Copper’s Record-Breaking Rally: Structural Supply Deficits, Demand Anchors & the New Pricing Paradigm

US copper tariffs create 30% COMEX premium, driving supply realignment. Analysis of investment opportunities in Tier 1 jurisdictions amid structural deficits.

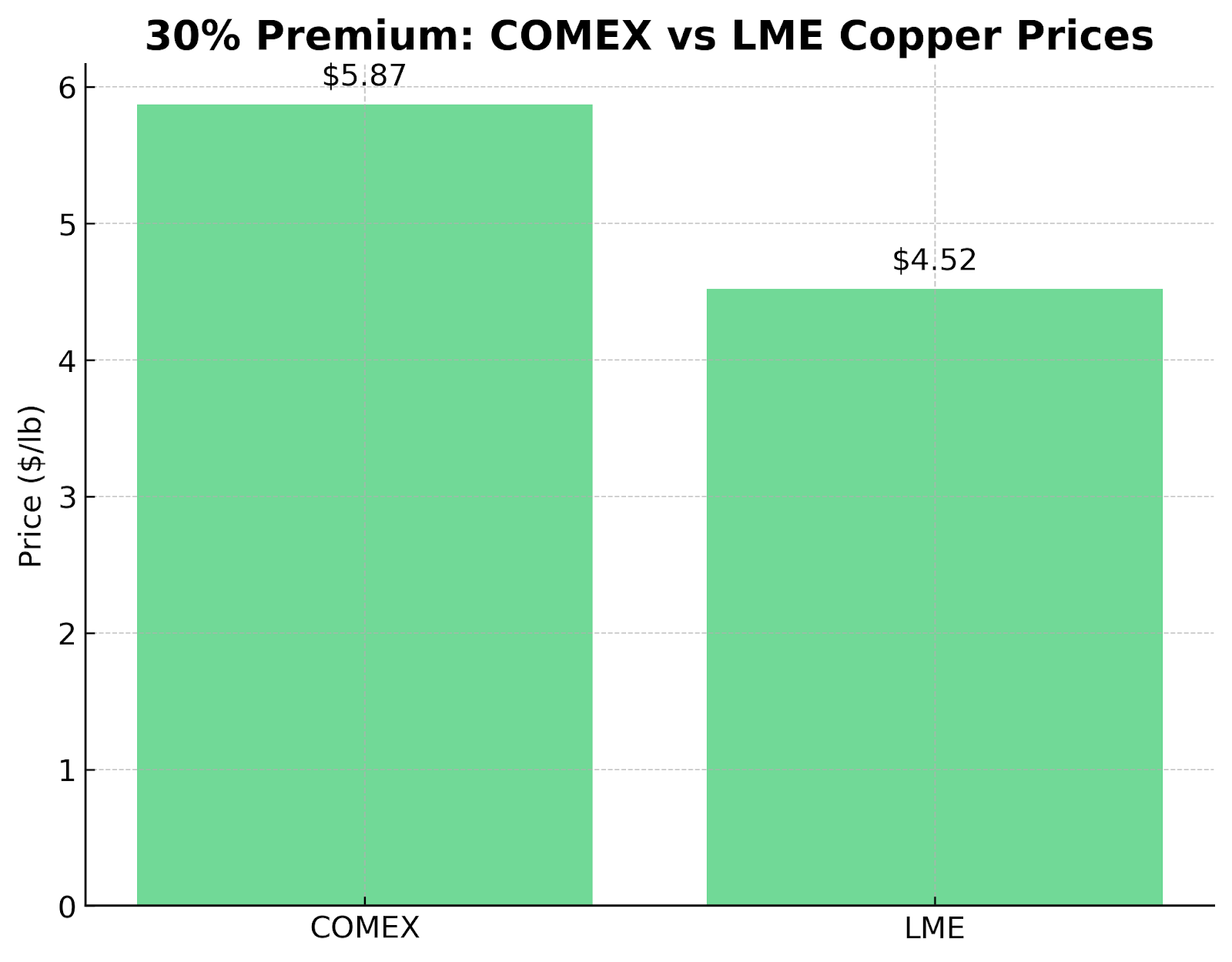

- US tariffs on refined copper have created a record 30% COMEX-LME premium, reshaping trade flows and investor positioning across $180 billion in global copper assets.

