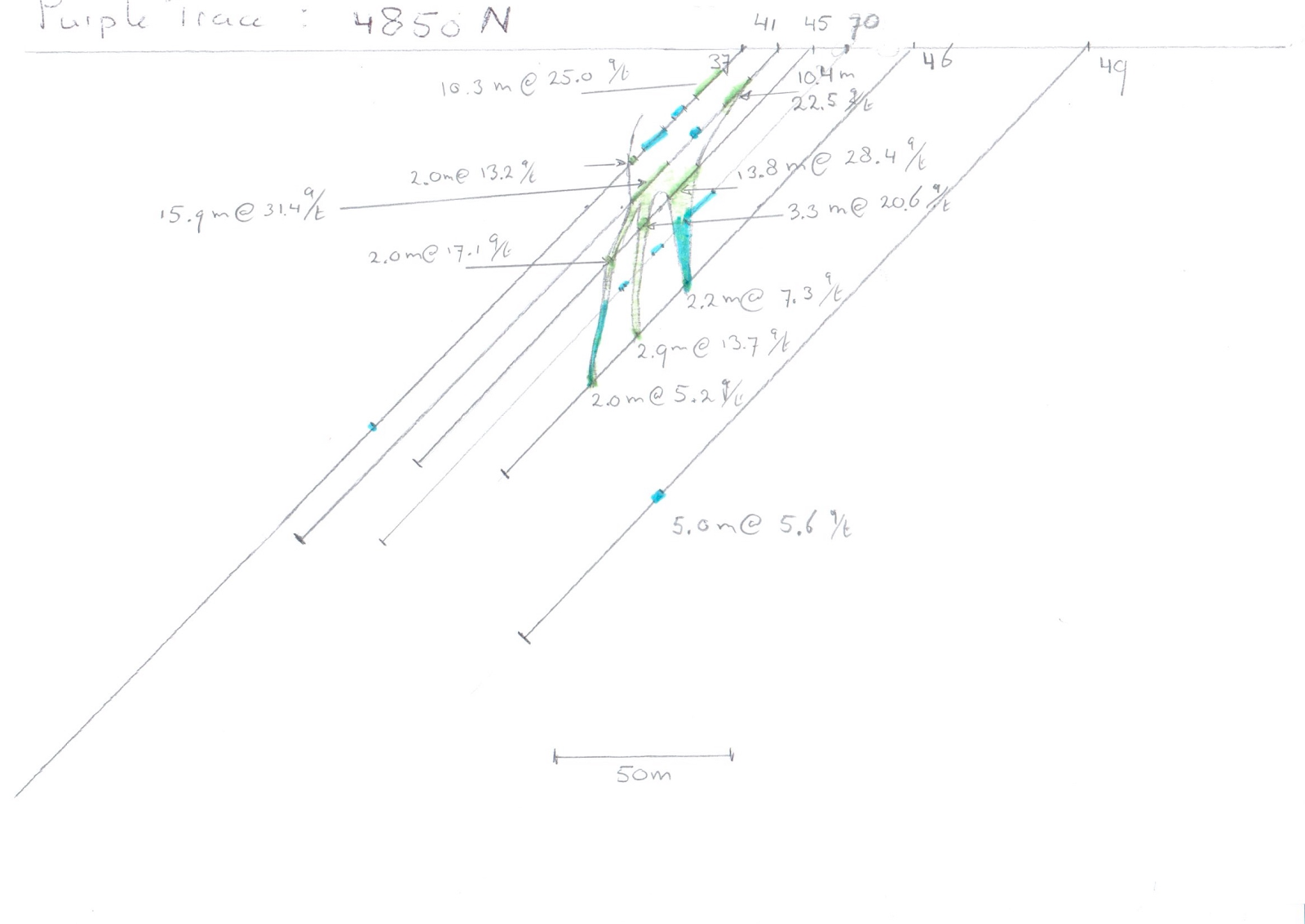

The table has identified in different colours holes that are along a fence ±10 m on either side of the fence coordinate: green-grey for 4705 N, red for 4755 N, green for 4785 N, blue for 4800 N and purple for 4850 N. The fact that sections “red”, “green” and “blue” are in total within 45 m strike shows the very dense nature of drilling, something that will be further explored below.

Smearing

Some of the intersections have the gold predominantly present in a very much narrower interval. Hole 29 has 96% of the gold in 3.90 m of the reported 25.0 m and hole 80 has 98% of the gold in 1.00 m of the reported 25.8 m. This is called smearing (where high-grades are spread over much wider width to achieve more substantial dimensions). Smearing is bad practice.

