China's Refined Copper Output Drop Tightens Supply & Anchors Investor Focus on Price Stability

China's 4-5% copper output decline tightens global supply as electrification demand surges. Mining equities in Canada and Chile offer strategic exposure.

Macroeconomic Signals & Supply-Driven Market Stress

China's September 2025 production decline represents more than a temporary disruption, it signals a structural tightening in global copper markets. With Chinese smelters responsible for approximately 45% of global refined copper output, a 4–5% monthly contraction removes roughly 500,000 tonnes from annualized supply calculations. This reduction arrives as global inventories sit near multi-year lows, with London Metal Exchange warehouses reporting stock levels 40% below their five-year average.

Dollar weakness compounds the supply narrative. The U.S. Dollar Index has declined 7% since January 2025, while Federal Reserve rate cut expectations have crystallized around an 87% probability for a 25-basis-point reduction in September according to CME FedWatch data. This monetary backdrop reduces the opportunity cost of holding commodities, particularly for non-dollar-denominated buyers who gain purchasing power as the greenback retreats. Historical precedent from 2010–2011 demonstrates how synchronized dollar weakness and Chinese supply constraints can drive copper prices toward $5.00 per pound territory.

The tariff landscape adds another layer of complexity. Current U.S. exemptions for refined copper imports but tariffs on semi-finished products have created arbitrage opportunities while disrupting traditional trade flows. Chinese refined copper exports to Southeast Asia have increased 23% as material gets rerouted to avoid direct U.S. tariff exposure, creating regional premium disparities that range from $50 to $150 per tonne.

Hayden Locke, President and Chief Executive Officer of Marimaca Copper, frames the current environment within a broader context:

"We're seeing a convergence of factors that haven't aligned since the last major copper cycle. The supply response simply cannot match demand growth trajectories when you combine Chinese production constraints with decade-low project pipelines globally."