- Global copper demand remains anchored by China's infrastructure push and energy transition requirements projected to add 11.5 million tons of annual demand by 2030.

- Supply deficits are deepening with average ore grades declining 40% since 1990 while new project lead times extend to 16.3 years versus 12.3 years historically.

- Development-stage companies in Tier 1 jurisdictions are attracting premium valuations as institutional capital prioritizes political stability and ESG compliance over traditional tonnage metrics.

- Investment opportunities emerge for projects offering near-term production capability, strategic jurisdiction positioning, and multi-commodity exposure during copper's structural repricing.

A Historic Price Breakout Signals Copper's Strategic Asset Transition

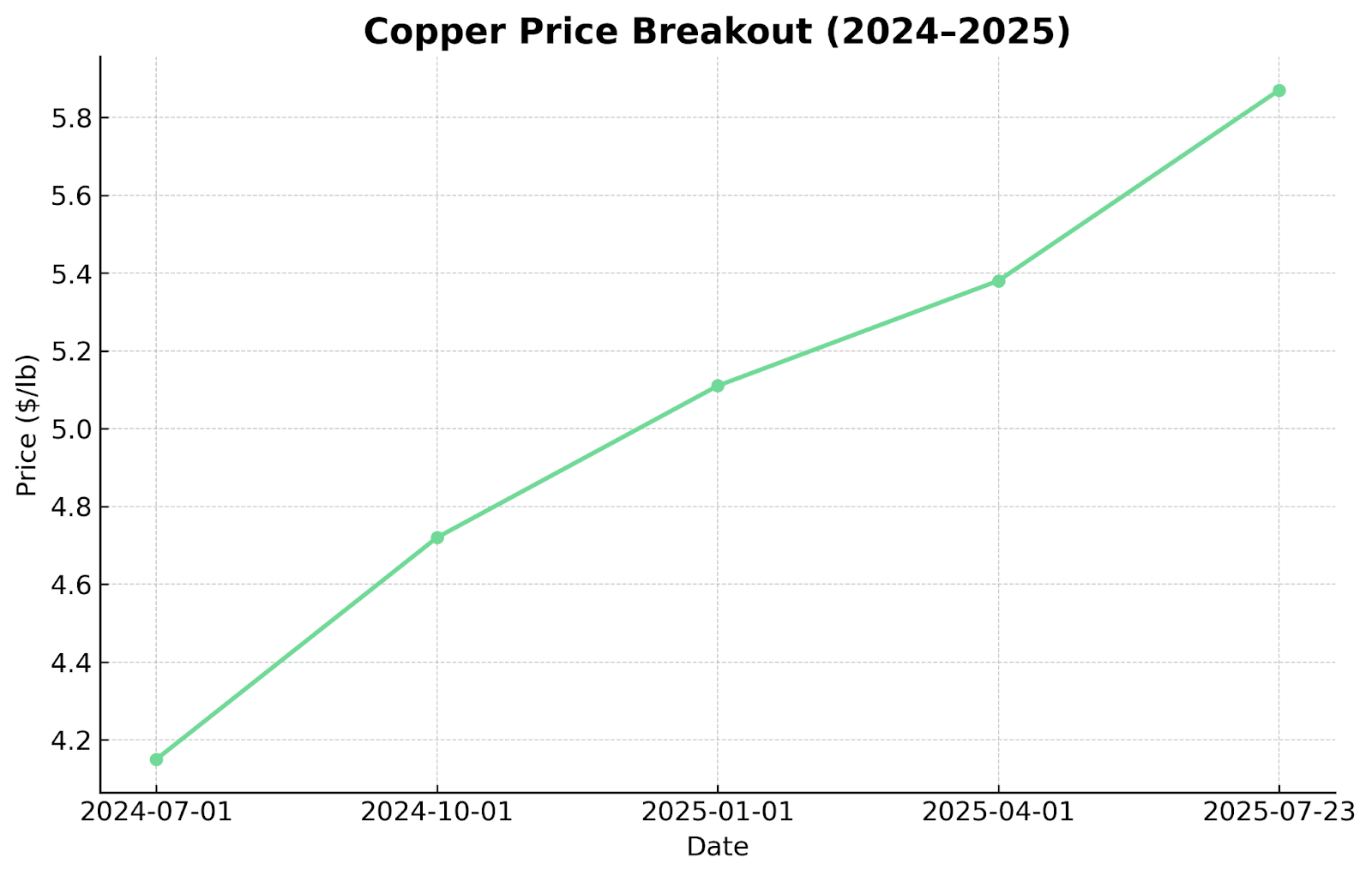

Copper reached $5.87 per pound on July 23, 2025, approaching the all-time high of $5.89/lb and signaling fundamental market structure changes beyond cyclical pricing dynamics. This milestone reflects the intersection of US trade policy intervention and accelerating electrification demand, creating investment opportunities that institutional capital is rapidly repricing.

The immediate catalyst stems from Washington's 50% import duty on refined copper, but underlying drivers include structural supply constraints and China's sustained infrastructure investment program. For portfolio managers focused on commodity exposure, this environment demands recalibration of traditional mining investment frameworks to incorporate geopolitical risk premiums and ESG compliance requirements.

The London Metal Exchange inventory stands at 135,000 tons—representing just 1.8 days of global consumption—while COMEX stockpiles remain near decade lows. This supply tightness, combined with tariff-induced market segmentation, has created pricing dislocations that sophisticated investors can exploit through strategic positioning in development-stage companies with advantageous jurisdiction and resource profiles.

Institutional mining specialists recognize this repricing reflects copper's evolution from cyclical industrial metal to strategic asset class. Goldman Sachs projects copper demand will reach 30 million tons annually by 2030, requiring $150 billion in new mine development investment. This capital requirement, coupled with extended permitting timelines, creates barriers to entry that favor companies with advanced development status and established regulatory pathways.

Policy Shock Creates Structural Market Segmentation