Drill Results in Context

The way New Found Gold presents data is challenging for investors. We specialise in this stuff, and even we found it really difficult to review and analyse the reported results. After the press release dated 11 January 2021, New Found Gold no longer provides a drill location plan with the numbering of all holes drilled and it does not identify along at coordinate a hole has been drilled at Keats Zone.

For drillhole collar locations after 11 January 2021, we have had to review all press releases to collate drillhole collar locations on a master plan. The pierce points of the drill holes on the longitudinal sections were also used to determine along what north-coordinate holes were drilled.

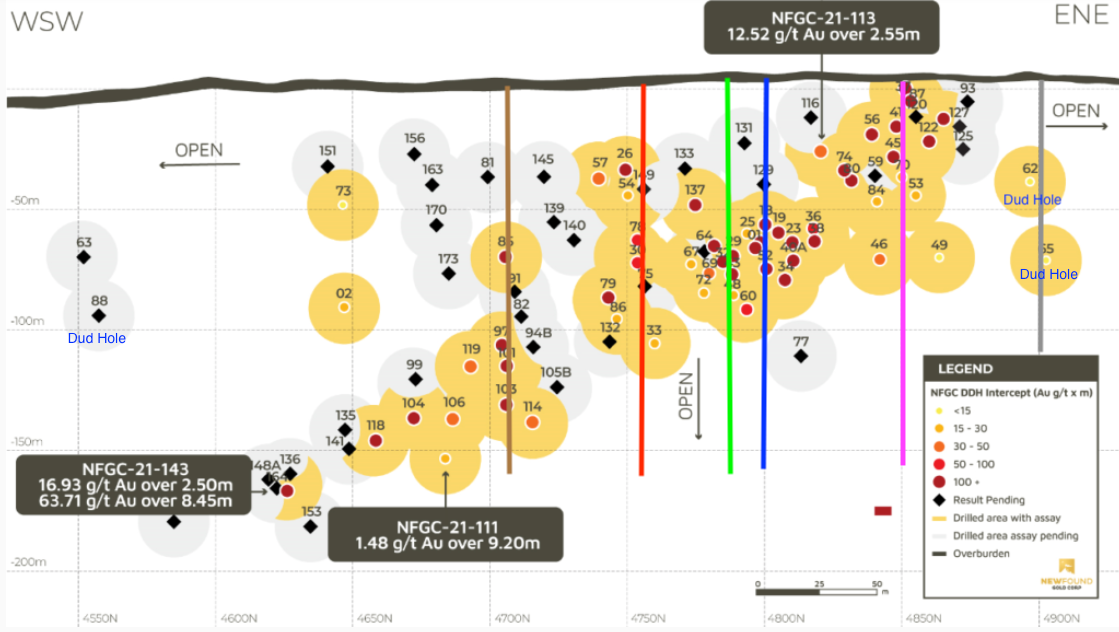

Figure 3 shows as an example the provided drill collar plan on 20 April, which shows the locations of highlighted results only.

The illustration is extra confusing as it shows for the same drillhole, the collar position and intercept location projected to surface. Note the considerable interpreted width of the blue outlines which shows the “Mineralized Zone Footprint”. Given the distance between coordinates, the width of the mineralised zone is implied to be 65 m wide in the far south on the map and to still exist in the far north.

You can see in Figure 3 that the drill density in certain places is extremely high, especially around 4800 N. In this area, holes are collared as close as 10 m apart both along the drill fence and along the strike of the target.

We previously stated (8 February 2021 Analyst Notes) that there is a logic to very intense drilling in the early phases given the probable complexity of the deposit given the history of intense deformation of the rocks. However, it is concerning the company finds it necessary to keep drilling at this density.

We also continue to worry that New Found Gold does not provide cross-sections to show the relative location of the drill intersections in news releases. Cross-sections are a vital piece of the jigsaw, and investors are entitled to be very cautious of any company that does not adequately present its information in three dimensions to the public.

Instead of cross-sections, New Found Gold has, since 10 March, included longitudinal sections with grade colours for the intersections where it pierces the deposit. Figure 4 is the latest version of the longitudinal section.

The illustration is a poor tool to educate the reader and is also inclined to overstate the size of the deposit.

