Bannerman Energy (ASX: BMN) - Solid DFS Puts Uranium Company in Driving Seat

Interview with Brandon Munro, MD/CEO of Bannerman Energy (ASX: BMN).

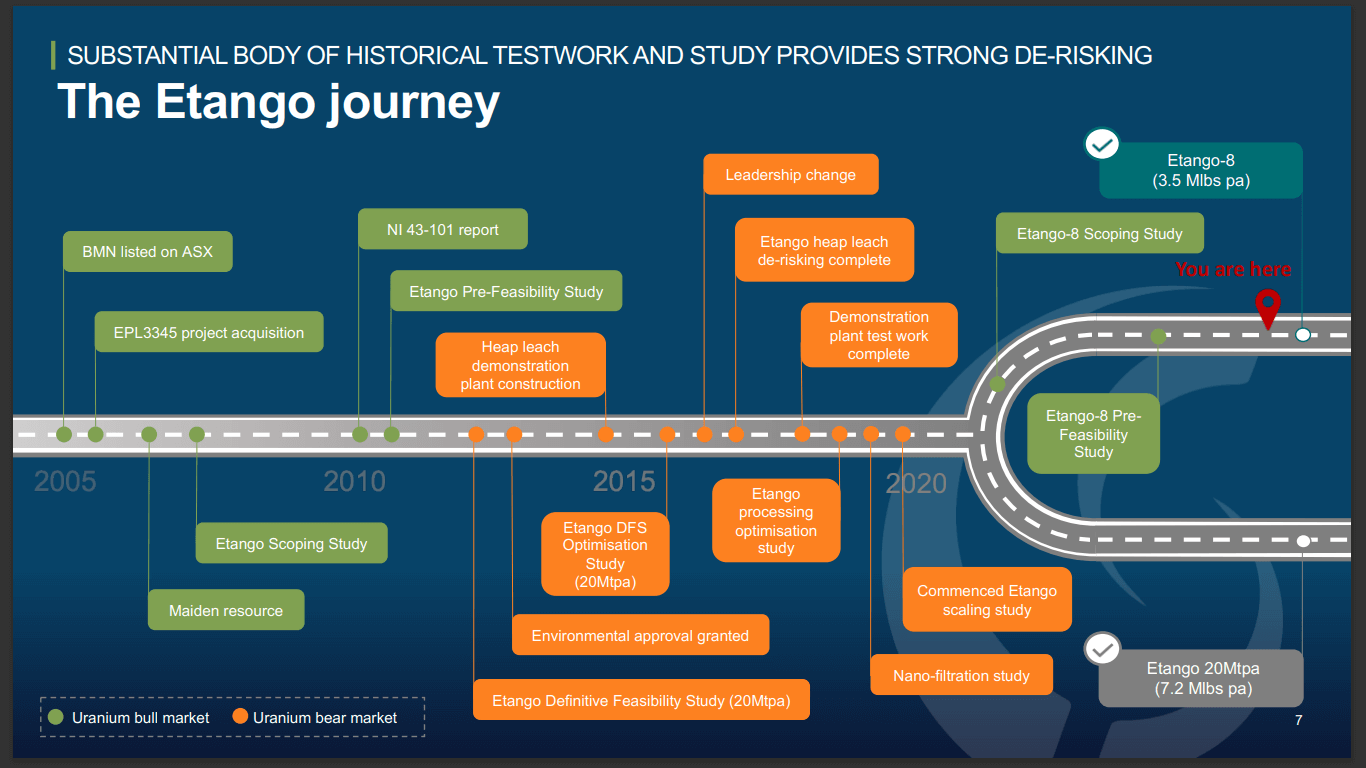

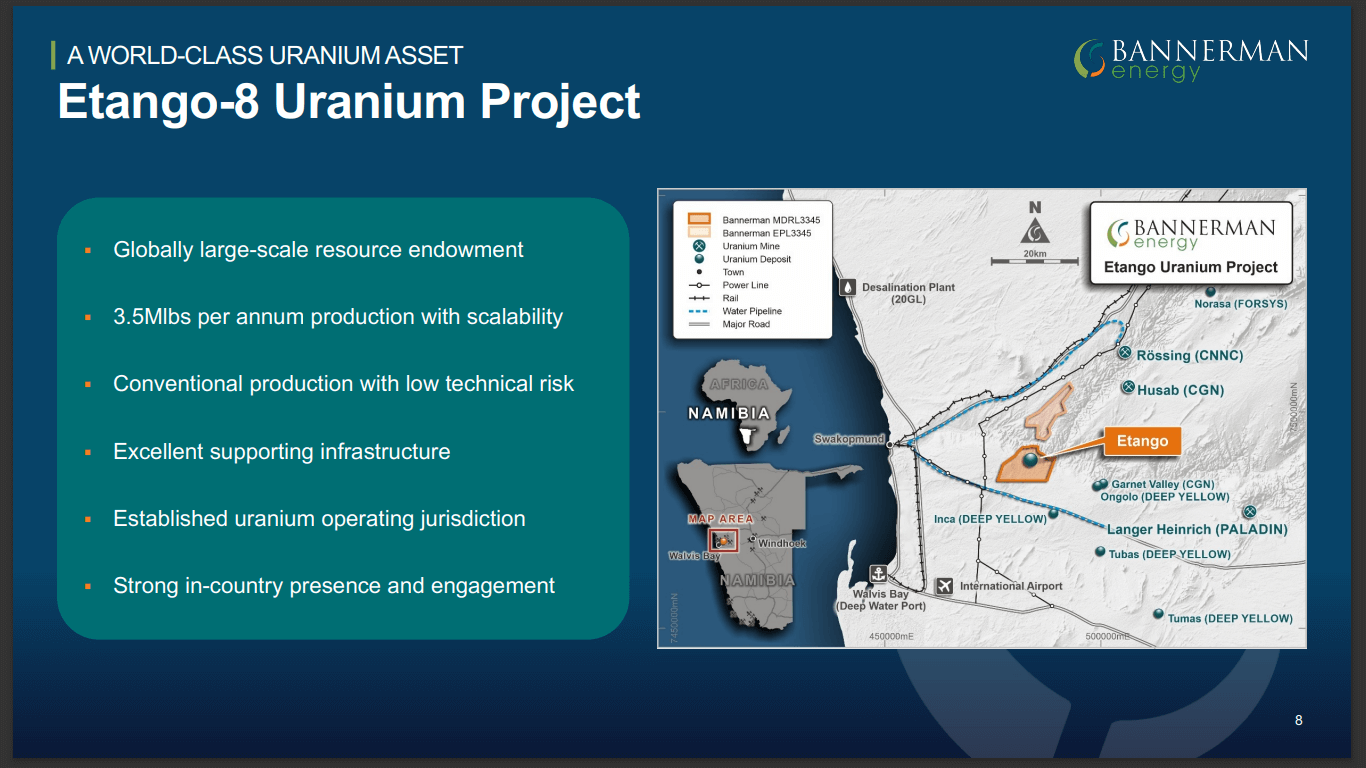

Bannerman Energy Ltd. is an Australian-listed uranium development company. The company’s flagship asset is the Etango Project, one of the world’s largest undeveloped uranium assets. The project is located in the highly established uranium mining jurisdiction of Namibia, where the company has environmental permits in place for development. The Etango Project has been strongly de-risked through extensive drilling, technical evaluation, and operation of a process demonstration plant facility.

Matt Gordon caught up with Brandon Munro, CEO and Managing Director, Bannerman Energy. Brandon has over 20 years of experience as a corporate lawyer and resources executive, including as Bannerman’s General Manager between 2009-2011. He was appointed the company’s CEO in 2016. He lived in Namibia for over five years between 2009-2015, where he also served as Governance Advisor to the Namibian Uranium Association, Strategic Advisor- Mining Charter to the Namibian Chamber of Mines, and Trustee of Save the Rhino Trust Namibia, a high profile Namibian NGO. Brandon is a prominent thought leader within the uranium sector. He has served as Co-Chair of the World Nuclear Association’s Nuclear Fuel Demand working group. He has also been an expert contributor on uranium to the UN Economic Commission for Europe. Brandon’s voluntary service includes board roles in the conservation, arts, and education sector.

