Gold Retreats on Dollar Strength & Fed Pause Signals: A Tactical Reset for Rate-Sensitive Investors

Gold drops 1.5% to $3,940/oz on dollar strength and reduced December rate cut odds. Despite correction, stagflation risks and Fed uncertainty support long-term positioning.

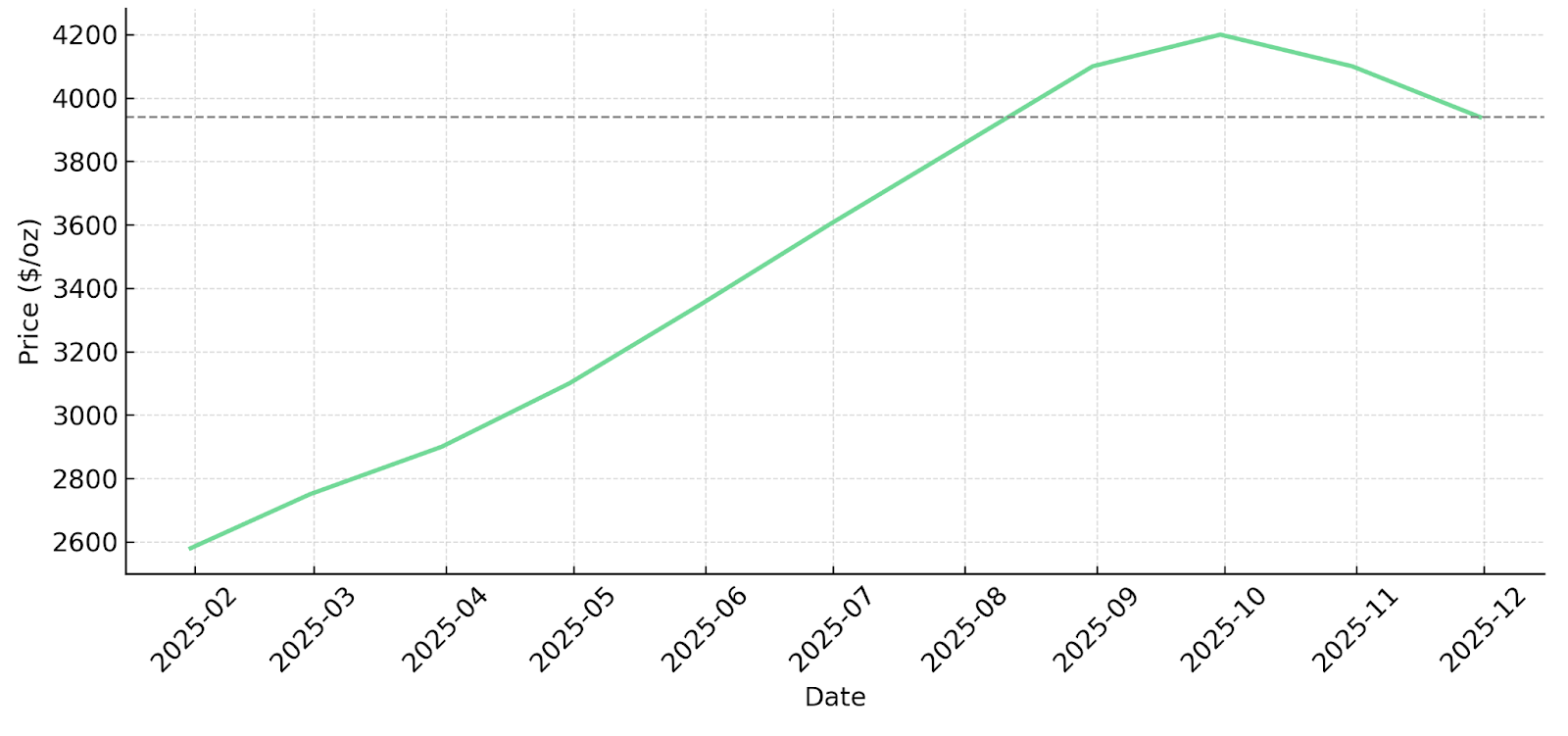

- Spot gold declines 1.5% to $3,940/oz, marking a 9% pullback from October highs after a 53% year-to-date rally.