For example, the colour code of hole 65 at the extreme right of the illustration is associated with 2.9 m at 1.04 g/t Au and hole 49 further to the left with 5.0 m at 5.6 g/t Au. Strangely enough New Found Gold had reported “no significant values” for this particular hole in an earlier press release.

At the other side of the illustration, hole 2 has an intersection of 12 m at 1.54 g/t Au and hole 73 associated with 2.5 m with 21.9 g/t Au all of which gold was found in 0.7 m.

Strange Gaps and Clustered Sections

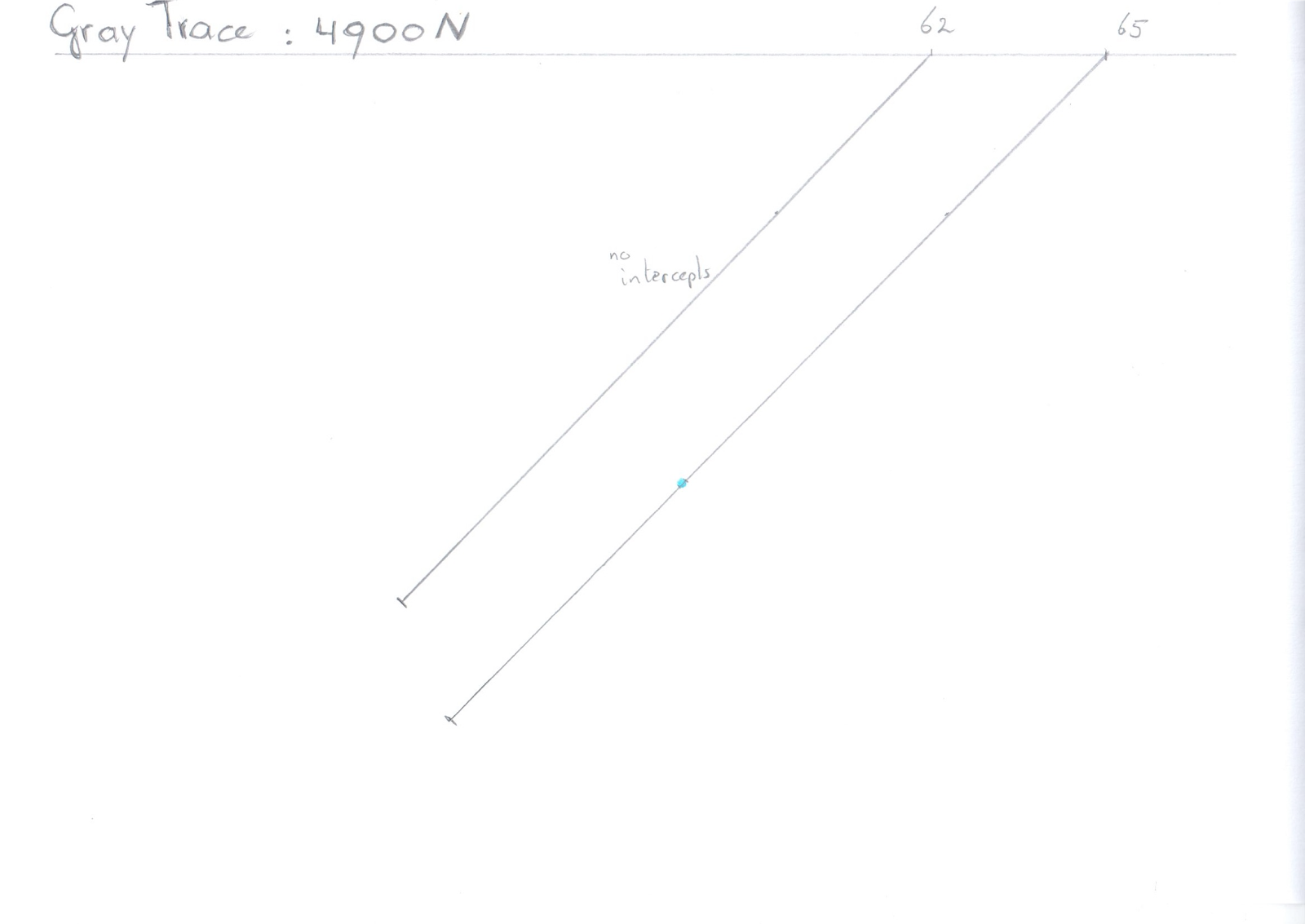

Earlier we observed that there are strange gaps in laboratory results, with early holes (low hole ID numbers) either unreleased or only released later with much later holes (high hole ID numbers). There is a cluster of unreleased early holes just south of the 4850 N line (highlighted in Table 2 in purple) trace”, another cluster just south of the 4780 N line (green highlight), and another such cluster between the 4705 N and 4750 N lines (brown and red highlights).

