Oil & Gas Deliver Strong Cash Flow in Evolving Energy Landscape

Oil sector navigates $60-67 pricing amid policy shifts and OPEC+ tensions while companies focus on disciplined growth, dividends and strategic asset development.

The oil and gas sector in 2025 finds itself at a critical juncture, characterized by price volatility, geopolitical tensions, and shifting regulatory landscapes. With WTI crude hovering around $62.86 per barrel and Brent at approximately $67.44, investors are witnessing a market shaped by complex and often contradictory forces including a recent brutal $10-per-barrel drop this month.

The contradiction is emblematic of where U.S. shale finds itself in 2025: stuck between political slogans and fiscal reality. On one hand, the Trump administration pursues a "drill, baby, drill" agenda while simultaneously wanting lower prices at the pump for consumers. Meanwhile, Wall Street demands dividends rather than aggressive drilling programs. This tension creates both challenges and opportunities for strategic investors.

OPEC+ Dynamics and Global Supply Considerations

The U.S. Bureau of Ocean Energy Management recently increased the Gulf of America's untapped reserves estimate to 5.77 billion barrels, and the Trump administration has launched a new 5-year offshore oil and gas leasing plan, which might include blocks in the Arctic. This represents a significant policy shift favoring expanded production opportunities for U.S. energy companies. However, regulatory clarity remains elusive. U.S. Energy Secretary Chris Wright has sent mixed signals to the market. Wright has gone from praising shale's ability to boost production even at $50 oil to declaring that "$50 oil is not sustainable for producers.", as taken from Bloomberg’s Stephen Stapczynski. This contradiction highlights the challenges in formulating investment strategies around potentially inconsistent policy positions.

OPEC+ continues to exert significant influence over global oil markets, though internal disputes have intensified. Several OPEC+ members will suggest the group accelerates oil output hikes in June for a second consecutive month. This follows a surprising decision to increase output by 411,000 barrels per day in May, which was three times more than originally planned.

The compliance issues within OPEC+ are particularly notable. Kazakhstan and Iraq have angered Saudi Arabia by producing well above their allocated quotas, with Kazakhstan explicitly stating it would prioritize national interests over OPEC+ when deciding on output levels.

"Kazakhstan's statement cements our view that OPEC+ may implement another accelerated three-month unwind again in the May meeting and it may continue again in July and through the summer," - Amrita Sen, co-founder of Energy Aspects

Geopolitical Factors Influencing Markets

Geopolitical tensions continue to create both risks and opportunities for oil investors. Oil markets are bracing for the next big external shock as Trump's trade war with China continues to escalate and talks of a potential nuclear deal with Iran threaten to bring fresh supply to markets.

U.S. relations with Iran represent a particularly volatile factor. The U.S. issued fresh sanctions targeting an Iranian liquefied petroleum gas and crude oil shipping magnate and his corporate network. This occurred despite both sides reporting progress in nuclear talks, complicating the outlook for Iranian oil exports. New York-based Again Capital partner John Kilduff observed, "Either some nuclear deal is agreed or the U.S. tries to drive Iran's oil flows to zero, and it's increasingly looking like a zero-flow scenario."

The U.S.-China trade relationship also significantly impacts energy markets. Equity markets rebounded on April 22 on signs of a potential de-escalation in U.S.-China trade tensions. However, Washington's standoff with Beijing, and tariffs on virtually all U.S. trading partners, have weighed heavily on oil prices in recent weeks as investors expressed concerns of a potential global economic slowdown that would severely erode oil demand.

