Copper Super-Cycle: Strategic Investment Opportunity

Copper faces structural supply deficit as EV adoption, renewable energy, and AI drive unprecedented demand growth while new discoveries remain scarce in tier-one jurisdictions.

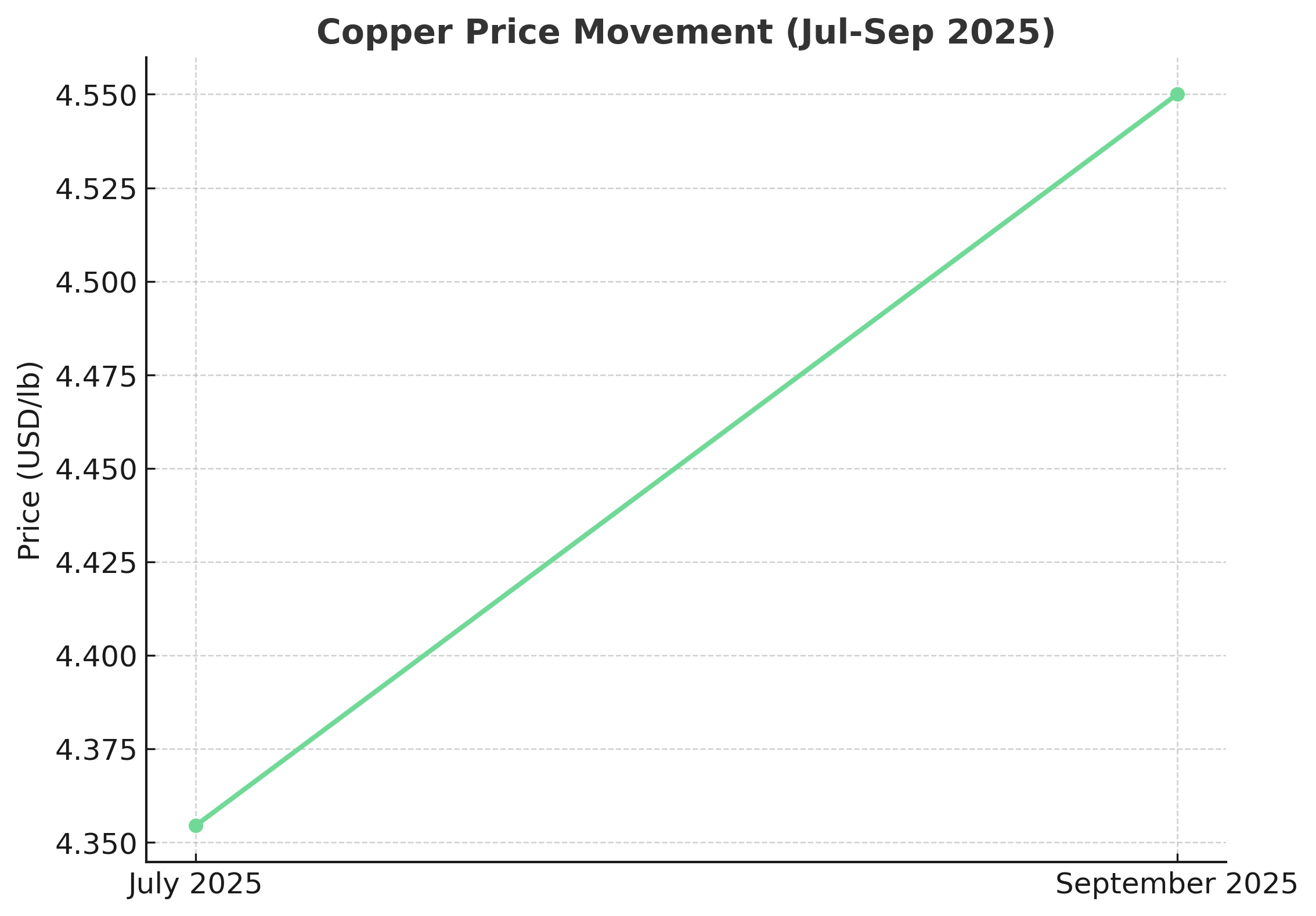

- Copper prices fell to $4.3545/lb in July 2025, down 14.3% month-over-month after copper cathodes were excluded from proposed tariffs, with current prices around $4.55/lb as of September 2025 and inclusion in the 2025 critical minerals list indicating policy support for the metal's strategic importance.

