China's Rare Earth Grip Forces Global Supply Chain Reset

China's rare earth grip forces Western supply chain reset. Demand to triple by 2035 with 30% shortfall risk. Defense sectors pivot to allied producers.

- China’s near-monopoly on rare earth element (REE) mining and refining is exerting unprecedented influence over Western defense and clean energy sectors.

- Recent export controls on gallium, germanium, and heavy rare earths threaten to delay production, inflate costs, and undermine strategic autonomy.

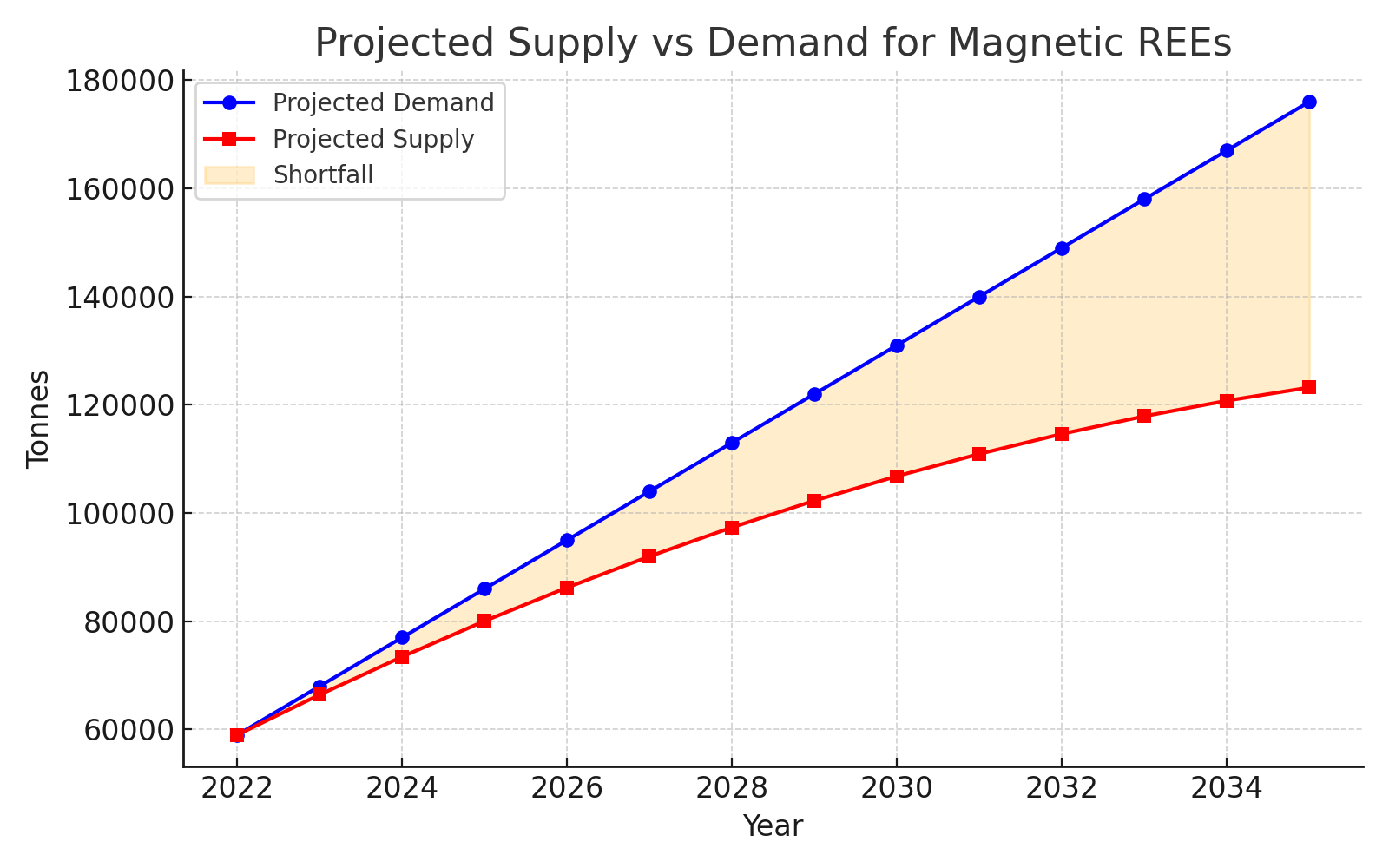

- Demand for magnetic REEs is forecast to triple by 2035, with supply projected to fall short by up to 30% without new, non-Chinese capacity.

