Asian Urbanization & the Titanium Pigment Cycle Driving Accelerated Power Demand, Pulling Forward Returns Linked to REEs, Nickel, & Rutile

Uranium supply deficits, policy shifts, and SMR demand are reshaping nuclear markets. Utilities abandon spot purchasing for premium long-term contracts.

- Asia's sustained urbanization and industrial power demand expands construction, autos, white goods, and infrastructure activities that represent core end-markets for TiO₂ pigments in paints, plastics, and coatings.

- Structural feedstock quality shift toward chloride-route TiO₂ processing keeps natural rutile in premium territory versus ilmenite/synthetic rutile, with supply concentration across a few heavy mineral sands jurisdictions creating scarcity dynamics.

- Western supply-chain re-shoring initiatives (United States, European Union), China export/tech controls (rare earth elements), and permitting frictions elevate the scarcity premium for high-grade, low-impurity rutile feeds across global markets.

- Brownfield mineral processing hubs and heavy mineral sands mines with co-product streams capture multi-cycle optionality and lower weighted average cost of capital through diversified revenue streams.

- Energy Fuels (United States heavy mineral sands/rare earth elements hub), Sovereign Metals, Pensana Plc, Namibia Critical Metals, Ionic Rare Earths, Ucore Rare Metals, (rare earth elements midstream build-out), and Canada Nickel (industrial metals signal) illustrate corporate positioning aligned to the macro theme.

Why Asia's Urbanization & Power Demand Matter Now

Asia's demographics, industrial policy, and infrastructure catch-up continue to compound electricity consumption and fixed-asset investment. Asia currently houses 54% of the global urban population (over 2.2 billion people), with urbanization rates projected to increase from 51% in 2020 to 66% by 2050, representing an additional 1.2 billion urban residents. This translates into higher per-capita coatings usage (housing starts, commercial real estate, public works) and original equipment manufacturer demand (automotive, appliances, machinery). Coatings intensity typically scales with urban income and built-environment maintenance cycles, pulling TiO₂ demand structurally higher through both new build and recoat cycles.

The grid build-out (transmission towers, substations, protective coatings) and transport links (Belt and Road Initiative-style corridors, ports, roads) add long-duration paint demand. China's 14th Five-Year Plan allocates USD 4.2 trillion toward transportation and urbanization infrastructure projects, creating sustained pigment requirements across multi-year construction cycles.

The same urbanization forces driving titanium dioxide consumption also elevate demand for industrial metals including nickel in stainless steel infrastructure, electrical grid components, and electric vehicle manufacturing. This parallel demand growth creates correlated investment cycles where financing conditions and policy support for one critical mineral sector often benefit adjacent materials, particularly when projects offer co-product optionality across multiple commodity streams.

Asia will account for more than 60% of global urban population growth through 2030, with the region's urban population exceeding 2.6 billion people despite maintaining a lower overall urbanization rate (53%) compared to other regions. This structural demand expansion differs from cyclical construction booms, providing a durable foundation for titanium feedstock demand across multiple economic cycles.