- Growing electrification, renewable energy deployment, and AI/5G infrastructure expansion are creating unprecedented copper demand, while global ore grades decline and exploration budgets remain constrained, setting up a structural supply deficit.

- Chile remains the world's premier copper jurisdiction, with projects like Marimaca's 900kt contained copper resource and Fitzroy's dual-discovery portfolio (Buen Retiro IOCG system and Caballos Cu-Mo-Au-Re) demonstrating the country's continued exploration upside.

- Mining majors are aggressively acquiring copper assets as development pipelines thin, creating significant optionality for advanced development projects with district-scale potential in tier-one jurisdictions.

- Projects utilizing seawater, renewable energy, and heap-leach processing (like Marimaca's 38% lower carbon intensity) are positioned to capture premium pricing as ESG requirements tighten across the copper supply chain.

The Investment Case for Copper: Why 2025-2026 Presents a Strategic Opportunity

Copper stands at an inflection point that hasn't been seen in decades. As the world accelerates toward electrification and renewable energy adoption, this red metal has emerged from commodity obscurity to become perhaps the most strategically important industrial material of the 21st century. The convergence of surging demand, constrained supply, and supportive policy frameworks has created what many analysts believe represents the most compelling investment opportunity in the copper space since the early 2000s super-cycle.

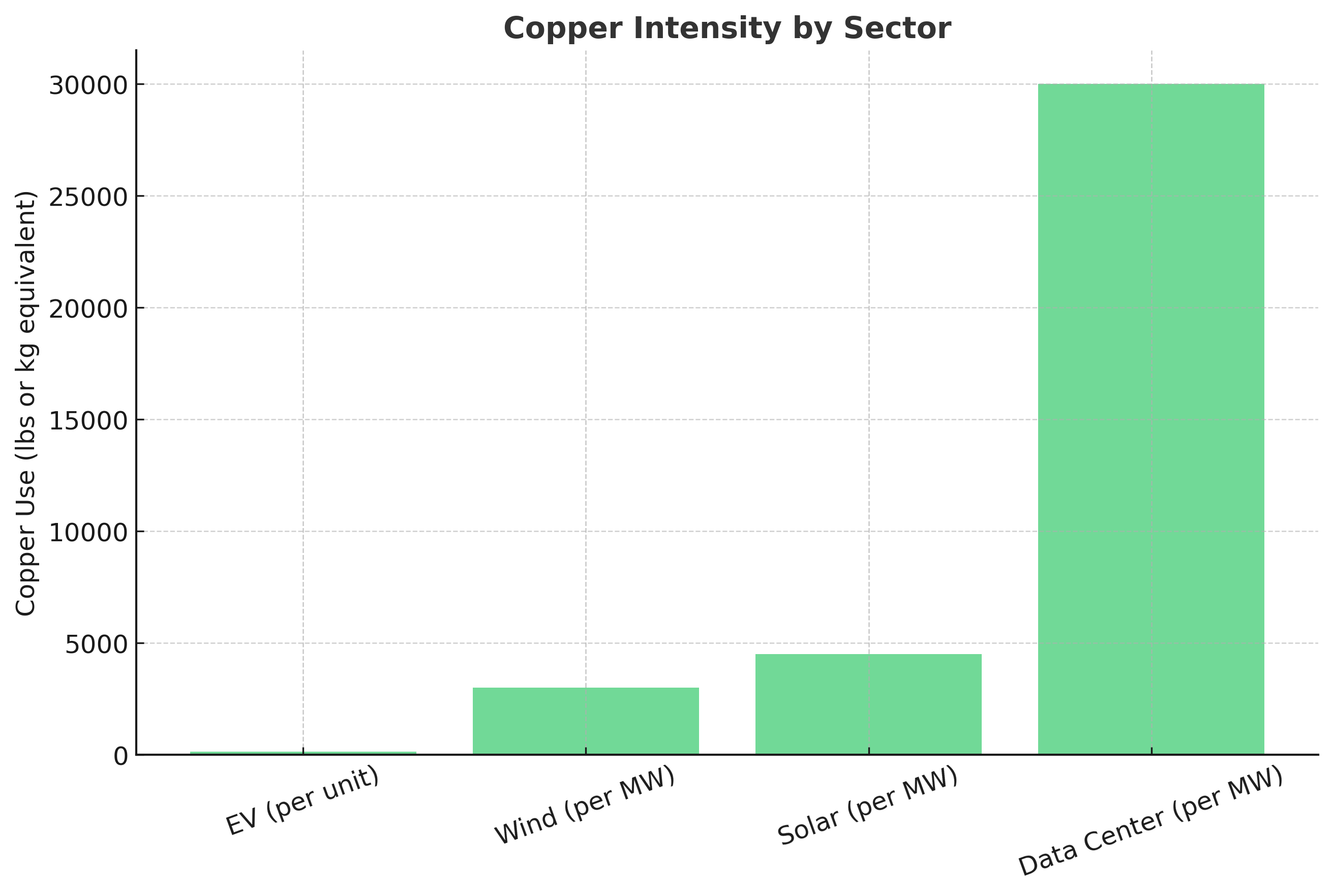

The fundamentals are clear: every electric vehicle requires approximately 132-183 pounds of copper compared to 48 pounds in internal combustion vehicles. A single 3-megawatt wind turbine contains about 9 tons of copper. The artificial intelligence revolution demands massive data center expansion, with each facility requiring 27-33 tons of copper per megawatt of applied power. Yet global copper discovery rates have plummeted, with no major new deposits found in recent years, while existing mines face declining grades and increasing operational challenges.