Company Overview

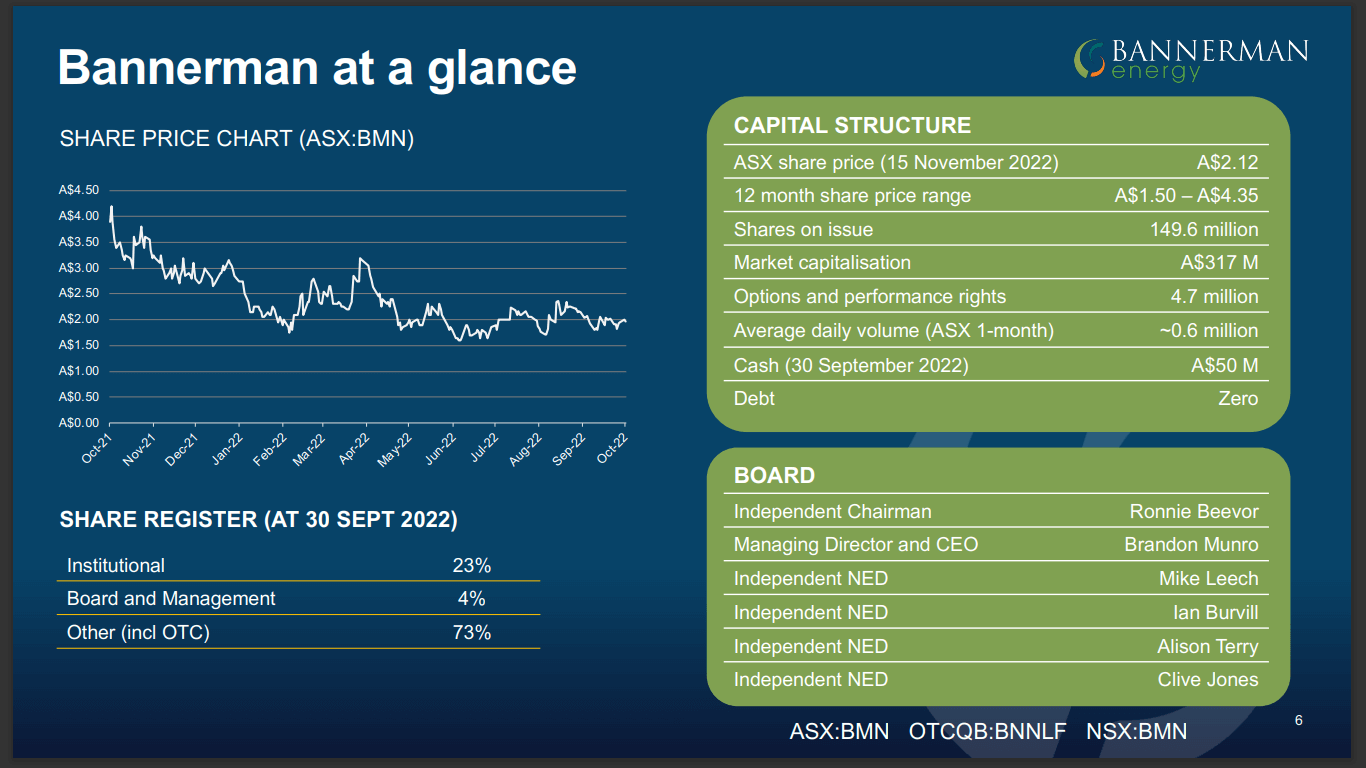

Bannerman Energy is a uranium development company that is established as an ESG (Environmental, Social, and Governance) leader within Namibia, and the global uranium sector. The company exercises best-practice governance in all aspects of its business. The company was founded in 2005 and is based in Subiaco, Australia. It is listed on the Australian Stock Exchange (ASX: BMN), the OTC Markets (OTCQB: BNNLF), and the National Stock Exchange (NSX: BMN).

Bannerman Energy has the Etango Uranium project in Namibia. The company recently released a DFS (Definitive Feasibility Study) on the project and acquired environmental clearances. It is now on the pathway to financing and constructing the project.

The Uranium Market

The uranium market has seen a downturn in recent times. For the DFS, the initial feedback from the analysts and professional investors has been highly positive. The company anticipates that the type of investors that will move the needle in terms of volume and share price need some time to understand the DFS study in depth. Despite the market setbacks, the company is confident that the DFS study will enable it to advance the project further.

For the Etango Project, the post-tax NPV (Net Present Value) is US$209M, delivering a 17% IRR (Internal Rate of Return). These metrics are based on a $65/lb uranium price. The company has assumed the numbers in the study to create contiguity from its PFS (Preliminary Feasibility Study) which was released in August 2021, and the Scoping Study which was released in August 2020.

According to the company, it’s important for the analysts and fund managers to be able to track the progress. The market has changed a lot in recent times, making the uranium sector fundamentally different, more buoyant, and with higher prospects compared to when the company first started operating in 2020. The company has offered an alternative price assumption at $80/lb, which it believes is more appropriate for the investors to judge the project on. An $80/lb uranium pricing would effectively double the NPV, bringing the IRR close to 25%.

Currently, limited long-term contracting is being carried out. Over the past few months, the uranium spot prices are lurking around $50, and things are relatively quiet. According to the company, this is the ideal time to double down on uranium, finish a study, and publish it to the market.