Systemic Constraints & the Structural Supply Deficit

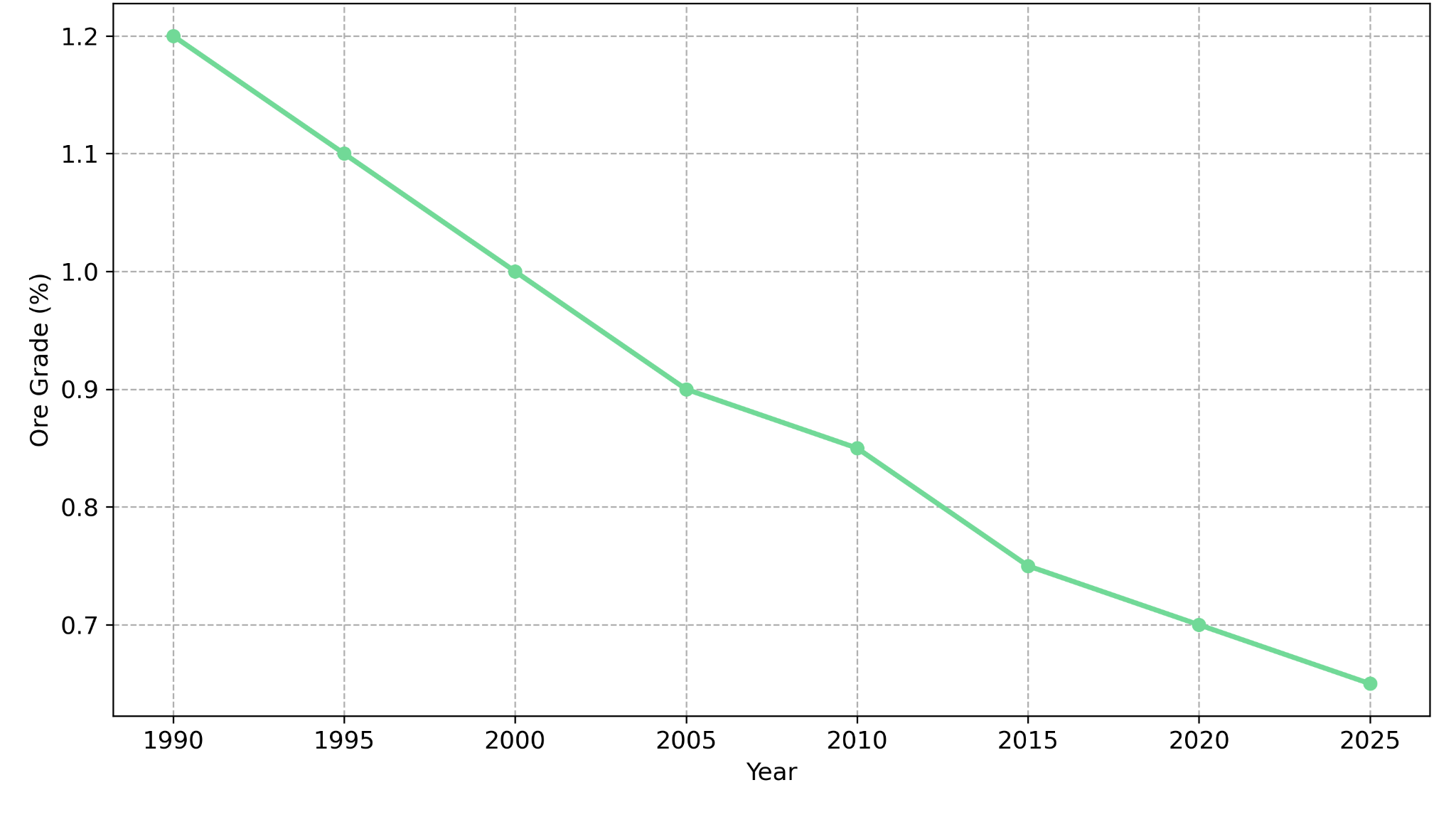

The September production decline in China illuminates deeper structural challenges confronting global copper supply. Average copper ore grades have declined 40% since 1990, forcing miners to process substantially more material to maintain production levels. This grade deterioration translates directly into higher costs, with energy consumption per tonne of copper production increasing 16% over the past decade according to industry data.

New project development faces its own obstacles. The timeline from discovery to production now averages 12–15 years, compared to 7–10 years in the 1990s. Grassroots exploration budgets have contracted 35% from their 2012 peak, while environmental and social governance requirements have lengthened permitting processes across major copper-producing jurisdictions. The global project pipeline remains dominated by complex sulfide deposits requiring capital expenditures exceeding $3 billion and technical expertise that limits the pool of capable developers.

China's shift away from recycling subsidies represents a structural change rather than a cyclical adjustment. Scrap copper has historically provided 20–25% of China's refined copper input, but the economic viability of collection and processing networks depended heavily on government support. Without subsidies, marginal recycling operations have ceased, removing approximately 400,000 tonnes of annual scrap supply from the Chinese system.

Within this constrained environment, companies advancing high-grade, near-surface deposits gain relative advantage. Gladiator Metals' Whitehorse Copper Project in Yukon exemplifies this opportunity. The project's Cowley Park prospect has delivered exceptional drill results including 79 meters at 1.37% copper with significant zones grading above 3%. These grades sit well above the global average of 0.5% copper, potentially offsetting the industry-wide grade decline challenge.

Jason Bontempo, Chief Executive Officer and Director of Gladiator Metals, emphasizes the project's strategic positioning:

"When you're dealing with grades that are two to three times the industry average from near surface, the economics fundamentally change. We're targeting over 100 million tonnes at above 1% copper, which would represent one of the few high-grade development opportunities globally."

Policy Volatility & Currency Effects on Pricing

Copper pricing increasingly reflects monetary policy dynamics alongside traditional supply-demand fundamentals. The Federal Reserve's anticipated September rate cut marks a potential inflection point, with futures markets pricing in 100 basis points of total easing through 2026. Lower yields reduce the opportunity cost of holding commodities while weakening the dollar enhances copper affordability for international buyers, particularly in Asia where 75% of global copper consumption occurs.

Currency volatility has amplified copper price swings by 30% compared to historical norms. The correlation between copper prices and the trade-weighted dollar has strengthened to -0.75, the highest negative correlation in a decade. This relationship suggests that each 1% decline in the dollar index translates to approximately $0.08 per pound increase in copper prices, all else being equal.

Tariff structures have created unprecedented distortions in copper trade flows and regional pricing. The bifurcated approach, exempting refined copper while taxing semi-finished products, has generated unintended consequences. Domestic U.S. copper premiums have risen to $200 per tonne above global benchmarks, while fabricators face input cost pressures that squeeze margins. These distortions create opportunities for vertically integrated producers who can capture value across the supply chain.

Companies with robust project economics demonstrate resilience to policy-driven volatility. Marimaca Copper's definitive feasibility study reveals strong returns even in stressed scenarios, with all-in sustaining costs projected at $2.09–2.29 per pound and a post-tax internal rate of return of 31% at $4.20 per pound copper. At current spot prices near $4.50, the net present value exceeds $1 billion.

The company's Chief Executive Officer Hayden Locke addresses financing readiness amid the volatile backdrop:

"Our capital structure planning assumes continued currency and policy volatility. We've structured our approach to maintain flexibility while protecting against downside scenarios, which becomes critical when you're advancing a project toward construction in this environment."