This supply-demand imbalance has caught the attention of governments worldwide. The U.S. government's recent decision to exclude copper cathodes from proposed tariffs and include copper in the 2025 critical minerals list signals recognition of the metal's strategic importance. As one industry executive noted, "We're not just looking at a cyclical upturn—this is a structural shift that could last decades."

Global Demand Drivers: The Electric Vehicle Revolution

The transportation sector's transformation represents perhaps the largest demand driver for copper in modern history. Electric vehicles require between 132-183 pounds of copper compared to 48 pounds in traditional vehicles, with the metal used in motors, batteries, charging infrastructure, and power electronics. Global EV adoption is accelerating rapidly, though exact future volumes remain subject to infrastructure development and policy support.

This exponential growth extends beyond individual vehicles to the supporting ecosystem. EV charging networks require extensive copper wiring, with charging infrastructure representing a significant source of copper demand as adoption scales globally.

Renewable Energy Infrastructure Expansion

Wind and solar installations have become copper-intensive endeavors. A typical wind turbine requires approximately 3 tons of copper per megawatt of installed capacity, while solar installations need 4-5.5 tons per megawatt. As governments worldwide commit to renewable energy targets, copper demand from this sector is projected to grow significantly throughout the decade.

Grid modernization compounds this demand. Smart grids, energy storage systems, and long-distance transmission lines all require substantial copper infrastructure, with renewable energy systems requiring 4-6 times more copper per installed megawatt than conventional power plants.

Artificial Intelligence and Data Center Growth

The AI revolution has created an unexpected but significant new source of copper demand. Data centers supporting AI workloads require approximately 27-33 tons of copper per megawatt of applied power, used in power distribution, cooling systems, and connectivity infrastructure. BHP estimates that copper demand from data centers could grow six-fold by 2050—from around half a million tonnes annually today to around 3 million tonnes by 2050.