- Dollar index at three-month highs reinforces short-term downside pressure as traders reduce rate-cut bets to 71% from over 90% the prior week.

- United States data blackout from the government shutdown shifts investor focus to private reports like ADP Employment Data for policy cues.

- Despite short-term volatility, stagflation and geopolitical risks continue anchoring long-term gold allocation strategies.

- Leading developers and producers such as Perseus Mining, Integra Resources, and i-80 Gold demonstrate resilience through cost discipline, cash flow generation, and operational leverage to elevated prices.

Gold's Pullback Reflects a Reset, Not a Reversal

Gold's recent 1.5% decline—trading near $3,940/oz—marks the sharpest weekly pullback since the October 20 record high. With spot prices now 9% below that peak, analysts interpret the move as a necessary correction in a market still up 53% year-to-date.

The immediate catalyst is a resurgent United States dollar, now at a three-month high, which raised the cost of gold for non-dollar buyers and curtailed speculative flows. Futures markets mirror this recalibration, with December contracts hovering near $3,960/oz.

Rhona O'Connell, analyst at StoneX, contextualized the pullback: "Gold is losing some froth while still pricing in concerns over Fed independence and the possibility of stagflation as well as underlying geopolitical risk and international tensions. Some of the froth has been blown off in a much-needed correction."

Shifting Fed Dynamics & the New Cost of Carry

The most significant macro pressure comes from waning rate-cut optimism. According to CME FedWatch data, the probability of a December rate cut has dropped to 71%, down from over 90% a week earlier. Federal Reserve Chair Jerome Powell's statement that recent borrowing-cost reductions may be "the last of the year" signals a possible pause in easing, complicating gold's near-term narrative.

Higher yields increase the opportunity cost of holding non-yielding assets like gold, prompting some investors to rotate into fixed-income markets. This dynamic also affects mining equities, as funding costs and discount rates rise—particularly for developers advancing feasibility-stage projects.

Impact on Projects with Capital Intensity

Projects like Integra Resources' DeLamar (feasibility study expected Q4 2025) and U.S. Gold Corp's CK Gold Project (prefeasibility stage, advancing toward permitted construction) are directly exposed to this macro variable. Integra Resources' DeLamar Technical Report, dated October 31, 2023, provides the foundation for a project now approaching feasibility study completion, while U.S. Gold Corp's February 2025 PFS reports all-in sustaining costs of $937/oz.

George Salamis, President and Chief Executive Officer of Integra Resources, emphasized downside protection amid rate volatility:

"We're covered on the downside, we have puts down to $2,750, which basically locks in a margin for us that guarantees the cash flows to go back into the operation to make it self-sustaining and grow."

Cost of Capital & Hedging Discipline

Producers like Perseus Mining, which reported zero debt and $837 million in cash and bullion as of September 2025, are positioned to outperform peers during rate transitions.

Craig Jones, Managing Director and Chief Executive Officer of Perseus Mining, articulated the company's risk management philosophy:

"Our hedging policy is prudent. Gold's not always going to be at $4,100 an ounce, and there is always downside protection that's needed… Even more recently we've been focusing on just buying put options because they've been relatively cheap. We're finding ways of having more exposure to the upside but at the same time protecting the downside moving forward."

Dollar Strength & the Currency Effect on Cost Curves

A strengthening dollar exerts dual pressure: it erodes international demand for bullion and inflates operating costs for miners outside the United States who report in local currencies.

Operational Impact Across Jurisdictions

For Brazilian producers like Serabi Gold and developers like Cabral Gold, the dollar's rise affects consumables and capital imports, though currency dynamics can partially offset input cost pressures. Serabi Gold, an established producer and sustainable operator with 2025 guidance of 44,000 to 47,000 ounces, has historically maintained production in the 30,000 to 40,000 ounce annual range.

Mike Hodgson, Chief Executive Officer of Serabi Gold, highlighted the dual tailwinds supporting Brazilian operations:

"We've got this great economic tailwind, not just gold price, but gold price plus Brazilian exchange rate, the Real to the dollar. That's really helped too."

Cabral Gold, a developer advancing its Stage 1 oxide heap-leach project toward construction, demonstrates how development-stage projects in emerging jurisdictions can structure competitive economics. The company's updated Prefeasibility Study, released July 29, 2025, reports all-in sustaining costs of $1,210/oz with an after-tax internal rate of return of 78% at a $2,500/oz gold price assumption. The project targets 25,000 ounces annually during the initial two years, with initial capital expenditure of $37.7 million and a 12-month construction timeline.

Alan Carter, President and Chief Executive Officer of Cabral Gold, quantified the profitability leverage:

"We should be producing 25,000 ounces of gold per year at an all-in sustaining cost of just $1,210 per ounce. At the current gold price, this means we should be making a profit of almost $3,000 per ounce, or around $70 million United States dollars per year."

Portfolio & Jurisdictional Diversification

Producers like i-80 Gold in Nevada and West Red Lake Gold Mines in Ontario operate in jurisdictions with established mining codes and historical permitting precedent. The United States Immediate Measures to Increase American Mineral Production Executive Order, signed in March 2025, aims to boost domestic mineral production and fast-track permits, potentially improving timeline certainty for Nevada-based operations.

i-80 Gold's Granite Creek Underground entered production in 2025, establishing the company as an emerging Nevada producer. The 2025 outlook projects 20,000 to 30,000 ounces from this asset. In Q2 2025, i-80 Gold reported approximately 8,400 ounces in gold sales at an average realized price of $3,301 per ounce, generating approximately $28 million in total revenue.

Paul Chawrun, Chief Operating Officer of i-80 Gold, emphasized the leverage inherent in the Granite Creek underground project:

"The Granite Creek underground looked like a fairly conservative estimate. Now it's ultra-conservative at $2,175 per ounce… It significantly exceeds that at current spot prices which is over 4,000 today."

Trading Without a Compass: Data Vacuums & Market Psychology

The ongoing United States government shutdown has interrupted official data releases, leaving investors reliant on private indicators such as the ADP Employment Report. This lack of clarity amplifies volatility as markets extrapolate from limited data sets.

Advanced-stage developers like New Found Gold and transitional producers like West Red Lake Gold illustrate how operational milestones attract attention during macro uncertainty. New Found Gold, an emerging Canadian gold developer, has its Queensway Gold Project supported by a Preliminary Economic Assessment with feasibility studies planned to commence in H2 2026. The company targets Hammerdown production ramp-up in early 2026 and Queensway Phase 1 production in 2027.

West Red Lake Gold Mines, a transitional producer that put the Madsen Mine back into production in May 2025, completed successful test mining and bulk sample programs that resulted in approximately 12,800 ounces produced and sold through Q1-Q3 2025. The company is establishing prominent cash flow as it advances toward producing more than 100,000 ounces annually by 2029.

Persistent Risk Anchors: Stagflation, Policy & Geopolitics

Despite short-term softness, gold's underlying thesis remains intact. Institutional flows continue to price in stagflation risk, Federal Reserve independence concerns, and ongoing geopolitical instability.

Inflation Resilience & Cost Compression

Development-stage projects such as Cabral Gold's all-in sustaining costs of $1,210/oz (July 2025 PFS at $2,500/oz gold assumption) and U.S. Gold Corp's $937/oz (February 2025 PFS) provides a substantial cushion relative to current spot prices near $3,940/oz.

Keith Boyle, Chief Executive Officer of New Found Gold, noted the persistent inflationary pressures:

"It's the input costs, right now with the uptick in gold price, inflation will be not far behind. We know that it's a repeating theme."

Emerging-Market Resilience

Latin American developers like Cabral Gold showcase organic growth models that emphasize self-funded expansion. With initial capital expenditure of $37.7 million for the Stage 1 heap-leach operation, the development-stage company aims to minimize reliance on equity financing during construction.

Alan Carter of Cabral Gold emphasized the strategic importance of cash flow generation:

"The cash flow from stage one will more than fund that required drilling and eliminate the need for future dilutive equity finances. It'll essentially mean that we're self-funding."

Mining Sector Resilience Amid Broader Commodity Weakness

Gold's decline also aligns with softness in broader precious metals. Silver fell 1.5% to $47.32 per ounce, platinum eased 1.8% to $1,538.05, and palladium fell 3.1% to $1,400.30.

U.S. Gold Corp, a development-stage company advancing the CK Gold Project toward construction, has secured major state operating permits including the Mine Operating Permit (approved April 2024 for a 10-year renewable term), Industrial Siting Permit (approved June 2023, extended through 2026), and air quality permit (approved November 2024). The project requires no federal involvement as the footprint does not impact waters of the United States per U.S. Army Corps of Engineers Jurisdictional Delineation.

Luke Norman, Executive Chairman of U.S. Gold Corp, highlighted the project's economic strength:

"The economics are outstanding. You've got about an 80% gold economic component and 20% copper economics right now, just because the gold price has surged so high. The fact that we're going to be generating a copper-gold concentrate has led to a lot of interest from the offtakers, and there's been term sheets presented to us from a debt component for building this project."

Integra Resources, an established producer and developer, advances a multi-asset platform with cash flow from its Florida Canyon operating heap leach gold operation—the company's principal operating asset with 2025 guidance of 70,000 to 75,000 ounces—funding project advancement from the DeLamar development project. The DeLamar Mine Plan of Operations was deemed complete by the Bureau of Land Management in Q3 2025, with the Feasibility Study expected in Q4 2025.

i-80 Gold, an emerging Nevada producer, exemplifies how companies transitioning to commercial production can enhance margins through infrastructure control. The company currently processes Granite Creek production through toll milling arrangements, which provide approximately 55-60% of gold value. Development of the Lone Tree Autoclave, currently in technical refurbishment with a study expected in Q4 2025, would increase recovery to approximately 92% by 2028-2032.

The Investment Thesis for Gold

Gold's correction presents a recalibration of portfolio positioning rather than a structural deterioration of the investment case.

- Rate normalization timelines remain uncertain, reinforcing gold's role as a defensive allocation, particularly for inflation-linked portfolios and investors seeking monetary diversification amid Federal Reserve policy ambiguity.

- Currency volatility driven by dollar strength pressures near-term prices but creates operational complexity for international producers while potentially enhancing economics for developers in jurisdictions where local currency weakness offsets input cost inflation.

- Operational discipline among development-stage companies with robust feasibility study economics—such as Cabral Gold's $1,210/oz all-in sustaining costs and U.S. Gold Corp's $937/oz, provides insulation from capital expenditure inflation when projects advance at gold prices substantially above study assumptions.

- Jurisdictional positioning in Nevada, Ontario, and other established mining regions offers regulatory frameworks with historical precedent, though evolving stakeholder expectations and policy initiatives such as the March 2025 United States Executive Order on mineral production create dynamic regulatory environments.

- Cash flow generation from established producers like Perseus Mining, with $837 million in cash and bullion and zero debt as of September 2025, and Integra Resources' Florida Canyon operation producing 70,000 to 75,000 ounces in 2025, provides liquidity and operational stability anchoring sector performance through commodity cycles.

- Self-funding growth models demonstrated by developers like Cabral Gold, with initial capital expenditure of $37.7 million and targeted annual free cash flow sufficient to fund ongoing exploration, reduce reliance on equity or debt markets during periods of monetary tightening.

- Production timelines aligned with multi-year demand growth, as demonstrated by New Found Gold's phased approach targeting Hammerdown production ramp-up in early 2026 and Queensway Phase 1 production in 2027, position companies to capture anticipated structural supply deficits during the production phase.

- Emerging producers like i-80 Gold demonstrate how companies transitioning from development to commercial production can optimize margins through infrastructure control, with Granite Creek Underground production in Q1 2025 and plans to enhance processing recovery through Lone Tree Autoclave refurbishment.

Correction as Calibration, Not Capitulation

Gold's short-term weakness is better viewed as portfolio calibration than structural deterioration. A stronger dollar and rate re-pricing have reset speculative positioning, but long-term allocation drivers, stagflation risk, currency diversification, geopolitical instability, and Federal Reserve policy uncertainty, remain intact.

For investors, this correction provides an opportunity to assess capital efficiency across the gold complex. Producers with disciplined cost bases and strong balance sheets, developers advancing fully permitted projects with robust feasibility study economics, and companies leveraging operational milestones during macro uncertainty all represent differentiated plays on a resilient macro theme.

While the dollar dictates short-term price action, structural scarcity, persistent inflationary pressures, and policy uncertainty anchor the long-term case for gold as a portfolio diversifier and wealth preservation asset. The current pullback offers sophisticated investors a tactical entry point into a sector characterized by improving fundamentals, substantial margins at current prices, and institutional-grade risk management among leading operators.

TL;DR

Gold fell 1.5% to $3,940/oz, 9% below October's record high, driven by a resurgent U.S. dollar at three-month highs and declining December rate cut expectations (now 71% vs. 90% prior week). Fed Chair Powell's signaling of a potential pause in easing increases the opportunity cost of holding gold, pressuring near-term sentiment. However, long-term fundamentals remain intact: stagflation risks, geopolitical uncertainty, and Fed policy ambiguity continue anchoring institutional allocations. Leading miners demonstrate resilience through cost discipline, with developers like Cabral Gold ($1,210/oz AISC) and U.S. Gold Corp ($937/oz AISC) maintaining substantial margins at current prices. The correction represents portfolio recalibration rather than structural deterioration, offering tactical entry points for sophisticated investors.

FAQs (AI-Generated)

1.5% to $3,940/oz primarily due to U.S. dollar strength reaching three-month highs and reduced expectations for a December Fed rate cut (dropping from 90% to 71% probability). Higher yields increase the opportunity cost of holding non-yielding assets like gold, prompting rotation into fixed-income markets.

probability dropped to 71% from over 90% the previous week. Fed rate cuts typically support gold prices by reducing the opportunity cost of holding non-yielding assets. A pause in easing complicates gold's near-term narrative and affects mining equities through higher funding costs and discount rates.

Companies with strong balance sheets (Perseus Mining: $837M cash, zero debt), low all-in sustaining costs (Cabral Gold: $1,210/oz; U.S. Gold Corp: $937/oz), established cash flow (Integra Resources: 70,000-75,000 oz guidance), and jurisdictional advantages in Nevada and Ontario demonstrate resilience through operational discipline and substantial margins at current prices.

A stronger dollar creates dual pressure: it reduces international demand for bullion and inflates operating costs for non-U.S. miners who import consumables and capital equipment. However, currency dynamics can partially offset costs—Brazilian producers benefit when local currency weakness enhances gold price realizations in Real terms.

Analysts view this as a "necessary correction" rather than structural deterioration. Despite short-term volatility, long-term drivers remain intact: stagflation risks, Federal Reserve policy uncertainty, geopolitical instability, and structural supply constraints. The 9% pullback follows a 53% year-to-date gain, representing portfolio recalibration as speculative positioning resets.

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

.jpg)

Stay Informed