.webp)

Alamos Gold Inc.

NYSE: CLOSED

TSE: CLOSED

LSE: CLOSED

HKE: CLOSED

NSE: CLOSED

BM&F: CLOSED

ASX: CLOSED

FWB: CLOSED

MOEX: CLOSED

JSE: CLOSED

DIFX: CLOSED

SSE: CLOSED

NZSX: CLOSED

TSX: CLOSED

SGX: CLOSED

NYSE: CLOSED

TSE: CLOSED

LSE: CLOSED

HKE: CLOSED

NSE: CLOSED

BM&F: CLOSED

ASX: CLOSED

FWB: CLOSED

MOEX: CLOSED

JSE: CLOSED

DIFX: CLOSED

SSE: CLOSED

NZSX: CLOSED

TSX: CLOSED

SGX: CLOSED

Commodities

Development Stages

Exchanges

Project Locations

Themes

Carolina Rush

Crux Investor Index

5

–

Market Cap (USD)

9539974

Symbol

TSXV:RUSH

OTCQB:PUCCF

Stage of development

Exploration

Primary COMMODITY

Gold

Additional commodities

Copper

Nickel

Company Overview

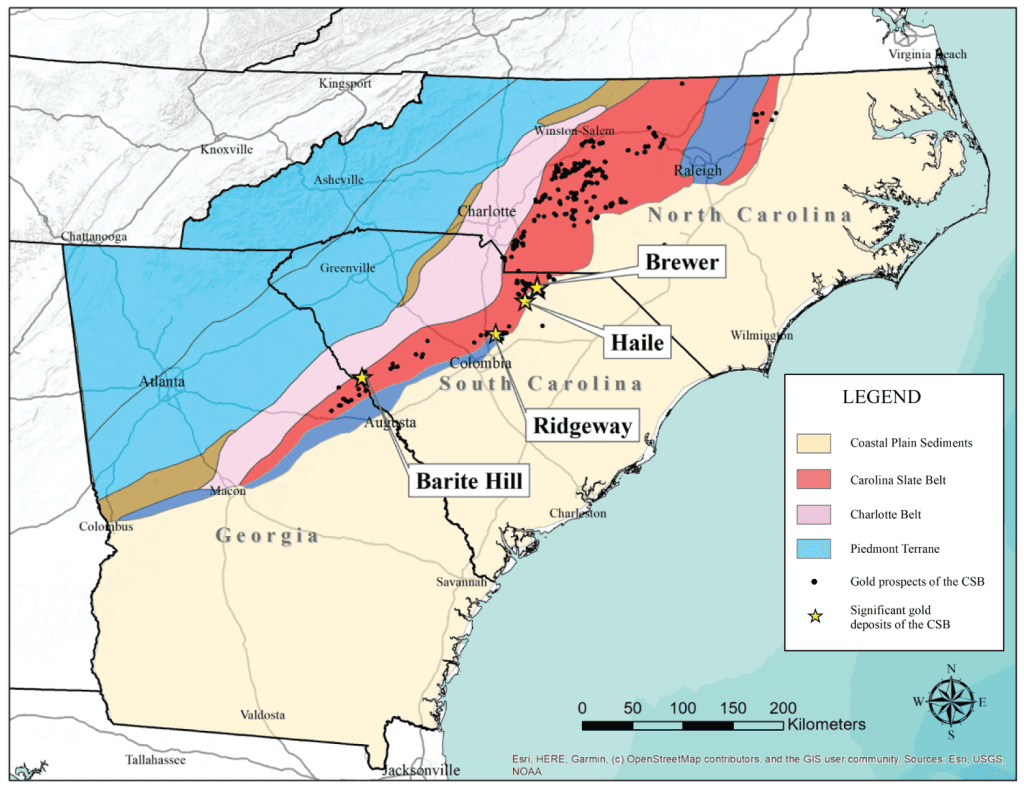

Carolina Rush (TSXV: RUSH; OTCQB: PUCCF) is a junior gold-copper exploration company advancing the Brewer Gold-Copper Project, a brownfield asset located in South Carolina near the town of Jefferson. The Brewer site has a documented mining history stretching back to the 1820s, with modern production occurring between 1987 and 1995 when oxide gold mineralization was extracted using heap leach technology, yielding approximately 178,000 ounces of gold. Following the cessation of mining in 1999, the US Environmental Protection Agency assumed responsibility for the site's water treatment operations and placed it on the Superfund National Priorities List in 2005. Carolina Rush was awarded the option to explore Brewer in January 2020 following a competitive process overseen by a South Carolina state-appointed receiver, positioning the company as custodian of an asset with known gold endowment but historically unexplored depth potential. The company completed a maiden National Instrument 43-101 mineral resource estimate in August 2025, prepared by Qualified Person Patrick J. Hollenbeck, establishing an in-situ resource of 192,000 ounces of gold in the Indicated category and 210,000 ounces Inferred, alongside a theoretical backfill resource of 139,000 ounces Inferred. This resource base was constructed using a combination of Carolina Rush's own core and rotary airblast drilling together with extensive historical drilling and production blasthole data, including 194 rotary airblast holes, 1,020 historical drill holes and 49,926 historical production blastholes.