The 50% import duty has generated a sustained 30% premium between COMEX and LME pricing—unprecedented in modern commodity markets where arbitrage mechanisms typically maintain single-digit spreads. This dislocation has triggered immediate capital allocation shifts, with Chilean copper exports redirecting toward the United States to capture premium pricing while European and Asian buyers face supply constraints.

Analysis of trade flow data reveals 1.2 million tons of refined copper annually affected by the tariff structure, representing approximately 15% of globally traded material. The resulting market segmentation creates distinct pricing mechanisms across geographic regions, effectively establishing separate commodity markets with limited convergence capability.

For institutional investors, this segmentation presents both opportunity and complexity. Currency hedging requirements intensify as USD-denominated copper pricing diverges from local currency cost structures in major producing regions. Companies with USD revenue exposure and local currency operating costs benefit from this differential, while integrated producers face margin compression on non-US sales.

Refining Capacity Constraints Extend Premium Duration

United States domestic refining capacity totals 1.7 million tons annually against consumption of 2.2 million tons, creating a structural 500,000-ton deficit that tariff protection cannot immediately address. New smelting and refining facility development requires 36-month construction timelines, suggesting the COMEX premium could persist through 2027-2028.

This capacity constraint amplifies investment appeal for projects located in politically stable jurisdictions with established trade relationships. The Yukon territory exemplifies these advantages through regulatory predictability and proximity to North American infrastructure networks.

Chief Executive Officer Jason Bontempo of Gladiator Metals emphasizes operational advantages in Tier 1 jurisdictions:

"We're working along the western margin of the city. We have excellent highway and road access and trail access, excellent draw on labor resources, and being so close to the city, we can pretty much work all year round."

Institutional Capital Repositioning Toward Electrification Demand

China maintains copper import volumes averaging 4.8 million tons annually despite domestic economic headwinds, with infrastructure modernization and industrial capacity expansion providing sustained demand support. The National Development and Reform Commission's 14th Five-Year Plan allocates $1.4 trillion toward infrastructure investment, including grid expansion requiring copper intensity 40% above traditional applications.