- Western governments and corporations are accelerating investment in domestic and allied REE supply chains, including recycling technologies and alternative mineral sources.

- Case studies from Energy Fuels, Pensana, Ionic Rare Earths, Ucore, and Namibia Critical Metals show how companies are positioning to benefit from supply realignment.

China's Consolidated Control of Rare Earth Supply Chains

Market Share, Refining Dominance, and Technology Lock-In

China's strategic control over rare earth supply chains extends well beyond raw material extraction. While maintaining over 60% of global mining capacity, China's true advantage lies in its 80% share of rare earth refining operations and proprietary separation technologies that have been systematically protected through export restrictions and technology transfer limitations.

The processing bottleneck represents the most significant constraint facing Western supply chain development. Unlike mining operations that can be established in multiple jurisdictions, rare earth separation requires specialized metallurgical expertise, environmental management systems, and substantial capital investment that China has concentrated within its borders over three decades.

Recent regulatory changes have reinforced these advantages through technology export bans that restrict the transfer of separation equipment and retain key technical personnel within Chinese operations. These measures effectively prevent technology leakage while maintaining China's processing monopoly, creating structural dependencies that extend throughout Western manufacturing sectors.

Energy Fuels has identified this processing gap as a strategic opportunity, leveraging its unique domestic processing capability. Chief Executive Officer Mark Chalmers notes:

"The White Mesa Mill is the only United States facility able to process monazite and produce high-purity rare earth oxides."

Escalating Export Controls and Their Strategic Purpose

China's export control timeline reveals an escalating strategy that targets specific materials critical to Western defense and technology sectors. Beginning with gallium and germanium restrictions in 2023, China has systematically expanded controls to include antimony, specific rare earth oxides, and dual-use technologies essential for military applications.

The strategic purpose extends beyond immediate supply disruption. By controlling access to materials required for advanced manufacturing while maintaining domestic supply chain integrity, China can influence Western production schedules, increase manufacturing costs, and potentially delay critical defense programs.

Recent examples demonstrate the immediate impact of these controls. United States antimony shipments experienced significant delays following export restrictions, while samarium prices increased by approximately 60 times normal levels due to supply constraints. These disruptions have forced Western manufacturers to reassess supply chain resilience and accelerate alternative sourcing strategies.

Defense sector exposure has prompted the most immediate responses from Western governments. The Department of Defense has established specific timelines for eliminating Chinese-origin materials from magnet supply chains by 2027, while providing targeted funding to domestic rare earth processors including Ucore's Strategic Metals Complex in Louisiana.

Strategic Vulnerabilities in Western Defense & Clean Energy

Defense Manufacturing Exposure

Western defense manufacturing sectors face unprecedented exposure to Chinese rare earth supply disruptions, with over 80,000 United States defense components now dependent on materials subject to export controls. Critical applications include jet fighter engines, missile guidance systems, night-vision equipment, and defense satellite technologies that require specific rare earth elements with limited alternative sourcing options.

The vulnerability extends beyond individual components to entire weapons systems. Modern defense platforms integrate rare earth permanent magnets throughout propulsion, guidance, and communication systems, creating single points of failure that cannot be easily substituted with alternative materials or technologies.

Ucore's Strategic Metals Complex project represents a direct response to these vulnerabilities, with Department of Defense funding supporting the development of domestic separation capacity specifically designed to serve defense sector requirements. Chief Executive Officer Pat Ryan emphasizes the strategic imperative:

"Our plan includes developing a vertically integrated North American rare earth element supply chain, disrupting the People's Republic of China's control of this supply chain."