Until these unpublished results are made available there is still much uncertainty about the consistency of the shoot. In this respect, we refer back to Figure 1 and point to the NE-SW trending control which may well have resulted in very localised but rich mineralisation along the Appleton Fault Zone.

To get a better understanding of the significance of the results that have been published we updated our hand-drawn cross sections interpretation of the 8 February Analyst’s Notes and reproduced these on a smaller scale to accommodate future results (see Figures 5-10 below). We have added in cross sections for 4705 N and 4900 N that were not included in the earlier note.

We are the first to concede that the interpretation in the sections is highly speculative and New Found Gold geologists may well differ. The key point, however, is that the cross-sections demonstrate dramatic changes over very short distances both along strike and perpendicular to the strike. The sections also illustrate how the deposit becomes rapidly much less impressive in size away from the densely drilled strike extent between 4750 N and 4850 N.

It is concerning that New Found Gold prefers to drill going southwards with deep holes in preference to testing the down dip extent of the deposit with relatively short holes at cross-sections 4785 N and 4800 N. However, the lack of gold in hole 49 along cross-section 4850 N is somewhat ominous for the prospects of extensions down dip.

The most recent holes are focused on testing in addition to the down-plunge extension (e.g. holes 135,136, 141,143, 148A, 151) the up-dip extensions of the deposit (139,140, 145, 149, 151, 156,163,170,173).

We also record that the projection of the “Mineralized Zone” to surface in Figure 3 gives an exaggerated impression of the dimensions of the zone, especially in the north, where the holes there drilled failed to prove material mineralisation and in the south where the zone has at best a width of 10 m, but is shallowly dipping, thereby giving a flattering wide projection to surface.

In our first interpretation of the data back in February we used dimensions of 100 m along strike length with 30 m true width over a vertical distance of 120 m. The latest cross-sections interpretation shows these assumptions to have been far too optimistic. Whereas an argument can be made to use 175 m strike, as soon as one moves either north or south away from the central area of 4770 N – 4820 N the width is clearly far less than the average 30 m previously assumed. We do not, therefore, see any need to change our very optimistic ball-park estimate of 0.4 Moz upwards.

Conclusion

Victoria Gold

Gold production went down in Q1/21 as predicted by Crux Investor, but will now rapidly recover with the recommencement of crushing and stacking as already pointed out by Crux Investor in Analyst’s Notes 1. Building nicely.

Excelsior Mining

There has been no production update which again points to major problems with the process. Our conclusion stands that until the company can prove consistent production generating positive cash flow this share carries major risk.

New Found Gold

Based on the updated drillhole interpretation there is nothing for us to change our view that the market has gotten ahead of itself with respect to New Found Gold.

The drill results after Analyst’s Notes 2 are such that the company has not obviously increased the size of the deposit, yet the market value has increased considerably. It reinforces our previous conclusion that the market is getting ahead of itself and discounts very much upside which is not evident at all. At the share price of C$6.29 on 27 April 2021 the diluted Enterprise value of New Found Gold is above US$750 million, which places a value of around US$1,890/oz on the optimistically estimated gold content. As pointed out on 8 February, as such a valuation would already be exceedingly high for Measured and Indicated resource ounces, the current company valuation is excessive.

Want to hear more from the Analysts?

Are you looking for consistent returns for more confident investing? That's where we come in. Crux Investor is an investing app for busy people.

You’ll receive a single stock recommendation each month, curated by industry experts and presented in a clear and focused one-page memo. You’ll also receive access to a platform full of programmes that will allow you to grow your financial knowledge, overall, all at your own pace.

Crux Investor is for anyone interested in saving time while investing with confidence. It's an ideal resource for the novice that needs guidance and is tired of throwing money away with guesses and gambles. But it's also a perfect fit for the experienced investor that wants a faster and more efficient way to arrive at the perfect stock or significantly increase their knowledge.

Finally, you can afford the analysts the big funds use. No more gambling, no more guesswork. Instead, save time, slay stress, and start investing with confidence by joining Crux Investor today.

If you are a Family Office investor, or an Institutional investor, and you would like the full report behind this article, please contact matthew@cruxinvestor.com

Analyst's Notes

Subscribe to Our Channel

Stay Informed