The Titanium Dioxide Flywheel, From Construction to Feedstock

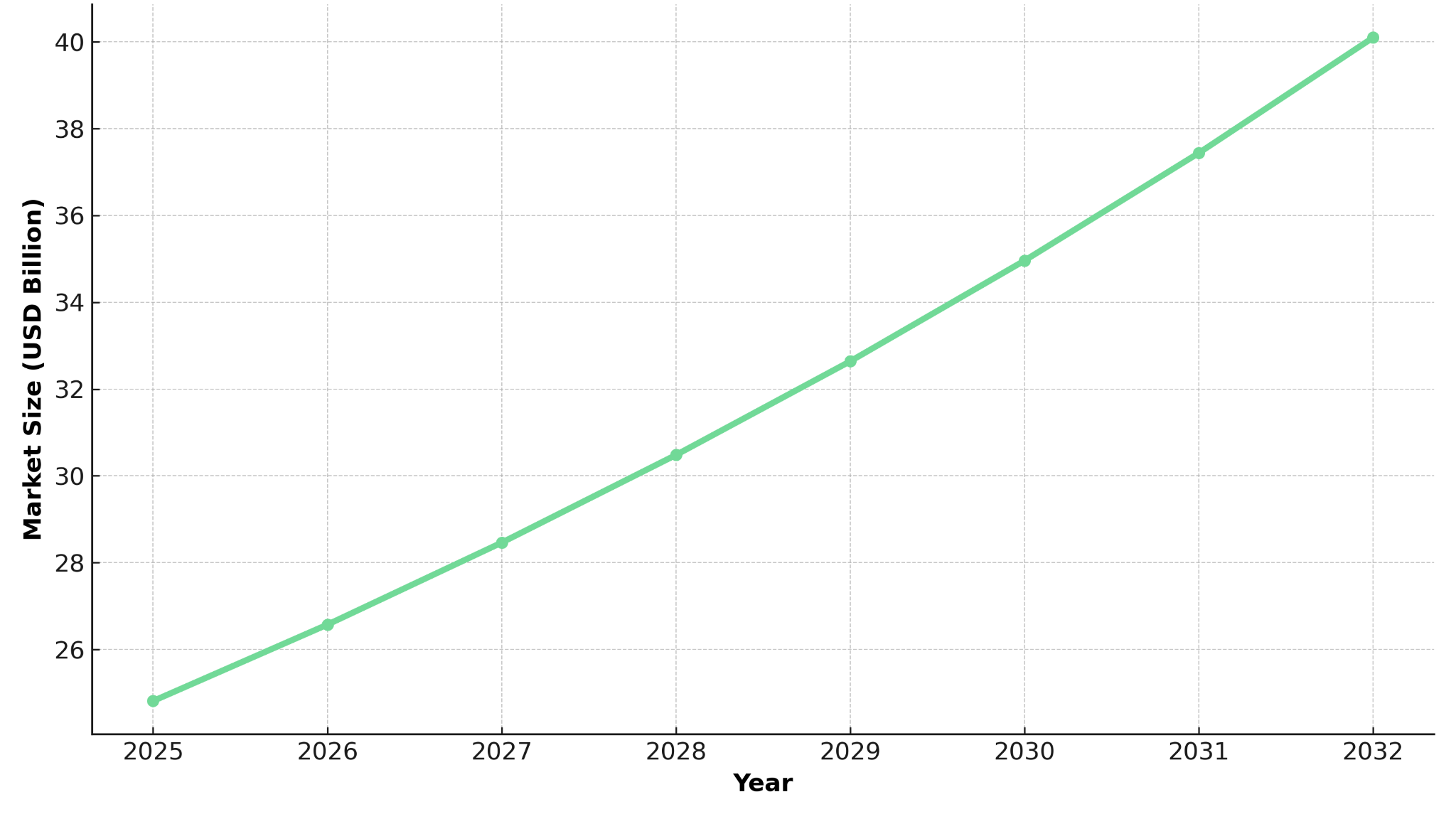

TiO₂ is the dominant opacifier and whitener in architectural and industrial coatings, plastics, and papers, with the global market valued at USD 24.81 billion in 2025 and projected to reach USD 40.07 billion by 2032 at a compound annual growth rate of 7.1%. Asia-Pacific dominates with a 53.95% market share, driven by construction and manufacturing activities across China, India, and Japan. Two processes dominate pigment production: sulfate (currently 53-78% of production, more tolerant of lower-grade ilmenite) and chloride (prefers high-TiO₂, low-impurity feed such as natural rutile or upgraded ilmenite/synthetic rutile).

Because natural rutile is geologically rarer and concentrated in a handful of heavy mineral sands provinces, its pricing tends to outperform on quality spreads when TiO₂ operating rates tighten. Asia's urbanization accelerates this mechanism: higher coating demand leads to higher TiO₂ pigment runs leads to a feedstock pull biased toward rutile for premium grades, especially for architectural durability and corrosion-resistant industrial coatings.

The feedstock quality imperative extends beyond titanium minerals to encompass rare earth elements processing, where high-purity separation requires specific mineral assemblages and processing expertise. Heavy mineral sands deposits that contain monazite alongside rutile benefit from this dual demand vector, as rare earth elements midstream capacity development creates additional revenue streams and improves project bankability through diversified cash flows.