Clean Energy Transition & Rare Earth Element Demand Growth

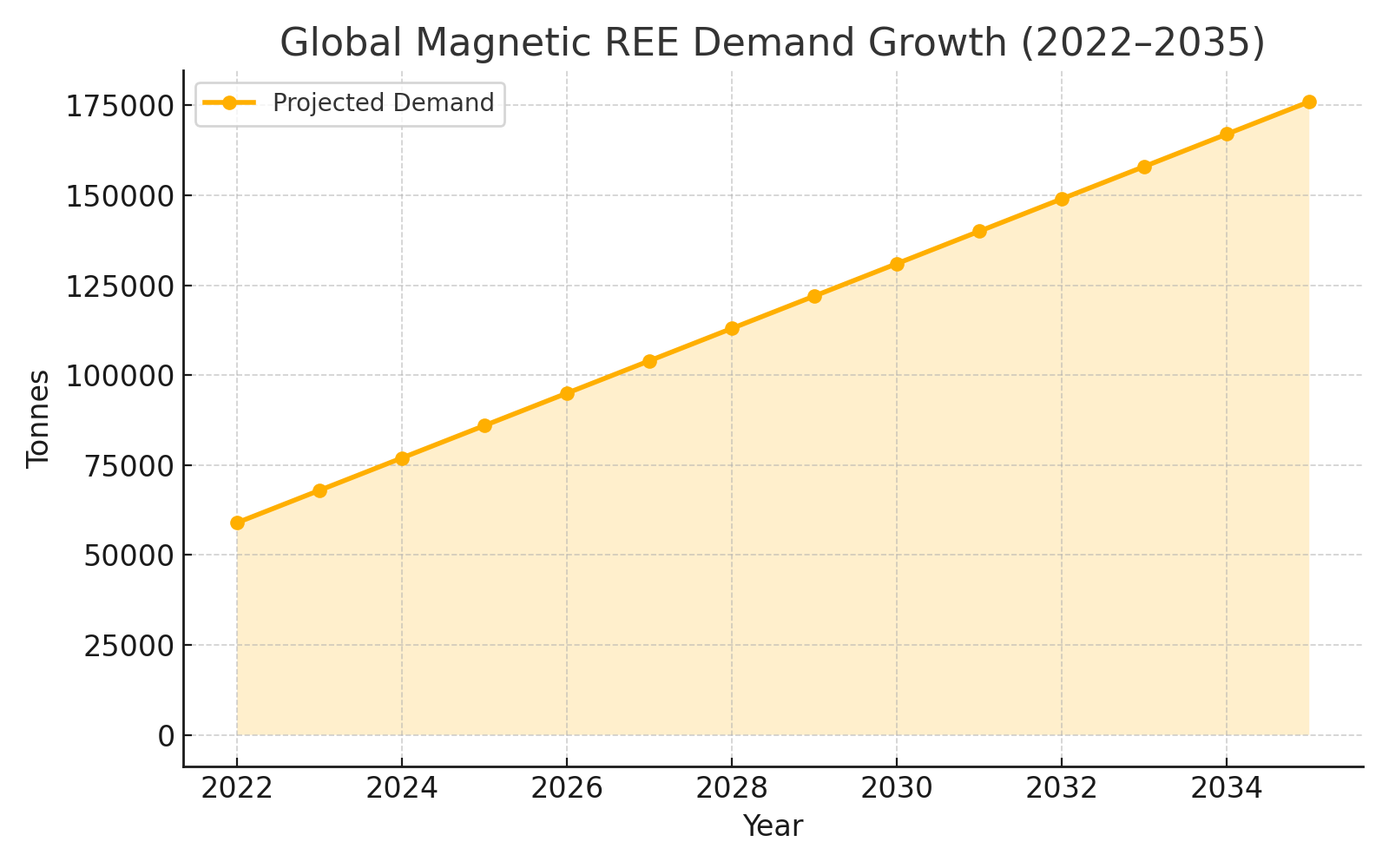

Clean energy sector demand for magnetic rare earths has emerged as the primary driver of supply-demand imbalances, with electric vehicle drivetrains and wind turbine nacelles requiring substantial quantities of neodymium, praseodymium, dysprosium, and terbium oxides. Current demand projections indicate growth from approximately 59,000 tonnes in 2022 to 176,000 tonnes by 2035, representing a nearly threefold increase driven primarily by transportation electrification.

Wind energy deployment creates additional demand pressures, with offshore wind turbines requiring significantly larger permanent magnets than onshore installations. European and United States offshore wind development programs have established aggressive capacity targets that will require substantial rare earth supply additions beyond current Chinese production capabilities.

Pensana Plc's Longonjo project exemplifies strategic positioning to serve clean energy demand growth, with planned neodymium-praseodymium production capacity of 20,000 tonnes annually by late 2026, expanding to 40,000 tonnes by 2027. Chief Executive Officer Tim George highlights the market opportunity:

"We are constructing one of the world's largest magnet metal rare earth mines to meet rapidly growing demand."

Supply-Demand Mismatch & Market Forecasts

Structural Shortfalls

McKinsey projections indicate potential shortfalls of up to 30% in magnetic rare earth supply by 2035 without substantial Chinese capacity expansion or significant non-Chinese production additions. These forecasts assume continued Chinese market participation and do not account for potential export restrictions that could exacerbate supply constraints.