LNG Market Shifts and Regional Dynamics

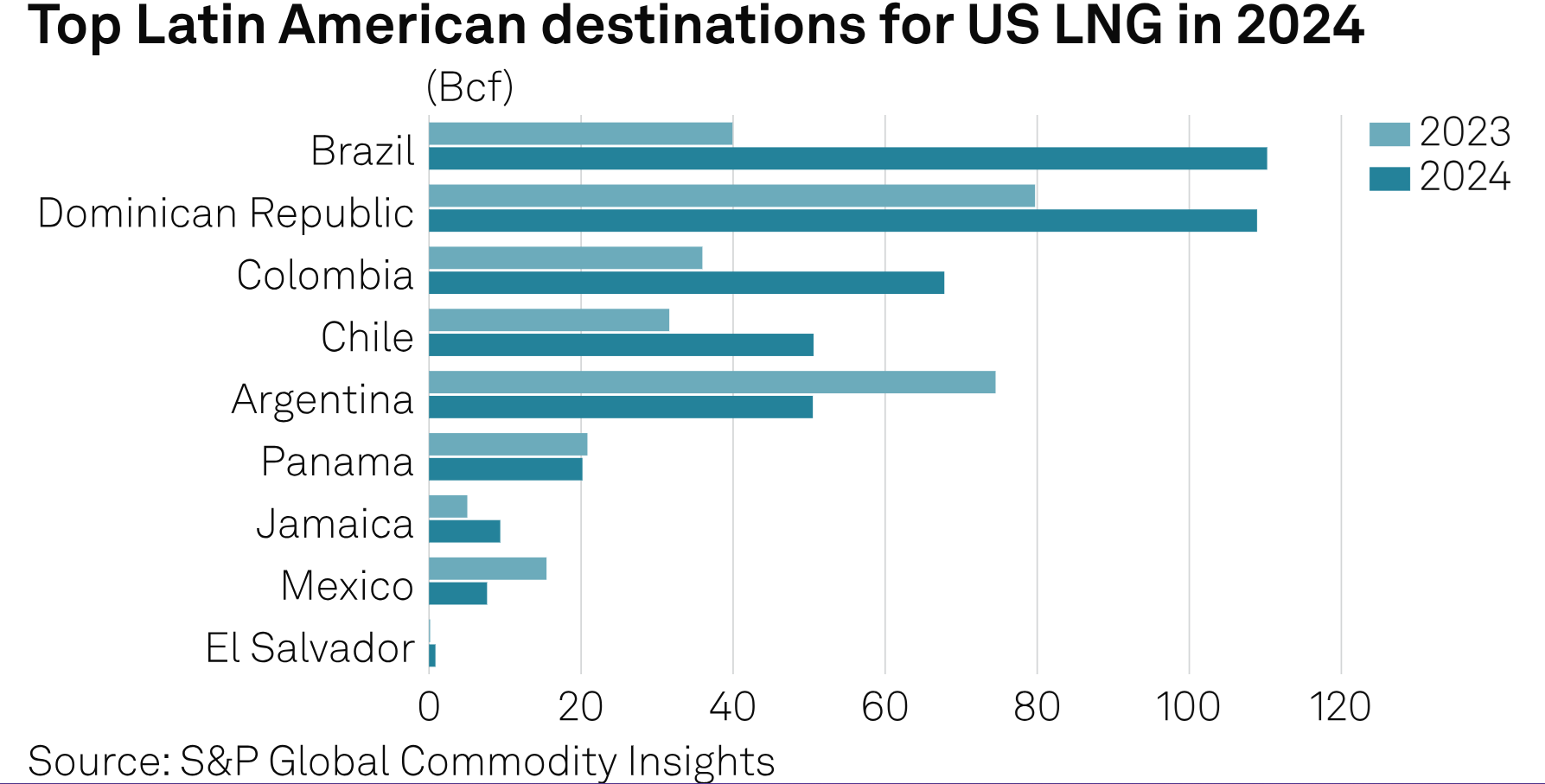

The liquefied natural gas (LNG) market is experiencing significant realignment along geopolitical lines. Taiwan's President Lai Ching-te announced that Taipei would seek to increase the share of US LNG imports from the current 10% to 33%, potentially discontinuing some term supplies from Australia and Qatar. Similarly, South Korea is considering a 20-25% increase in US LNG imports, currently accounting for 12% of its liquefied gas needs.