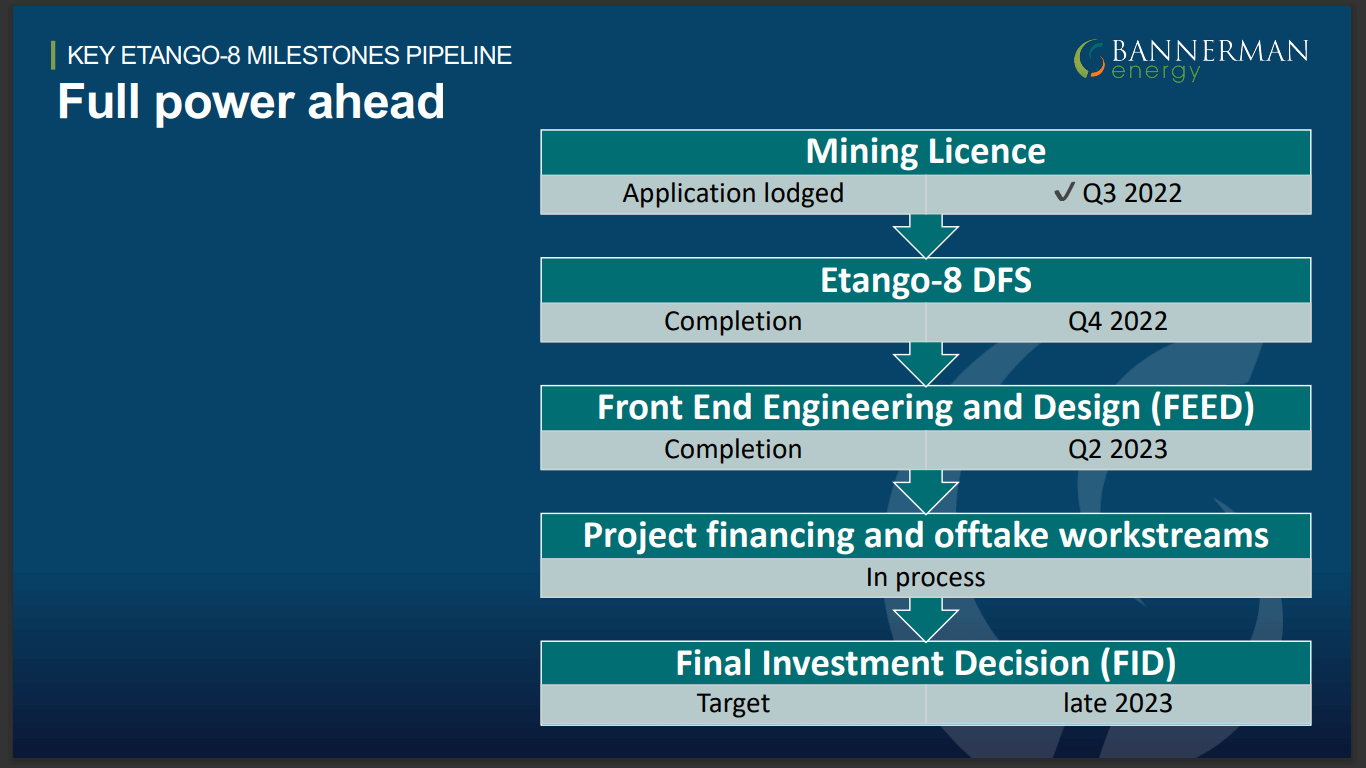

Bannerman Energy has one of the most advanced projects in the uranium sector. The DFS opens doors for further advancing the project. It enables the company to engage with the utilities differently and gauge the government. The quality and results of the DFS study allow the company to have better discussions with the Ministry of Mines and Energy in relation to the mining license. At the same time, the company has progressed through front-end engineering and design.

Following the DFS, the company has a range of different work streams in front-end engineering and design. However, it is looking to rule a line under the main, dominant technical study before it starts chasing different optimizations. The DFS is also a huge enabler when it comes to building the team. This is because people are more likely to leave well-paid jobs when they understand how the project and its potential.

The DFS study takes into account the current market environment, along with ongoing concerns including cost inflation, availability, and supply chain issues. The study defines the economics and the execution plans for the project.

The company is looking to move the project forward so that it can leverage the future bull market. The uranium market has started to reflect the current supply and demand dynamics, and the company is seeing the pricing going through the price targets. This enables the company to immediately finance the project and commence construction to deliver into the market deficit by producing pounds. If the market is ready, the company can effectively have an FID (Final Investment Decision) by the end of next year so that it can start delivering pounds in 2026.

Cash Position

Bannerman Energy has been at the Etango project for 15 years. Shareholders understand that the company is patiently waiting for the right price signals so that it can lock in a contracting portfolio that is optimized for all stakeholders and shareholder value. Notably, the company had $50M in cash flow at the end of September. It hasn’t expended a lot of capital in the current quarter. As a result, the company does not need to rush the financing.

The company intends to carry out financing on its own terms and in a way that suits the shareholders. At the same time, the current cash balance enables the company to continue the engineering to keep moving the project forward without taking on a big debt facility that needs to be drawn down.

Brandon Munro, the company’s CEO has been heavily involved with the WNA (World Nuclear Association) in both the modeling of WNA’s demand and supply forecasts along with other aspects of the organization. As a result, the company is well-integrated into the nuclear sector and has one of the most nuanced understandings of the global uranium sector at large. Over the past 2 years, the company has positioned itself in a way so that it can time the market.

Despite the ongoing cost inflation, the company’s shares have been up by 15%. One of the mines down the road from the Etango project recently published a revised study, which led to a 36% increase in its share price. Bannerman Energy’s team has done a commendable job in controlling cost inflation. The 15% growth includes some new capital on an asset handling facility, where the company intends to build a port, translating to a $10M capital increase. The $10M will be accountable in the new CapEx (Capital Expenditure) introduced by the company. At the same time, the company has secured a 5% operating cost win.

Even though the headline capital number including contingency has gone up a bit, the overall project economics remain essentially the same as the PFS numbers. The company is continuing the front-end engineering and design, along with ongoing investment in advancing the project to ensure that the numbers remain current. The company intends to continue working with the numbers and making them bankable so that it can stand up against the interrogations from counterparties and utilities.

In terms of the capital forecast going forward, some numbers are coming down, while other aspects are going up. One of the major reasons why it has been able to control capital effectively is because a very large portion of the capital is being provided from South Africa. The Namibian dollar is pegged to the South African Rand, and the depreciating value of the latter has greatly benefitted the company.

As all the contracting, earthworks, steel, and concrete comes out of the border from South Africa, the depreciating Rand has helped the company in containing the capital. The company continues to have a number of optimization opportunities that weren’t included in the DFS. It plans to work on these opportunities during the feed process and later stages. These aspects act as a buffer, and the company anticipates that it will be able to maintain the current numbers even in the face of the continuing cost inflation in the broader resources sector.