Heavy rare earth elements face more severe supply limitations, with dysprosium and terbium production concentrated in select Chinese operations that maintain technical advantages in ion-adsorption clay processing. Western heavy rare earth development remains limited to specific projects including Energy Fuels' monazite processing capability and Namibia Critical Metals' xenotime mineralization.

Energy Fuels has developed capabilities to address heavy rare earth supply gaps through monazite processing at the White Mesa Mill, leveraging existing uranium processing infrastructure to produce dysprosium and terbium oxides for defense applications. The company's strategy involves importing high-grade monazite concentrates from heavy mineral sand operations globally, providing feedstock flexibility while maintaining domestic processing control.

Price & Volatility Implications

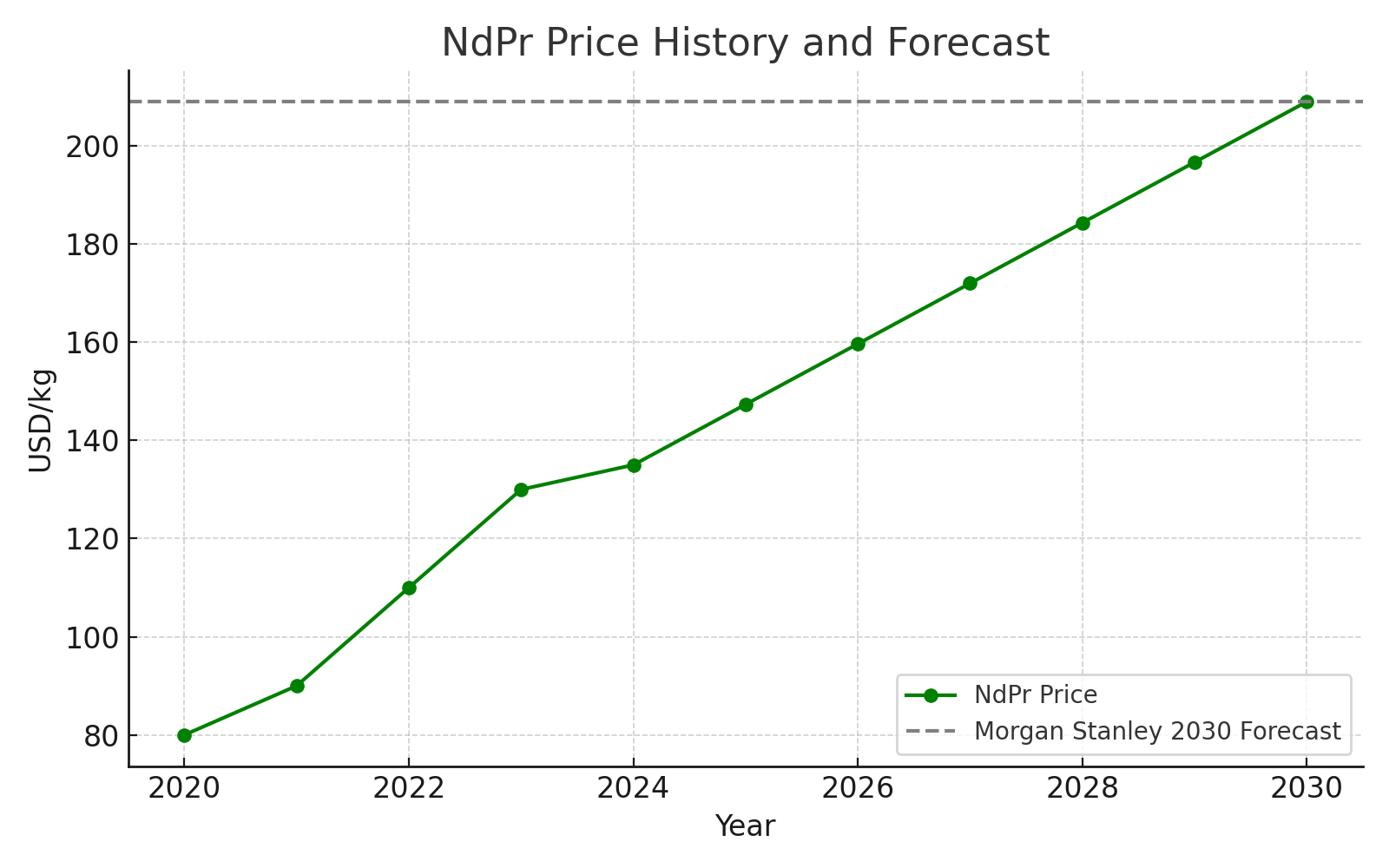

Rare earth oxide price volatility has increased substantially following Chinese export control implementation, creating challenges for project development financing while supporting higher long-term price forecasts that improve project economics. Morgan Stanley recently upgraded long-term neodymium-praseodymium prices from 135 dollars per kilogram to 209 dollars per kilogram, reflecting supply constraint expectations.