This demand comes at a time when data center construction is accelerating globally, driven by AI adoption and cloud computing expansion, with each facility representing a substantial copper consumption event.

Supply Challenges: Declining Discovery Rates & Ore Grades

The copper mining industry faces a stark reality: discovery rates have collapsed while demand soars. No world-class copper deposits (>10 million tons contained copper) have been discovered since 2010, despite record exploration spending in recent years. Existing discoveries typically take 15-20 years to reach production, meaning today's supply constraints reflect exploration failures from decades past.

Compounding this challenge, average ore grades at major mines continue declining. Chile's massive Escondida mine, the world's largest copper producer, has seen grades fall from over 2% copper in the 1990s to approximately 0.5% today. This grade decline means mining companies must process exponentially more rock to produce the same amount of copper, increasing costs and environmental impact.

Geopolitical Concentration Risk

Copper supply remains heavily concentrated in politically sensitive regions. Chile and Peru account for approximately 40% of global production, while China dominates refined copper production and processing. The Democratic Republic of Congo, despite being primarily known for cobalt, also supplies significant copper volumes but faces ongoing political instability.

Recent supply disruptions have highlighted these concentration risks. Panama's Cobre Panama mine closure removed 300,000 tons of annual copper supply virtually overnight. Labor strikes at major Chilean operations regularly impact global prices, while Peru's political instability has delayed several major projects.

Capital Allocation Challenges

Mining companies have struggled to deploy capital effectively in copper projects. The industry's poor track record of cost overruns and schedule delays has made investors wary of funding new developments. Major projects like Oyu Tolgoi and Quebrada Blanca have faced multi-billion-dollar cost escalations, making boards increasingly cautious about approving new copper developments.

This capital discipline, while beneficial for existing shareholders, exacerbates supply constraints. Industry estimates suggest the sector needs substantial new investment over the next decade to meet projected demand, yet current investment levels remain constrained by risk management concerns.

Company Case Studies: Marimaca Copper Advanced Development in Chile

Advanced development companies with de-risked projects in tier-one jurisdictions represent perhaps the most compelling investment opportunity in today's market. Companies like Marimaca Copper exemplify this opportunity: located in Chile's established Antofagasta mining district, the company's Oxide Deposit contains 900,000 tons of contained copper in measured and indicated resources, with 86% of tonnage in the higher-confidence categories.

Marimaca's strategic advantages extend beyond resource size. The project benefits from existing infrastructure located just 25 kilometers from Mejillones Port and 40 kilometers from Antofagasta city dramatically reducing development costs and risks. The company has secured recycled seawater from Mejillones Bay, eliminating freshwater requirements and reducing environmental opposition.

The project's economics appear compelling even at current copper prices. Simple open-pit mining of near-surface oxides, combined with heap-leach processing, offers relatively low capital intensity compared to traditional sulfide projects. With the Definitive Feasibility Study expected in late 2025, Marimaca represents a near-term production opportunity in the world's premier copper jurisdiction.

"We are in the bottom decile of capital intensity for new copper projects globally, with a very competitive cost profile. Combine that with industry-leading returns — over $700 million NPV at $4.30 per pound copper and more than 30% IRR — and Marimaca stands out as a financeable, growth-ready project positioned to deliver meaningful new supply." — Hayden Locke, President & Chief Executive Officer of Marimaca Copper

Gladiator Metals: Exploration in Canada's Whitehorse Belt

For investors seeking higher-risk, higher-reward exposure, quality exploration companies in established mining districts offer significant leverage to copper price appreciation. Gladiator Metals, operating in Canada's Whitehorse Copper Belt, demonstrates this opportunity. The company's Cowley Park prospect has delivered intercepts including 98 meters at 1.49% copper, including 14 meters at 7.67% copper.

