The Middle East Has Oil, China Has Rare Earths

Trader Fergus Cullen shares his outlook on the global Rare Earth Elements market and names the companies poised to compete with China's REE dominance.

Fergus Cullen immediately gets straight to the heart of the Rare Earth Elements (REE) industry: it’s dominated by China and there are no two ways about it. China currently mines 70% of the global supply of REEs, separates 90% of the mixed oxides which contain REEs, and controls or produces 100% of the new REE based metals.

The implication of a Chinese monopoly is the complete control they will possess over the supply of REEs for military applications, renewable energy programs, and consumer technologies, like smartphones.

Three key reasons for China’s REE dominance

Firstly, China mines REEs as a by-product of other mining products. China sources 50% of its 132,000 ton REE output from a single mine, Bayan Obo in Inner Mongolia. Bayan Obo is an iron mine, not an REE mine. By mining REEs as a by-product they have successfully kept the prices for the mixed oxides incredibly low.

Secondly, China has the edge when it comes to expertise and research, far eclipsing any other country in terms of REE exports. In a previous interview with Rare Earths expert Jack Lifton, he suggested that China has roughly 100-200 exports for every one expert in the West. The Chinese industry has perfected the process of separation and the production of base metal.

Finally, the Chinese state has subsidised the production of REEs to an astounding level. Taking the production of steel as an example, Fergus emphasises that there is a 400% value add from turning iron ore into steel, making it highly profitable. With REEs, China operates on a 10% value add. The minute margins employed by the Chinese have crippled the economics of any independent endeavour.

“There’s no margin and it’s a difficult, tough business to get into, lots of expertise and like 10%, no-one’s even going to look at that,” said Cullen.

For more on REE: The Truth About Investing in Rare Earths (China vs USA)

Demand: Where are REEs going?