In contrast, China is moving in the opposite direction, completely halting its imports of US LNG in March and signing three long-term deals with the UAE for the supply of liquefied gas over the next 10 years. This divergence in Asian market approaches creates selective opportunities for LNG-focused energy companies depending on their geographic exposure.

Infrastructure and Corporate Developments

Infrastructure developments continue to shape investment opportunities in the sector. Easter precipitation has finally allowed German shippers to transport full cargoes along the River Rhine, the country's main energy transportation artery, with water levels in Kaub rising by 40% to 125cm. This alleviation of a key transportation bottleneck could benefit European energy operators.

In North Africa, Morocco is preparing to begin tendering procedures for its first-ever liquefaction terminal, to be located in the port of Nador, as its gas requirements are expected to soar from 1 Bcm currently to 8 Bcm by 2027. This represents a significant growth opportunity for companies involved in LNG infrastructure and supply.

The oil and gas sector continues to see significant merger and acquisition activity as companies reposition themselves in response to market conditions. Argentina's second-largest oil company, Vista Energy, bought Petronas' 50% stake in the La Amarga Chica shale play in the country's Vaca Muerta basin for a total of $1.5 billion.

Major international oil companies are also recalibrating their portfolios. U.S. oil major Chevron is reportedly looking to divest some of its upstream interests in Angola, potentially exiting Block 14K that currently produces some 42,000 b/day across Angola and Congo. This ongoing portfolio optimization by majors can create acquisition opportunities for growth-oriented independent producers.

Empire Energy (ASX:EEG) is making significant progress in developing its Beetaloo Basin assets in the Northern Territory. Flagship Carpentaria Pilot Project shows promising advancement with the recent drilling of Carpentaria-5H, which features the longest horizontal section in the Beetaloo Basin at 3,310 meters. The company is preparing for hydraulic stimulation of C-5H in June 2025, with plans to commence gas sales from EP187 in late 2025 or early 2026.

The company has secured key financing through a Macquarie Midstream Infrastructure Facility and maintains a healthy liquidity position of $32.2 million. Notably, the political environment in the Northern Territory has become more favorable with the Finocchiaro CLP Government scrapping the previous 50% renewables target and removing third-party merits review processes.

Elixir Energy (ASX:EXR) has successfully executed a strategic farmout agreement for their ATP 2077 Diona Sub-block in Queensland. The deal with Xstate Resources includes a 51% interest transfer to XST, who will fully fund and operate the exploration of the Diona-1 well, scheduled for Q3 2025. Elixir retains 49% interest in this sub-block and 100% of the Taroom Trough blocks. The company location is ideal with proximity to existing gas infrastructure and production facilities. The Diona Prospect represents a low-risk opportunity with structural and stratigraphic components targeting Showgrounds, Tinowon, and Wallabella Sandstone levels.

Strike Energy (ASX:STX) continues to build momentum in Western Australia, completing key milestones in their South Erregulla development while maintaining steady production from Walyering. The company has executed financing documentation with Macquarie for $217 million and commenced earthworks at South Erregulla for the construction of an 85 MW Peaking Gas Power Station.

Executive Director and Acting CEO Jill Hoffmann emphasizes in the company's quarter report,

"Energy market conditions continue to underline the value of developing gas in the Perth Basin through integrated gas-to-power as Western Australia grapples with its energy transition."

Athabasca Oil Corporation (TSX:ATH) delivered record results in 2024 with significant growth across key metrics. Annual production reached 36,815 boe/d (98% Liquids), representing 7% growth year-over-year, while Adjusted Funds Flow hit $561 million ($1.02 per share), representing 102% per share growth over 2023.