The Whitehorse Copper Belt's advantages extend beyond geological potential. Located in Yukon, Canada, the district offers road access, nearby hydroelectric power, and skilled local workforce none of the infrastructure challenges that plague many exploration projects. Historic production from the Little Chief mine totaled 8.54 million tons at over 1.5% copper and approximately 0.75 g/t gold, demonstrating the district's proven productivity.

Gladiator's recent discovery at the Valerie Trend, a 2.5-kilometer geophysical anomaly adjacent to Little Chief, suggests the potential for district-scale development. With an inferred resource estimate for Cowley Park targeted for the first half of 2026, the company offers both near-term catalysts and long-term district consolidation potential.

"For 25 years copper has gotten cheaper in real terms but that can't continue. Demand from AI, electrification and urbanization is rising just as deposits get deeper and permitting gets slower. That gap is the super-cycle." — Merlin Marr-Johnson, President & CEO, Fitzroy Minerals

Fitzroy Minerals: Multi-Asset Portfolio in Chile

Companies with diversified copper portfolios across multiple jurisdictions and development stages offer balanced exposure to the copper opportunity. Fitzroy Minerals exemplifies this strategy with two distinct projects in Chile: the Buen Retiro IOCG (Iron Oxide Copper Gold) system and the recently discovered Caballos Cu-Mo-Au-Re prospect.

Buen Retiro offers near-term development potential with surface oxide copper mineralization suitable for heap-leach processing. Located 60 kilometers from Copiapó and just 5 kilometers from highway and power infrastructure, the project benefits from excellent logistics. Historic drilling has delivered intercepts including 110 meters at 1.94% copper and 135 meters at 0.73% copper.

The Caballos discovery adds significant optionality with its multi-metal endowment. First drilling returned 200 meters at 0.46% copper, 591 ppm molybdenum, and 0.07 g/t gold (0.81% copper equivalent), including 42 meters at 1.20% copper, 1,764 ppm molybdenum, and 0.23 g/t gold (2.26% copper equivalent). Molybdenum's 4-5x copper payability provides substantial by-product credits, while rhenium and gold further enhance project economics.

"The long-term demand fundamentals are very strong. There's maybe some uncertainty about the short term, but structurally, this is a kind of market that you want to be long of in terms of copper." — Merlin Marr-Johnson, President & CEO, Fitzroy Minerals

Market Dynamics: Policy Support & Critical Minerals Status

Government recognition of copper's strategic importance has created unprecedented policy support. The U.S. inclusion of copper in the 2025 critical minerals list provides access to expedited permitting, tax incentives, and potential strategic stockpile purchases. Similar policies in Europe and other jurisdictions are creating demand floors and reducing regulatory risks for copper projects.

The tariff exclusion for copper cathodes in proposed U.S. trade measures demonstrates policymakers' understanding of copper's supply security importance. As noted in the CME Group's September 2025 analysis, this exclusion "dampens downside risk for refined copper in U.S. markets" while supporting continued investment in copper supply chains.

ESG Considerations Drive Premium Pricing

Environmental, Social, and Governance factors increasingly influence copper purchasing decisions. Projects utilizing seawater instead of freshwater, renewable energy sources, and lower-carbon processing methods command premium pricing from ESG-conscious end users.

Marimaca Copper's commitment to heap leaching with 38% lower carbon intensity compared to conventional processing positions the company advantageously in this evolving market. The project's use of recycled seawater and commitment to renewable power aligns with automotive and technology companies' supply chain requirements.

M&A Activity Signals Market Recognition

Mining majors' aggressive acquisition activity in copper reflects industry recognition of supply constraints. Recent transactions by Freeport-McMoRan, Teck Resources, BHP, and Mitsubishi demonstrate institutional appetite for copper assets. This M&A activity creates significant optionality for well-positioned development and exploration companies.