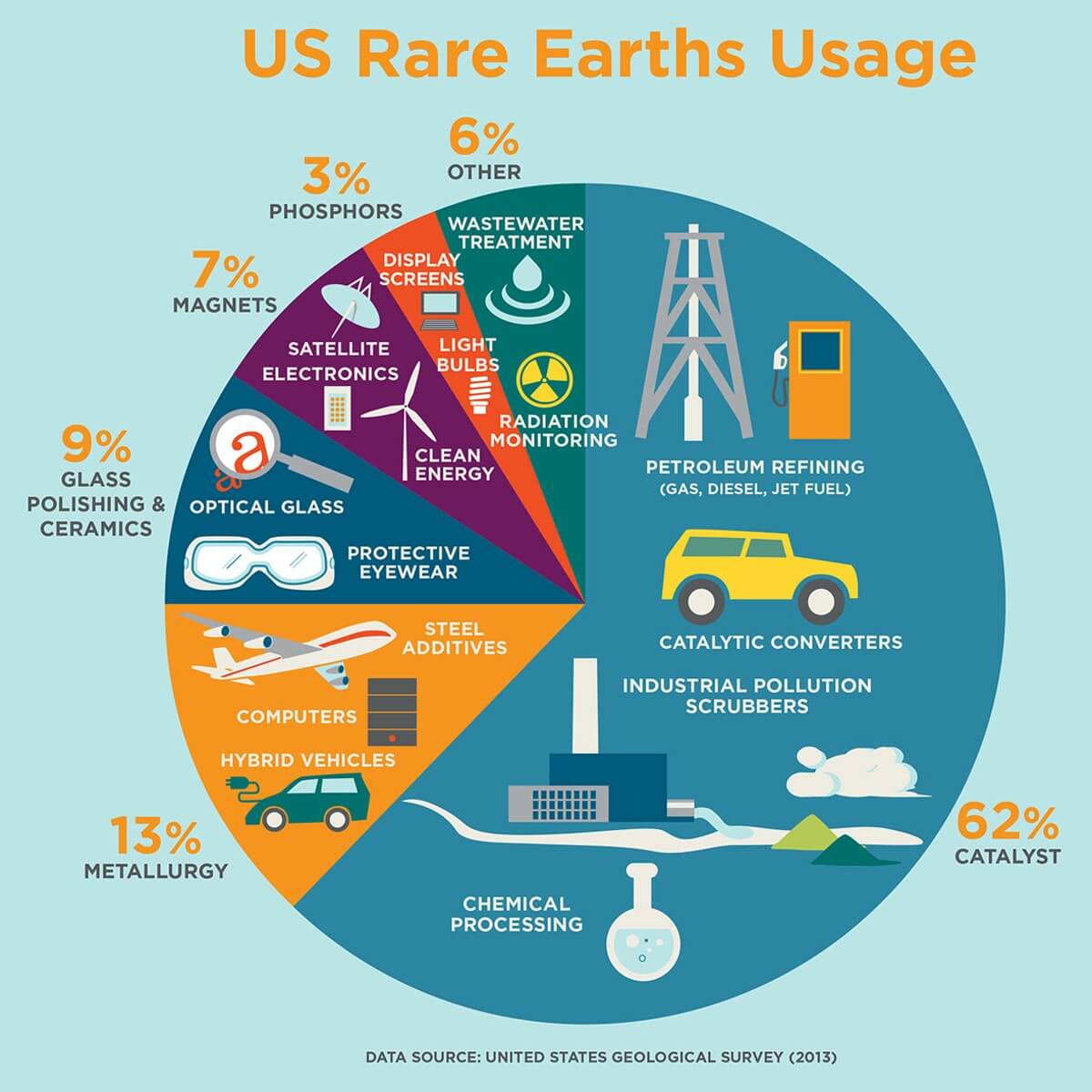

Batteries, oil cracking catalysts, magnets, lasers, fibre optics, nuclear control rods – there are a lot of uses for REEs. As an investor, where does Fergus Cullen believe REEs will count the most in the next few decades?

First of all, it is important to understand the widespread use of REEs in everyday technologies. A single smartphone requires 11 different Rare Earths to function. The applications for these metals are enormous in today’s economy, but they will only become more essential in the future.

For Cullen, the electric vehicle market will be one of the most important factors for determining the growth of the REE industry. With each new electric vehicle requiring roughly a kilo of REEs, the demand is going to soar. At present, 22 countries are planning on banning new petrol and diesel cars by 2050, with many aiming to implement these bans before 2035.

The UK aims to ban the sale of all diesel and petrol-powered cars by 2030, shifting the entire market to electric and hybrid vehicles, before a ban on new hybrids in 2035. Cullen emphasises that the world’s current supply of Neodymium, an essential for electric vehicle chain drives, will not even be enough to sustain the UK’s electric vehicle demand by 2030.

Cullen also highlights demand from the renewable energies sector, due to the increasing popularity of the direct-drive over the gearbox system for wind turbines. Direct drives are typically more reliable and require far less maintenance than gearboxes, which are at risk of damage from turbulence. These new direct-drive turbines will require roughly 200kg of REEs to manufacture.