Namibia Critical Metals' Lofdal project economics demonstrate heavy rare earth price sensitivity, with the preliminary economic assessment indicating a net present value of 632.7 million dollars pre-tax and internal rate of return of 34% based on conservative price assumptions. Updated price forecasts incorporating supply constraint premiums could significantly improve project returns.

The company's focus on heavy rare earth production positions it to benefit from price differentials that typically favor dysprosium and terbium over light rare earth elements. Planned production of approximately 117 tonnes of dysprosium and 17 tonnes of terbium annually represents approximately 5% of global demand for these critical materials.

Western Supply Chain Responses & Capital Flows

Government-Led Interventions

Western governments have implemented unprecedented funding programs to support domestic rare earth supply chain development, with the United States Department of Defense providing over 400 million dollars in direct investment to rare earth processors including MP Materials and targeted grants to separation technology developers.

Department of Defense funding strategies prioritize projects with near-term production capability and alignment with defense sector requirements. Ucore has received 22.4 million dollars in Department of Defense funding for Strategic Metals Complex development, supporting construction of production-ready separation equipment and related infrastructure in Alexandria, Louisiana.

Canadian government support includes strategic partnerships with rare earth developers and technology companies, while European Union initiatives focus on processing capability development and recycling technology advancement. Japan has established bilateral partnerships including the Japan Organization for Metals and Energy Security agreement with Namibia Critical Metals to develop heavy rare earth production capacity.

Corporate Strategic Realignments

Corporate responses to supply chain vulnerabilities have included vertical integration strategies, strategic offtake agreements, and technology development partnerships that reduce Chinese dependencies while securing market access for Western-aligned producers.

Energy Fuels' acquisition of Base Resources reflects strategic positioning to secure heavy mineral sand feedstock access while maintaining processing flexibility through the White Mesa Mill. President and Chief Executive Officer Mark Chalmers explains the integrated approach:

"We believe importing high-grade monazite sand byproducts from heavy mineral sands mines globally is a lower cost way to produce separated rare earth oxides versus primary rare earth production."

Pensana's financing and construction progress demonstrates successful project execution in challenging jurisdictions, with the Longonjo development maintaining aggressive timelines despite Angola's complex regulatory environment. The company's approach includes strategic partnerships with Chinese engineering firms while maintaining Western financing and offtake arrangements.

Recycling as a Structural Mitigation Path

Shifting Scrap Pools & Technology Readiness

Rare earth recycling represents a strategic mitigation path for Western supply chain development, with current scrap pools dominated by consumer electronic devices transitioning toward larger components from electric vehicles and wind turbines by 2050. This transition will provide higher-grade feedstock for separation technologies while reducing primary mining requirements.

Current recycling contributions remain limited due to technical challenges in rare earth separation from complex magnet assemblies and economic constraints that favor primary production. However, advancing separation technologies and increasing rare earth prices are improving recycling economics while supporting technology development investments.

Ionic Rare Earths has developed proprietary separation technology through partnerships with Queen's University Belfast, achieving 99.9% rare earth oxide separation efficiency from permanent magnet feedstock. The company's leadership emphasizes the technology's strategic value, Managing Director Tim Harrison states:

"The technology and the skill sets we've developed do have a very unique IP on magnet recycling producing the separated oxides."

European Union recycling targets require 15% of rare earth consumption from recycled sources by 2030, creating regulatory drivers for technology deployment and feedstock development. These targets align with rare earth price forecasts that support recycling economics while providing strategic supply chain diversification.

Project Readiness & Execution Risk

Permitting, Capital Expenditure Discipline, and Timeline Certainty

Project execution risk assessment requires evaluation of permitting timelines, capital expenditure requirements, and construction scheduling that determines production ramp timing relative to market demand growth. Western rare earth development faces jurisdictional advantages in permitting transparency while confronting higher capital costs and more stringent environmental requirements compared to Chinese operations.

Pensana's construction schedule demonstrates aggressive timeline execution with planned commercial production by late 2026 despite complex jurisdictional requirements in Angola. The company's capital expenditure estimate of 217 million dollars for Stage 1 development reflects disciplined project scoping while maintaining production capacity targets of 20,000 tonnes of mixed rare earth carbonate annually.

Energy Fuels maintains multiple final investment decision opportunities through the Toliara project in Madagascar and Donald project expansion, providing strategic flexibility while leveraging existing White Mesa Mill processing infrastructure. The company's approach reduces capital intensity requirements while maintaining production growth optionality.

Namibia Critical Metals' pre-feasibility study delivery scheduled for October 2025 represents a critical derisking milestone for the Lofdal project, with the Japan Organization for Metals and Energy Security partnership providing development funding and technical support. The study will update project economics based on current rare earth price forecasts while incorporating processing technology improvements.

Permitting regimes in the United States, Angola, and Namibia provide varying levels of regulatory certainty, with established frameworks supporting project development while maintaining environmental and social compliance standards. These jurisdictions offer strategic alternatives to Chinese supply chain dependencies while providing long-term operational security.

ESG Differentiators in Critical Mineral Development

Environmental, social, and governance considerations have become increasingly important for rare earth project development, with Western offtakers requiring supply chain transparency and environmental compliance that exceeds typical Chinese production standards. These requirements create competitive advantages for Western-aligned producers while supporting premium pricing for compliant supply.

Namibia's Extractive Industries Transparency Initiative membership provides governance frameworks that support international investment while ensuring community benefit distribution. Energy Fuels' partnerships with Chemours and POSCO demonstrate strategic offtake arrangements that provide financing support while securing market access for compliant rare earth production.

Strategic offtake agreements play essential roles in project financing and execution risk reduction, with long-term contracts providing revenue certainty that supports debt financing while reducing market exposure. These arrangements typically include pricing mechanisms that provide inflation protection while ensuring competitive supply costs for offtakers.

Namibia Critical Metals' thorium offtake memorandum of understanding with Copenhagen Atomics exemplifies innovative approaches to byproduct revenue optimization, with thorium production providing additional cash flow streams that improve project economics while supporting advanced nuclear technology development.

The Investment Thesis for Rare Earth Elements

- Exposure to non-Chinese rare earth producers mitigates concentration risk and captures premium valuations tied to supply chain realignment, especially as trade tensions escalate and resource security becomes a national priority.

- Multi-decade demand growth from EV adoption, wind energy build-out, and defense modernization supports sustained capital deployment, with magnetic REE demand forecast to grow 15–18% annually.

- Producers of dysprosium and terbium benefit from scarcity-driven margins that significantly exceed those of light REEs, supported by supply constraints that are not easily resolved through capacity expansion.

- Projects backed by the US Department of Defense, Japan Organization for Metals and Energy Security, or European Union funding enjoy reduced financing risk, strategic validation, and accelerated development timelines.

- Ownership of proprietary separation and recycling technologies enables downstream margin capture, reduces feedstock dependence, and creates durable competitive advantage across the rare earth supply chain.

China's strategic leverage over rare earth supply chains represents more than temporary market disruption. It reflects fundamental shifts toward multipolar mineral geopolitics where resource access determines technological leadership and strategic autonomy. Western recognition of these dependencies has triggered unprecedented policy responses and capital deployment that will reshape global rare earth markets over the coming decade.

The structural nature of current supply-demand imbalances ensures this realignment will unfold over multiple years, creating sustained opportunities for companies with jurisdictional advantages, proven technologies, and strategic partnerships. Unlike cyclical commodity investments, rare earth development reflects permanent changes in global supply chain architecture that support long-term investment themes.

For investors, the opportunity lies in identifying projects with secure jurisdictional positioning, advanced development readiness, and aligned offtake strategies that reduce execution risk while capturing supply chain realignment value. Companies including Energy Fuels, Pensana, Ionic Rare Earths, Ucore, and Namibia Critical Metals have positioned themselves strategically within this transition, offering exposure to structural market changes that extend well beyond traditional commodity cycles.

The generational nature of rare earth supply chain realignment creates compelling investment opportunities for participants who understand the strategic importance of mineral resource control in an increasingly multipolar world. Success will favor companies that combine technical capability with strategic positioning and government alignment, creating sustainable competitive advantages in critical mineral supply chains that power the modern economy.

Analyst's Notes

Subscribe to Our Channel

Stay Informed