As one mining executive recently observed, "The majors are paying up for copper assets because they recognize the difficulty of organic growth. Quality projects in tier-one jurisdictions are becoming scarce commodities themselves."

The Investment Thesis for Copper

- Focus on companies with measured and indicated resources in established mining districts with existing infrastructure, targeting projects within 2-3 years of production decisions.

- Balance portfolios with 60% advanced development, 30% expansion-stage exploration, and 10% early-stage discovery plays to capture both near-term production and long-term discovery upside.

- Invest in projects utilizing seawater, renewable energy, and low-carbon processing methods, as these will command premium pricing as supply chain requirements tighten.

- Target companies with district-scale potential in consolidated ownership structures, as mining majors increasingly seek bolt-on acquisitions rather than greenfield development.

- Critical minerals status and trade policies increasingly influence copper market dynamics, creating both opportunities and risks that require active management.

- Use temporary price corrections to accumulate positions in quality assets, as structural demand growth supports higher long-term pricing.

Key Takeaways & Investment Implications

The copper investment opportunity extends beyond typical commodity cycles. The convergence of electrification, renewable energy deployment, and artificial intelligence infrastructure development has created structural demand growth that existing supply cannot meet. Companies with quality assets in tier-one jurisdictions, strong ESG credentials, and clear paths to production represent the most compelling opportunities in today's market.

For investors seeking exposure to the most critical commodity of the energy transition, copper offers unparalleled leverage to global decarbonization efforts. The question is not whether copper demand will grow—it's whether supply can keep pace. Current evidence suggests it cannot, creating exceptional opportunities for positioned investors.

TL;DR Summary

Copper faces a structural supply-demand imbalance driven by electrification, renewable energy expansion, and AI infrastructure growth. Electric vehicles require 132-183 pounds of copper versus 48 pounds for traditional cars, while wind turbines need 3 tons per megawatt and data centers require 27-33 tons per megawatt. However, no major copper discoveries have emerged since 2010, existing mines face declining grades, and development timelines stretch 15-20 years. Government recognition through critical minerals status and tariff policies provides support. Investment opportunities span development companies like Marimaca Copper (900kt contained copper in Chile), exploration plays like Gladiator Metals (Yukon's Whitehorse Belt), and diversified portfolios like Fitzroy Minerals (dual Chilean discoveries). ESG-compliant projects command premium pricing, while M&A activity signals institutional recognition of supply scarcity.

Copper's unique position stems from its essential role in electrification and renewable energy infrastructure. Unlike other metals with substitutes, copper's electrical conductivity properties make it irreplaceable in EVs, renewable energy systems, and data centers. The structural demand growth from these sectors, combined with declining discovery rates, creates a supply deficit scenario not seen in other industrial metals.

Focus on five key criteria: jurisdiction quality (political stability, mining-friendly policies), resource confidence (measured and indicated vs. inferred), infrastructure access (proximity to ports, power, roads), processing method (heap leach vs. flotation complexity), and management track record. Companies in Chile, Canada, and Australia with near-surface oxide deposits and existing infrastructure typically offer the best risk-adjusted returns.

Most new copper projects require sustained prices above $3.50-4.00/lb for economic viability, while marginal existing operations need $3.00-3.50/lb. However, project-specific factors like grade, processing method, and jurisdiction significantly impact breakeven prices. Heap-leach oxide projects typically have lower operating costs than sulfide flotation operations.

Portfolio allocation should depend on risk tolerance and investment timeline. Conservative investors should focus 70-80% on near-production developers with definitive feasibility studies, while growth-oriented investors might allocate 40-60% to quality exploration companies in proven districts. Diversification across development stages provides balanced exposure.

ESG considerations increasingly influence copper pricing, with projects using renewable energy, seawater instead of freshwater, and lower-carbon processing methods commanding premiums. Major technology and automotive companies require ESG-compliant supply chains, making these factors material to project economics rather than just regulatory requirements.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed