Complex Landscape Battery Metals Market in 2025: Price Volatility & Economic Uncertainties

The battery metals market in 2025 presents a complex yet promising landscape for investors. While price volatility and economic uncertainties pose challenges, strategic investments and diversification efforts by major corporations underscore the sector's potential.

- The global demand for battery metals like lithium, nickel, and cobalt is surging due to the shift towards renewable energy and electric vehicles.

- Price volatility in the battery metals market has been influenced by oversupply, fluctuating demand, and China's economic slowdown.

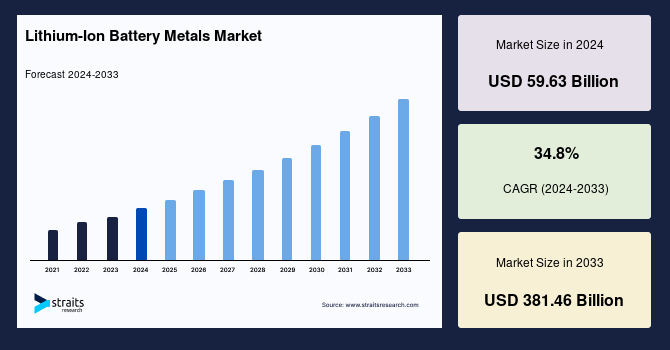

- The lithium-ion battery metals market is projected to reach USD 381.46 billion by 2033, driven by the growing demand for EVs, consumer electronics, and energy storage systems.

- Major corporations, such as Saudi Aramco, are diversifying their portfolios by investing in lithium production to reduce reliance on oil and establish a presence in the mining sector.

- Investors considering the battery metals market should evaluate factors like supply and demand dynamics, technological advancements, regulatory environment, and geopolitical considerations.

The global shift towards renewable energy and electric vehicles (EVs) has intensified the demand for battery metals such as lithium, nickel, and cobalt. These materials are essential components in battery technology, making them critical to the clean energy transition. Understanding the current market dynamics and future prospects of these metals is crucial for investors aiming to capitalize on this sector.

Market Dynamics and Price Volatility

In recent years, the battery metals market has experienced significant price volatility. For instance, lithium prices saw a substantial decline due to oversupply and fluctuating demand. However, analysts anticipate a stabilization by 2025, driven by mine closures and robust EV sales in China, which are expected to absorb the excess supply.[1]

The economic landscape, particularly in China, plays a pivotal role in shaping the battery metals market. China's economic slowdown has led to decreased demand for mineral-intensive goods, contributing to price volatility. Additionally, China's market strategies, including increased production despite low demand, have resulted in commodity surpluses, further affecting global prices.

The global lithium-ion battery metals market, valued at USD 59.63 billion in 2024, is projected to reach USD 381.46 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 22.9% during the forecast period.[4]

This substantial growth is primarily driven by the escalating demand for electric vehicles (EVs), advancements in consumer electronics, and the expansion of energy storage systems. The automotive sector, in particular, has experienced a significant surge in lithium-ion battery demand, with EV sales reaching unprecedented levels. In 2023, vehicles accounted for 80% of lithium-ion battery demand, a figure expected to rise as EV adoption accelerates worldwide.[4]

Similarly, nickel production has surged, particularly in Indonesia, leading to a global surplus and subsequent price declines. This oversupply has impacted the profitability of major mining companies and introduced uncertainty into the nickel market.

Global Economic Influences

Strategic Investments and Diversification

Recognizing the strategic importance of battery metals, major corporations are diversifying their portfolios. Notably, Saudi Aramco, the world’s largest oil company, has announced plans to expand its investments in lithium production aiming to commence commercial production by 2027.[3] This initiative aligns with Saudi Arabia's broader strategy to reduce its economic reliance on oil, build supply chain for metal vital for batteries to power electric cars, and establish itself as a significant player in the mining sector.

Rome Resources

Rome Resources' tin-copper project in the DRC shows promise with 30-40m wide tin intercepts in initial drilling. Applying the proven San Rafael geological model, Rome plans deeper drilling to further delineate the resource. Kalayi prospect drilling is nearly complete with a maiden resource expected in Q1 or early Q2 2025.

CEO Paul Barrett noted, "These are relatively wide tin intercepts. The key focus obviously is the tin. If we can close off Kalayi drilling and this phase of Mont Agoma and come up with a resource, we'll still have a lot of money in the bank to continue the next phase."

Well-funded after a recent financing, Rome is now pursuing larger partners rather than further dilution. Management sees positive long-term fundamentals for the tin market, which faces projected supply deficits as demand grows for clean energy applications. Rome's Congo tin project provides exposure and a path to production in an undersupplied critical metal.

MTM Critical Metals

MTM Critical Metals' patented Flash Joule Heating (FJH) technology enables more selective, efficient, and scalable extraction of lithium, rare earths, gallium, indium and germanium. Finalizing design of a 1 ton/day pilot plant, MTM aims for commercial production and cash flow in 2025 via a revenue model combining licensing, processing fees, and metal profit sharing.

President Steve Ragiel highlighted, "Even at one ton per day, the gallium opportunity is commercial. The total consumption of gallium in the US is about 400 to 500 tons per annum, so this one ton per day plant could address most of the US's needs."

With an institutional investor, strategic government/industry partnerships, and a modular technology enabling phased capex and agile response to shifting critical mineral needs, MTM is well-positioned in the clean energy transition.

Sovereign Metals

Sovereign Metals holds the world's largest natural rutile and second largest flake graphite deposits at Kasiya in Malawi. Natural rutile is the purest titanium feedstock for pigments, aerospace, and other tech applications. Global rutile supply is decreasing as demand grows. Sovereign's rutile has significantly lower CO2 intensity than alternatives, helping to decarbonize titanium supply chains.

The Kasiya graphite is also low-carbon and provides non-China supply diversification for the booming lithium-ion battery market. An independent life cycle analysis estimated Sovereign's graphite produces just 0.2 tonnes of CO2 per tonne vs. 1.2 for Chinese natural graphite and 15-25 for synthetic graphite. This positions Sovereign to support decarbonization of the EV battery supply chain.

American Critical Minerals

American Critical Minerals is positioned to capitalize on both potash and lithium opportunities in Utah's Paradox Basin, one of eight global "Potash Super Basins" now also emerging as a major US lithium brine resource. The company secured Federal approval in late 2024 for its Green River Project exploration plans, one of only two companies in the Basin to hold such permits.

CEO Simon Clarke stated, "The company enters 2025 in excellent shape and well positioned to execute its plans to launch confirmation/brownfield drilling and publish maiden potash and lithium resources during 2025. The final months of 2024 were highly successful for the company."

Historic data and adjacent projects provide confidence for their initial 600Mt-1Bt potash target and lithium brine potential. In a tightening US critical mineral supply landscape, American Critical's permitted Utah project and experienced team make it a company to watch in 2025.

The Investment Thesis for Battery Metals

Investors considering entry into the battery metals market should evaluate the following factors:

- Supply and Demand Dynamics: Monitor production levels and demand forecasts to identify potential imbalances that could influence prices.

- Technological Advancements: Stay informed about innovations in battery technology that may affect the demand for specific metals.

- Regulatory Environment: Assess how government policies, such as environmental regulations and trade agreements, may impact mining operations and metal availability.

- Geopolitical Considerations: Be aware of geopolitical developments that could disrupt supply chains or alter market dynamics.

The battery metals market in 2025 presents a complex yet promising landscape for investors. While price volatility and economic uncertainties pose challenges, strategic investments and diversification efforts by major corporations underscore the sector's potential. By carefully analyzing market trends and external factors, investors can make informed decisions to navigate this evolving market successfully.

References:

- Reuters (January 2025). Lithium Prices To Stabilise In 2025 As Mine Closures, China EV Sales Ease Glut, Analysts Say

- Baskaran, Gracelin (June 2024). Drivers of Base Metals Price Volatility

- Financial Times (January 2025). Saudi Aramco To Expand Investments In Lithium As It Diversifies From Oil

- Straits Research (November 2024). Lithium-Ion Battery Metals Market Size, Growth to 2025 to 2033

Analyst's Notes

Subscribe to Our Channel

Stay Informed