Opportunity

The central investment case for Carolina Rush rests on the transition from a known, near-surface gold resource to a company now testing for a much larger copper-gold porphyry system at depth, funded by a partner rather than by shareholder capital. In September 2025, Carolina Rush entered into an earn-in agreement with OceanaGold, which operates the Haile gold mine approximately 13 kilometers from Brewer and therefore brings direct geological familiarity with the district. Under the agreement, OceanaGold committed to fund up to US$20 million of exploration in stages, beginning with a minimum US$1.5 million spend within 12 months, rising to US$8 million for a 50% project interest by December 2027, and up to US$12 million for an 80% interest by December 2030.

Separately, Carolina Rush holds the Brewer property under an option from the US government, consistent with the EPA's title to the site under the Superfund designation, and OceanaGold would be responsible for paying the purchase price of approximately US$26.7 million to the US government to secure its 80% interest if it exercises the option by the end of 2030. Carolina Rush retains a carried 20% interest through to the full US$20 million exploration threshold, meaning the company is not required to fund the deep drilling program itself, regardless of whether or when OceanaGold exercises the option. Between January and April 2026, OceanaGold funded the first systematic deep drill program at Brewer, completing 3,579 meters across three holes and confirming a hydrothermal alteration system extending beyond one kilometer in depth. Assay results from the first hole, B26C-037, returned 410 meters averaging 183 ppm copper from 198 meters downhole, including higher-grade intervals of 78 meters at 260 ppm copper and 14 meters at 490 ppm copper, with copper hosted in chalcopyrite consistent with a porphyry system, though no economic gold-copper mineralization was identified in this hole. Hole 38 intersected gold-copper mineralization below the lithocap for the first time, confirming a copper-gold porphyry system, while Hole 39, did not encounter porphyry mineralization but demonstrated expanded potential for near-surface mineralization. The opportunity therefore combines an established, quantifiable gold resource as a baseline value with a copper-gold porphyry system now confirmed at depth, tested at no direct cost to Carolina Rush shareholders.

Management

Carolina Rush is led by Layton Croft as President, CEO and Director, who brings 30 years of global experience including 20 years in mining and exploration, with prior senior roles at Ivanhoe Mines, Rio Tinto, Peabody Energy and Duke Energy, and current service as Chairman of Erdene Resource Development. Patrick Quigley, a Qualified Person under NI 43-101 with more than 15 years of exploration experience across base and precious metals systems, serves as VP Exploration, and leads exploration strategy, drilling execution and geological interpretation. Mark McMurdie, CFO, brings more than 30 years of senior financial leadership across public and private companies, including CFO roles at Sylla Gold Corp and KO Gold Inc. The technical and strategic advisory bench includes David Burrows, a former Chief Geologist at Vale with a specialization in porphyry copper-gold systems directly relevant to the Brewer deep target, and Laurie Curtis, an independent director who led the team behind the Tujuh Bukit gold-copper discovery in Indonesia, cited as an analog to the geological setting at Brewer. Additional board depth comes from Don McLean, a senior gold analyst at Paradigm Capital with capital markets experience, and Brahm Spilfogel, a former Managing Director and Senior Portfolio Manager at RBC who oversaw more than $2 billion in assets across multiple funds.

Growth Strategy

The company's near-term growth strategy is oriented around de-risking and expanding the porphyry target using OceanaGold's committed capital rather than shareholder dilution. With Hole 37 results in hand and Holes 38 and 39 pending, the immediate priority is full integration of the combined geological, geochemical and geophysical dataset to refine the vector toward a potential intrusive centre, with Phase 2 drilling targeting the northwest extension where the alteration system appears to strengthen.

Beyond the porphyry test, the existing in-situ gold resource of 192,000 ounces Indicated, plus 349,000 ounces Inferred across the in-situ and backfill categories combined, is based on only 36 company-drilled holes supplemented by extensive historical data, a point the company itself identifies as a value driver at its current stage. The staged nature of the OceanaGold earn-in also creates defined near-term catalysts: the minimum spend milestone at 12 months, the decision point on continuation once all Phase 1 results are analyzed in the second half of 2026, and the Stage 1 earn-in milestone in December 2027.

Each of these represents a point at which the market can reassess project economics without requiring Carolina Rush to raise additional exploration capital. The jurisdictional setting is a brownfield site in South Carolina with established permitting precedent from prior mining and Superfund remediation activity.