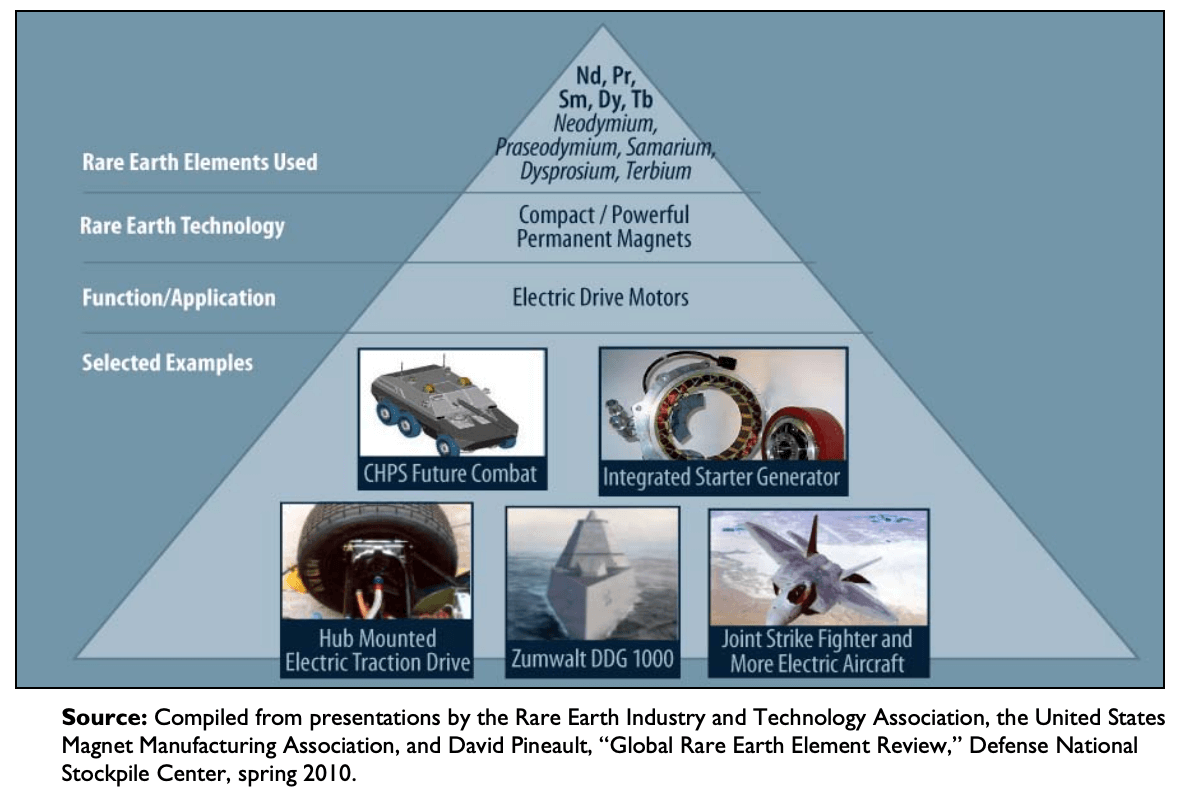

Considering China’s dominance in the REE market, perhaps the most pressing demand for these materials will come from Western militaries. New military technologies like missile guidance systems, military-grade lasers and advanced radar systems all rely on REEs. According to Cullen, a single Lockheed Martin F-35 aircraft requires roughly half a ton of REEs.

To reach demand from the electric vehicle, renewable energy and military sectors, REE mining and production must increase at a colossal scale. Unfortunately, due to the dominance of China, the West is at a significant disadvantage when it comes to accessing these materials.

Cullen predicts that unless supply chains can be constructed economically and outside of the influence of China, this demand will lead to a feedback loop of reliance on China.

There are a few companies in the West producing REEs, namely MP Materials in the US and Lynas Corporation in Australia. However, Cullen says these companies should not be relied upon and attention needs to shift to newer players in the REE space.

Below, Cullen explains why MP Materials and Lynas aren’t as good as they seem, and lists some promising REE companies.

MP Materials (NYSE:MP) and Lynas Corporation (ASX:LYC): Where they went wrong

Straight away it’s important to understand that only 7 of the 17 Rare Earth Elements are truly profitable, fetching over $1,000 per kg. When it comes to REEs, geochemistry is everything. Finding a balance of profitable elements to those that will pile up in storage is crucial to a company’s success.

To Cullen, both Molycorp (the predecessor to MP Materials) and Lynas “went after a substandard sort of geochemistry” – the mineral Bastanite. The main reason for this was the low abundance of radioactive elements, which have proven to be very difficult to get rid of in the U.S. Unfortunately, while Bastanite has little by the way of radioactive materials, it also has little in the way of the profitable REEs.

Bastanite contains high levels of Cerium and Lanthanum, both of which are priced at below $5 per kg, rendering them almost worthless in a market saturated with these elements. To make matters worse, roughly 79.8% and 83.4% of the outputs of Lynas and MP, respectively, are ‘non-economic’ elements.

Accounting for the relative value of REEs, roughly 50% of MP’s Mountain Pass deposit has a negative value and Lynas isn’t faring much better.

It is important to note that China’s non-economic output stands at 70.2%. However, this still means that the remaining 30% is selling at thousands of USD per kg, with Neodymium selling at well over $50,000 per kg at present.

MP’s Mountain Pass mine doesn’t produce any of the most important REEs for military applications, namely Terbium and Dysprosium. Any dream of MP Materials being able to cover the U.S. military’s REE demand is simply that: a dream.

“They can’t even produce the minerals that the military requires for the likes of smart bombs,” said Cullen.

Cullen compares this situation to a gold mine that only produces 2% gold and 98% coal in a market swamped with coal. While they may claim to be a gold mine, they’re actually a coal mine in a very unprofitable market.

Lynas has also been struggling with its REE processing plant in Malaysia. The plant has faced repeated difficulties in securing and renewing its permits, as the process produces radioactive materials and requires what Cullen describes as “nasty solvents.” While they may be able to secure permits in the short term, these challenges will remain long term and ultimately “no-one really wants it in their backyard”.

“The comparative economic value for Mountain Pass is only 10% of China and Lynas is 30%, which means that China’s essentially 30% cheaper and it’s got scale,” said Cullen.

Where is Ferg investing?

Energy Fuels (NYSE: UUUU)

Fergus Cullen believes that Energy Fuels has the best chance of creating an REE supply chain independent of China. Nominally a Uranium and Vanadium producer, Energy Fuels could have a strong future as the U.S.’s single truly viable REE producer.

The key factor behind this potential is the mineral Monazite, which Energy Fuels will be processing at its White Mesa Mill in Utah. Monazite has a fantastic REE mix, with roughly 50-60% of its content being REEs.

It is one of the highest quality minerals for the production of Rare Earth Metals yet has been produced as a waste by-product by several US firms, including Chemours. Chemours will supply monazite to Energy Fuels, due to regulations introduced by the U.S. Nuclear Regulatory Commission in 1980. As a waste product, it places its raw material costs within range of China’s.

