Why Natural Gas is a Victim of Shale's Implosion: The Price of High Grading

Trader Ferg explains why another unpopular, unloved sector is not yet ready for investors: Natural Gas. We break down one potential rationale and approach for you.

Another wonderful session on our weekly show with Fergus Cullen – better known as Trader Ferg – where he explains why another unpopular, unloved sector is not yet ready for investors: Natural Gas. We break down one potential rationale and approach for you.

Starting With Shale

While many think the shale industry is an oil story, Cullen believes that it is integral to understand the outlook for natural gas in the US.

Currently, 75% of US natural gas comes from shale, an industry which Cullen believes to be on its last legs, with falling rig numbers and a looming wall of maturing debt.

“Natural gas is going to be one of the biggest victims of shale’s implosion”

Shale managed to plug the gap between falling oil discoveries and rising production levels, primarily facilitated by huge Federal investments. However, the replacement rate (the ratio of barrels consumed to new sources) of the conventional oil industry has continued to fall with only 1 in 6 barrels being replaced, placing additional strain on shale.

Despite the US now producing roughly 17% of the world’s oil on the back of shale, Fergus predicts that it won’t be able to plug the production gap for much longer.

While the production decline rate of a typical oil well stands at around 10% per year, for shale many sites see a decline rate of 70% in their first year, and 85% within their first 3 years. Shale is “a temporary solution”.

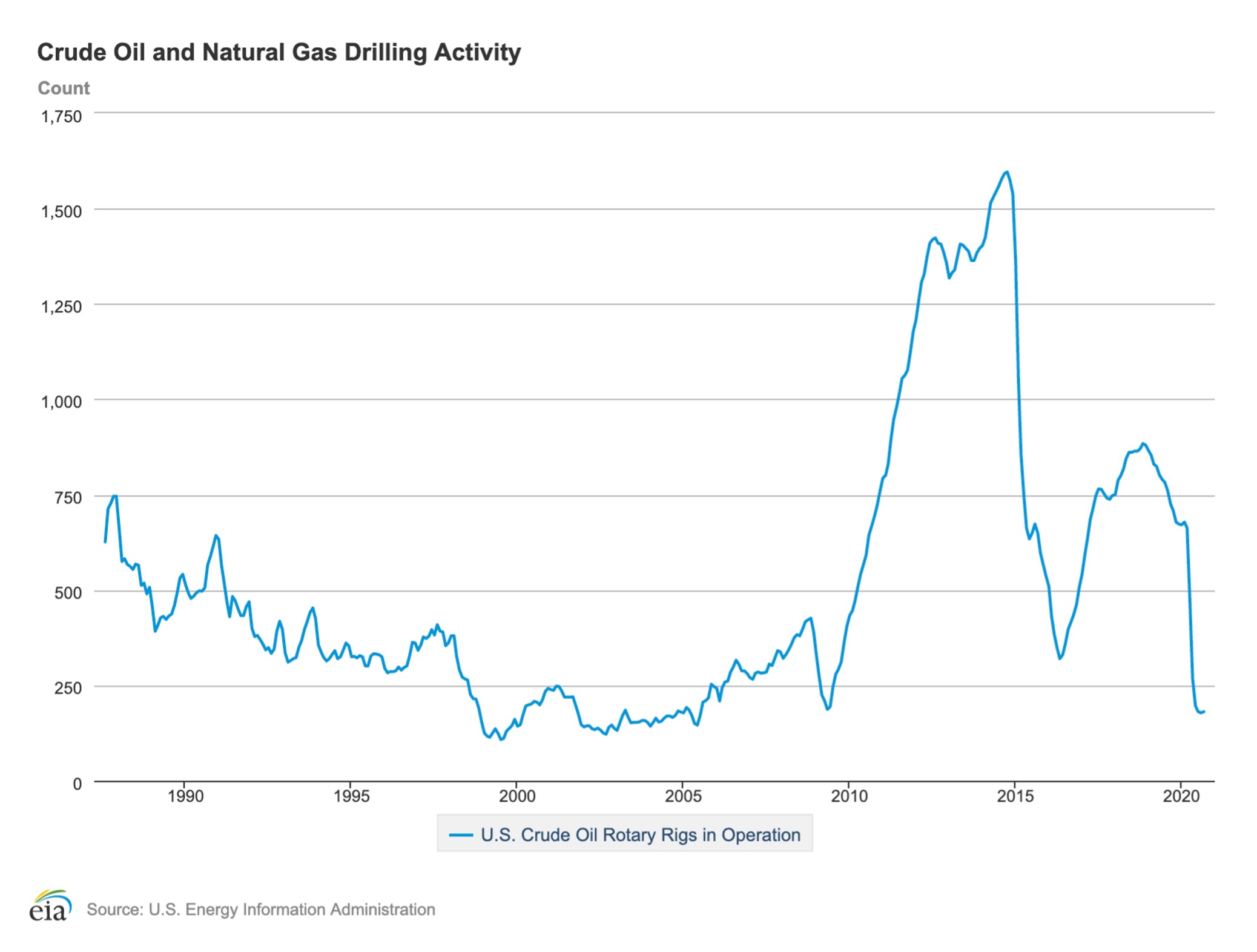

The Rise and Fall of Shale Rigs

The astronomic rise of shale can be seen from the rig numbers, in 2010 there were just 200 shale rigs in the US, just 4 years later that figure had increased 8x to 1,600 rigs.

