Catalyst for Investors: Russian Uranium Ban Ignites U.S. Nuclear Revival

Russian uranium ban to disrupt 24% of U.S. nuclear fuel supply, forcing utilities to seek alternatives and creating opportunities for domestic producers.

Congress Bans Russian Uranium Imports

The U.S. Senate has unanimously passed the Prohibiting Russian Uranium Imports Act (H.R. 1042), which bans imports of low-enriched uranium (LEU) produced in Russia. The bill, previously passed by the House, now heads to the president to be signed into law. Once enacted, the legislation will prohibit the importation of unirradiated LEU produced in Russia or by a Russian entity, starting 90 days after the bill's enactment. The ban will remain in effect through at least 2040, with limited waiver authority granted to the Energy Secretary to allow imports if no alternative sources are available to sustain U.S. reactor operations. Additionally, the bill mandates a market evaluation to assess if further federal support is necessary to expand domestic LEU production capacity and replace Russian supplies.

This legislation represents a significant step towards reducing U.S. dependence on Russian nuclear fuel and creating long-term certainty in the domestic market. By implementing the ban upfront, rather than waiting to develop domestic fuel cycle infrastructure, the bill aims to avoid potential market distortions and wasteful spending. The ban is expected to stimulate investment in U.S. uranium mining, conversion, and enrichment capabilities, which have declined in recent years due to global market disruptions and competition from state-subsidized foreign suppliers.

Reducing Dependence on Russian Uranium

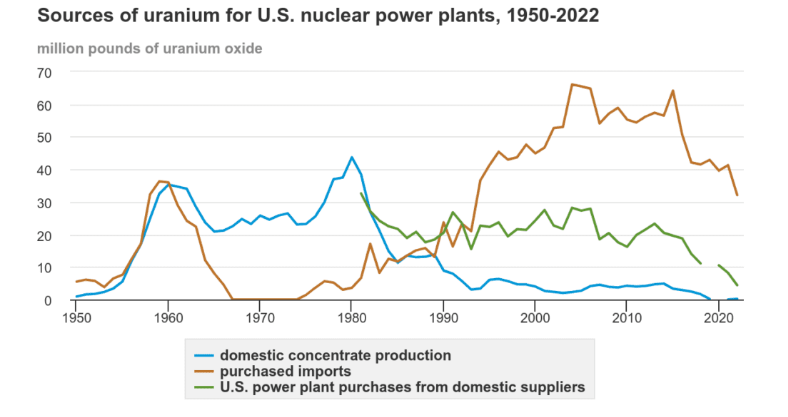

The U.S. currently imports a substantial portion of its uranium fuel, with only 12% of the uranium purchased by U.S. nuclear plant operators in 2022 sourced domestically. While direct imports from Russia account for a relatively small share of total U.S. uranium purchases, Russian-origin enrichment services represented a significant 24% of U.S. enriched uranium demand in 2023. This dependency on Russian supply poses risks to U.S. energy security and the competitiveness of the domestic nuclear fuel industry.

Russia's state-owned nuclear enterprises remain influential in global nuclear fuel supply chains, particularly in the conversion and enrichment stages. With vast production capacities that exceed domestic requirements, Russian suppliers can export enriched uranium products at prices that undercut allied and domestic producers. This market distortion has been detrimental to U.S. supply chains, as repeatedly found by U.S. International Trade Commission investigations over the past three decades.

The ban on Russian uranium imports aims to address this vulnerability and create a level playing field for U.S. producers. By providing long-term certainty that Russian nuclear fuels will not enter the domestic market, the legislation enables a more accurate evaluation of market responses and infrastructure priorities. This assessment will help determine if additional federal support is warranted to assist in expanding domestic production capacity and ensuring a secure, reliable supply of nuclear fuel for U.S. reactors.

Impact on Nuclear Fuel Costs and Supply Chains

The upcoming ban on Russian uranium imports is set to have far-reaching consequences for the U.S. nuclear energy sector. Despite the U.S. sourcing only 12% of its uranium directly from Russia in 2022, a staggering 24% of the nation's enriched uranium demand was met by Russian-origin separative work units (SWU) in 2023.

With Russia dominating the global uranium enrichment capacity at 45%, U.S. utilities have relied heavily on Russian-origin SWU to fuel their reactors. In 2023, an estimated 3.9 million SWU purchased by U.S. utilities came from Russia, while domestic enrichment plants provided just 27% of the demand, and Western European plants supplied the remaining 49%.

The implementation of the Russian uranium ban is expected to disrupt this significant portion of the U.S. nuclear fuel supply chain, forcing utilities to seek alternative sources for nearly a quarter of their enriched uranium requirements. This presents both challenges and opportunities for investors in the domestic uranium mining, conversion, and enrichment sectors, as the industry gears up to fill the void left by the exclusion of Russian-origin SWU.

As the U.S. nuclear energy sector navigates this transitional period, investors should keep a close eye on utilities' strategies to secure alternative fuel sources and the growth and expansion plans of domestic uranium producers and enrichment service providers. The ban's impact on nuclear fuel prices and the long-term competitiveness of the U.S. nuclear energy industry will be key factors to watch in the coming years.

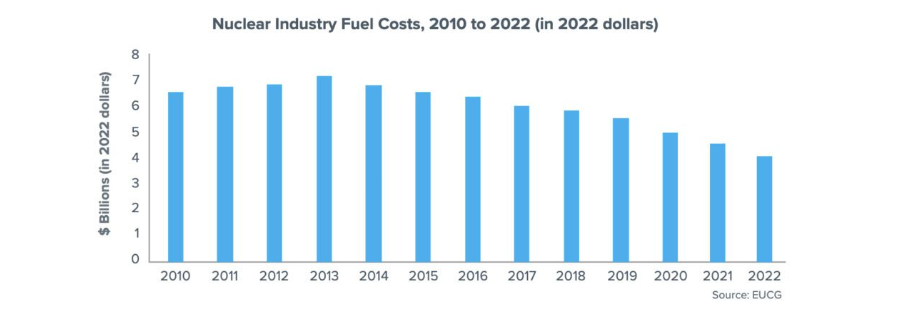

Nuclear fuel costs represent a significant portion of total U.S. nuclear generation costs, accounting for approximately 17% in 2022. While uranium prices have fluctuated over the years, with a notable spike in 2008, the delayed impact on nuclear fuel costs was not fully realized until 2013 due to the long lead times associated with uranium procurement. Utilities typically purchase uranium several years before refueling, and the fuel remains in reactors for four to six years. As a result, the effects of commodity price changes on fuel costs are often delayed.

Following the 2008 price spike, uranium prices remained relatively low for several years, prompting some utilities to shift towards shorter contract cycles. Despite recent price increases driven by the COVID-19 pandemic and the Russia-Ukraine war, U.S. nuclear fuel costs remained comparatively low in 2022. However, utilities are increasingly focused on managing risks to their fuel supply chains, particularly in light of sanctions on Russia and the potential for supply disruptions.

Constellation, a company with a significant nuclear power portfolio, has proactively increased its nuclear fuel purchases to build inventory and mitigate supply risks. The company projects that 44-47% of its capital expenditures in 2024-2025 will be dedicated to acquiring nuclear fuel, ensuring sufficient supply to bridge potential Russian supply disruptions through 2028. This strategic stockpiling aligns with the expected timeline for multiple new suppliers to increase production capacity online, reducing reliance on Russian-origin fuel.

As utilities work to secure their fuel supply chains and minimize exposure to potential disruptions, the Russian uranium ban is expected to accelerate investment in domestic fuel cycle capabilities. The legislation creates a more predictable market environment, encouraging long-term contracts and providing the necessary signals for producers to expand capacity. While the transition from Russian supply may result in short-term cost pressures, developing a robust and resilient domestic nuclear fuel industry is crucial for the U.S. nuclear power sector's long-term competitiveness and energy security of the U.S. nuclear power sector.

Revitalizing the U.S. Nuclear Fuel Cycle

The decline of the U.S. front-end nuclear fuel cycle can be traced back to significant disruptions in the global nuclear fuel market disruptions following the 2011 Fukushima accident. The event suppressed worldwide demand for nuclear fuel, leading to a plummet in uranium prices and a contraction of the domestic uranium mining, conversion, and enrichment industries. As foreign suppliers, particularly those backed by state support, captured market share, U.S. capabilities in these critical fuel cycle stages diminished.

Recognizing the strategic importance of a strong domestic nuclear fuel supply chain, efforts to revitalize the U.S. uranium industry began in earnest in 2020. The Nuclear Fuel Working Group, convened by the Trump administration, outlined a three-pronged strategy to support uranium mining, conversion services, and the development of domestic enrichment capabilities. This strategy has yielded some initial successes, with several U.S. uranium mines restarting operations in 2022-2023 following a rebound in prices and growing demand expectations.

However, the U.S. still faces significant gaps in its fuel cycle infrastructure. Current domestic enrichment capacity can only meet about 30% of the nation's fuel requirements, while the sole operating conversion facility has the potential to supply approximately 40% of U.S. demand in the near term. Substantial investments in new and expanded production capacities are necessary to truly revitalize the U.S. nuclear fuel cycle and reduce dependence on foreign suppliers, substantial investments in new and expanded production capacities are necessary.

The Russian uranium ban serves as a catalyst for this revitalization process, creating a strong market signal for domestic producers and investors. By ensuring a stable, long-term demand for U.S.-origin nuclear fuel, the legislation provides the foundation for the capital-intensive investments required to rebuild the nation's front-end fuel cycle capabilities. This renewed focus on domestic production will not only enhance energy security but also create skilled jobs and strengthen the competitiveness of the U.S. nuclear industry in the global market.

International Collaboration to Boost Supply Chains: The Sapporo 5

In parallel to its domestic efforts, the U.S. has engaged in international collaboration to strengthen global nuclear fuel supply chains and reduce reliance on Russian suppliers. The "Sapporo 5" initiative, a partnership between the U.S., Canada, France, Japan, and the UK, aims to mobilize $4.2 billion in investments to increase enriched uranium production capacity that is free from Russian influence. This collaborative approach recognizes the importance of diversifying supply sources and building resilience in the face of geopolitical risks.

The Sapporo 5 collaboration has already yielded tangible commitments from major nuclear fuel manufacturers to expand their enrichment capacities. Urenco, a leading global enrichment company, has announced plans to add centrifuges and boost capacity by 15% at its New Mexico facility by 2025, while also expanding its plants in the Netherlands and Germany. The company is pursuing regulatory approvals to enrich uranium to higher levels, supporting the development of advanced reactor fuels.

In the U.S., Centrus Energy commenced HALEU enrichment operations at its Ohio facility in late 2023, producing over 100kg of the advanced fuel material by April 2024. The company is working towards an additional 900kg production target, demonstrating the growing domestic capabilities in this critical segment of the fuel cycle. Meanwhile, France's Orano has announced plans to increase enrichment capacity at its Georges Besse II plant by nearly a third by 2028 and is exploring the possibility of constructing an enrichment facility in the U.S.

Other Sapporo 5 members have also made significant commitments to bolster their domestic fuel cycle capabilities. Japan aims to increase its enrichment capacity from 75 to 450 tons SWU annually by 2027, while the UK has pledged £300 million to launch Europe's first domestic HALEU program. These coordinated efforts, alongside Canada's ongoing support for uranium mining and conversion, underscore the global push to establish secure, diverse, and competitive nuclear fuel supply chains.

The international collaboration fostered by the Sapporo 5 initiative complements the U.S. Russian uranium ban, providing a multilateral framework for investments in fuel cycle infrastructure. This partnership accelerates the development of alternative supply sources by leveraging key nuclear energy nations' combined resources and expertise of key nuclear energy nations. It reduces the risks associated with over-reliance on any single supplier. As the global nuclear energy landscape evolves, with a growing emphasis on energy security and the deployment of advanced reactors, international cooperation in the fuel cycle domain will be increasingly vital to ensure a stable, sustainable, and competitive nuclear energy future.

Funding to Expand Fuel Infrastructure

Expanding domestic nuclear fuel cycle capabilities requires significant capital investments, particularly in the enrichment stage. Nuclear fuel firms have emphasized the need for firm off-take commitments, from reactor developers or government entities, to underwrite these investments and provide the long-term demand certainty necessary for infrastructure development.

To support the objectives of the Sapporo 5 collaboration and address the funding challenges, the U.S. has allocated $2.7 billion to build out LEU and HALEU production capabilities. This funding, made available through the FY2024 spending bill, was contingent on the passage of the Russian uranium ban, underscoring the interconnected nature of these policy initiatives. The substantial financial commitment demonstrates the U.S. government's resolve to revitalize the domestic nuclear fuel supply chain and reduce dependence on Russian suppliers.

Other Sapporo 5 members have also pledged significant funding to support the expansion of fuel cycle infrastructure. France has mobilized $1.8 billion, while the UK has earmarked $383 million for its domestic HALEU program. The combined funding commitments from the Sapporo 5 nations have already exceeded the initial $4.2 billion target, highlighting the growing global momentum behind developing secure, diverse, and competitive nuclear fuel supply chains

In addition to the Sapporo 5 funding, the U.S. Department of Energy (DOE) is making targeted investments to address specific gaps in the domestic fuel cycle. The agency recently closed requests for proposals to purchase enriched and deconverted HALEU, leveraging $700 million allocated by the Inflation Reduction Act. These funds, part of the HALEU Availability Program established by the Energy Act of 2020, aim to stimulate demand for advanced fuel materials and encourage private investment in domestic fuel supply infrastructure. The DOE expects to award contracts for enrichment and deconversion services in the summer of 2024, further accelerating the development of a robust and resilient U.S. nuclear fuel industry.

Combining government funding, international collaboration, and targeted investments in key fuel cycle stages creates a powerful enabling environment for expanding domestic nuclear fuel infrastructure. By providing the necessary financial support and policy certainty, these initiatives help de-risk private investments and attract the capital required to rebuild the U.S. front-end fuel cycle capabilities. As the Russian uranium ban takes effect and market demand for secure, domestic supply grows, the groundwork laid by these funding commitments will be instrumental in ensuring a successful transition to a revitalized and self-reliant U.S. nuclear fuel industry.

Industry Optimism and Path Forward

The passage of the Russian uranium ban has been met with optimism from the U.S. nuclear energy industry, which views the legislation as a crucial step towards revitalizing the long-dormant domestic fuel cycle. Beyond prohibiting Russian imports, the bill unlocks the $2.72 billion in funding appropriated by Congress to bolster the U.S. nuclear fuel supply chain, providing the financial support necessary to spur investment in domestic production capabilities.

However, industry stakeholders recognize that substantial market challenges remain on the path to a fully self-sufficient nuclear fuel industry. In a recent technical analysis, the Nuclear Innovation Alliance (NIA), highlighted the need for more detailed public discussion and clear financial strategies to effectively encourage private investment in HALEU production. The NIA report comprehensively assessed HALEU production costs, including uranium enrichment and deconversion expenses. It evaluated potential government initiatives, such as material offtake agreements and production services agreements, as mechanisms to address economic hurdles.

The Nuclear Energy Institute (NEI), representing a broad cross-section of the U.S. nuclear industry, has echoed the need for sustained effort and collaboration to realize the full potential of the Russian uranium ban. NEI President and CEO Maria Korsnick emphasized that rebuilding domestic fuel cycle capabilities to support the existing reactor fleet and enable the deployment of next-generation nuclear technologies will be a multi-year endeavor. She noted that implementing an effective program to support this capacity expansion is critical to the long-term success of the U.S. nuclear energy sector.

To this end, the industry is actively engaging with the DOE to design and implement a comprehensive capacity expansion support program, while also working to establish a predictable and efficient waiver process for the Russian uranium ban. By maintaining open lines of communication and collaboration between industry stakeholders and government agencies, the U.S. nuclear energy sector aims to navigate the challenges associated with transitioning to a domestic-oriented fuel supply chain.

The Russian uranium ban, in conjunction with the recently passed Nuclear Fuel Security Act, establishes a solid foundation for the long-term growth and competitiveness of the U.S. uranium industry. With positive market fundamentals and growing demand for clean, reliable nuclear energy, major uranium companies are well-positioned to ramp up domestic production in the near future. Uranium Energy Corp. (UEC), a leading U.S. uranium company, has expressed its enthusiasm for the supportive policy backdrop and plans to restart uranium production in Wyoming in August 2024, followed by the resumption of operations in South Texas in the following year.

As the U.S. nuclear energy industry navigates the path forward, continued public-private coordination will be essential to address remaining economic hurdles and fully realize the legislation's vision of a secure, competitive domestic nuclear fuel supply chain. By leveraging the momentum generated by the Russian uranium ban, industry stakeholders and policymakers can work together to create a sustainable, long-term framework for the growth and success of the U.S. nuclear fuel cycle.

For investors, the passage of the Russian uranium ban represents a significant positive catalyst for the long-term growth prospects of domestic uranium miners, converters, and enrichers. While the process of rebuilding U.S. fuel cycle capabilities will take time, the combination of substantial government funding, supportive policies, and growing market demand creates a compelling investment thesis for companies well-positioned to capitalize on the evolving nuclear energy landscape.

As utilities work proactively to mitigate supply chain risks and bridge potential disruptions, the demand for secure, domestic nuclear fuel sources is set to rise. The international collaboration fostered by the Sapporo 5 initiative provides further tailwinds, as key nuclear energy nations work together to establish diverse, competitive uranium supply chains that are free from Russian influence.

Investors should remain attuned to the ongoing efforts to address the economic challenges of expanding domestic fuel cycle infrastructure, particularly in the HALEU segment. Successfully implementing government support programs, coupled with clear financial strategies to encourage private investment, will be key to unlocking the full potential of the U.S. nuclear fuel industry.

Companies that are able to navigate the shifting nuclear energy landscape, capitalize on supportive policies, and meet the growing demand for reliable, clean power are likely to be well-positioned for long-term growth and success. As the U.S. nuclear fuel cycle enters a new era, marked by a focus on energy security, competitiveness, and sustainability, investors can participate in revitalising a critical component of the nation's energy infrastructure.

The North American Uranium Companies Likely to Benefit

Energy Fuels: A Leading US-Based Critical Minerals Company

Investment Highlights:

- Leading US uranium producer: Energy Fuels is the top uranium producer in the United States, supplying major nuclear utilities with uranium concentrates for clean, carbon-free nuclear energy production.

- Expansion into rare earth elements (REEs): The Company has recently commenced production of advanced REE materials, including mixed REE carbonate, and plans to produce commercial quantities of separated REE oxides in the future, positioning itself in the growing REE market.

- Vanadium and radionuclide potential: Energy Fuels produces vanadium when market conditions are favorable and is exploring the recovery of radionuclides for emerging cancer treatments, diversifying its revenue streams.

- Strategic US-based assets: The Company owns two key uranium production centers in the US: the White Mesa Mill in Utah (the only operating conventional uranium mill in the US) and the Nichols Ranch ISR Project in Wyoming. These assets give Energy Fuels a significant competitive advantage in the domestic uranium market.

- International expansion: Energy Fuels has acquired the Bahia Project in Brazil, which is believed to contain significant quantities of titanium, zirconium, and REE minerals, offering the potential for further growth and diversification.

- Extensive uranium resource portfolio: The Company holds one of the largest NI 43-101 compliant uranium resource portfolios in the US, along with several uranium and uranium/vanadium mining projects in various stages of permitting and development, ensuring a strong pipeline for future growth.

- Dual-listed on major exchanges: Energy Fuels' common shares are traded on the NYSE American under the symbol "UUUU" and on the Toronto Stock Exchange under the symbol "EFR," providing investors with ample liquidity and exposure to the growing critical minerals market.

With its strong position in the US uranium market, expansion into REEs, and potential for vanadium and radionuclide production, Energy Fuels presents a compelling investment opportunity in the critical minerals sector. The Company's US-based assets, international expansion, and extensive resource portfolio position it well for future growth and success.

enCore Energy: America's Clean Energy Company™

Investment Highlights:

- Newest US uranium producer: enCore Energy Corp. has recently commenced uranium production at its licensed and past-producing South Texas Rosita Central In-Situ Recovery (ISR) Uranium Processing Plant (CPP) in November 2023, positioning itself as the newest uranium producer in the United States.

- Proven ISR technology: The Company solely utilizes ISR for uranium extraction, a well-known and proven technology co-developed by the leaders at enCore Energy. This environmentally friendly and cost-effective method extracts uranium using natural groundwater and oxygen, coupled with a proven ion exchange process.

- Experienced management team: enCore's team is led by industry experts with extensive knowledge and experience in all aspects of ISR uranium operations and the nuclear fuel cycle, ensuring the Company's success in the uranium mining sector.

- Robust production pipeline: In addition to the Rosita Central CPP, enCore plans to restart uranium production at its licensed and past-producing South Texas Alta Mesa CPP in 2024. Future projects include the Dewey-Burdock project in South Dakota and the Gas Hills project in Wyoming, along with significant uranium resource endowments in New Mexico, providing long-term growth opportunities.

- Proprietary uranium database: Encore owns a proprietary uranium database that includes valuable technical information from many past-producing companies, offering a significant competitive advantage in identifying and developing new projects.

- Diversification potential: The Company is committed to realizing value from its various non-core assets and leveraging its ISR expertise to research opportunities for applying this technology to other metals, potentially diversifying its revenue streams.

- Community engagement: enCore is dedicated to working with local communities and indigenous governments to create positive impact from corporate developments, ensuring sustainable and responsible operations.

With its recent commencement of uranium production, proven ISR technology, experienced management team, and robust production pipeline, enCore Energy Corp. presents an attractive investment opportunity in the clean energy sector. The Company's proprietary uranium database, diversification potential, and commitment to community engagement further strengthen its position as a leading uranium producer in the United States.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).jpg)

Stay Informed