The main reason that Monazite hasn’t been processed in the US before is simple. It contains high levels of Thorium, roughly 5-10%, and a smaller amount of Uranium. Getting a license to process radioactive materials is notoriously difficult, which is where Energy Fuels come in.

Energy Fuels already has a permit to process Uranium, which also allows them to process the Thorium present in Monazite. They have a great deal of expertise in the separation process, already possessing all the necessary equipment and organisational structures.

Essentially, Energy Fuels already have all the permits and infrastructure they need whilst hardly making a dent in their huge capacity of 720,000 tonnes per year. At present, they are implementing a pilot scheme of 2,500 tonnes per year and aim to reach 15,000 tonnes per year.

There is potential for Energy Fuels to produce roughly 80% of the U.S.’s REE demand, making the company a game-changer in terms of global supply.

Cullen sees a US government offtake agreement as a “no brainer” which will help ensure that they remain economic, despite China’s grip on the market.

Cullen also foresees a possible collaboration with NEO Performance Materials, which owns the Silmet refining facility in Estonia, potentially creating a complete processing chain fully independent of China.

“With this view and Energy Fuels’ current valuation of $550 million, I believe the re-rating of the stock has only just begun,” said Cullen.

And all of this is on top of Energy Fuels’ position as the biggest Uranium and Vanadium producer in the U.S.

Greenland Minerals LTD (ASX:GGG)

The second company Cullen is interested in is the Australian firm Greenland Minerals Ltd. While it is far more speculative than Energy Fuels, it does have potential.

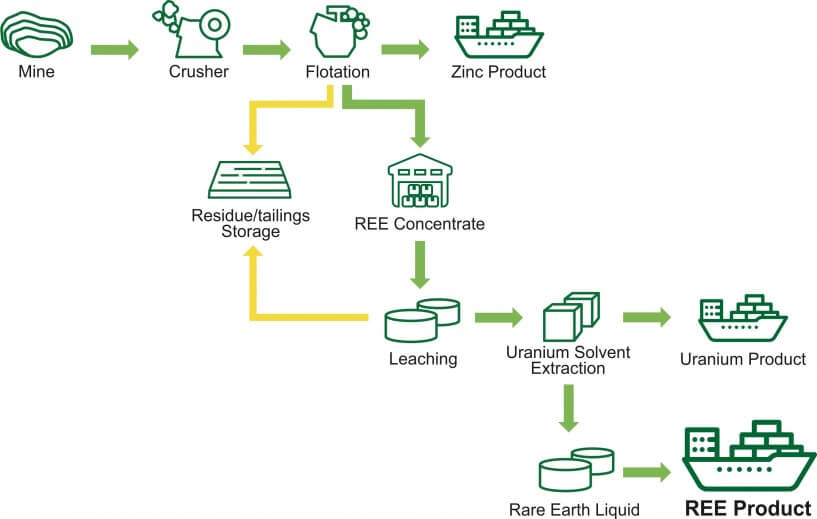

Greenland Minerals is one of the newer players in the market, but Cullen stresses that it has the right geochemistry to be a potential success. With over 11 million tonnes of REEs at their Kvanefjeld site in Greenland, they aim to generate 80% of their revenue from REEs whilst the rest will be from Uranium and Zinc mined as by-products.

The site contains roughly 590 million lbs of Uranium which give the mine resilience should the REE side not meet expectations. Cullen thinks “that it could be a Uranium story as well as a Rare Earth story.”

However, he emphasises that the company is 10% owned by Shenghe Ltd, a Chinese firm, which suggests that it will be China that finances the mine in exchange for an offtake agreement of sorts. Unlike Energy Fuels, Greenland Minerals hasn’t managed to dodge Chinese influence.

Ferg’s Verdict

First of all, Cullen stresses the dangers of this industry. With China having such an enormous degree of power, the likelihood of success for junior REE minors is low.

The combination of a margin of safety and an asymmetrical investment in a company like Energy Fuels makes sense to Cullen, as the main business is already successful in the Uranium and Vanadium markets.

For Energy Fuels it would be a pleasant surprise if the REE venture takes off but it isn’t a necessity for their core business.

Greenland Minerals also holds some promise but it is far more speculative than Energy Fuels. It is 80% reliant on the success of its REE business and it is beholden to China to a degree.

Cullen concludes with some perspective for investors: “To put this in context, Energy Fuels is getting pushed up to a 5% position in my portfolio while Greenland Minerals sits at 0.5%.”

Analyst's Notes

Subscribe to Our Channel

Stay Informed