Electrification, Grid Expansion & Demand Anchors

Structural copper demand from electrification and infrastructure development provides a compelling counterweight to near-term supply constraints. Electric vehicles require 25–50 kilograms of copper per unit compared to 8–12 kilograms in conventional vehicles. With global EV production projected to exceed 30 million units annually by 2030, this transition alone could add 1.5 million tonnes to annual copper demand. Solar installations consume approximately 5.5 tonnes of copper per megawatt of capacity, and the International Energy Agency projects 5,400 gigawatts of new solar capacity through 2030.

Grid infrastructure requirements amplify these demand drivers. The transition to renewable energy necessitates substantial transmission and distribution upgrades, with copper intensity in grid applications averaging 3–5 tonnes per megawatt. China's 14th Five-Year Plan allocates $440 billion for grid modernization, while the U.S. Inflation Reduction Act designates $65 billion for transmission infrastructure. India's ambitious renewable targets require 500 gigawatts of capacity additions by 2030, implying copper consumption exceeding 2 million tonnes for this program alone.

Critical mineral designations have elevated copper's strategic importance beyond pure economic considerations. The European Union, United States, and Japan have all classified copper as essential for energy security, unlocking preferential financing and fast-track permitting for qualifying projects. This policy support reduces development risk for companies operating in allied jurisdictions while potentially accelerating project timelines by 2–3 years.

Strategic Project Positioning

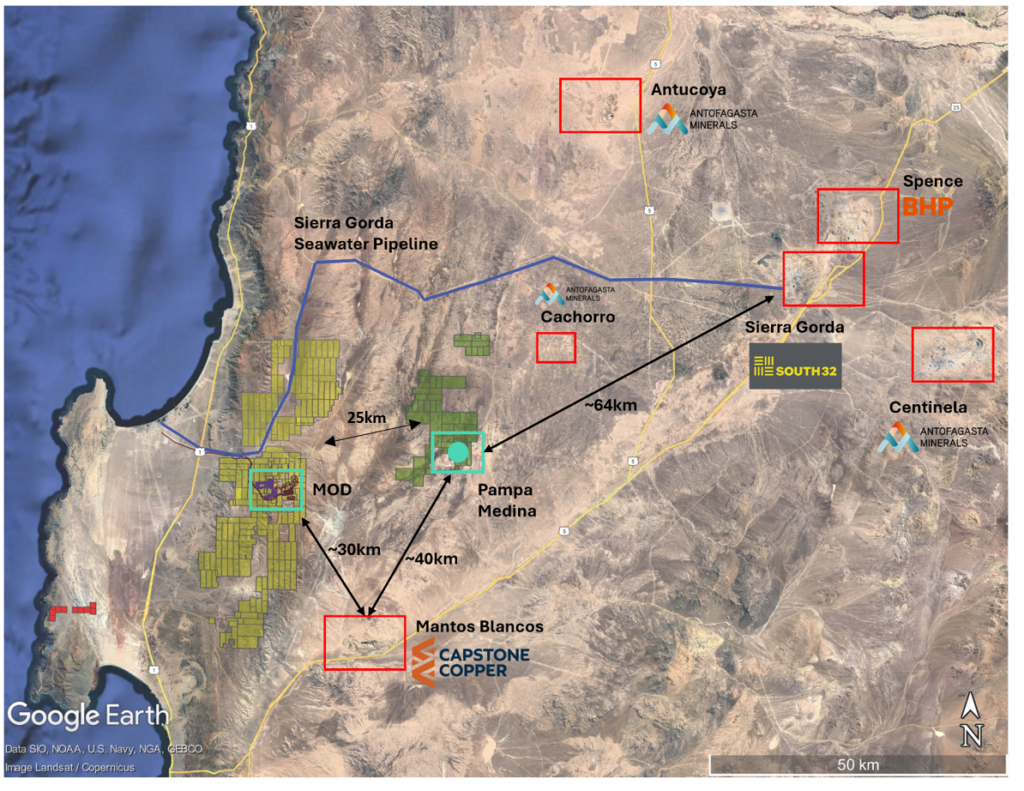

Within this demand framework, companies controlling projects with favorable metallurgy and infrastructure access position themselves advantageously. Fitzroy Minerals' portfolio in Chile exemplifies this approach through its Buen Retiro and Caballos projects. Buen Retiro's near-surface oxide mineralization suits heap leach processing, offering capital-efficient development potential. The Caballos project adds strategic value through molybdenum and rhenium by-products, both designated as critical minerals.

Merlin Marr-Johnson, President and Chief Executive Officer of Fitzroy Minerals, highlights the exploration leverage to accelerating demand:

"We're in discovery mode at both Buen Retiro and Caballos. The combination of copper with critical mineral by-products like molybdenum and rhenium provides multiple pathways to value creation as these markets tighten simultaneously."