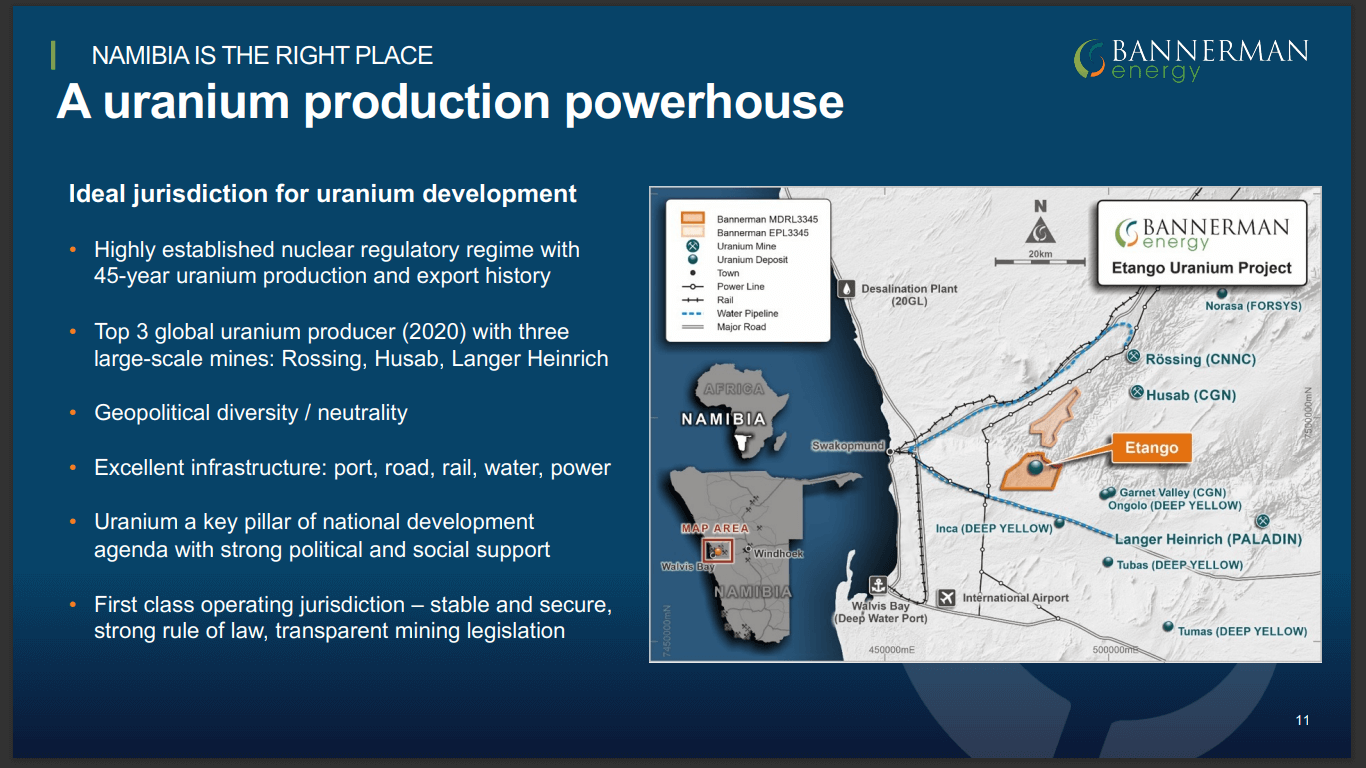

The current uranium market is highly constrained in its current standing. Notably, there are 3 major players that currently dominate the uranium supply, out of which 2 are linked to the government, namely the French and the Kazakhstan government. This leaves only one truly independent player in the sector. The utilities are keen on bringing new production, particularly in Namibia, a country that is very broad in its capacity to deal with different uranium markets.