Supply-Side Realities, Heavy Mineral Sands Geology, Project Pipelines & Cost Curves

Natural rutile is typically recovered from heavy mineral sands deposits alongside ilmenite and zircon. Key supply centers include Australia, East Africa, and Madagascar, with project pipelines frequently constrained by coastal ecology, community engagement, and logistics. While synthetic rutile upgrades ilmenite to raise TiO₂ content, its cost and energy intensity can cap volumes, especially under carbon-cost regimes or feedstock impurity constraints.

The natural rutile pipeline has thinned as legacy operations deplete and new projects face permitting lead times of three to seven-plus years. Unit cash cost dispersion hinges on strip ratios, mineral assemblage, slimes management, and co-product credits (zircon, rare earth element monazite). Projects that integrate modular wet concentration with brownfield processing or existing tailings handling can compress capital expenditure and lower execution risk, improving bankability and internal rate of return.

World-class scale becomes particularly important in achieving competitive cost positions within heavy mineral sands operations. Exceptional project economics emerge from geological advantages that enable simple processing methods, as Ben Stoikovich, Chairman of Sovereign Metals explains regarding the Kasiya project's cost advantages:

"The geological structure, hosted in soft, friable saprolite, enables simple processing, basic scrubbing. This results in an incremental cost to produce graphite of only $241 US per ton."

Heavy mineral sands geology often presents additional complexity through rare earth elements-bearing minerals like monazite, which can significantly enhance project economics but require specialized processing capabilities and regulatory approvals. The intersection of titanium feedstock demand with rare earth elements supply chain security creates compounding value for deposits with appropriate mineralogy, particularly as Western governments prioritize domestic critical minerals processing capacity.

Energy Fuels operates a fully licensed hydrometallurgical hub at White Mesa Mill capable of processing monazite from global heavy mineral sands streams that co-produce rutile, ilmenite, and zircon. The brownfield advantage reduces execution risk compared to greenfield developments, while the facility's rare earth elements processing capability creates additional revenue streams from monazite byproducts.

The scarcity of Tier-1 rutile units suggests multi-cycle pricing resilience and contracting power for reliable suppliers. Geological constraints further complicate the supply outlook, as heavy mineral sands deposits require specific geological conditions that limit potential discovery areas. This geological scarcity underpins the structural supply tightness that benefits existing and near-term producers.

Policy & Geopolitics, Why Scarcity Premiums Persist

Western supply-chain strategies (United States "mine-to-magnet," European Union Critical Raw Materials Act) prioritize domestic/ally processing, lifecycle sustainability, and traceable feedstocks, tailwinds for high-grade rutile and heavy mineral sands operations in rule-of-law jurisdictions. Simultaneously, China's tech/export controls in critical minerals have reinforced the risk case for diversified midstream capacity outside China. Although most acute in rare earths, this policy architecture spills over to heavy mineral sands: monazite co-products, chloride-route feed reliability, and pigment plant life cycle assessment reporting drive premium for clean, secure rutile.

The rare earth elements sector exemplifies how policy imperatives create cascading benefits for heavy mineral sands projects. China's export restrictions have created acute supply-demand imbalances that benefit Western producers, as Chief Executive Officer Tim Harrison of Ionic Rare Earths observes:

"China restricted export licenses on heavy rare earths in April, creating a situation where there is a dramatic demand where can I get it."

This supply constraint has elevated dysprosium pricing to three times Chinese quoted prices in Europe, creating substantial premiums for Western sources. The strategic imperative extends beyond immediate pricing as Chief Executive Officer Pat Ryan of Ucore Rare Metals notes:

"The need for a western supply chain price or a floor pricing model is crucial to protect against manipulation and ensure that investors know there is an economic outcome."

The United States Department of Defense investment in establishing floor pricing for neodymium/praseodymium creates similar support structures for heavy rare earth elements, indirectly benefiting heavy mineral sands projects with monazite co-products.

Where Value Accrues Across the Chain

In tightening cycles, the margin stack favors reliable feed (miners with rutile units, co-product credits) and processing hubs with permitting and radiological licenses already in place. Pigment producers secure premiums on specialty grades but face input cost pass-through lag; mining/processing nodes with optionality (Ti, Zr, rare earth elements, U) can smooth earnings before interest, taxes, depreciation, and amortization and maintain capital expenditure discipline across cycles.

Scale advantages become particularly pronounced in heavy mineral sands operations where fixed infrastructure costs can be amortized across larger production volumes. The economics of world-class deposits demonstrate this principle, with projects achieving exceptional returns through geological advantages that enable low-cost production as Chief Executive Officer Ben Stokovich of Sovereign Metals explains:

"The Kasiya project in Malawi is a massive deposit covering over 200 kilometers, ranking as the world's largest rutile deposit and the second-largest natural graphite deposit globally."

The project's exceptional scale enables robust economics with pre-tax net present value exceeding $2.3 billion United States and 64% operating margins, while graphite co-production provides additional revenue diversification at minimal incremental cost.

Co-product leverage extends beyond traditional heavy mineral sands assemblages into high-value specialty metals that command substantial premiums. Heavy rare earth elements represent particularly attractive co-product opportunities given their strategic importance and limited supply sources, as Managing Director Darren Campbell of Namibia Critical Metals notes:

"Namibia Critical Metals is developing the Lofdal heavy rare earth project in Namibia, which is described as one of the largest deposits of dysprosium and terbium anywhere in the world outside of China."

These high-value rare earth elements trade at substantial premiums, with dysprosium selling around $201 USD per kilogram and terbium selling around $890 USD per kilogram, creating significant value enhancement potential for projects with appropriate mineralogy.

Similarly, Pensana Plc's Longonjo project in Angola demonstrates how rare earth elements processing capacity outside China benefits from current supply chain constraints. The project's Stage 1 capital expenditure of $217 million and planned production of 20,000 tonnes per annum of mixed rare earth carbonate from late 2026 reflect the economics of developing Western processing capacity during a period of heightened geopolitical tensions.

Market Setup, Pricing, Cost Curves, Contracts & Timing

Rutile markets are characterized by long-term contracts with pigment producers, often reflecting quality differentials (TiO₂ grade, impurity suite) and logistics. The cost curve bifurcates among natural rutile, synthetic rutile, and upgraded ilmenite. When pigment utilization rises (driven by Asia's construction and industrial cycles), premium feedstock clears first, with price signals strongest where chloride capacity dominates.

From a capital cycle perspective, new rutile units can require multi-year permitting, water/environmental and social impact assessment baselines, and coastal infrastructure. This keeps the market inelastic in the near term. Projects with permitted hydromet capacity or co-product cash flow are more likely to reach final investment decisions on cycle. Rapid development timelines become increasingly valuable in tight commodity markets, as demonstrated by integrated projects in established mining jurisdictions. Chief Executive Officer Mark Selby of Canada Nickel illustrates this advantage:

"Canada Nickel is moving quickly, expecting to get the federal permit in place within just over six years from the fifth drill hole, and aiming to be in production by 2027 or 2028."

Contract structures increasingly reflect the strategic nature of rutile supply. Unlike spot-driven commodities, rutile transactions often involve multi-year agreements with embedded quality specifications and delivery guarantees, providing revenue visibility for producers and supply security for consumers. This contractual framework supports project financing and reduces execution risk for developers with established relationships.

Risk Management, Regulatory Trends, Environmental Social Governance & Foreign Exchange

Key risks include commodity cyclicality where demand shocks can compress TiO₂ runs, permitting and social license challenges for coastal heavy mineral sands projects, environmental regulations favoring higher-grade feeds, and foreign exchange/rate exposure in international projects. Geopolitical risks involve export restrictions and trade route disruptions that can affect both supply and demand dynamics.

Successful risk mitigation often involves technological innovation and operational efficiency. Ucore's RapidSX™ technology exemplifies this approach, requiring one-third of the space compared to traditional solvent extraction while offering modular scalability with low capital expenditure of "$65 million United States for Stage 1 (2,500 tons per annum) versus $300 million for a traditional solvent extraction plant.

Environmental, social, and governance considerations increasingly influence project viability and financing access. Early-stage environmental baseline work not only de-risks permitting but also improves access to capital as lenders tighten due diligence requirements. Projects with established community agreements and transparent environmental management plans often secure more favorable financing terms.

Portfolio Construction: Position Sizing, Catalysts & Liquidity

For institutional and sophisticated retail mandates, rutile exposure should balance execution certainty with growth potential across the development spectrum. Brownfield processors offer immediate production capability and cash flow generation, while development-stage projects provide leverage to commodity price appreciation and resource expansion.

The modular nature of many rare earth elements separation facilities enables staged development that matches capital deployment with market conditions. Ionic Rare Earths emphasizes this flexibility, with Chief Executive Officer Tim Harrison noting:

“Our recycling approach is fundamentally much more straightforward than processing all 15 rare earth elements, focusing on separating four elements (neodymium/praseodymium, dysprosium, terbium), representing 85–90% of the value."

Catalyst timing becomes crucial for position entry and sizing, as heavy mineral sands projects often experience volatile trading around key development milestones. Investors should stage positions into definitive feasibility study/final investment decision milestones, offtake signings, and policy disbursements, using drawdown windows around macro concerns to accumulate fundamentally strong names.

The Investment Thesis

- Macro pulls from Asia where urbanization and power demand translate into durable coatings growth, sustaining TiO₂ volumes across new build and recoat cycles.

- Feedstock quality premium where chloride-route expansion maintains structural premiums for natural rutile and clean upgraded feeds.

- Constrained pipeline where few Tier-1 rutile projects are near final investment decision; permitting elongates supply response, reinforcing multi-year tightness potential.

- Co-product economics where heavy mineral sands assets with zircon/monazite credits and brownfield processing hubs lift internal rate of return/net present value and reduce cash-cost volatility.

- Policy tailwinds where Western re-shoring of midstream (rare earth elements separation, titanium/zircon value-add) lowers weighted average cost of capital and supports offtake finance.

- Execution advantage through brownfield processing capabilities and established regulatory approvals that reduce development risk and accelerate production timelines.

- Scale benefits in world-class deposits that enable low-cost production and superior project economics across commodity cycles.

- Strategic positioning in Western-aligned jurisdictions that benefit from supply chain security premiums and policy support for domestic processing capacity.

Positioning for the Asian Urbanization Pull

Asia's urbanization and electrification underpin a durable, multi-sector demand vector spanning construction materials, industrial metals, energy storage, and permanent magnets, creating interconnected demand growth across titanium dioxide pigments, nickel for stainless steel and batteries, and rare earth elements for electrification technologies. The process shift toward chloride-route titanium dioxide processing amplifies structural premiums for natural rutile feedstocks, while policy-driven supply chain re-shoring elevates the value of Western-aligned critical minerals processing capacity across multiple commodity streams.

With limited Tier-1 supply approaching final investment decision across rutile, heavy rare earth elements, and battery-grade nickel, scarcity dynamics are set to persist across cycles for interconnected critical minerals. Investors should concentrate exposure in execution-ready processing hubs with multi-commodity capability, world-class resource projects offering co-product diversification, and midstream build-out opportunities that improve funding certainty through policy-anchored offtake agreements spanning titanium feedstocks, rare earth elements separation, and industrial metals processing.

Strategic positioning requires balancing immediate production cash flows with development-stage leverage to commodity price appreciation, while using industrial metals indicators and policy disbursement timing to gauge capital cycle health and optimize entry points. The result: a balanced critical minerals portfolio with policy alignment, geographic diversification, co-product resilience, and catalysts sequenced across definitive feasibility studies, final investment decisions, and multi-commodity offtake execution that captures the structural demand growth emanating from Asia's continued urbanization and global electrification trends.

TL;DR

Asia's sustained urbanization and electrification are creating persistent demand growth across construction, automotive, and industrial applications that require titanium dioxide pigments in paints and coatings. This demand expansion, combined with the industry's shift toward chloride-route processing that favors high-grade natural rutile feedstocks, is tightening supply chains and creating scarcity premiums. Western supply-chain security policies and Chinese export restrictions are further constraining rutile availability, benefiting companies with brownfield processing capabilities, world-class heavy mineral sands deposits, and co-product economics from zircon and rare earth elements. Investment opportunities center on execution-ready projects positioned to capture quality premiums and policy-driven re-shoring trends, with catalysts including definitive feasibility studies, final investment decisions, and multi-commodity offtake agreements providing entry timing signals for balanced critical minerals portfolio construction.

FAQs (AI-Generated):

Analyst's Notes

Subscribe to Our Channel

Stay Informed