The company's balance sheet strength is evident with a Net Cash position of $123 million and Liquidity of $481 million. Their capital program focused on expanding Leismer production capacity toward 40,000 bbl/d by the end of2027. Athabasca's shareholder returns have been robust, completing $317 million in share repurchases in 2024 and committing to direct 100% of Free Cash Flow to share buybacks in 2025.

Arrow Exploration (LSE:AXL) demonstrated exceptional growth in 2024, with oil and gas revenue increasing 65% to $73.7 million and production up 63% to 3,542 boe/d. The company reported net income of $13.2 million and Adjusted EBITDA of $48 million (78% higher than 2023), while maintaining a strong cash position of $18 million at year-end. The growth was driven primarily by successful drilling at the Carrizales Norte field in Colombia, where the company completed seven horizontal wells and five vertical wells. Arrow has an aggressive 2025 work program totaling $51 million and targeting up to 23 wells, mainly in the Tapir block.

The Investment Thesis for Oil and Gas

The near-term outlook for oil prices remains uncertain as multiple factors pull the market in different directions. Add to that a shaky macro backdrop, potential U.S.-China tariff détente, and OPEC+ infighting, the oil and gas market is trying to price in about nine different realities at once.

Current market positioning suggests a temporary consolidation phase before the next catalytic event. Oil producers are preparing for another external shock to oil markets as Brent futures took some collateral damage from Monday's equity sell-off and remain pressured by the prospect of a potential US-Iran nuclear deal. For the time being, the $66-67 per barrel price for ICE Brent seems to be a temporary resting place for crude before the next big thing happens.

- Energy Transition Positioning: Despite renewable energy growth, oil and gas remain essential to global energy security through 2025 and beyond. Companies with clear transition strategies that balance traditional production with investments in lower-carbon technologies offer compelling value.

- Policy Tailwinds: The current administration's support for domestic production through expanded leasing opportunities, particularly in the Gulf of Mexico and potentially the Arctic, creates growth runways for companies with expertise in these regions.

- Dividend Yield Advantage: With Wall Street demanding shareholder returns over aggressive growth, many oil and gas companies offer dividend yields significantly above market averages, providing income in an uncertain economic environment.

- Consolidation Opportunities: The wave of M&A activity is creating larger, more efficient operators. Consider companies with strong acquisition track records and balance sheets capable of further accretive transactions.

- Geographic Diversification: Companies with exposure to multiple global basins can better manage geopolitical risks and capitalize on regional pricing advantages. Look for operators with strategic positions in both U.S. shale and select international markets.

- Natural Gas and LNG Exposure: Growing global LNG demand, particularly from strategic U.S. allies in Asia seeking to reduce dependence on other suppliers, creates long-term value for companies with gas-weighted production portfolios and LNG infrastructure.

- Free Cash Flow Generation: At current price levels ($60+ WTI), well-managed oil and gas companies can generate substantial free cash flow. Prioritize companies with low breakeven costs and demonstrated capital discipline.

- Inflation Protection: Energy commodities historically perform well during inflationary periods, providing a natural hedge against currency devaluation in investment portfolios.

The oil and gas sector in 2025 presents a complex but potentially rewarding investment landscape. While price volatility and geopolitical uncertainties create challenges, they also generate opportunities for well-positioned companies. The industry's shift toward capital discipline, shareholder returns, and portfolio optimization has created more resilient business models than in previous cycles. Current pricing around $60-67 per barrel supports healthy margins for efficient operators while incentivizing continued production growth in premium basins. Investors should focus on companies with strong balance sheets, operational flexibility, and clear strategies for navigating both short-term market disruptions and longer-term energy transition considerations. As global energy demand continues to grow, particularly in emerging markets, selective investments in quality oil and gas companies can provide both income and growth potential within a diversified portfolio.

References:

- OilPrice.com (April 2025) Kern, M. Oil Markets Are Bracing for Another External Shock; Geiger, J. Thrive or Survive? U.S. Energy Secretary Makes U-Turn on Oil Prices

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed