Nuclear Innovation Captures Billions While Traditional Uranium Miners Struggle With Execution

Keller shifts 50% to nuclear innovation as tech giants' PPAs create demand certainty without fuel security. Every restart struggles; $80 uranium reflects unfunded promises.

- Australian uranium market remains underwhelming compared to North America, with liquidity concerns and lack of investor conviction despite recent gains, complicated by ongoing political opposition to nuclear power.

- Tech companies like Microsoft, Meta, and Google are becoming price-insensitive end customers willing to commit to long-term power purchase agreements, creating unprecedented demand certainty that hasn't yet translated to fuel supply securing.

- Keller's fund has shifted significantly toward nuclear innovation investments (around 50% of portfolio), moving beyond uranium commodity exposure to capitalise on billions flowing into North American nuclear technology companies.

- Almost every brownfield uranium restart has encountered problems, and greenfield projects remain price-dependent, causing management teams to lose confidence and focus inward rather than pursuing growth through M&A.

- Market hasn't yet priced in three critical catalysts: utility fuel buying urgency, full deployment of US government funding commitments, and actual capital deployment from tech company agreements beyond current MOUs and LOIs.

The Australian uranium market continues to underperform relative to North America, with investor concerns centered on liquidity constraints and limited conviction in the sector's trajectory. While Australian uranium stocks have experienced recent gains, the market lacks the urgency evident in North America, where companies are raising hundreds of millions through convertible notes and equity offerings. This disparity occurs despite Australia's significant uranium resources and potential role in global supply chains.

The political landscape remains challenging, with the federal government's opposition to nuclear power standing in the way of including uranium in critical mineral discussions with the United States.

Portfolio Evolution Toward Nuclear Innovation

Guy Keller's investment approach has undergone significant evolution, particularly regarding exposure beyond traditional uranium mining. Beginning in a smaller capacity in May 2024 and accelerating in recent months, Keller has increased allocation to nuclear innovation to approximately half of the fund's holdings. This strategic shift removes direct uranium commodity price risk while capturing opportunities in North American nuclear technology companies receiving billions in investment driven by data center and technology company demand for baseload electricity.

This nuclear innovation segment demands significantly more active management than traditional uranium holdings, with Keller estimating 5-10 times greater activity in risk management. These investments exhibit extreme volatility, with some positions showing implied volatility exceeding 120%. Rather than trading on traditional valuation metrics which universally suggest these stocks are expensive, the investment thesis centers on news flow, government announcements, technology company commitments, and the eventual conversion of memoranda of understanding and letters of intent into actual capital deployment and project progress.

The Price-Insensitive Customer Paradigm

A fundamental shift is occurring in the nuclear power sector: for the first time, the industry has end customers who are price-insensitive and prepared to enter long-term commitments. Technology companies like Meta have signed power purchase agreements with utilities such as Constellation for 20-year terms at $20-30 per megawatt-hour pricing that utilities haven't secured from customers in decades. This pattern is replicating across North America, Europe, and emerging in Asia, though not exclusively for nuclear generation.

However, a critical disconnect persists in the supply chain. While utilities have secured demand certainty through these power purchase agreements, they have not translated this certainty into their fuel supply chains. Utilities continue operating on outdated procurement models based on the assumption that fuel will be available when needed because it always has been. The expectation is that technology companies having committed to multi-billion dollar electricity agreements will eventually demand fuel supply assurance from utilities or bypass them entirely to secure uranium, conversion, and enrichment supplies directly.

Technology companies already employ hedging strategies for lithium and other battery materials for electric vehicles and energy storage systems. Their due diligence processes for nuclear power purchase agreements likely included meetings with fuel procurement teams to verify supply security. The risk exists that these sophisticated buyers, recognising potential fuel supply vulnerabilities, may independently secure 20-year uranium supply commitments and arrange conversion and enrichment contracts, then present completed fuel packages to utilities.

Production Execution Challenges Across the Sector

The uranium sector faces a significant credibility challenge: nearly every brownfield restart has encountered operational difficulties, and all greenfield projects characterise their development as price-dependent. Companies that previously projected confidence have refocused internally on operational execution rather than growth initiatives.

This pattern of execution challenges doesn't appear to concern utilities as it should, though it does impact investor sentiment. However, recent capital raises totalling billions of dollars in North American uranium companies suggest some investor segments remain undeterred. When contextualised against global resource investment, these capital inflows represent a small fraction of funds deployed in other commodity sectors - uranium's global market capitalization remains hundreds of times smaller than other energy and commodity markets.

The supply response includes concerning dynamics. Recent spot market activity illustrates this problem: when spot prices approached $83 per pound due to apparent supply constraints, substantial volumes suddenly appeared 200,000, 350,000, and 450,000 pounds, representing developers with inventory capitalising on higher prices rather than authentic new supply. These opportunistic sales, while generating positive quarterly cash flow reports for individual companies, signal to utilities that sufficient uranium remains available, undermining price discovery and supply urgency.

Strategic Implications of Consolidation Activity

M&A activity continues in the sector, with ISO Energy's acquisition of Toro Energy representing a consolidation within an existing stable of related projects. The transaction reflects growing speculation that Western Australia might include uranium in green mineral classifications without explicitly naming it, allowing project advancement. The Toro assets, previously undervalued and under-promoted within their corporate structure, benefit from integration into a larger capitalization vehicle.

However, M&A carries significant timeline implications for supply delivery. When different management teams with different geological interpretations and project approaches consolidate assets, the acquiring team typically cannot trust the target's studies, plans, and geological models, particularly for projects where the original team failed to advance them successfully. This necessitates comprehensive re-evaluation, effectively resetting project timelines. This dynamic applies particularly to speculation around potential acquisition of NexGen Energy: any major acquiring that asset would likely restart technical reviews rather than accept existing development plans, pushing the previously projected 2029-2030 production timeline significantly later.

The motivation behind M&A has evolved problematically. Growing company scale to achieve ETF index weightings, rather than advancing actual production, has become a tired strategy among experienced investors. Management teams skilled at market positioning through acquisitions don't necessarily intend to operate mines - they excel at market mechanics and creating scale narratives for eventual larger consolidation. This creates shareholder value in the current market environment but doesn't address the fundamental supply deficit utilities will eventually face.

Active Drilling as the Primary Investment Filter

For exploration-stage investments, Keller emphasises active drilling programs over paper exercises. Companies advancing outdated studies or conducting minimal fieldwork to maintain tenement compliance hold no appeal. The preference is for explorers with drill-ready targets and substantial, properly funded drilling campaigns - ideally raising double their initial capital plans to execute comprehensive programs. The era of lifestyle companies that periodically resurface with minimal activity appears less sustainable, though such entities persist in understanding how to navigate market cycles.

The challenge for retail investors in this environment is significant. Nuclear innovation opportunities, despite offering substantial potential returns for those willing to accept extreme volatility and conviction-based rather than valuation-based investing, present difficulties for individual investors in terms of access, analysis capability, and risk management. The universe of listed opportunities remains limited, though several SPACs are bringing additional nuclear technologies to public markets, expanding but also fragmenting the investment landscape.

Three Unfunded Catalysts Supporting Higher Prices

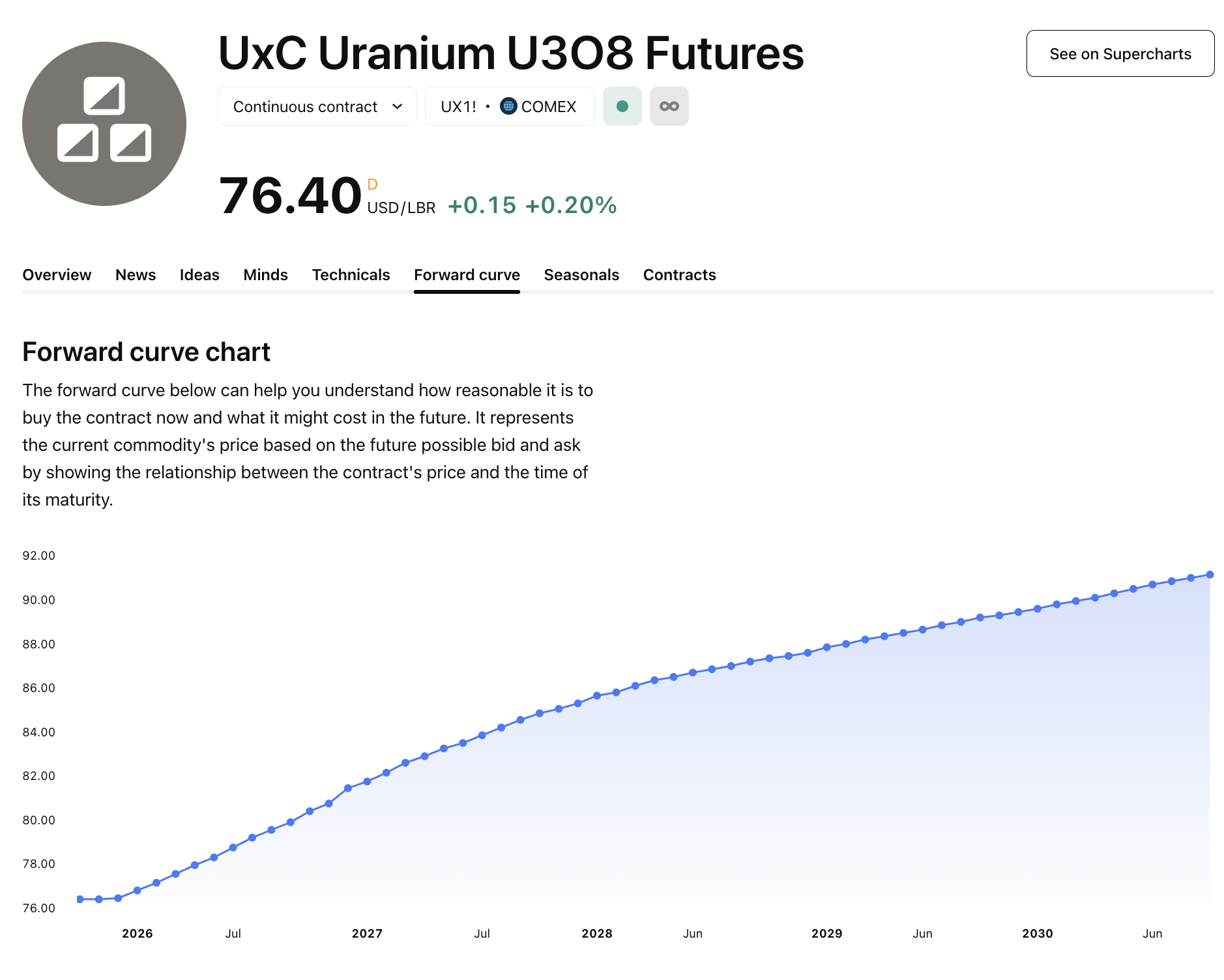

Keller draws parallels to September 2023, when the market began a significant rally culminating in $106 uranium prices. That move saw the uranium ETF gain approximately 20% by November-December 2023 before doubling again subsequently. Current price levels around $80 per pound have been achieved without three critical catalysts materialising: utilities have not demonstrated necessary urgency in uranium procurement despite activity in conversion and enrichment; the US government has not committed the full scope of fuel cycle funding previously announced, with uncertainty around uranium reserve reactivation; and technology companies' agreements remain largely unfunded beyond initial announcements. Forward curve pricing indicates December 2030 uranium at $96 per pound, suggesting market expectations for continued price appreciation.

The current price levels reflect promises and positioning rather than actual capital deployment or supply commitments. Term price indicators - where only 10-15% of actual uranium transactions occur provide limited visibility because utilities have learned that maintaining low term prices and avoiding aggressive contracting prevents market panic and supply competition. Recent activity around the World Nuclear Association conference showed some shift in this dynamic. However, inventory sales from developers and other market window-dressing activities cannot continue indefinitely without reaching a breaking point where supply constraints become undeniable.

Long-Term Electricity Demand Fundamentals

The uranium and nuclear investment landscape presents a complex picture where strong fundamental thesis components have not yet translated to reliable production growth or supply certainty. Technology company involvement represents a genuinely new dynamic, price-insensitive buyers with long-term electricity requirements create demand characteristics the nuclear fuel cycle has never previously experienced. However, this demand certainty exists in parallel with persistent execution challenges across nearly all production and development projects.

The long-term electricity demand driving nuclear interest spans 5-30 year horizons and continues growing. Western nations face challenges meeting this demand through gas and coal alone, particularly if carbon considerations remain relevant to electricity generation policy. Nuclear must form part of the longer-term equation. Technology companies may view nuclear construction challenges consistently over-budget and over-schedule historically as engineering problems their capital and innovation capabilities can solve, similar to SpaceX's rocket recovery achievements or autonomous vehicle development.

The risk remains that if uranium mining companies cannot demonstrate reliable supply capability, either external capital and government intervention will forcefully solve the problem, or established energy companies like ExxonMobil may be directed to take over nuclear fuel supply responsibilities from traditional uranium sector participants who entered the industry decades ago.

TL;DR:

Guy Keller's nuclear fund has shifted ~50% into nuclear innovation plays, capturing tech company-driven billions flowing into advanced reactor technologies while managing extreme volatility. Tech giants signing long-term PPAs with utilities haven't secured corresponding fuel supplies creating potential for direct procurement bypassing traditional buyers. Despite strong thesis fundamentals and forward curves indicating $96/lb uranium by 2030, the sector hasn't yet triggered three key catalysts: utility fuel buying urgency, full US government funding deployment, or tech company capital moving beyond MOUs. Every brownfield restart has stumbled and greenfields remain price-dependent, creating credibility gaps that paradoxically might attract outside capital to solve supply constraints by force.

FAQ's (AI Generated)

Nuclear innovation investments capture billions flowing from tech companies into advanced reactor technologies, removing direct uranium commodity risk while accessing higher-growth opportunities despite extreme volatility requiring significantly more active management.

Tech companies are price-insensitive, willing to commit to 20-year power agreements at premium pricing utilities haven't seen in decades, creating unprecedented demand certainty though this hasn't translated to fuel supply security.

Acquiring management teams typically cannot trust target company studies and geological interpretations, especially for stalled projects, necessitating comprehensive re-evaluation that resets development timelines regardless of previous projections.

Despite signing multi-billion dollar electricity agreements with tech companies, utilities continue operating on outdated "just-in-time" procurement models assuming fuel availability, with minimal urgency in contracting compared to their conversion and enrichment activity.

Current $80 pricing reflects unfunded promises rather than actual capital deployment. Three major catalysts haven't triggered: utility procurement urgency, full US government funding deployment, and tech company capital moving beyond MOUs to contracted commitments.

Analyst's Notes

Subscribe to Our Channel

Stay Informed