The Etango Project

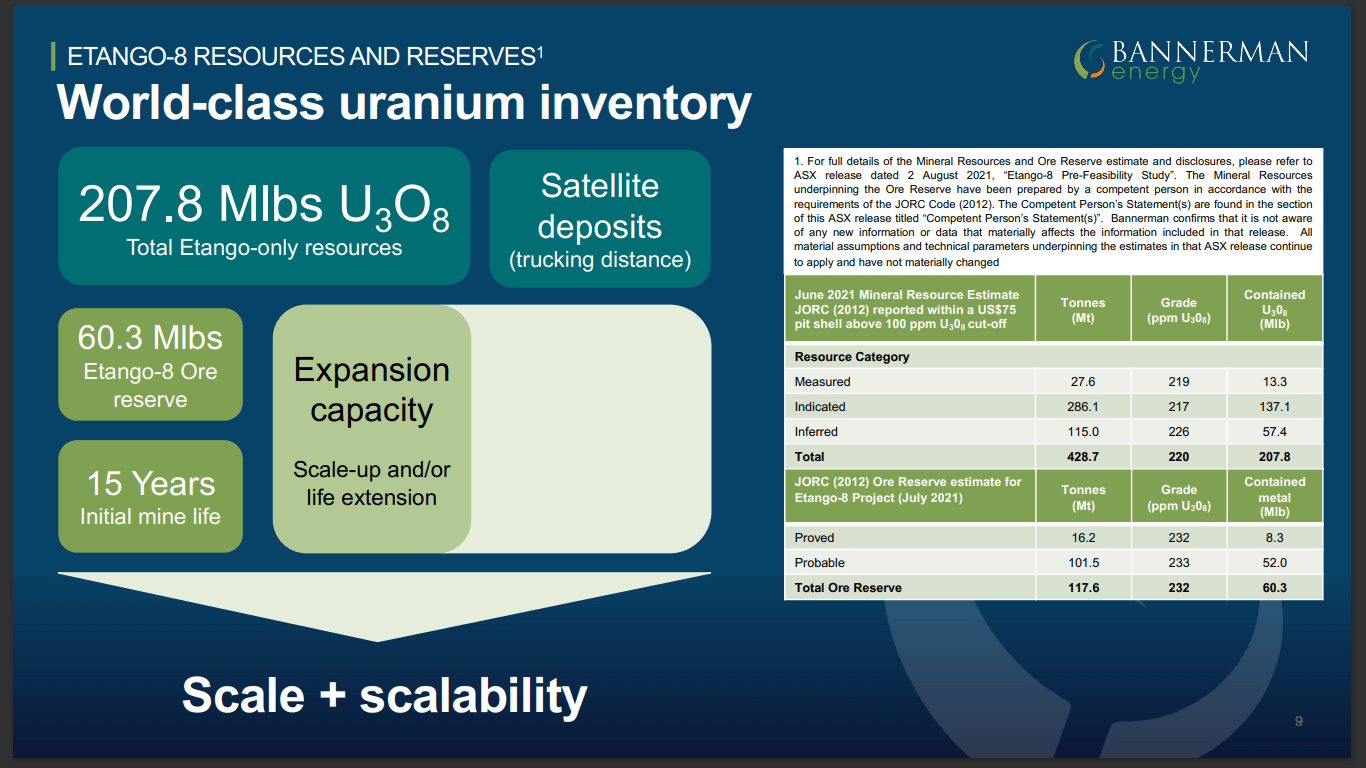

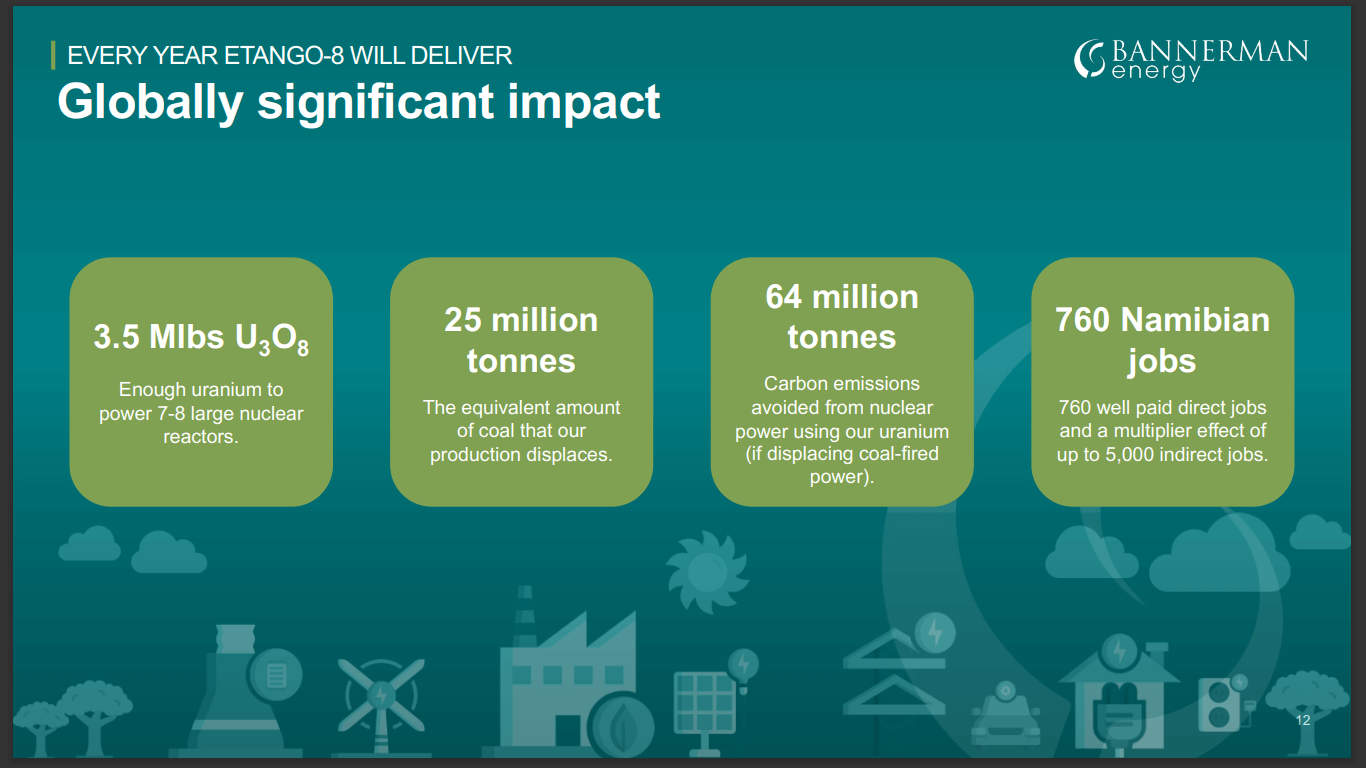

Bannerman Energy’s 3.5Mlbs resource is enough to service 7GW- 8 GW (GigaWatt) of nuclear power. This makes Etango one of the largest uranium projects that are close to development. The company compares the Etango project to the Rossing mine, which was in a similar position in the 80s. Back then, the Rossing asset had a 16 years mine life. The market considered the grade to be low. 45 years later, the Rossing project is looking at an additional 10 years of mine life in a cutback that’s currently under consideration. The Etango asset is expected to have a similar outlook. Within the current resource, the company is willing to drill out over 200Mlbs.

The company has 2 substantial satellite deposits featuring tens of millions of pounds each that are within easy tracking distance. The company has confirmed that the ore body continues under the current pitch. Similar to the Rossing mine, Bannerman Energy plans to drill deeper to access additional pounds. As a result, the utilities believe that the Etango asset has the potential to become a multi-decade source of politically-neutral uranium supply out of Namibia, offering some commercial and geopolitical diversification.