While the number of rigs fell dramatically between 2014-2016, down to 300, Cullen makes it clear that this didn’t spell the end for the industry due to increasing levels of productivity and, most importantly, high-grading.

High-grading is essentially when a producer extracts the highest quality resource from a site, before moving onto another, leaving the lower grade resources for potential extraction at a later date.

At the start of the shale boom in 2014, just 50% of the wells were considered first-tier, in terms of quality, with 400 barrels being produced daily, by 2018 the percentage of first-tier wells was up to 70% and produced 625 barrels per day. Current estimates place this level in the region of 80%.

“Absolutely gutting all the good stuff”

One of the key reasons why this is so damaging to the economics of shale is that these sites still need to be maintained even once a company moves on, particularly due to the high levels of pressure within each well. “Gas was almost like an unwanted by-product”, with many producers selling it at a loss or even flaring off the gas.

High grading points to the fact that the industry was obsessed with increasing production regardless of the long-term economics, causing an enormous surplus of gas supplies.

Cullen believes that the price of gas will rise dramatically once the consequences are realised.

Structural Deficit

To complicate the matter further, Cullen believes that we are fast approaching a major structural deficit in terms of oil.

At its peak the US was producing 13 million barrels of oil per day, however, production dropped off significantly in March 2020, down to 10.5 million per day, primarily due to the COVID pandemic.

While a lot of analysts are expecting production to rise by 500,000 barrels this year, Cullen wholly disagrees.

Citing figures from Goehring & Rozencwajg Cullen expects to see production drop by another 1.5 million barrels in 2021, resulting in a structural deficit of 2 million barrels per day. All as a result of shale high grading and a business model which hasn’t prioritised economics.

Fergus also sees the potential for oil consumption to grow across the globe once the COVID pandemic has subsided as millions seek to travel. With China's oil consumption growing by 10% in 2020 despite the pandemic, the evidence suggests that higher global consumption is a distinct possibility for 2021.

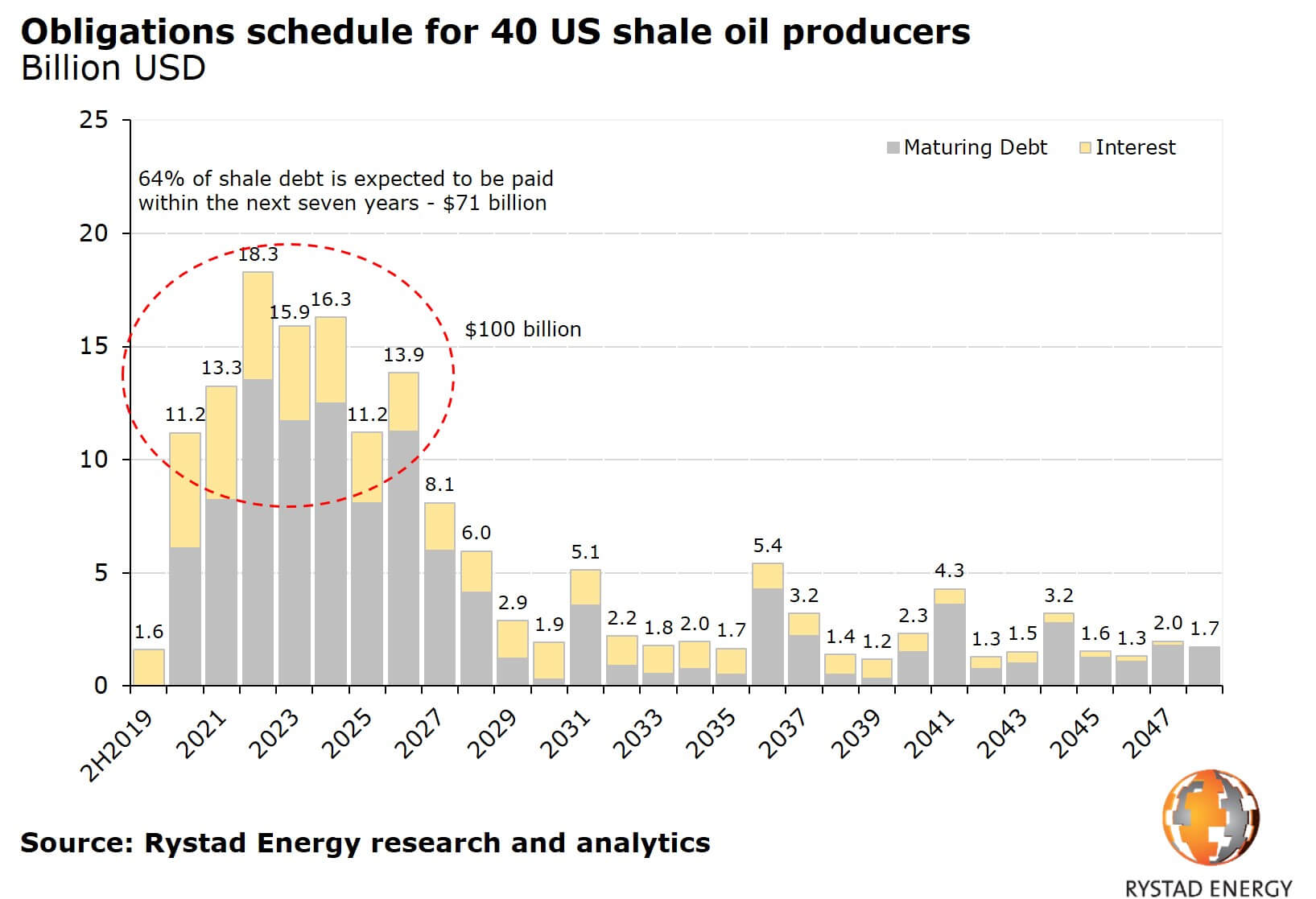

The Wall of Debt

Even with looming production issues due to high grading, and a widening structural deficit, shale’s woes are not over. Debt maturity is going to hit the industry hard over the next 6 years.

In 2022 over $18 billion worth of debt expected to mature, with a further $16 billion per year for the next 2 years, before it begins to drop off.

Combined with the impact of COVID and the high grading which will make it impossible to increase productivity, the shale oil industry is in a dire position.

ESG directives will also make it much harder for these companies to access capital, alongside a Biden administration ban on shale permits on federal land.

“As oxygen is to life, capital is to the oil and gas market, and these guys are in the midst of having their knees chopped off when they’ve got the biggest wall of debt coming”.

In an industry that has never generated free cash flow which has $71 billion of debt expected to be paid over the next 7 years the outlook is bleak.

Cullen firmly believes that shale will not bounce back from this.

How Did Fergus Play This?

With a looming disaster in the shale space, how did Fergus Cullen navigate the US natural gas sector?

He took a basket approach, investing in Antero Resources (NYSE:AR), CNX Resources (NYSE:CNX), and EQT Corporation (NYSE:EQT), all of which operate in the Appalachian Basin.

Antero which operates from Denver, Colorado, has reserves of 535 billion cubic metres, 61% of which are natural gas. They reported a 2019 revenue of $4.4 billion. However, the company reported a net loss of $536 million in the third quarter of 2020.

CNX, a Pennsylvania based natural gas company with over 270 billion cubic metres of proven gas reserves, with a revenue of $1.28bn in 2019. The company is currently operating both shale and coal-bed methane wells and are steadily trading at between $12-13. The company was also ranked in the top 250 of Newsweek's most responsible companies in 2021.

EQT is currently the largest natural gas producer in the US, with just below 495 billion cubic metres in reserves, and it is currently ranked in the top 1500 of largest public companies by Forbes in 2018. The company claims a 130 year history, however, reported a net loss of $601 in the third quarter of 2020.

However, for Cullen Denver based Antero was the clear favourite, despite predictions that they were heading for bankruptcy due to the wall of debt in 2021/22.

The simple reason for this is that Antero has access to enough capital to shield itself from maturing debts. The company holds a large stake in Antero Midstream Corp. (NYSE:AM) and also reported $1.1 billion in hedge gains, both of which could be liquidated to bail them out.

Antero had also massively reduced overhead costs throughout 2020, reducing spending by $520 million.

At the same time that rumours were circulating that they were headed for a Chapter 11 bankruptcy, Antero’s management was busy buying stock. Over the last 2 years, they bought back 10% of issued shares, and in the last months of 2020, they bought a further 6%, indicating Antero’s confidence.

Trading at just $2 in April last year, Antero is now up to $8.

A prime example of objective research outwitting media chatter.

However, Cullen emphasises that it is important to be aware of the potential risks of investing in a company in Antero’s position, as there is always a chance that the company will end up filing for bankruptcy. But, in the case of Antero, it paid off.

Fergus is no longer investing in the natural gas space, and is holding his position, and advises against anyone seeking to chase these stocks. However, for those interested in profiting from the imminent structural deficit of oil, Fergus recommends offshore oil drillers.

A few weeks ago we covered Fergus's views on the offshore drilling space and its outlook for 2021 and beyond.

Analyst's Notes

Subscribe to Our Channel

Stay Informed