Financial Overview

As of June 1, 2026, Carolina Rush traded at $0.12 per share, with 90,799,482 shares outstanding and a fully diluted share count of 128,549,730 when including 31,662,748 warrants at an average exercise price of $0.205 and 6,087,500 options at an average price of $0.301. This gives the company a market capitalization of approximately $11.3 million against a 52-week trading range of $0.065 to $0.20. Cash on hand as of December 31, 2025 stood at $2.7 million. Insider ownership is reported at 20%, with institutional ownership at 23%, high-net-worth investors representing 37% of the share register, and retail holding the remaining 20%. Analyst coverage is provided by Don Blyth at Paradigm Capital. The most material financial consideration for prospective investors is that the exploration program testing the porphyry target, which represents the primary re-rating catalyst, is being funded by OceanaGold rather than by Carolina Rush's own treasury, meaning the company's cash position is not a binding constraint on the pace of drilling at Brewer, though it will remain relevant to the company's ability to fund other corporate activities and any resource expansion drilling outside the earn-in structure.

Risk Factors and Mitigation

- Commodity Price Volatility: The project's economics, including the resource estimate's reasonable economic extraction cutoff, were calculated using a three-year trailing gold price of US$2,045 per ounce. Sustained declines in gold or copper prices would affect the economic viability of both the in-situ resource and any future porphyry discovery, though the company's own carried interest structure limits its direct capital exposure to commodity swings during the earn-in period.

- Regulatory & Permitting Risks: Brewer's history as a Superfund site introduces environmental oversight considerations, though the EPA has stated that the site under current control and maintenance poses no threat to people or the environment. The brownfield, pro-mining jurisdiction of South Carolina is cited as offering established permitting precedent relative to a greenfield project.

- Technical & Operational Risks: Hole 38 confirmed gold-copper porphyry mineralization below the lithocap, though Hole 39 did not encounter porphyry mineralization, indicating the system remains only partially defined and further drilling will be required to establish its scale and continuity. The backfill resource also remains theoretical pending metallurgical studies. The in-situ resource model was validated using two independent estimation methods, Inverse Distance Squared and nearest neighbor, along with visual and swath plot validation, and the exploration program is overseen by technical advisor David Burrows, a former Chief Geologist at Vale with a specialization in porphyry copper-gold systems.

- Environmental & Social Risks: The site's history includes a 1990 tailings dam breach that released cyanide solution into a nearby waterway, an incident that was addressed at the time by repairing the dam and tailings pond, after which mining resumed in 1991. A separate water treatment plant was later constructed during the 1995–1999 mine closure and reclamation period to manage acid drainage, and this system has since been operated by the EPA, which confirms the site under its current control and maintenance, costing approximately US$1.3 million per year, poses no threat to people or the environment.

- Financing Risk: While the porphyry exploration program itself is externally funded, Carolina Rush's broader corporate and resource expansion activities depend on its own cash position of $2.7 million and access to capital markets. The company's carried interest in the OceanaGold earn-in means its primary near-term catalyst is not contingent on Carolina Rush raising additional capital.

- Execution Risk: The earn-in structure depends on OceanaGold continuing to meet its staged expenditure commitments and electing to proceed through subsequent decision points, and a decision not to continue after Phase 1 results are fully analyzed would shift funding responsibility back to Carolina Rush. OceanaGold has already met its minimum US$1.5 million spend commitment, completing the full Phase 1 deep drill program between January and April 2026 as scheduled.

Conclusion

Carolina Rush combines a quantified, NI 43-101-compliant gold resource of 192,000 ounces Indicated plus 349,000 ounces Inferred across the in-situ and backfill categories, built from a substantial historical and current drilling database, with a well-funded mid-tier producer that has now confirmed a copper-gold porphyry system at depth through its Phase 1 drilling program. Hole 38 intersected gold-copper mineralization below the lithocap for the first time, while Hole 39 demonstrated expanded near-surface mineralization potential without encountering porphyry mineralization itself, meaning the system's full scale and continuity remain to be defined through further drilling.

The staged OceanaGold earn-in, together with its separate option exercise arrangement, under which OceanaGold would pay the US government approximately US$26.7 million to secure full exercise of its interest, provides defined milestones through 2030 that will progressively clarify both the scale of the porphyry opportunity and Carolina Rush's retained interest in it. Investors should weigh the still-developing definition of the porphyry system, the theoretical status of the backfill resource, and the site's environmental legacy against the combination of an established resource baseline, externally funded and now partially successful exploration, an experienced technical and management team, and a favorable operating jurisdiction.

Article

Carolina Rush Analyst Notes

No analyst notes

Charts

Similar Companies

Stay Informed

Sign up for our FREE Monthly Newsletter, used by +45,000 investors

By clicking send you'll receive occasional emails from Crux Investor. You always have the choice to unsubscribe within every email you receive.