The Etango asset currently has a 3.5Mlbs resource within a total ore reserve of about 60Mlbs. This 60Mlbs ore reserve is the first 60Mlbs of a 130Mlbs ore reserve, which is expected once the project reaches a larger scale. Back in 2015, the company conducted a DFS on Etango at a 20Mt throughput rate per annum. This has been put into the ore reserve, and the 130Mlbs ore reserve sits within a 225Mlbs mineral resource with a couple of satellite deposits. The satellite deposits are present within an ore body, and the company has found continuity at depth through a better understanding of the geology and by drilling deeper holes. It does not plan to expand the resource further due to the current uranium market conditions.

Permitting Considerations

Bannerman Energy already has the permits for environmental clearance, the uranium mine, and other permits associated with the linear infrastructure. It is currently looking to acquire a permit for the temporary construction water pipeline. The Etango project benefits from a well-built infrastructure that provides access to water pipelines, power lines, highways, railways, and a deep water port. As part of the current DFS, the company has received the environmental clearance for the water pipeline from the town of Swakopmund to the project.

Additionally, the company has received environmental clearance for the power lines that need to come from the nearest substation. It also has the heritage commission approvals in place. The pending temporary water pipeline permit is expected within the next few months.

From an operating and tenure point of view, the company does require a mining license application. However, it is important to note that the company has already been granted a 5-year mineral deposit retention license. This means that the company meets all the requirements for a mining license except the price wasn’t right to produce profitably. This was because when the company applied for the license when the uranium price was in the low 20s.

Yesterday, the company’s representatives met with the Ministry of Mines and Energy. It presented the DFS to the Ministry and had a transparent conversation about the mining license. The company is confident that it has support for the license from the Ministry and it will take some work to help them understand the DFS.

Uranium Pricing

According to Bannerman Energy, a $65 uranium pricing is unduly conservative for the Etango project and the market at large. Notably, both the PFS and Scoping Study were conducted with a $65 uranium price. Based on the market indications, the nuclear power thesis, and the uranium macros, the company believed that sub-$80 pricing was appropriate. The number was derived from the company’s internal modeling for the uranium sector, taking into account the number of projects that would come online in this decade to meet the uranium demand requirements. The numbers were also tested with leading industry consultants and their price assumptions. During the oil crisis, uranium pricing reached above $200/lb (adjusted for inflation). The company anticipates that the current market cycle is comparable to the oil crisis.

For investors that are looking to gain leverage on uranium prices above $65 or above $80, the Etango asset serves as a premier project. Through the price sensitivities in the DFS, the company has demonstrated that it has financial leverage and scalability. The company is in a position to deliver a mine life extension over decades, an outcome that is possible through scaling up the 3.5Mlb resource. The company has already factored in a 7.2Mlb or 20Mt resource in the DFS. It has the flexibility to take the 3.5Mlbs resource and modularize it into something significantly larger.

The water pipeline being built is big enough to add an extra pumping station. This would provide sufficient water to produce up to 7Mlbs. This line of thinking was introduced through the PFS and the Scoping Study. As investors start becoming accustomed to the increasing uranium prices and the uranium market begins to enter a bull phase, the company will gain leverage. It anticipates that there will come a time when uranium companies will be valued for the pounds in the ground. Based on this metric, Bannerman Energy has exceptional endowment and outstanding value in the ground. Even if the company restricts the resource down to M&I (Measured and Indicated) category, it would still have a 150Mlbs resource, that was drilled out during the last uranium boom.

According to the company, people who believe that the uranium price won’t surpass $65 do not understand the growth prospects of the nuclear and uranium sector. Through the delivery of the DFS, most of the shareholders have proved that the company has unparalleled price and value leverage to an increase in the uranium price. At an AUD$300M market cap, the company serves as an attractive entry point for investors.