Capital Markets & Investor Positioning in a Supply-Squeezed Market

Capital flows into copper-exposed assets have accelerated markedly in 2025, with copper-focused exchange-traded funds attracting $2.3 billion in net inflows year-to-date. This represents a 45% increase over the full-year 2024 total, signaling growing institutional recognition of the supply-demand imbalance. Futures positioning data reveals that managed money accounts hold net long positions of 68,000 contracts, approaching the multi-year highs seen during the 2021 commodity supercycle.

Mining equity valuations reflect this renewed interest but remain below historical peaks. Senior copper producers trade at enterprise value to resource ratios of $0.12–0.18 per pound, compared to $0.25–0.35 during previous cycle highs. This valuation gap suggests potential upside as the supply crunch intensifies. Development-stage companies with defined resources trade at even steeper discounts, typically $0.03–0.08 per pound, offering asymmetric return potential for projects that advance toward production.

Institutional capital shows clear preferences for specific project attributes. Tier 1 jurisdictions command valuation premiums of 30–50% over emerging market peers. Projects with all-in sustaining costs below $2.50 per pound attract disproportionate interest, as these assets generate robust margins even in downside price scenarios. Environmental, social, and governance credentials increasingly influence capital allocation, with companies demonstrating strong community relations and environmental stewardship accessing lower-cost financing.

Geographic Distribution & Strategic Positioning

The geographic distribution of new copper investments reveals strategic positioning by institutional investors. Canada and Chile continue to dominate capital flows, collectively attracting 65% of global copper exploration spending. Gladiator Metals benefits from this trend through its Yukon location, combining Canada's regulatory stability with proximity to infrastructure and skilled labor. Similarly, Marimaca Copper and Fitzroy Minerals leverage Chile's established mining ecosystem and proximity to Asian markets, where 75% of global copper consumption occurs.

Private equity and strategic investors have emerged as increasingly important sources of development capital. Mitsubishi Corporation's C$20 million investment in Marimaca Copper and Assore's C$68 million stake acquisition exemplify how strategic players position for long-term copper exposure while providing junior companies with capital and technical expertise. These partnerships often include offtake agreements that de-risk project financing while ensuring supply chain security for end users.

The Investment Thesis for Copper

- China's 4–5% September output drop highlights fragility in refined supply chains, removing critical tonnage when inventories sit at multi-year lows while maintenance schedules and environmental regulations constrain near-term production recovery potential.

- Declining ore grades averaging 40% deterioration since 1990 combine with underfunded exploration budgets and 12–15 year development timelines to create persistent supply constraints that cannot respond quickly to price signals.

- Dollar weakness amplified by 87% probability of Federal Reserve rate cuts enhances copper affordability for international buyers while tariff structures reshape trade flows, creating regional pricing disparities and arbitrage opportunities.

- Electrification drives exponential consumption growth through electric vehicles requiring 25–50 kilograms of copper per unit, solar installations consuming 5.5 tonnes per megawatt, and grid modernization programs totaling $500 billion globally requiring massive copper inputs.

- Companies advancing low-capital intensity projects in Tier 1 jurisdictions provide differentiated exposure to the copper thesis, with Gladiator Metals offering high-grade exploration upside in Yukon, Marimaca Copper delivering near-term production potential in Chile, and Fitzroy Minerals providing discovery leverage with critical mineral by-products.

Copper at a Critical Inflection Point

China's September production decline represents a crystallizing moment for copper markets, where temporary disruptions reveal deeper structural vulnerabilities. The 4–5% output reduction removes approximately 500,000 tonnes from annualized global supply precisely when inventories hover near critical levels and new project development remains constrained by decade-long timelines and capital requirements exceeding $3 billion for major developments.

Price stabilization around $4.50 per pound reflects market recognition of these supply realities. This level sits 50% above the 2020 lows yet remains 10% below the 2022 peaks, suggesting a sustainable equilibrium that balances near-term volatility with long-term structural deficits. The convergence of Chinese production constraints, dollar weakness, and Federal Reserve easing creates conditions reminiscent of previous copper cycles that delivered multi-year price appreciation.

Investors navigating this inflection point face a dual opportunity set. Short-term volatility driven by policy shifts and trade flow disruptions creates tactical trading opportunities for those able to parse regional arbitrage and currency effects. Longer-term positioning through companies advancing high-quality projects in stable jurisdictions offers exposure to the structural thesis, where electrification, infrastructure investment, and supply constraints combine to support a multi-year expansion in copper valuations. The companies best positioned to capture this value demonstrate clear advantages: proven high-grade resources, favorable development economics, strategic by-product credits, and management teams with demonstrated execution capability in complex market environments.

Analyst's Notes

Subscribe to Our Channel

Stay Informed