Energy transition demand represents additional structural growth independent of cyclical economic factors. International Energy Agency projections indicate clean energy sectors will require 11.5 million tons of additional annual copper consumption by 2030, equivalent to establishing four new mines of Escondida's scale within the decade.

This demand profile creates investment premiums for projects demonstrating ESG alignment and sustainable production capabilities. Automotive and renewable energy procurement departments increasingly implement supplier sustainability requirements, creating pricing advantages for compliant producers.

Marimaca Copper's approach exemplifies this positioning through integrated sustainable production methods:

"Carbon intensity, heap leaching 38% less carbon intensive than traditional processing. Water – recycled seawater supply secured from the Bay of Mejillones. Power – certified renewable electricity supply available."

Demand Elasticity Analysis Supports Higher Price Floors

Copper's price elasticity of demand measures approximately -0.15 in industrial applications, indicating consumption remains relatively stable despite price increases. This inelastic demand characteristic, combined with substitution constraints in electrical applications, supports higher equilibrium pricing as supply tightness persists.

Electric vehicle copper content averages 83 kilograms per unit versus 23 kilograms for internal combustion engines, while renewable energy generation requires 4-5 times the copper intensity of conventional power plants. These application-specific requirements create demand floors independent of economic cycles, supporting sustained pricing above historical averages.

Supply Deficit Analysis Reveals Investment Opportunity

Global average copper ore grades have deteriorated from 1.6% in 1990 to 0.9% currently, requiring increased energy inputs and processing complexity to maintain equivalent metal production. This grade decline, combined with rising energy costs, has elevated all-in sustaining costs (AISC) across the industry to approximately $3.20 per pound from sub-$2.00 levels in the previous decade.

New project economics require copper prices above $4.00 per pound to achieve 15% internal rates of return, establishing a structural cost floor significantly above historical averages. This cost inflation creates competitive advantages for high-grade deposits that can achieve superior economics even in volatile pricing environments.

Development timeline extension compounds supply constraints, with new projects now requiring average 16.3 years from discovery to production versus 12.3 years in 2005. Environmental assessment processes, community engagement requirements, and permitting complexity contribute to timeline inflation while increasing capital requirements.

Exploration Investment Deficit Creates Pipeline Constraints

Industry exploration budgets remain at $2.8 billion annually—approximately 28% of 2011 peak levels despite sustained high copper prices. Major mining companies have redirected capital toward brownfield expansion and acquisition strategies rather than grassroots exploration, creating a discovery pipeline deficit that will constrain future supply additions.

This exploration underinvestment cycle typically requires 5-7 years to reverse as increased budgets translate to discoveries and eventual resource development. Current supply tightness therefore reflects exploration decisions made during 2015-2019 when copper averaged below $3.00 per pound, suggesting sustained deficit conditions through the decade.

Early-stage exploration companies with systematic drilling programs in proven geological terranes offer institutional investors leverage to this discovery deficit. Chief Operating Officer, and Country Manager Gilberto Schubert of Fitzroy Minerals demonstrates this approach:

"At the beginning of this year we did our proof of concept drilling in the area. We got 200 meters with copper, molybdenum and gold, pure sulfides mineralization."

Jurisdictional Risk Premium Reshapes Valuation Metrics

The European Union's Critical Raw Materials Act designates copper as strategically important, providing preferential permitting treatment and potential financial support for domestic supply development. This policy framework reduces regulatory risk while accelerating development timelines for qualifying projects within member states.

Spain's Iberian Pyrite Belt benefits directly from this supportive policy environment, offering both geological prospectivity and regulatory advantages for copper development. The region's established mining infrastructure and skilled workforce provide additional operational benefits for institutional investors seeking de-risked exposure.

Chief Executive Officer Tim Moody of Pan Global Resources emphasizes these jurisdictional advantages:

"The infrastructure, the location, the advantage that we have there, I think it doesn't get any better than where we're situated. It's a great permitting environment. The European Critical Raw Materials Act recognizing copper bodes well for Spain."

Canadian Mining Framework Attracts Institutional Capital

Canadian provinces maintain established regulatory frameworks with transparent permitting processes and predictable timelines that reduce development risk for institutional investors. Mining represents significant economic activity in territories like Yukon, creating political support for responsible resource development.