Team Members

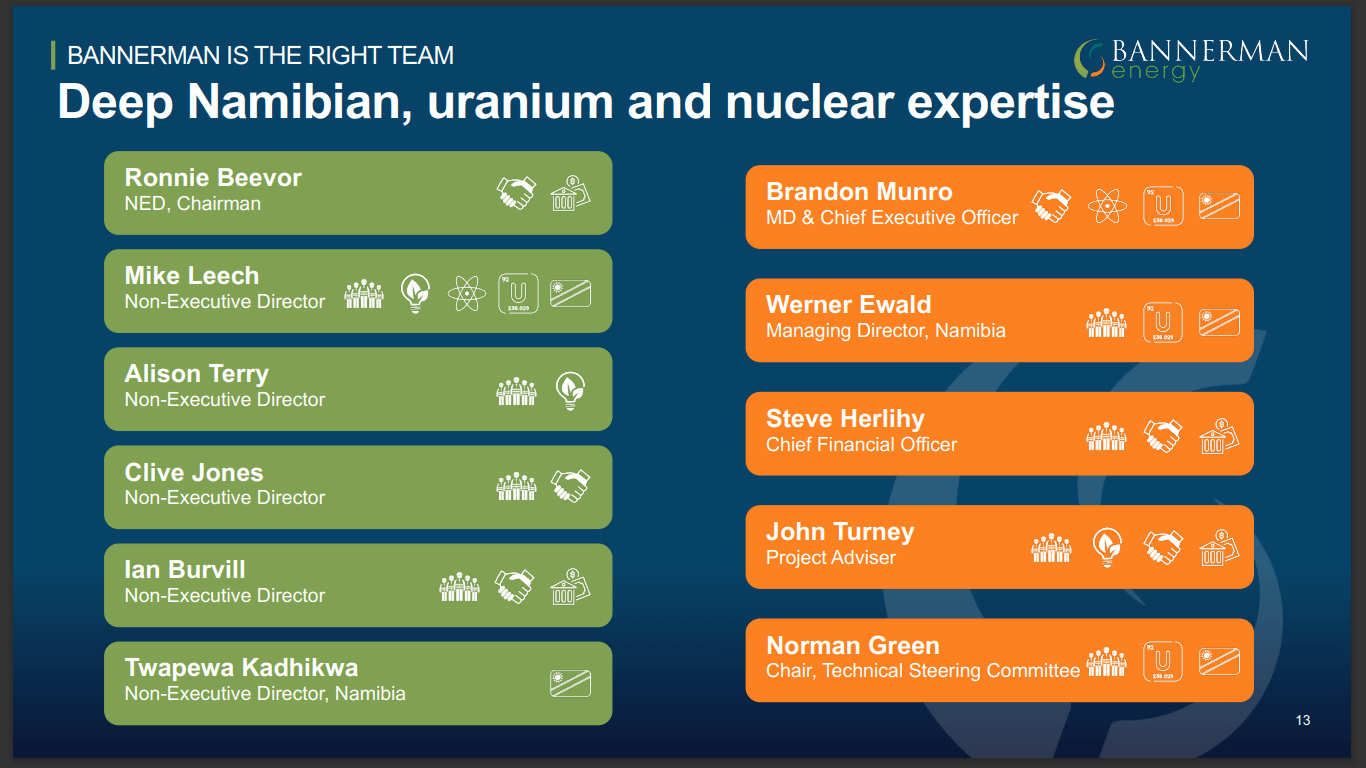

Over the past few years, during the uranium bear market, the company has been working towards bringing in highly-experienced people in key positions to build a commodity-agnostic team. It specifically sought people with expertise in uranium and in Namibia.

Mike Leech was the Managing Director of Rossing Uranium Mine, the largest uranium mine in the world. He continues to be the ideal analog for the Etango project.

Through the DFS, the company realized that the single biggest cost was from mining. As a result, it brought in Werner Ewald, the best mining expert in the country. He previously served as the Mining Manager at Rossing and has been with Bannerman Energy since 2010, as the country’s Managing Director.

Next, the company established a Technical Steering Committee that was chaired by Norman Green. Norman has been responsible for building a few of the 10 largest projects ever delivered in Sub-Saharan Africa, including the Husab Uranium Mine. The project was a $2Bn construction. He also worked on the Scorpion Zinc Mine and Refinery, a multi-billion dollar project from Anglo American. While Norman is semi-retired, he continues to be actively involved in the Etango project. On Monday, the company’s CEO, along with Norman have key appointments with the Ministry of Mines and Energy.

According to the company, having a strong base of knowledgeable personnel in key areas will help attract additional skilled and talented people to the project. Currently, there’s a limited number of people who truly understand uranium. The company is looking to source talented people from both the local uranium industry in Namibia and other commodities and mining sectors.

In mid-2022, the company hired debt advisors for future financings. The advisors are skilled with highly-complex financings. In fact, they recently closed a rare earth financing that involved multi-lateral, multi-party financing, delivering incredible results for an ASX-100 company. The team has a really good understanding of conventional financing for the Etango project. The company is cognizant that there are a range of intermediate steps between conventional financing on one hand and what ultimately the balance sheets of customers will look like if they partake in the financing. Although very few companies are being financed in uranium over the last decade, Bannerman Energy is ahead of the game and it has hired the right people to deliver the results.

Targets 2022 and Beyond

Bannerman Energy has a pedigree of being a uranium company focused on the Etango project in Namibia since 2005. Over time, the company has become well-known in the nuclear power industry. The company’s CEO has had the opportunity to build his profile while also developing collaborative and collegiate relationships in the nuclear power industry. Brandon Munro sits on WNA’s advisory panel that advises the Board and the Director General of the World Nuclear Association. The first time he took the stage at the WNA Symposium was back in 2010.

According to the company, the utilities are distracted at the moment and aren’t signing a lot of contracts. This is expected to turn fairly quickly once the enrichment challenges are resolved and the utilities have secured conversion contracts, following which they are expected to immediately move to uranium. Through the DFS, the company is ready for long-term contracting with the utilities. The DFS provides a fair idea of how cost inflation would impact the sector.

Bannerman Energy is one of the few companies that are cognizant of the actual project costs. This has been made possible through the Scoping Study, the PFS, and the most recent DFS study. Given the current cost inflation environment, DFS studies that are more than 6-12 months old are outdated and no longer provide an accurate forecast of project costs.

For the past 2 weeks, the company has been in a risk-off position. This is because investors are not looking for reasons to buy or to position themselves at a higher uranium price point. The company anticipates that once the investor sentiment returns, people will be looking to position themselves in uranium either for the first time or in a greater way, choosing companies that offer the most potential. The investors’ strategy will shift from saving money to making money.

The Etango project is an outstanding asset with robust economics. As the asset is located in Namibia, the company can develop it fairly quickly. The project also offers a strategic scale along with scalability. These aspects make Bannerman Energy a compelling opportunity for any uranium portfolio.

To find out more, go to the Bannerman Energy website

Analyst's Notes

Subscribe to Our Channel

Stay Informed