Flow-through share tax advantages provide additional investment incentives for Canadian exploration companies, enabling retail and institutional investors to claim exploration expenditures as tax deductions. This structure has attracted approximately $1.8 billion in annual investment capital toward Canadian mining projects.

The combination of political stability, regulatory transparency, and tax advantages creates premium valuations for Canadian development projects relative to comparable resources in higher-risk jurisdictions. This premium typically ranges from 15-25% based on comparable project analysis.

Strategic Company Analysis: Positioning for Copper's Structural Shift

Gladiator Metals: Consolidating Strategic Canadian Resource Base

- Market capitalization: CAD $42 million (as of August 2025)

- Target resource: 100+ million tons at >1% copper excluding credits

- 2025 drilling program: 30,000 meters across Whitehorse Copper Belt

- Expected maiden resource: Q1 2026

Gladiator Metals has consolidated control over a 35-kilometer copper belt in Yukon through systematic land acquisition, creating a district-scale opportunity with year-round operational capability. The company's resource target of over 100 million tons at above 1% copper positions the project for institutional investment consideration requiring minimum 50 million ton resources.

The Yukon location provides multiple advantages including political stability, established infrastructure access, and favorable mining tax regime. Provincial mining taxes range from 1-3% of net revenue compared to 20%+ royalty rates in some international jurisdictions, improving project economics and investor returns.

Management has established community engagement protocols with First Nations groups, including a capacity funding agreement with Kwanlin Dün First Nation representing initial steps toward social license achievement. This proactive approach reduces permitting risk while demonstrating ESG commitment to institutional investors.

Pan Global Resources: European Critical Mineral Strategy Beneficiary

- Market capitalization: CAD $31 million (as of August 2025)

- Resource target: 100 million tons containing 400,000 tons copper

- La Romana trend: Extended to 1.7 kilometers with high-grade continuity

- Maiden NI 43-101 resource estimate: Expected Q2 2026

Pan Global Resources operates within Spain's Iberian Pyrite Belt, benefiting from European Union critical materials policy support and established regional mining infrastructure. The company's systematic exploration approach across multiple targets demonstrates technical competence while building resource inventory for potential institutional investment.

Recent exploration success at Carmenes Project has identified bulk-tonnage gold potential alongside copper mineralization, providing multi-commodity exposure that reduces commodity price risk. The discovery of 110 meters of continuous gold mineralization suggests district-scale potential beyond the primary copper focus.

The company's resource target of 100 million tons containing 400,000 tons of copper would establish scale necessary for institutional consideration, while the Spanish jurisdiction provides regulatory predictability and ESG compliance advantages valued by European institutional investors.

Marimaca Copper: Integrated Development & Exploration Strategy

- Market capitalization: CAD $456 million (as of May 9, 2025)

- MOD project: Definitive feasibility study completion imminent

- Pampa Medina potential: 1.4km x 1.2km mineralized system

- Production target: 2026 for MOD project

Marimaca Copper pursues a dual-track strategy combining near-term production through the MOD project with district-scale exploration at Pampa Medina. This approach provides institutional investors with both immediate cash flow exposure and exploration upside within a single investment vehicle.

The MOD project's emphasis on sustainable production methods, including 38% lower carbon intensity through heap leaching, positions the company favorably for ESG-focused institutional mandates. Certified renewable electricity supply and recycled seawater utilization further enhance sustainability credentials.

Recent exploration results at Pampa Medina have identified exceptional high-grade mineralization including 6 meters at 12% copper within broader zones exceeding 20 meters at above 5% copper. This discovery suggests potential for a second production center leveraging existing MOD infrastructure.

Chief Executive Officer Hayden Locke outlines the integrated development approach:

"Our number one focus is on getting that into production. Any sulfide project that is discovered of any scale at Pampa Medina is likely to benefit from piggybacking off the infrastructure of an already constructed project at the MOD."

Fitzroy Minerals: Multi-Commodity Chile Exposure

- Market capitalization: CAD $18 million (as of August 2025)

- Buen Retiro: Near-surface oxide mineralization with 800+ meter trend

- Caballos: Copper-molybdenum-gold-rhenium porphyry system

- Mineralization open along ~4 km of identified strike, with recent drilling confirming an 800+ meter continuous trend"

Fitzroy Minerals offers institutional investors leveraged exposure to Chile's mineral endowment through a portfolio combining near-term production potential with longer-term development opportunities. The company's focus on Chile's coastal range aligns with industry exploration trends toward less explored geological terranes.

The Buen Retiro project demonstrates fast-track production potential through oxide mineralization amenable to solution extraction. Metallurgical testing has confirmed effective recovery using chloride leaching, while near-surface mineralization reduces capital expenditure requirements relative to underground development.

Multi-commodity exposure through molybdenum, gold, and rhenium provides portfolio diversification benefits during copper price volatility. Rhenium represents particularly strategic value as Chile produces 50-60% of global supply, with industrial applications in aerospace and petroleum refining commanding premium pricing.

The Pucobre clawback arrangement provides additional strategic value through potential partnership with an established Chilean copper producer, offering development capital and operational expertise while maintaining exploration upside for Fitzroy shareholders.

Risk Assessment & Portfolio Positioning Considerations

US copper tariff policy faces potential retaliation from trading partners, creating uncertainty around premium duration and market segmentation sustainability. Portfolio managers should consider exposure diversification across multiple jurisdictions to mitigate policy reversal risk.

Currency exposure represents additional complexity as USD strength relative to local operating currencies creates margin compression for international producers. Companies with USD-denominated revenue streams and local currency cost structures benefit from this differential, while integrated producers face mixed impacts.

ESG Compliance Requirements Intensify

Institutional investment mandates increasingly incorporate ESG screening criteria that eliminate projects lacking comprehensive environmental impact assessments or community engagement programs. This trend creates competitive advantages for companies demonstrating proactive ESG integration while reducing available investment universe for institutional capital.

Water usage, carbon emissions, and community impact metrics are becoming quantified requirements rather than qualitative considerations. Projects demonstrating measurable ESG performance improvements command valuation premiums while those lacking documentation face institutional capital constraints.

The Investment Thesis for Copper

- Tariff-induced structural premiums create sustained arbitrage opportunities for projects positioned to serve protected markets through favorable trade relationships and strategic jurisdiction positioning.

- Electrification demand growth provides non-cyclical revenue exposure independent of traditional economic cycles, supporting sustained pricing floors above $4.00 per pound required for new project development.

- Supply deficit conditions persist through 2030 as declining ore grades and extended development timelines constrain new supply additions while demand grows 3-4% annually.

- Tier 1 jurisdictional positioning commands 15-25% valuation premiums as institutional investors prioritize political stability and regulatory predictability over traditional resource tonnage metrics.

- Development-stage companies with high-grade resources and established community relationships possess competitive advantages in environments where permitting complexity and social license requirements create barriers to entry.

- ESG-aligned production methods generate pricing premiums of 5-10% as automotive and renewable energy procurement departments implement sustainability-focused sourcing strategies with quantified compliance requirements.

- Multi-commodity exposure provides portfolio diversification benefits during copper price volatility while capturing value from strategic by-products like molybdenum, gold, and rhenium.

- Near-term production capability offers immediate cash flow exposure to current elevated pricing while maintaining exploration upside through district-scale resource potential.

Copper's structural repricing creates compelling investment opportunities for institutions willing to embrace development-stage exposure within disciplined risk management frameworks. The combination of supply constraints, demand growth, and jurisdictional risk premiums supports sustained higher pricing while creating barriers to entry that favor established development companies.

Portfolio construction should emphasize geographic diversification across Tier 1 jurisdictions while maintaining exposure to both near-term production and longer-term exploration upside. Companies demonstrating ESG compliance, community engagement, and technical execution capability offer superior risk-adjusted returns in this environment.

The current market dislocation presents tactical opportunities for institutions to establish positions in quality development companies before broader institutional recognition drives premium valuations. As copper completes its transition from cyclical metal to strategic asset class, early positioning in well-managed development companies with advantageous resource and jurisdiction profiles offers compelling risk-adjusted return potential for sophisticated mining investors.

Analyst's Notes

Subscribe to Our Channel

Stay Informed